GIS - General Mills: 2023 Pullback Provides Compelling Opportunity

2023-12-06 01:34:28 ET

Summary

- General Mills shares are undervalued with a low price-to-earnings ratio compared to historical and industry averages.

- GIS has a strong portfolio of consumer packaged food brands and dominates multiple food categories.

- The company presents a secure investment opportunity with steady growth, international expansion, and a focus on healthier options.

- An estimated 13x Risk:Reward over the NTM should not be overlooked when analyzing GIS.

Investment Thesis

Shares of General Mills ( GIS ) appear undervalued at present, having declined nearly 22% as of December 4th. This translates to a current price-to-earnings ratio of just 14x, significantly lower than both its historical average and the industry average of 17x.

GIS arguably boasts one of the most impressive consumer packaged food brand portfolios in the market. With 46 brands under its belt, the company holds a major position in multiple food categories, including cereal, dessert and baking mixes, savory and salty snacks, ice cream, frozen pizza and pizza snacks, nutrition bars, and much more. Within these categories, they dominate the market with their household names, including Bisquick, Cheerios, Chex Mix, Cocoa Puffs, Lucky Charms, Cinnamon Toast Crunch, Fruit Roll-Ups, Häagen-Dazs, Nature Valley, Old El Paso, Pillsbury, and many others.

GIS Household Brand Names (Google)

{kind=link}

General Mills presents a secure investment opportunity for investors. The stock has been penalized along with the rest of the industry due to concerns that obesity/diabetes pills will diminish consumer demand. However, I believe these fears are already embedded in the stock price and, in fact, are priced unfairly high.

Consumers will continue to consume and utilize their products, possibly just in smaller quantities. General Mills is also making commendable strides in developing healthier options for their customers.

