GIS - General Mills: A Steady Hold In Times Of Inflation

Summary

- General Mills has shown strong resistance to inflation. The stock has been rewarded with excellent performance during 2022;

- In light of this solid increase in stock price, GIS stock is now in line with trading comps and the value estimated by DCF analysis.

- With the exception of Blue Buffalo, the growth potential of the brands in the portfolio is relatively low.

- Given all of this, it is a stock for which I have a hold recommendation. It may offer at most a hedge against the case of higher-than-expected inflation.

General Mills ( GIS ) is one of the few companies that has performed well in 2022. Its stock has grown by 22% YoY, thanks to its ability to withstand the challenges of the current macroeconomic environment. Sales data, for example, show that the company has benefited economically from inflation: consumer prices have increased more than production costs.

According to my analysis, the stock is now very close to its intrinsic value and even slightly overvalued. Considering the profitability of bonds at this time, it is difficult to argue that the potential return on General Mills' stocks justifies buying them. My recommendation is to hold: I do not see great potential for growth in the stock price or dividends, but I believe that holding it in a portfolio can offer a hedge against the possibility that inflation remains higher than expected.

About General Mills

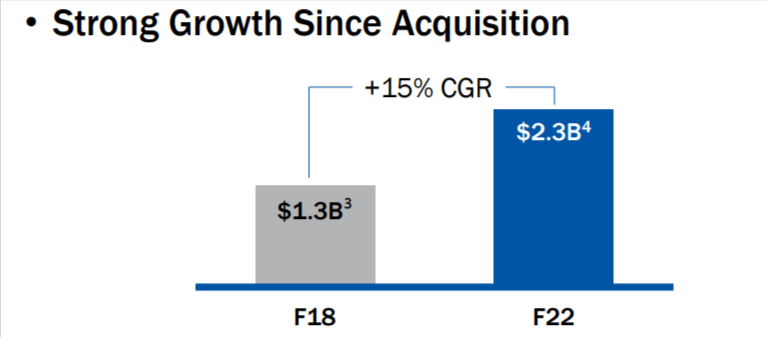

General Mills produces, distributes, and directly sells processed foods. The company manages over 100 brands, including Cheerios, Häagen-Dazs, and Old El Paso. Since 2018, with the acquisition of Blue Buffalo, it has also been operating in the pet food industry. In the last 5 years, General Mills' brand portfolio has had a turnover of 20%, so the offering is constantly updated.

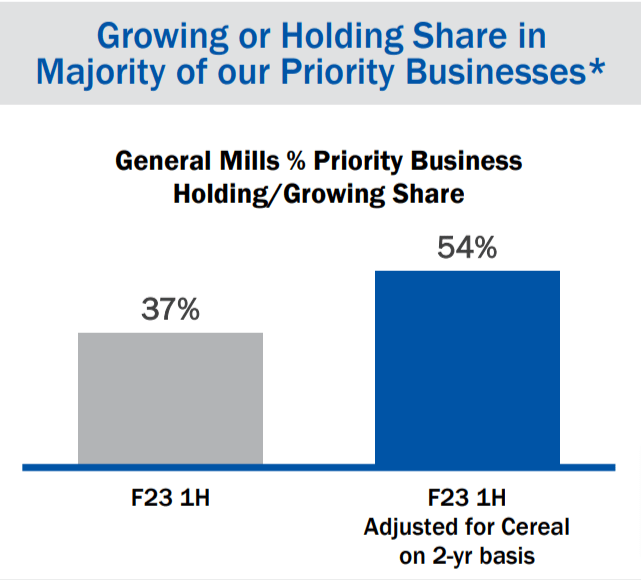

General Mills' most important brands sell worldwide, but most of the company's revenue still comes from North America. The appeal to consumers remains strong: for most brands, market share has remained unchanged or grown in the last three quarters, according to Nielsen data reported in the investor presentation.

{kind=link}

The strength of the dollar is partially masking revenue growth, especially due to the depreciation of the Canadian dollar. The estimated impact on revenue by the company itself is 4.50% for the current year. Organic net sales, i.e., sales adjusted for exchange rate movements and acquisitions/divestitures, are expected to increase by 10% during the calendar year 2023 according to the latest forecasts disclosed at the CAGNY conference .

General Mills therefore presents itself as a giant in its industry, with a large market penetration and growing revenue. For this reason, it can be considered a low-risk stock, which also offers a small dividend, but it is important to relate this data to the stock price.

