GIS - General Mills: A Dividend Diamond In The Rough

2023-07-31 17:37:26 ET

Summary

- General Mills has shown inconsistent performance with steep rallies and sell-offs, leading to underperformance compared to peers.

- The company's 3.1% yield sits between a dividend growth and high-yield stock, making it less appealing to investors.

- Despite challenges like inflation, General Mills is making progress in improving its business through brand updates, margin improvement, and dividend hikes.

Introduction

It's time to talk about General Mills ( GIS ) . This Minnesota-based corporation is one of the oldest consumer staples on the market. Founded in 1866, the company has become a leader in various products, including cereals, refrigerated yogurt, frozen snacks, and pet food.

Unfortunately, the performance of this company has been inconsistent. While it has shown a number of steep rallies in the past, it has also been prone to a number of steep sell-offs, causing the total return picture to show significant underperformance versus its peers and the S&P 500.

The company's 3.1% yield is also somewhat between a dividend growth stock and a high-yield income stock, which makes it hard for investors to pick GIS for their portfolios.

It also doesn't help that high inflation is causing the company to rely on pricing and operating efficiencies to grow margins.

The good news is that GIS is making good progress. Its brand portfolio is getting an update, margins are improving, and its outlook could be much worse, given the circumstances.

In addition to that, the company has started to hike its dividend again with support from buybacks. I expect this to continue, as GIS has a healthy balance sheet and plenty of free cash flow to facilitate future growth in shareholder distributions.

So, let's get to the details!

GIS - Between Headwinds & Tailwinds

General Mills' shares have risen from $40 in 2019 to $90 in early 2023. Despite falling by 17% since then, shares are still up close to 90% since 2019.

Unfortunately, despite these rallies, the total return of the past ten years is poor, as I showed in the introduction. The problem is that GIS is also prone to steep sell-offs, as it hasn't figured out how to consistently grow its income like high-quality peers such as PepsiCo ( PEP ), Procter & Gamble ( PG ), and The Hershey Company ( HSY ).

The same is visible when looking at the company's dividend track record.

- GIS currently yields 3.1%.

3.1% isn't a bad yield. However, it's somewhere between a dividend growth stock and a high-yield stock.

- The Vanguard Dividend Growth ETF ( VIG ) yields 1.9%.

- The Schwab US High Yield ETF ( SCHD ) yields 3.6%.

On top of that, the average annual dividend growth rate of GIS over the past five years is 2.4%, which means it has the dividend growth rate of a high-yielding stock but a lower yield.

The payout ratio is 50%, which is decent.

Having said all of this, GIS is improving its business.

On June 28, the company announced a 9.3% dividend hike, which is a great step in the right direction, backed by initiatives to take its business to the next level.

During its 4Q23 (fiscal year) earnings call at the end of June, the company highlighted its solid performance during the fiscal year 2023, achieving five consecutive years of meeting or exceeding top and bottom-line growth targets.

This success was attributed to its Accelerate strategy, which allowed it to navigate a challenging operating environment.

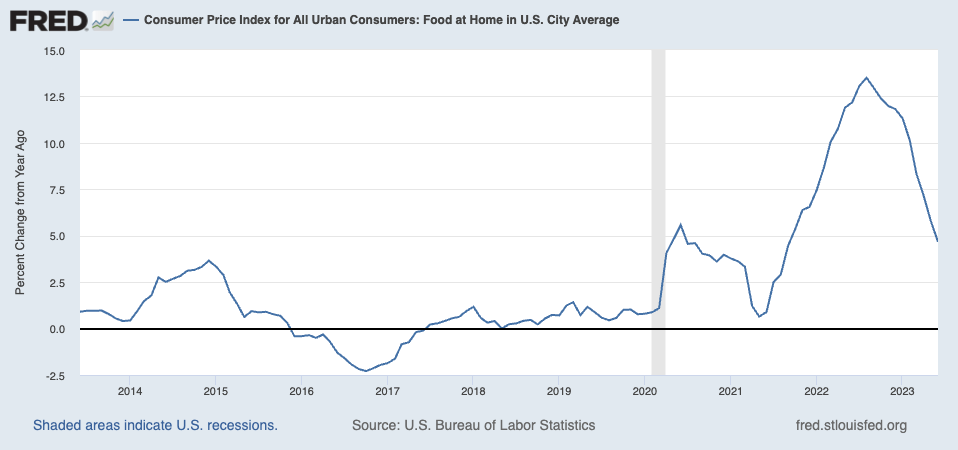

One of these challenges is elevated food inflation, which is a huge risk for consumer-focused brands that compete with generic brands and strong premium brands from competitors.