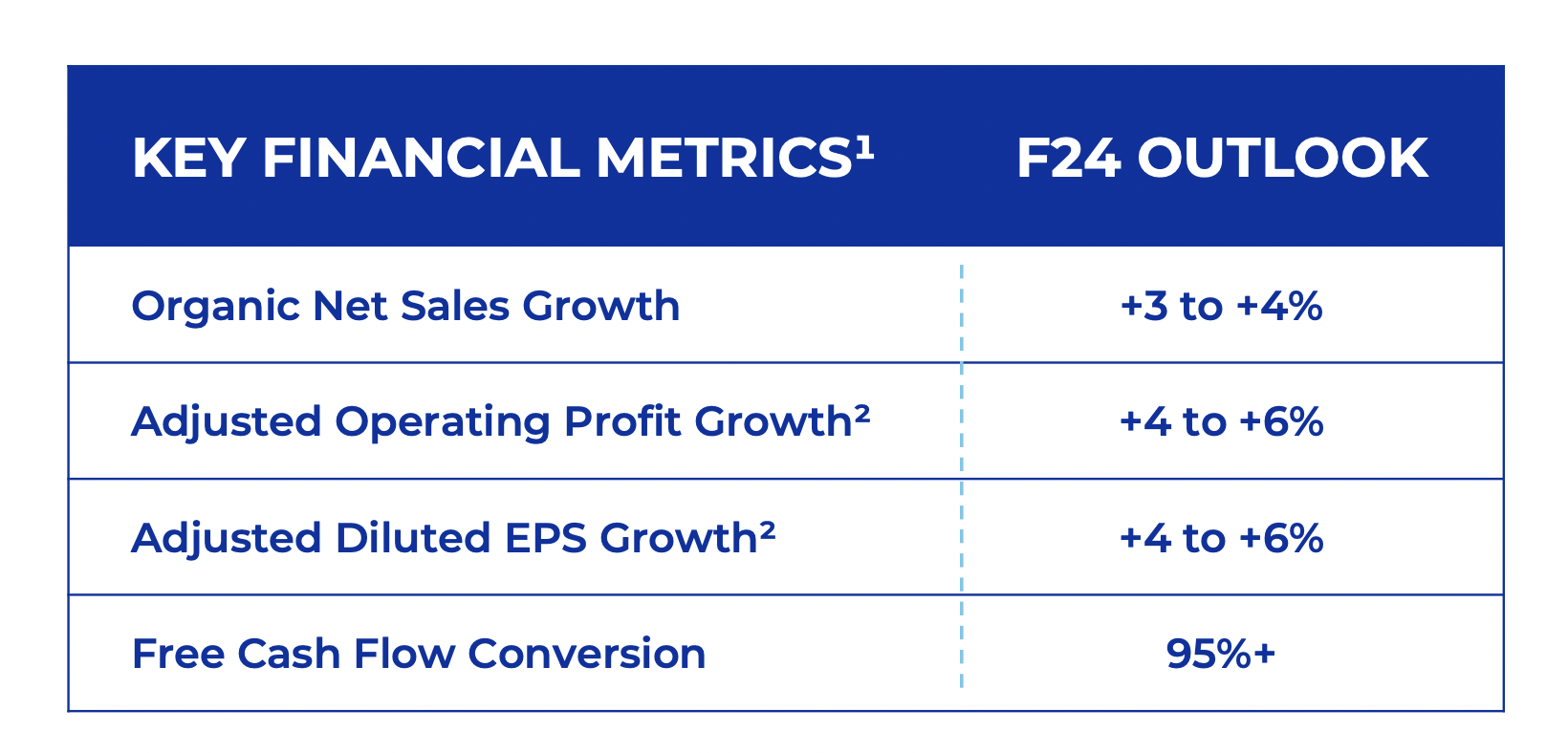

Management reaffirmed fiscal year (FY) guidance in Q1, and we will receive Q2 results in two weeks on the 20th. I anticipate strong earnings, with the stock rallying ahead of earnings and experiencing little reaction afterward (Buy the news, sell the hype).

GIS FY Guidance (General Mills Investor Relations)

{kind=link}

General Mills anticipates steady single-digit growth, with international expansion serving as a key driver. In Q1, international sales grew by 9%, outperforming the overall organic growth rate of 4%.

Management prioritizes driving growth while maintaining operational efficiency and optimizing its supply chain. They have effectively passed price increases to consumers, demonstrating the strong pricing power of their brands. Higher input costs have resulted in higher prices for customers, allowing GIS to safeguard and even increase its earnings.

Recent years have showcased the strength of General Mills' products and portfolio, and I believe they will continue to dominate grocery and convenience store aisles.

Management's focus on capital allocation and operational efficiency leads me to believe that the 2023 pullback presents an opportune entry point for long-term investors.

