GIS - General Mills: Softening Sales Growth Creates An Attractive Entry Point

2024-01-05 16:01:07 ET

Summary

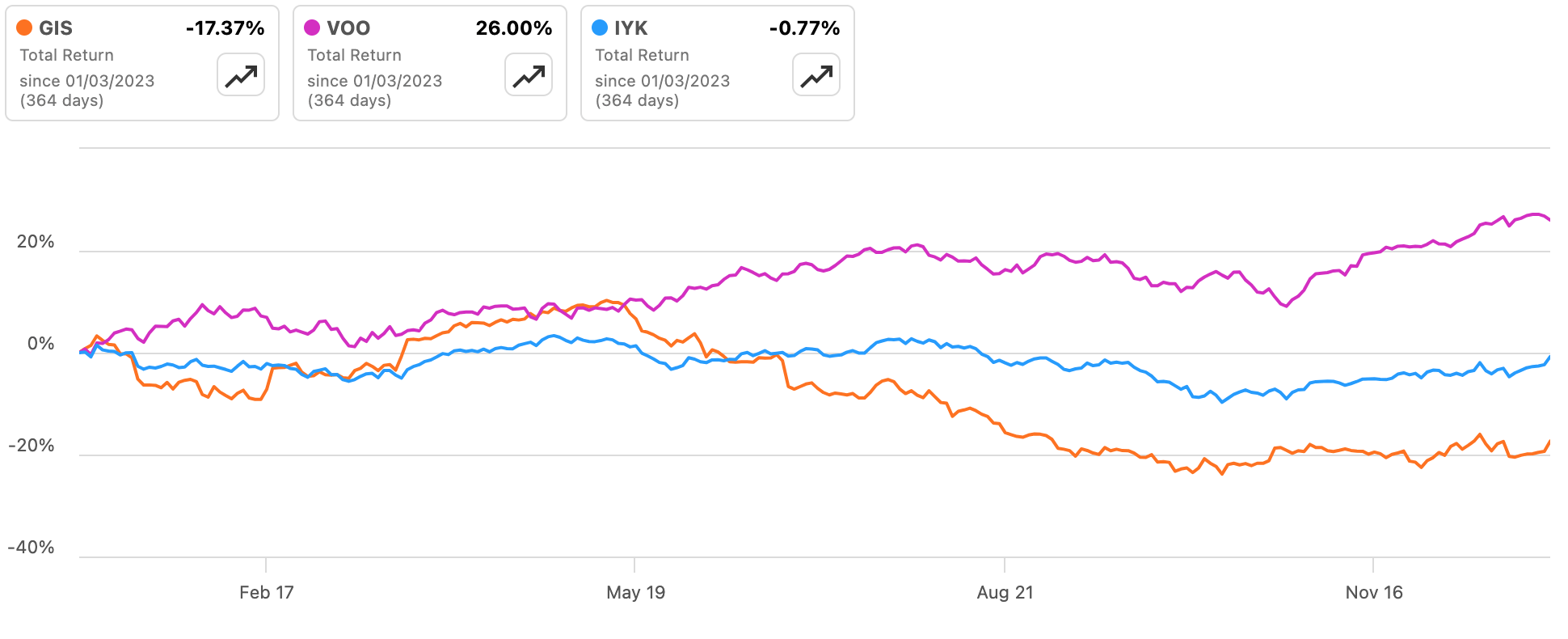

- General Mills stock has significantly underperformed over the past twelve months on the back of weakening organic sales growth.

- Top line performance looks more reflective of macro factors rather than company-specific problems, with consumer behavior and competitor shelf-availability both normalizing having been tailwinds previously.

- The stock now trades for under 15x forward EPS estimates, meaning the company can realize growth below management's own long-term targets and still deliver reasonable returns for investors.

It hasn't been a good twelve months for General Mills ( GIS ) stock. Shares of the fast-moving consumer goods giant have significantly underperformed both the wider U.S. staples space and the S&P 500 in that time, with that coming amid softer than expected sales growth at the firm. While this has led management to downgrade initial FY2024 guidance, the company's struggles look more macro-related rather than company-specific. With the stock now trading for just 15x forward EPS estimates, General Mills really only needs to produce modest underlying earnings growth to make things work, given the contribution from stock buybacks and its dividend. As this equates to a margin of safety relative to management's own long-term growth targets, now looks like a good time for investors to take up a position here.