{kind=link}

Federal Reserve Bank of St. Louis

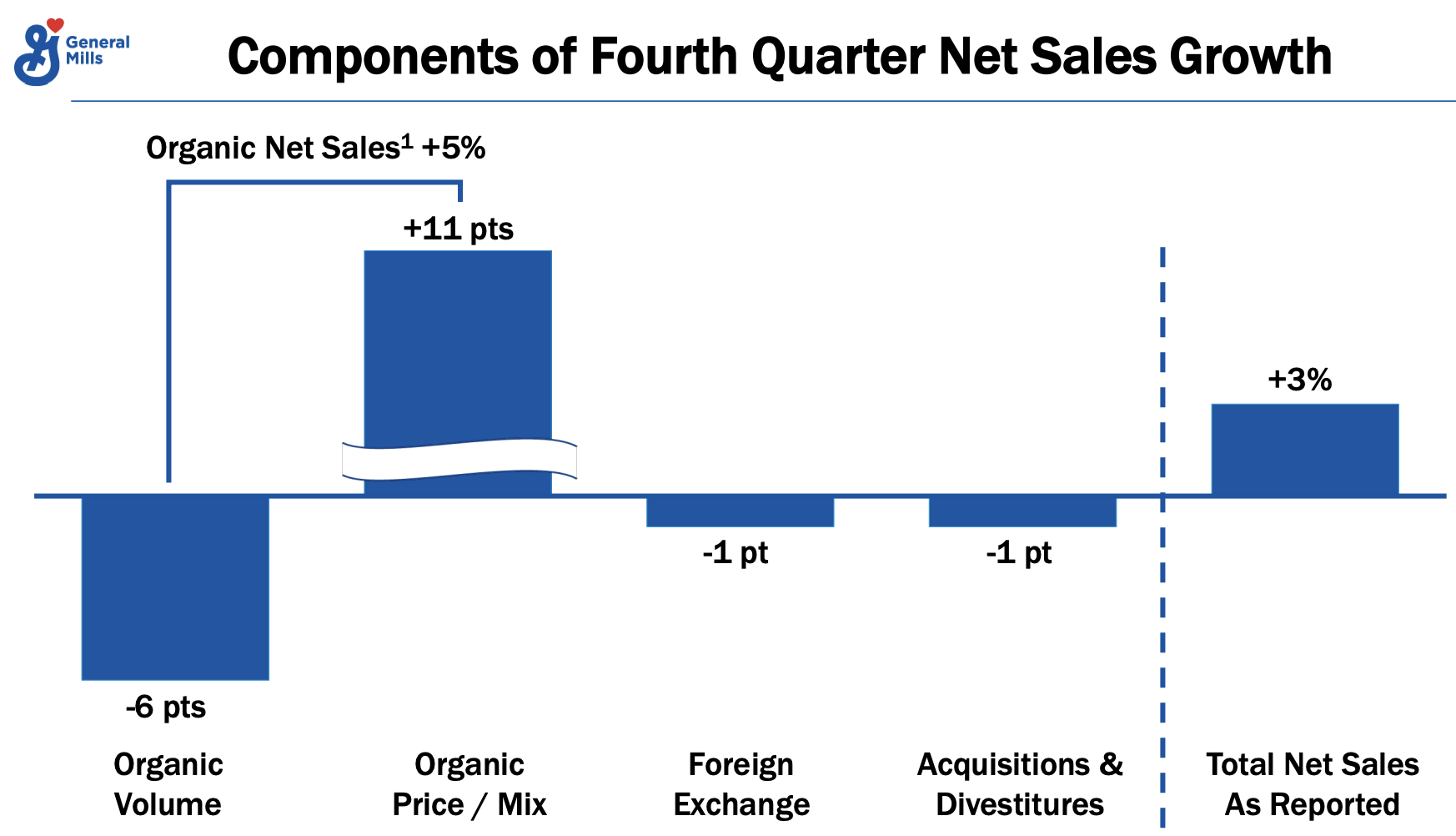

With this in mind, the company achieved 11 points of positive organic price/mix in the fourth quarter, but organic pound volume declined by 6 points due to the retailer inventory headwind.