Fundamentals

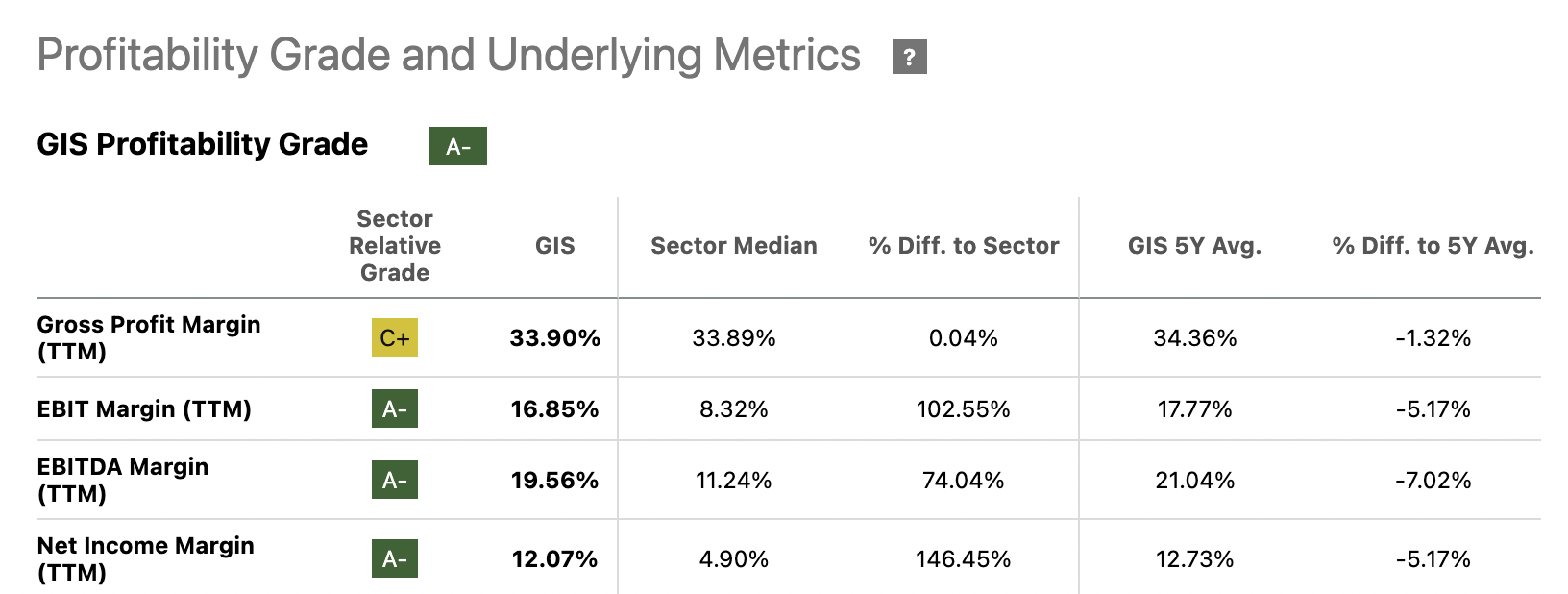

General Mills boasts impressive cash flow and margins in an industry not known for high profitability. GIS currently generates over $2 billion in annual free cash flow, translating to a strong 5.37% FCF yield. This yield surpasses its competitor, Mondelez ( MDLZ ), whom I also favor , and other consumer staple companies.

While margins have contracted across the industry, General Mills has weathered this trend relatively unscathed. Their gross margins remain comparable to the industry average, but their true differentiator lies in their bottom line. GIS currently boasts operating margins of 16.8% compared to the industry average of 8.3%, and its net income margin sits at 12% versus the industry average of 4.9%.

GIS Profitability Margins (Seeking Alpha)