{kind=link}

Source: Seeking Alpha

As one of America's leading FMCG companies, General Mills doesn't require a lengthy introduction. Brands like Cheerios, Nature Valley, Häagen-Dazs, Old El Paso and Blue Buffalo speak for themselves. The company's North America Retail segment accounts for around 80% of group EBIT, with International (~4%), Pet (~11%) and North America Foodservice (~7%) smaller contributors to group earnings.

I view General Mills as being a Steady-Eddy type company, as its range of products and market share makes it a very important supplier to grocery retailers. For instance, Walmart ( WMT ) accounted for 21% of the company's consolidated sales as per its most recent 10-K. Ten years ago, that figure was also 21%. Fifteen years ago? 20%. While there are naturally risks to consider - evolving consumer tastes to name but one - this points to a very stable business overall.

Why Has GIS Stock Underperformed Recently?

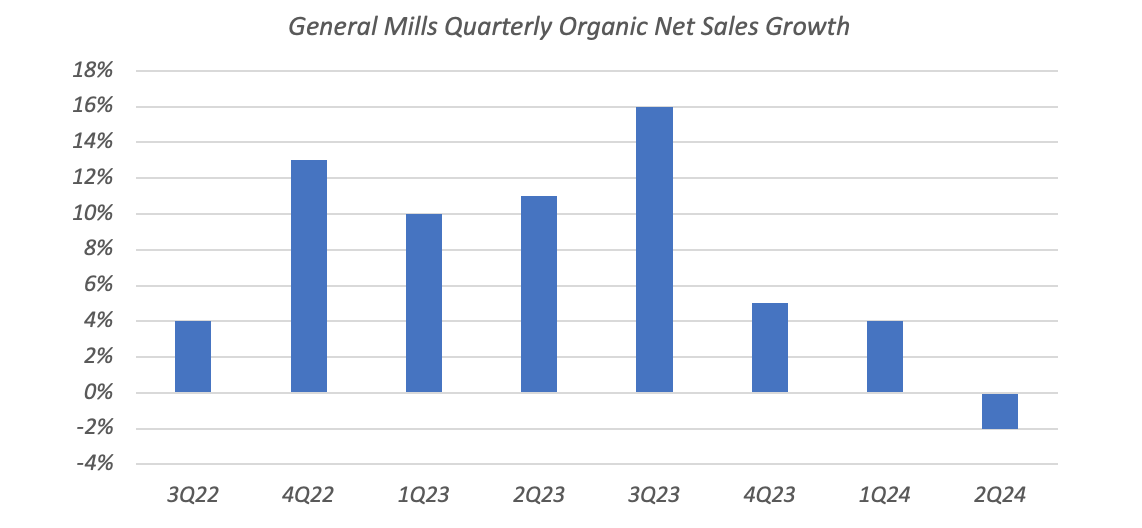

Partly thanks to all the stimulus cash released during COVID, General Mills and its peers managed to navigate the steep rise in inflation with better price elasticity than might have been the case pre-2020. The firm was realizing strong double-digit contributions to sales from price/mix while only seeing relatively modest push back in terms of volumes, leading to very strong organic sales growth overall:

{kind=link}

Data Source: General Mills Quarterly Results

This helped propel the stock toward 5-year highs in terms of valuation, taking it to levels seen during the COVID boom, when volumes and sales popped due to stay-at-home driven demand.

Sales have been softening in more recent quarters. The company reported a 2% fall in organic net sales in its fiscal Q2 (its financial year ends in May), with volumes down by 4ppt. Management noted in its quarterly remarks that price elasticity remained "below historical levels", but was rising, indicating normalizing consumer behavior. As a result, sales guidance was cut, with full-year organic net sales growth now seen at -1% to flat versus 3-4% growth previously. The market responded by slashing the stock's valuation, with this ultimately driving its underperformance, notwithstanding the fact that EPS estimates continue to point to modest growth.

Reasons To Be Optimistic

Despite sales growth softening, there are good reasons to remain optimistic. For one, management attributed part of the softer sales numbers to competition regaining shelf availability after the major supply chain disruptions in previous periods. This suggests to me that the company's underlying market position has not been weakening to the extent implied by its top line performance. Rather, the company is just seeing a normalization of industry trends to which it was previously a beneficiary:

And so we knew that on-shelf availability would be a headwind for us, because frankly our supply chain held up a lot better than our competition did a year ago. And so, we calculate, we factored that into our guidance for this year. But the fact of the matter is, on-shelf availability for our competition increased a lot faster, particularly private label and small players, faster than we had anticipated. Importantly, they're now catching up to our on-shelf availability. And so, we've actually improved our on-shelf availability this year.