Foreign exchange and the net impact of acquisitions and divestitures contributed to a 1-point headwind each to net sales growth for the quarter.

Or, to put it differently, the only reason why fourth-quarter net sales were up is because of price increases. Organic volumes were down big time. That's not sustainable if inflation turns out to be sticky.

{kind=link}

General Mills

Volume weakness is partially caused by weak consumer sentiment and inventory headwinds.

For example, in the North America Retail segment, fourth-quarter organic net sales increased by 5%, and comparable Nielsen-measured retail sales grew by 10%. The company blames this on retailer inventory decline, which pressured new orders.

GIS estimates that these retailer inventory headwinds accounted for roughly 3 points of headwind to total net sales growth in the fourth quarter.

With these developments in mind, the company's aforementioned Accelerate strategy is based on three priorities that the company worked on throughout the fourth quarter:

- Competing effectively,

- Investing in the future, and

- Reshaping its portfolio.

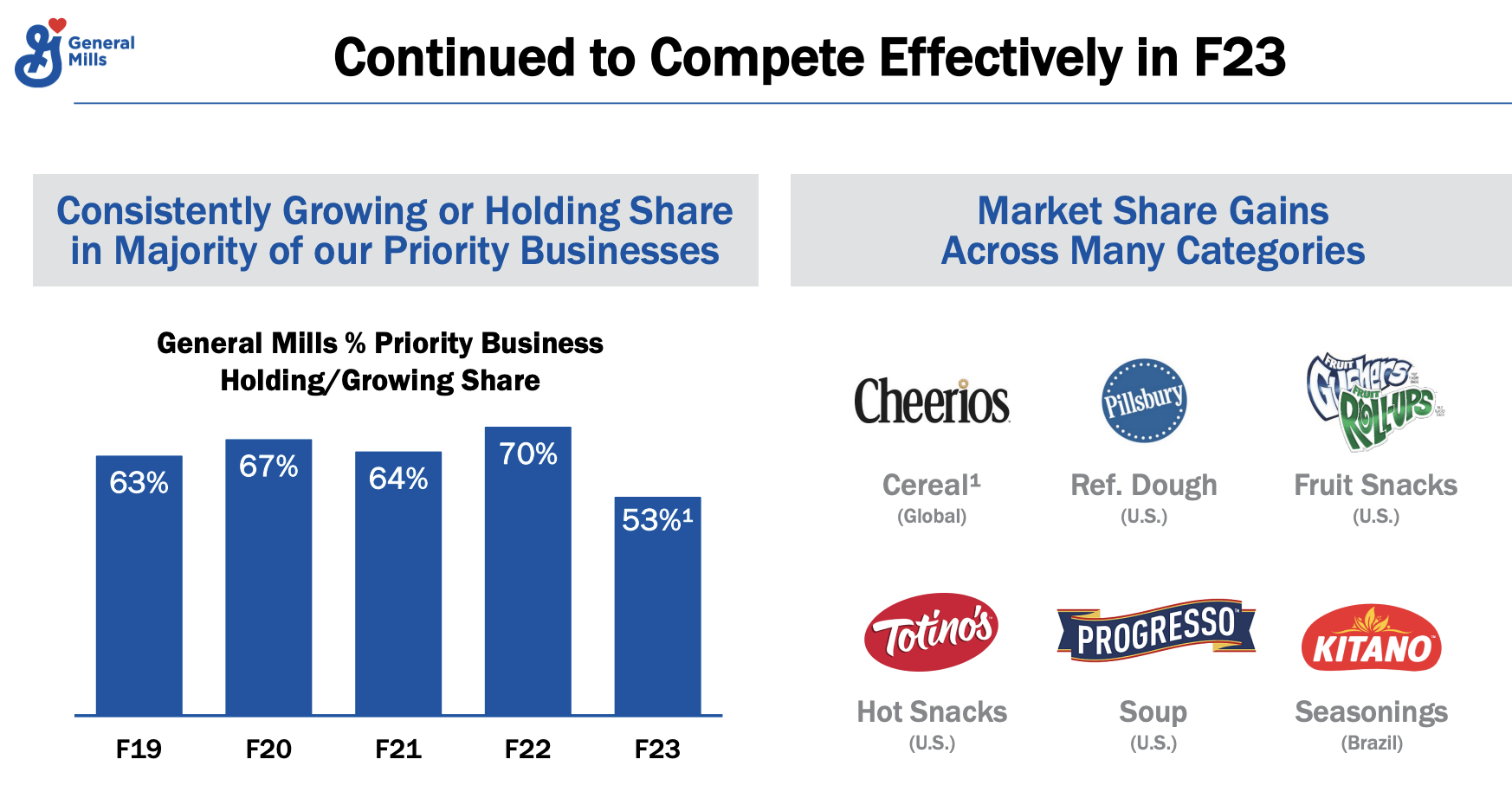

The company was able to gain or hold market share in 53% of its priority businesses globally, which reflects the strength of its brand-building and innovation. While this number is down from prior years, it still suggests that the company has pricing power, which is key in this environment.

{kind=link}

General Mills

Furthermore, investments were made in media, digital consumer engagement, technology, growth capital, and sustainability initiatives.

[...] our media spend in fiscal ’23 was 35 percent higher than our pre-pandemic level. We increased our total capability investment in fiscal ’23, including a double-digit increase in our digital and technology investment. We also increased our investment in growth capital by double-digits, supporting additional capacity on constrained platforms including fruit snacks, pet food, and hot snacks.