{kind=link}

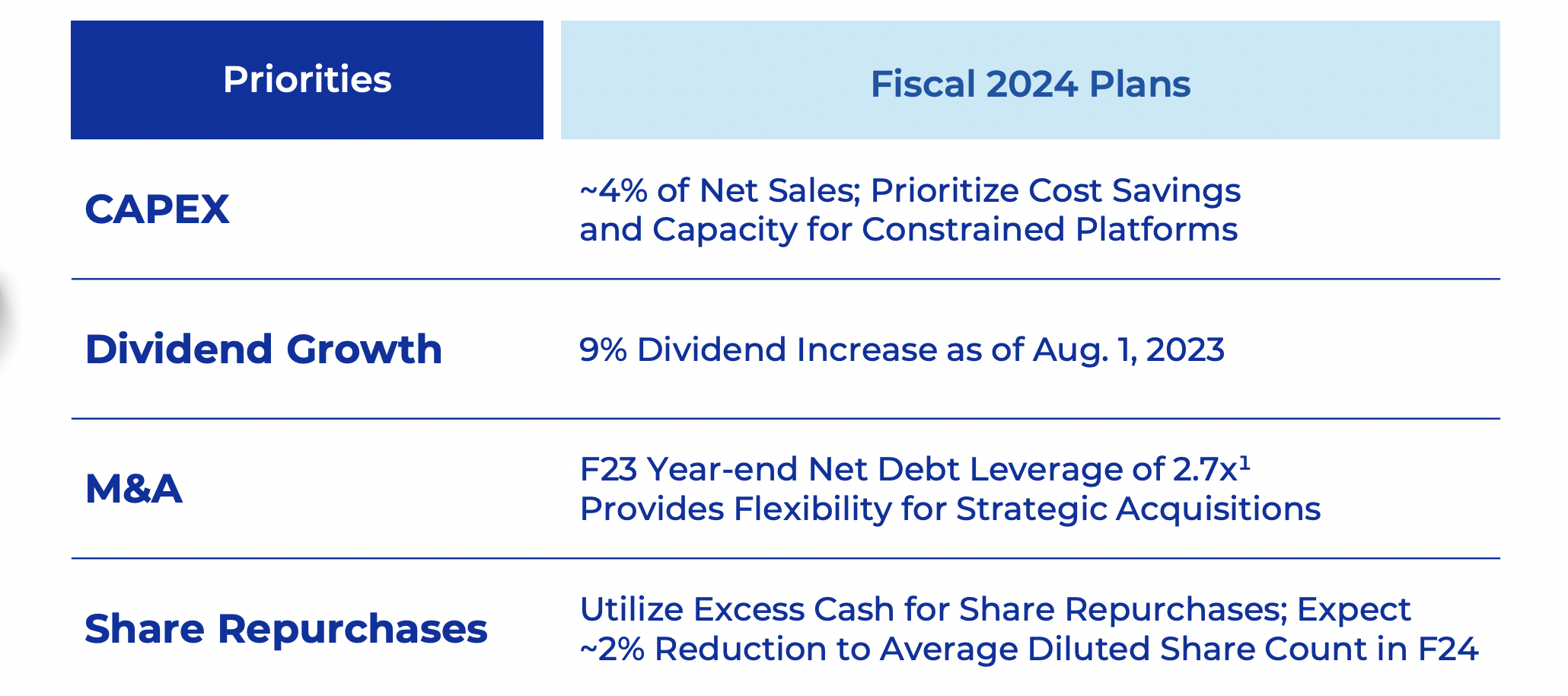

General Mills' higher margins and steady cash flow allow them to strategically allocate capital across various initiatives:

1. Dividends:

- Respectable Yield: GIS offers a currently attractive 3.6% dividend yield, amounting to $2.36 per share.

- Sustainable Payouts: A comfortable 52% payout ratio indicates room for continued dividend increases in the future.

- Proven Track Record: Despite COVID's impact on cash flow, the company has maintained a consistent dividend payout for over 50 years and recently increased it for four consecutive years.

2. Debt Reduction:

- Significant Progress: GIS has significantly reduced its total debt, which now stands at $12.28 billion, down from its peak of $15.8 billion.

- Strong Commitment: The company has diligently paid off $3.5 billion in debt over the past five years.

- Manageable Leverage: With a Net debt Leverage ratio of 2.7x, GIS maintains a healthy financial position.

3. Share Repurchases:

- Long-Term Strategy: In the past ten years, GIS has strategically reduced its outstanding shares by 8.35%.

- Temporary Dilution: While the company diluted shareholder ownership between 2018 and 2019 due to the lasting effects of bad timing and the COVID pandemic, requiring additional capital, it has since resumed its share repurchase program.

- Sustainable Future: GIS expects to continue reducing its share count by 2% annually.

4. Strategic Mergers & Acquisitions:

- Active Acquisitions: Throughout its history, GIS has acquired 21 companies, including 4 in the last five years alone.

- Transformative Deal: The largest acquisition in company history was the purchase of Pillsbury in 2000 for $10.5 billion.

GIS Capital Allocation Discipline (General Mills Investor relations)

{kind=link}

In the long term, GIS presents a compelling opportunity for value investors. Their robust product portfolio ensures sustainable cash flow and dividend growth. Their expertise in advertising and marketing positions them to leverage acquisitions as powerful growth catalysts.

GIS boasts a rich history spanning decades, demonstrating its resilience and longevity. While consumer preferences may evolve, the demand for snacks and breakfast options remains constant, ensuring continued relevance.

Don't let the fear-mongering surrounding new obesity drugs deter your investment in GIS. When others succumb to fear, we, as investors, seize the opportunity to be greedy.

Let's explore the true bargain that GIS represents.