Jeff Harmening, General Mills Chairman & CEO, Q2 FY2024 Earnings Call

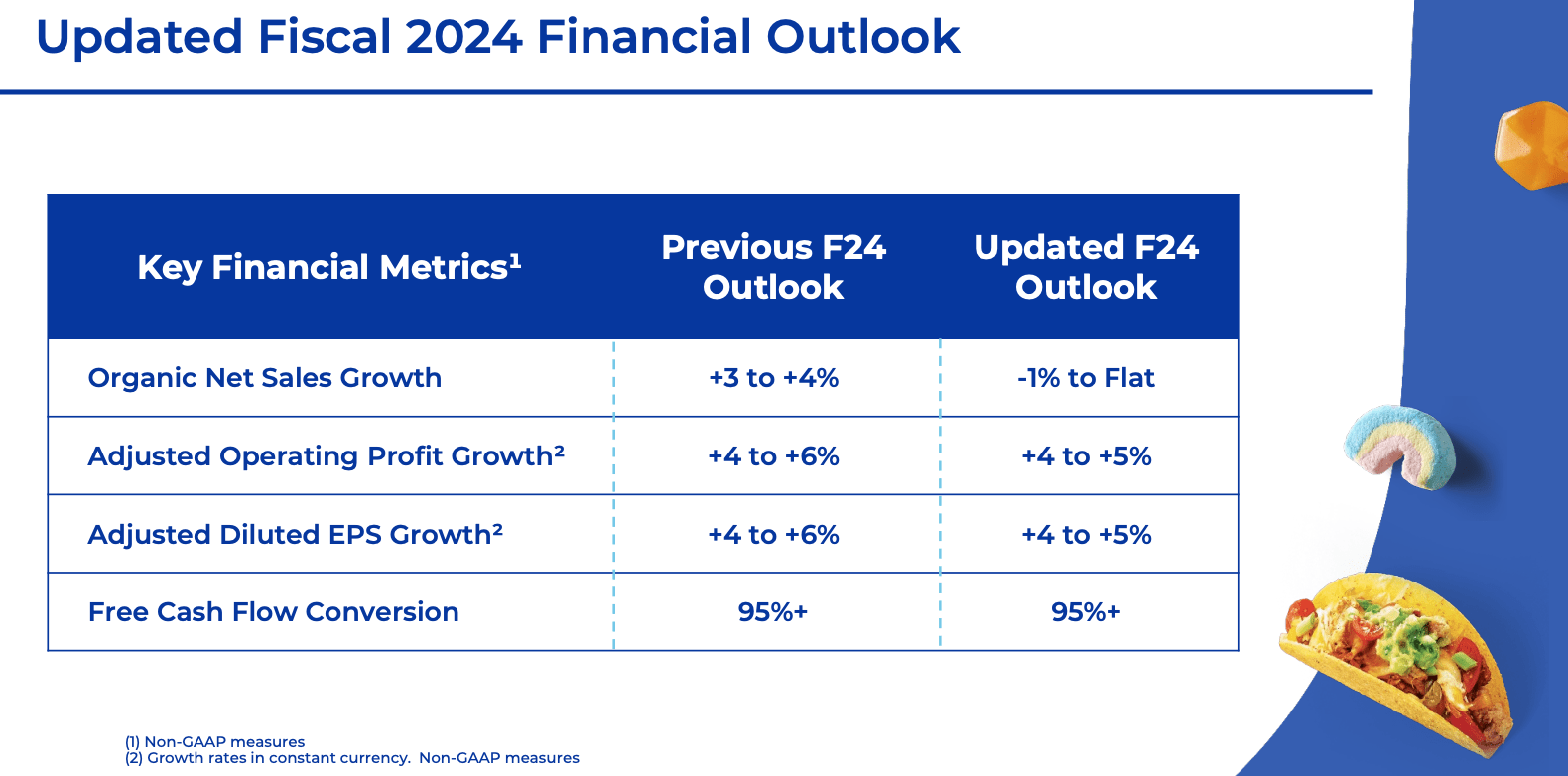

Secondly, guidance implies that earnings will actually hold up much better than sales. Adjusted operating profit and EPS are seen growing 4-5%, with that only tightened a shade from prior guidance of 4-6% growth.