{kind=link}

General Mills

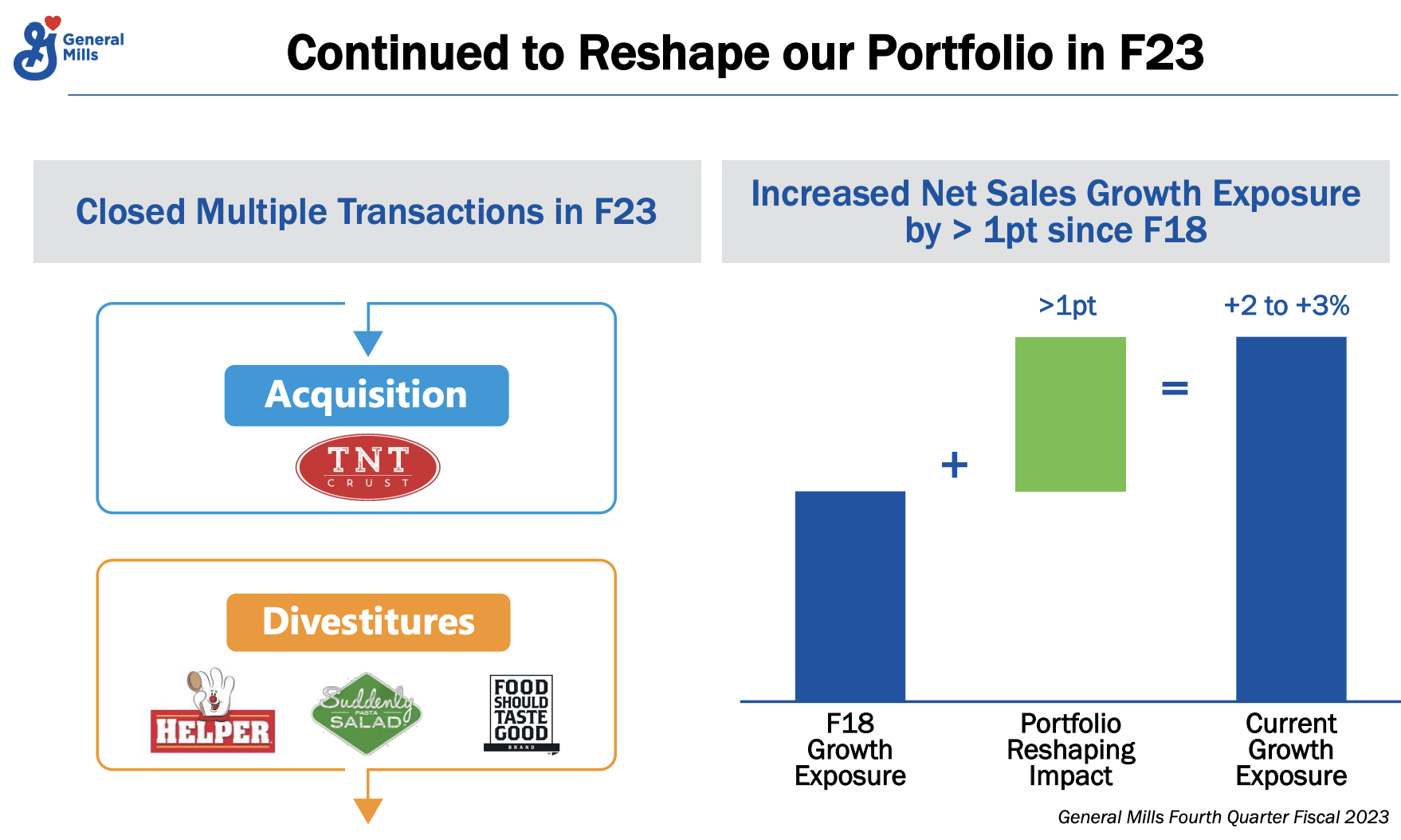

Additionally, General Mills completed acquisitions and divestitures to improve its growth profile, reshaping over 20% of its portfolio since fiscal 2018.

We believe that holding share across our current mix of categories and geographies will generate organic net sales growth that is squarely in the middle of our 2 to 3 percent long-term target.

{kind=link}

General Mills

With that in mind, for fiscal 2024, the company foresees a changing economic environment, with inflation moderating significantly but labor costs remaining a source of ongoing inflation.