Valuation & Price Targets

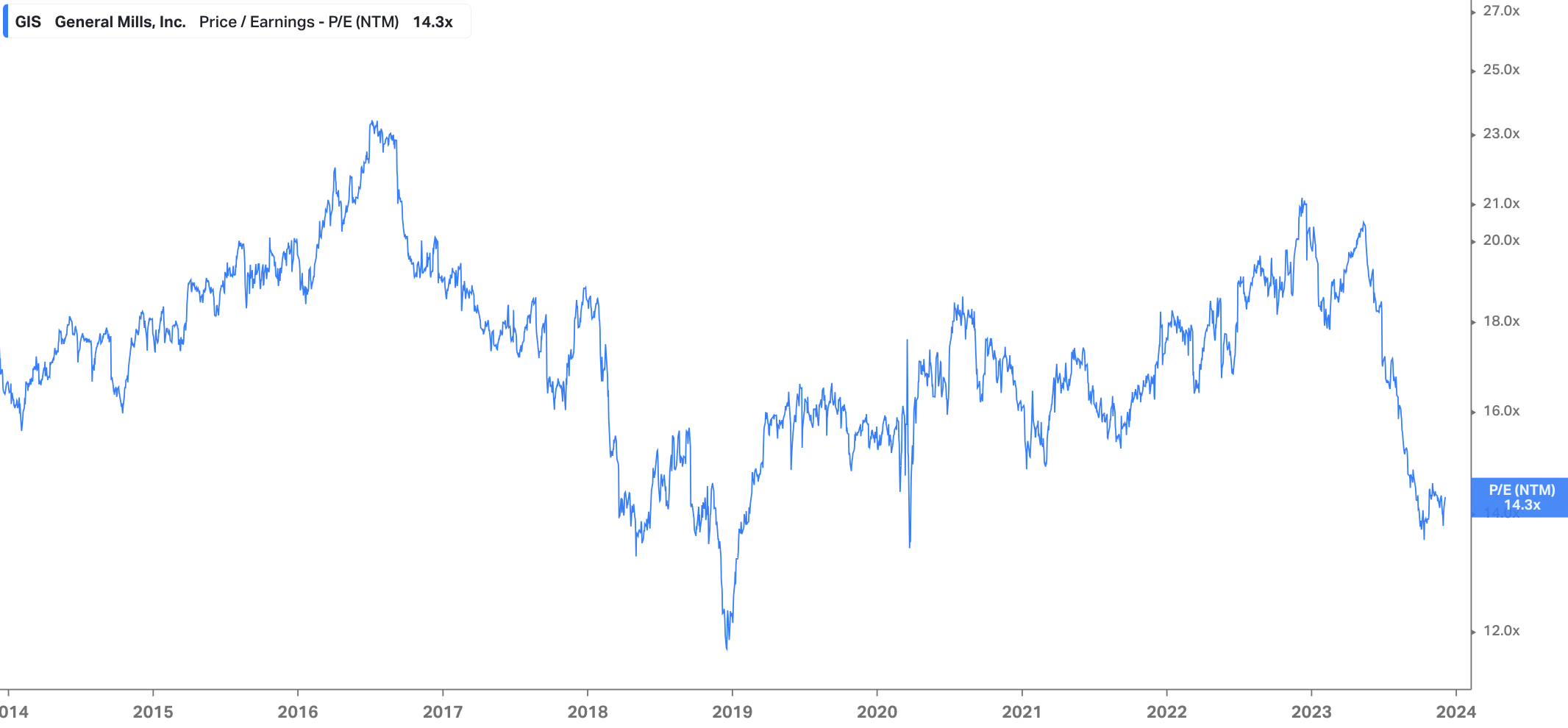

General Mills' current forward price-to-earnings (P/E) ratio of 14.3x stands well below both the industry average of 17.6x and its own 5-year average of 16.9x. This indicates that the stock is currently undervalued, especially for a leading player in the industry. Notably, competitors like Hershey ( HSY ) and Mondelez trade at 20x earnings despite similar cash flow and margin profiles.

Historically, GIS's P/E ratio has dipped below 14.3x on a few occasions over the past decade. However, the stock has typically rebounded once the P/E reached the 13x-14x range. We may be witnessing a similar scenario unfold right now.

Based on this historical pattern, a multiple expansion back to the 17x P/E level would translate to a potential stock price of $76 per share, representing a 16% upside.