{kind=link}

Source: General Mills Q2 FY2024 Results Presentation

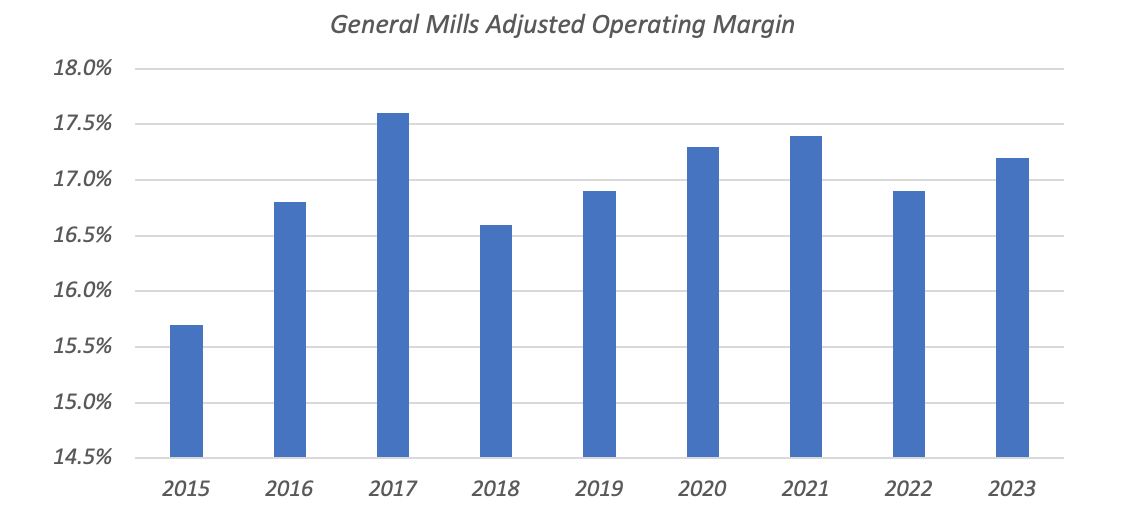

Indeed, despite the sales decline, the adjusted operating profit margin of 19.3% was up sharply on the year-ago period and is above its long-run average. Crucially, the company hasn't achieved this by reaching for the low-hanging fruit of making cuts to marketing and R&D, with management actually putting through a high single-digit increase in media investments last quarter.

{kind=link}

Data Source: General Mills Earnings Releases

Finally, I would note that the drop in the stock's valuation boosts buyback potential. Current annual earnings power is in the $2.6 billion region, and the company typically converts all of its GAAP net income into free cash flow. Because the dividend has only grown at a 3% annualized clip over the past five years, the payout ratio has now fallen to the 50% mark. That means the company has up to $1.3 billion in annual buyback capacity from surplus free cash generation. With the current market-cap at around $38 billion compared to over $50 billion mid-last year, GIS can use its surplus cash flow to lower its share count at a 3-4% annual clip.

At 15x consensus FY2024 EPS estimates, the stock is trading comfortably below its long-run average P/E:

Because of that, the company can now underperform management's long-term growth targets while still delivering attractive returns to shareholders. Those targets include 2-3% annual organic sales growth, mid-single-digit annual adjusted operating profit growth, and mid/high single-digit annual EPS growth as per the most recent 10-K:

{kind=link}

Source: General Mills FY 2023 Form 10-K

However, even more modest underlying earnings growth of 3% should do the trick at the current valuation. The company can deliver a further 3-4% from buybacks as outlined above, with the current $2.36 per share annualized dividend adding around 3.5% on top. All told, investors would be looking at a very reasonable 10% annualized total return, all else equal.

Risks

The main risks here are to sales growth and margin requirements. Although I would characterize General Mills as a low expectation investment right now, it does still need to deliver modest positive sales growth and hold operating margins steady in the high-teens area. The company has significant exposure to processed foods, which could prove a challenge to growing revenues if consumer preferences evolve. Margins could also come under pressure from cost inflation, especially if the company is unable to offset this with sales growth. Nonetheless, with growth requirements already baking in a significant margin of safety relative to the company's own long-term targets, now looks like a good entry point for investors.

For further details see:

General Mills: Softening Sales Growth Creates An Attractive Entry Point