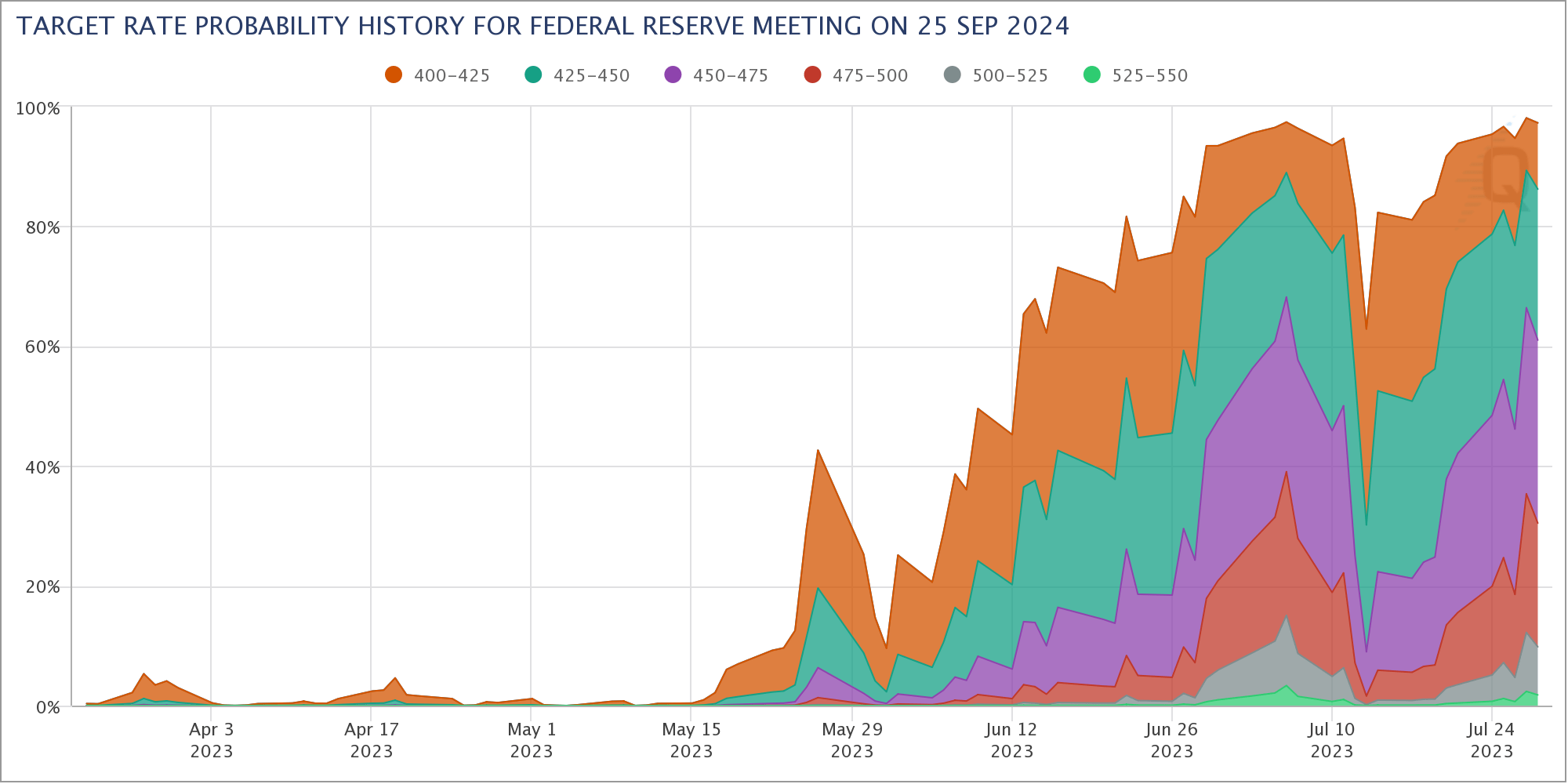

I agree with that. We're obviously past peak inflation, but not in a situation where inflation is likely to reach the Fed's 2% target. Too many structural issues keep inflation sticky, which is reflected in the outlook that Fed rates could remain elevated for longer.

For example, the implied chances that the Fed might keep interest rates above 4.00% at the end of September 2024 have risen from roughly 0% in May to almost 100%.