Strategy and outlook

General Mills' management has emphasized two key points of its strategy in the last conferences it attended:

-

Increasing focus on direct distribution in North America, investing in digital channels and e-commerce;

-

Continuing to increase market penetration in pet food, which has already doubled since the acquisition of Blue Buffalo.

{kind=link}

The company is investing in its growth with double-digit increases in marketing spending, production capacity, and digital channels. The management is trying to strengthen the power of its brands, loosening its grip on international markets and concentrating most of the marketing in North America.

Strengths and opportunities

One of General Mills' great strengths is its ability to improve its results during periods of high inflation. Like any other business, the company has experienced cost inflation, but it has managed to pass on a greater price increase to the end consumer. This is a typical strength of the entire essential goods sector, which is one of the few that has had a positive performance throughout 2022.

Sales volumes reported in the latest quarterly presentation show a 6% decrease in the amount of product delivered to customers. At the same time, the 17% price adjustment has more than compensated for this drop in demand. This gives us a numerical perspective on how inflation-resistant this company can be.

In the event that the dollar were to lose some of its strength acquired over the past year, the company could also benefit from a significant increase in sales in Canada and all international markets.

As for market share, the company exhibits significant results in virtually all verticals in which it operates. Some of the most relevant data, as reported by General Mills in its most recent investor presentation, is shown in the table below (data source: General Mills investor presentation, pub. dec. 2022 ).

| Vertical |

| Market Share |

| U.S. RTE Cereal |

| 33.8% |

| U.S. Refrigerated Dough |

| 73.2% |

| U.S. Fruit Snacks |

| 53.7% |

Finally, an important opportunity is represented by the new product lines that the company has introduced in the pet food industry. It is primarily focusing on the Wholesome Natural and Therapeutic verticals, which exhibit the highest growth rate within the industry.

Financials

The latest financial data available to us is the one published on December 20, 2022 , related to Q2 of fiscal year 2023. On that occasion, the company adjusted its guidance upwards for the current year, and then did so again at the CAGNY 2023 conference.

My approach usually consists of three phases:

A top-down view of the company's most important numbers over the years;

A direct comparison with trading comps;

An analysis of discounted cash flow.

My hold recommendation is confirmed by all three models, giving me some confidence in the forecast.

At a glance

The table that follows shows the data I consider most relevant for analyzing the situation of General Mills (data source: Seeking Alpha).

| 2022 |

| 2021 |

| 2020 |

| 2019 |

| 2018 |

| Revenue ($ mln) |

| 18,993 |

| 18,127 |

| 17,627 |

| 16,865 |

| 15,740 |

| EPS |

| 4.46 |

| 3.81 |

| 3.59 |

| 2.92 |

| 3.69 |

| Debt ratio |

| 65.30% |

| 67.41% |

| 71.13% |

| 73.70% |

| 76.27% |

| Price/book ratio |

| 4.05 |

| 3.89 |

| 4.65 |

| 4.57 |

| 4.33 |

| Operating margin |

| 18.30% |

| 17.35% |

| 16.76% |

| 14.92% |

| 15.94% |

| ROE |

| 25.68% |

| 24.71% |

| 27.07% |

| 24.85% |

| 34.70% |

| ROA |

| 8.71% |

| 7.35% |

| 7.08% |

| 5.82% |

| 6.96% |

| P/E Ratio |

| 15.77 |

| 15.76 |

| 17.19 |

| 18.40 |

| 12.47 |

The company's debt has dropped significantly in the last five years, good news as interest rates have become a problem for many companies today. The operating margin has improved with inflation, but I expect it to tend to oscillate around the historical average of 15-16% in the long term.

In general, these data show that General Mills is a stable company. A long-standing giant that seeks to optimize its portfolio year after year, trying to defend its market share and hunting for acquisitions at attractive prices. With an ROE of 25.68%, management has been quite efficient in distributing resources among the various business units.