{kind=link}

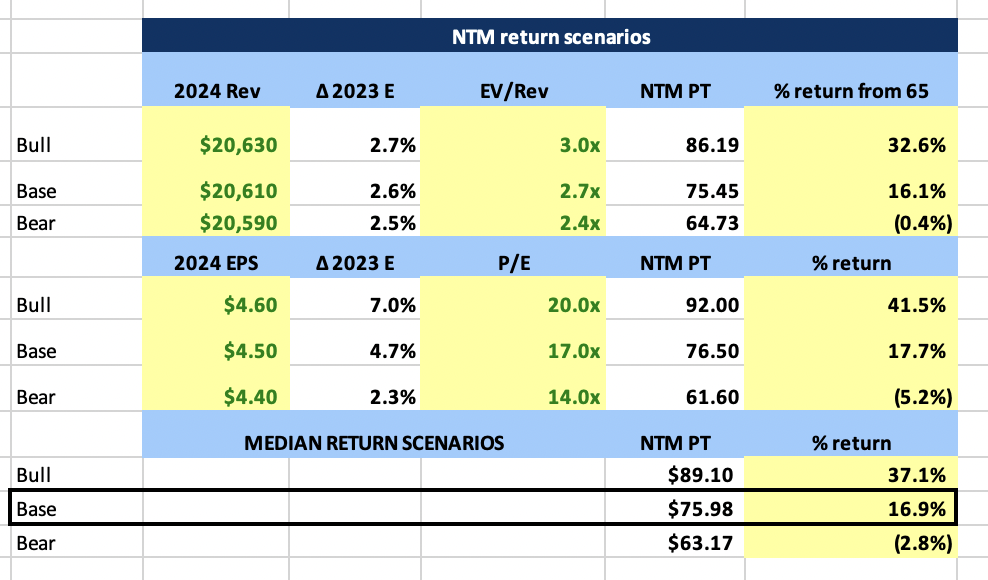

Leveraging historical valuations, analyst earnings estimates, and current financial data (such as cash and debt), I can create a comprehensive next twelve-month price target scenario table with bull, base, and bear case perspectives.

GIS NTM Price Target Scenarios (Author Calculations Based on Analyst Estimates From Data on Koyfin)

{kind=link}

For General Mills, the potential downside appears largely priced in. The stock has dropped from its all-time high of $90 per share in May 2023 to its current mid-60s price range. This presents an attractive 13x risk-reward ratio, leading me to consider it a top-hot pick for a bounce-back in 2024.

The market has exhibited excessive concentration in tech, while other sectors like staples, utilities, REITs, and healthcare have been disproportionately impacted. I believe that the market rally in 2024 will broaden, allowing GIS to regain its lost ground this year.

Therefore, I advise against selling GIS at a loss at this point. Instead, I recommend that investors consider buying General Mills while it remains seemingly undervalued.

Risk

The primary risk associated with investing in food producers like General Mills is their exposure to commodity prices and subsequent inflationary pressures. When inflation rises, increasing the cost of input materials, General Mills' earnings typically experience a temporary stall or contraction.

This often leads to decreased sales volume, countered by price increases to maintain margins. This phenomenon is currently observable across the industry, particularly when compared to snack rival PepsiCo (PEP).

While all consumer staple food and beverage producers face this risk, it's crucial to identify those who manage it most effectively and whose products hold the strongest shelf presence. Consumers are less likely to abandon certain "comfort food" staples, and these are the companies I favor.

Consumer preferences are constantly evolving, but that doesn't negate the enduring appeal of comfort foods. General Mills boasts over 46 brands, each offering a diverse range of products.

Though consumers may not be aware of it, General Mills products are deeply ingrained in everyday life and grocery shopping routines. This widespread presence is one of the reasons I favor GIS, as the potential reward outweighs the risks at current prices.

Conclusion

I have reached some key conclusions: concerns surrounding diabetes GLP drugs have caused General Mills and the broader snack, food, and beverage industry to suffer due to fears of declining demand.

However, I believe that demand will not simply vanish or contract by 50%. Instead, I anticipate that GIS and the industry will adapt by developing healthier snack options, diverse meal choices, and easier-to-prepare meals. General Mills is well-positioned to thrive in this evolving landscape.

They already possess strong brand recognition and loyalty through their unique product offerings. I'd wager that venturing into any household pantry or freezer would reveal at least one of General Mills' cereals, some pizza rolls, a Pillsbury treat, or one of their countless other products.

Therefore, I believe that now presents a compelling opportunity to invest in General Mills.

Editor's Note: This article was submitted as part of Seeking Alpha's Top 2024 Long/Short Pick investment competition , which runs through December 31. With cash prizes, this competition -- open to all contributors -- is one you don't want to miss. If you are interested in becoming a contributor and taking part in the competition, click here to find out more and submit your article today!

For further details see:

General Mills: 2023 Pullback Provides Compelling Opportunity