{kind=link}

CME Group

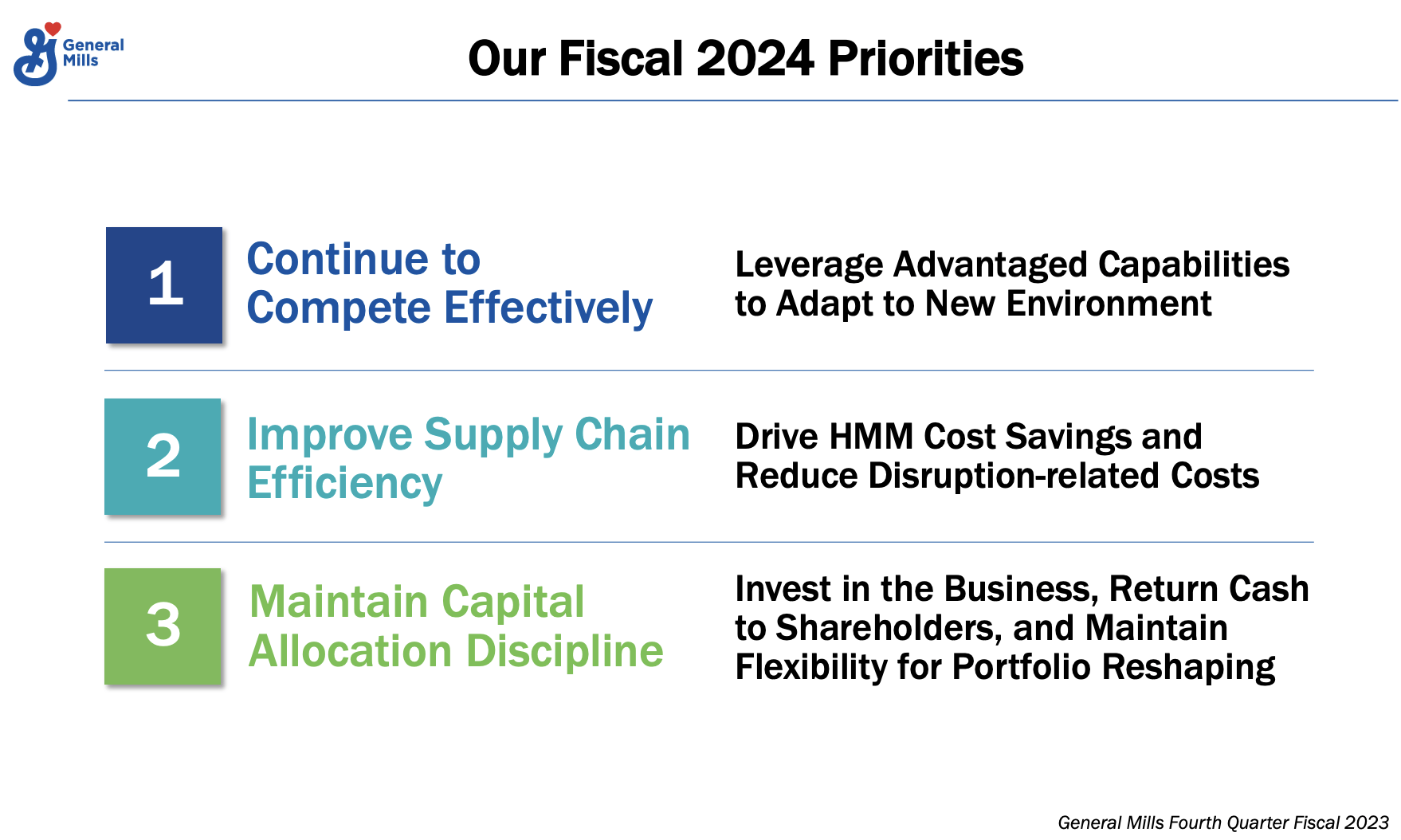

Having said that, for the 2024 fiscal year, GIS has outlined three priorities:

- Competing effectively,

- Improving supply chain efficiency, and

- Maintaining disciplined capital allocation.