Trading comps

From the analysis of trading comps, General Mills appears as a competitive stock compared to direct alternatives. Below are the data used in the analysis (data source: TradingView). The trading comps I have picked are NSRGY , DANOY , KO and UL .

| General Mills |

| Nestlé |

| Danone |

| Coca-Cola |

| Unilever |

| ROE |

| 28.35% |

| 25.90% |

| 5.30% |

| 40.28% |

| 27.29% |

| P/E RATIO |

| 16.76 |

| 31.67 |

| 36.35 |

| 27.24 |

| 22.07 |

| PRICE/BOOK |

| 4.76 |

| 7.56 |

| 1.42 |

| 10.70 |

| 5.80 |

| PRICE/FCF |

| 19.76 |

| 27.68 |

| 10.85 |

| 27.06 |

| 76.73 |

| Debt ratio |

| 66.88% |

| 68.34% |

| 60.26% |

| 72.16% |

| 72.11% |

| Revenue growth |

| 2.84% |

| 3.29% |

| 2.80% |

| 17.09% |

| 3.39% |

| EPS growth |

| 6.13% |

| 38.19% |

| -1.67% |

| 26.14% |

| 8.45% |

Of these companies, the one I would invest in if I had to is Danone. Being particularly dependent on the price of milk, it has had a difficult year in terms of profitability, as milk is one of the commodities that has been hit hardest by inflation. The group has decided not to transfer this price increase to consumers, or at least to limit price increases to a more moderate level, like General Mills. This can, in the medium term, reveal an improvement in market share and allow the company to remain steadily above $2 billion in annual profits. My second choice would be General Mills.

Discounted Cash Flow

The assumptions on which I built the discounted cash flow model are:

-

WACC of 9.23% based on the current risk-free rate and the stock's beta in the last five years;

-

Gradual return to a net income close to 11.50% of revenue, i.e., General Mills' historical average. Lately, it has been lower due to increased brand investments and digital channel development;

-

D&A equal to the historical average of 3.30%;

-

Adjusted tax rate of 21.30% as reported by the company in its presentations;

-

Annual Capex equal to the historical average of 2.35% of revenue.

The result is as follows:

| $ mln |

| 2022 |

| 2023 |

| 2024 |

| 2025 |

| 2026 |

| 2027 |

| 2028 |

| 2029 |

| 2030 |

| Revenue |

| 19,370.00 |

| 20,532.20 |

| 21,456.15 |

| 22,099.83 |

| 22,762.83 |

| 23,445.71 |

| 24,149.08 |

| 24,873.56 |

| 25,619.76 |

| Net Income |

| 2,710.00 |

| 2,463.86 |

| 2,574.74 |

| 2,541.48 |

| 2,617.73 |

| 2,696.26 |

| 2,777.14 |

| 2,860.46 |

| 2,946.27 |

| Tax rate |

| 21.30% |

| 21.30% |

| 21.30% |

| 21.30% |

| 21.30% |

| 21.30% |

| 21.30% |

| 21.30% |

| 21.30% |

| D&A |

| 581.1 |

| 616.0 |

| 643.7 |

| 663.0 |

| 682.9 |

| 703.4 |

| 724.5 |

| 746.2 |

| 768.6 |

| Interest |

| 484.25 |

| 615.97 |

| 643.68 |

| 663.00 |

| 682.88 |

| 703.37 |

| 724.47 |

| 746.21 |

| 768.59 |

| CapEx |

| 571.00 |

| 482.51 |

| 504.22 |

| 519.35 |

| 534.93 |

| 550.97 |

| 567.50 |

| 584.53 |

| 602.06 |

| Unlevered FCF |

| 2,720.1 |

| 2,597.3 |

| 2,714.2 |

| 2,685.1 |

| 2,765.7 |

| 2,848.7 |

| 2,934.1 |

| 3,022.1 |

| 3,112.8 |

| Discounted FCF |

| 2,720.1 |

| 2,377.93 |

| 2,478.05 |

| 2,451.50 |

| 2,525.05 |

| 2,600.80 |

| 2,678.82 |

| 2,759.19 |

| 2,841.96 |

We then add the terminal value:

| Present value (2023-30) |

| 20,713.30 |

| Terminal value |

| 45,646.16 |

| Actualized TV |

| 22,068.6 |

| Company valuation |

| 42,781.9 |

The result is in line with the current market capitalization of the company, suggesting that the stock is only slightly overvalued. Given the approximations necessary to build the DCF, one cannot really speak of an overvalued or undervalued stock.

Final considerations

General Mills is a large company with a well-established presence in North America and around the world. Its growth prospects are stagnant, but the company continues to reduce its debt and slightly raise the dividend year after year. For this reason, if one intends to add an inflation hedge stock to their portfolio, it can be a good decision without great expectations.

From the analysis of trading comps, it may seem slightly more advantageous to invest in Danone, but in this case, it is a company that is suffering from inflation in the name of a long-term market share advantage. Overall, it is not a stock that I expect to undergo significant changes in the next four or five years.

For further details see:

General Mills: A Steady Hold In Times Of Inflation