{kind=link}

General Mills

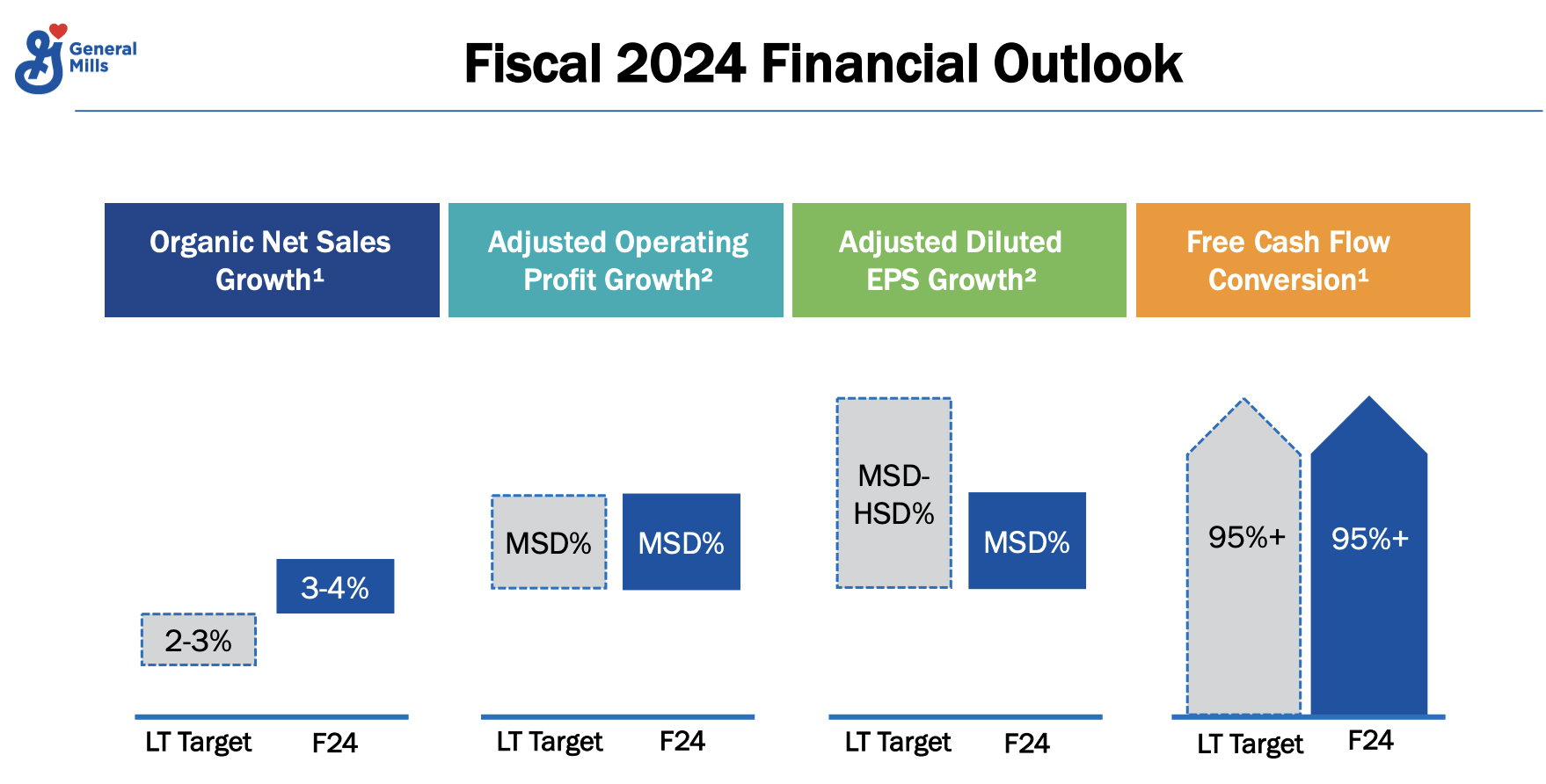

The company plans to increase investment in brand-building campaigns and innovation, leveraging a more stable supply chain environment to drive higher HMM cost savings.

It also aims to invest approximately 4% of net sales in capital expenditures while delivering strong and consistent dividend growth.

The company's growth targets for fiscal 2024 include 3-4% organic net sales growth, 4-6% growth in adjusted operating profit, and adjusted diluted EPS in constant currency.

{kind=link}

General Mills

GIS also expects contributions from organic price/mix to decelerate but remain positive, driven by the aforementioned actions taken in the back half of fiscal 2023.

Furthermore, the company anticipates improved organic pound volume performance, less headwind from pricing, and increased commercial activity due to a more stable supply chain.

Shareholder Distributions & Valuation

So far, shareholders aren't convinced that GIS is on the right track. We can blame it on profit-taking, but I believe that selling pressure since May results from the belief that persistent inflation makes consumer goods products with increasingly limited pricing power quite fragile.

It's hard to disagree with that.

FINVIZ

Nonetheless, the company isn't in a horrible spot. Yes, the stock is unlikely to outperform the market as long as inflation is expected to remain elevated. However, it is generating a lot of free cash flow.

Analysts expect the company to gradually increase free cash flow from $2.1 billion in its 2023 fiscal year to $3.0 billion in its 2026 fiscal year. In 2025, the company is expected to generate $2.9 billion in free cash flow, which would translate to a 6.6% free cash flow yield.

This implies a 47% dividend cash payout ratio and a lot of room to buy back stock and hike this dividend. After all, the company is expected to lower net debt below $11 billion this year, which implies a 2.6x net leverage ratio.

The company has an investment-grade BBB credit rating.

Hence, I believe that the dividend is now able to grow more consistently. When adding the high possibility that elevated inflation will keep a lid on the stock for a while, we could soon see a more satisfying dividend yield that better fits the company's slower-growth profile.

With regard to the valuation, GIS is trading at 15.2x next year's expected free cash flow. That valuation is fair. If we apply a 17x multiple, the fair value is 12% above the current price, which is $85 per share, slightly above the current consensus price target of $81.

While I believe that GIS is in an increasingly good spot to become a strong defensive income stock, I'm not a buyer at these levels.

I believe that inflationary headwinds will keep a lid on the stock - especially after the strong post-2019 rally.

Investors interested in buying GIS might be better off waiting for a bit more downside, as that makes the yield more attractive.

For now, I'm giving the stock a neutral rating, despite my somewhat bullish view. I believe that GIS needs to fall further for it to become a good buy.

Takeaway

General Mills presents a mix of headwinds and tailwinds for investors to consider. While the company has made progress in improving its business, its inconsistent performance has hindered its total return compared to peers and the market.

The 3.1% dividend yield falls between a growth stock and a high-yield stock, making it a challenging choice for portfolios.

However, there are positives to note, such as the recent dividend hike and the company's focus on brand updates and innovation.

Despite inflation challenges, General Mills is generating significant free cash flow, leading to potential dividend growth and share buybacks.

While the company's valuation appears attractive, it might be wise to wait for a better entry point, considering the current inflationary headwinds.

For now, a neutral rating is appropriate, but with the potential for further improvement, General Mills could become an attractive defensive income stock in the future.

For further details see:

General Mills: A Dividend Diamond In The Rough