GIS - General Mills: Upside Will Likely Be Limited At Current Levels

2023-08-31 10:54:25 ET

Summary

- Investors have different priorities and tailor their investment strategies around specific objectives.

- The S&P 500 and broader indexes are struggling to generate consistent returns, leading to more unconventional investing strategies.

- General Mills is a popular choice among income investors.

Investors often have different priorities. While some people will have similar goals, usually individuals have specific objectives that they want to tailor their investment strategies around. With the S&P 500 ( SPY ) and most of the broader indexes struggling to generate consistent solid returns or solid income, picking out specific companies or using less orthodox investing strategies has become more prevalent.

One of the more well-known companies that has been very popular for many income investors in particular is General Mills ( GIS ). General Mills is a $39 billion company that sell various food and beverage products under such well-known brands as Anne's, Cheerios, Betty Crocker, and Nature Valley.

General Mills has offered investors a total return of 77.51% since 2018, while the S&P 500 has offered investors a total return of 68.36% during the same time.

Still, this iconic company has struggled significantly over the last year.

General Mills offered investors a total return of negative 8.22% over the last year, while the S&P 500 has offered investors a total return of 14.64% during this same timeframe.

Today, I am initiating my rating of General Mills as a sell. This iconic company has brands that have reached a saturation point in most of the markets the company sells into, and management has no plan to deal with the continued margin compression that the company has dealt with over the last three quarter, and General Mills is dealing with rising input costs as well. The stock also looks overvalued looking at several metrics.

General Mills fourth quarter earnings report showed the continued challenges that the company has struggled to handle over the last year. The leading food maker recently stated that GAAP earnings were $1.03 a share and that the company made $5.03 billion in revenues. Analyst expectations were for GAAP earnings per share of $1.06 and revenues of $5.17 billion. While the company did not miss analyst projections by a significant margin, there were several issues that should concern investors that came up in this recent report.

{kind=link}

An excerpt of General Mills earnings report (generalmills.com)

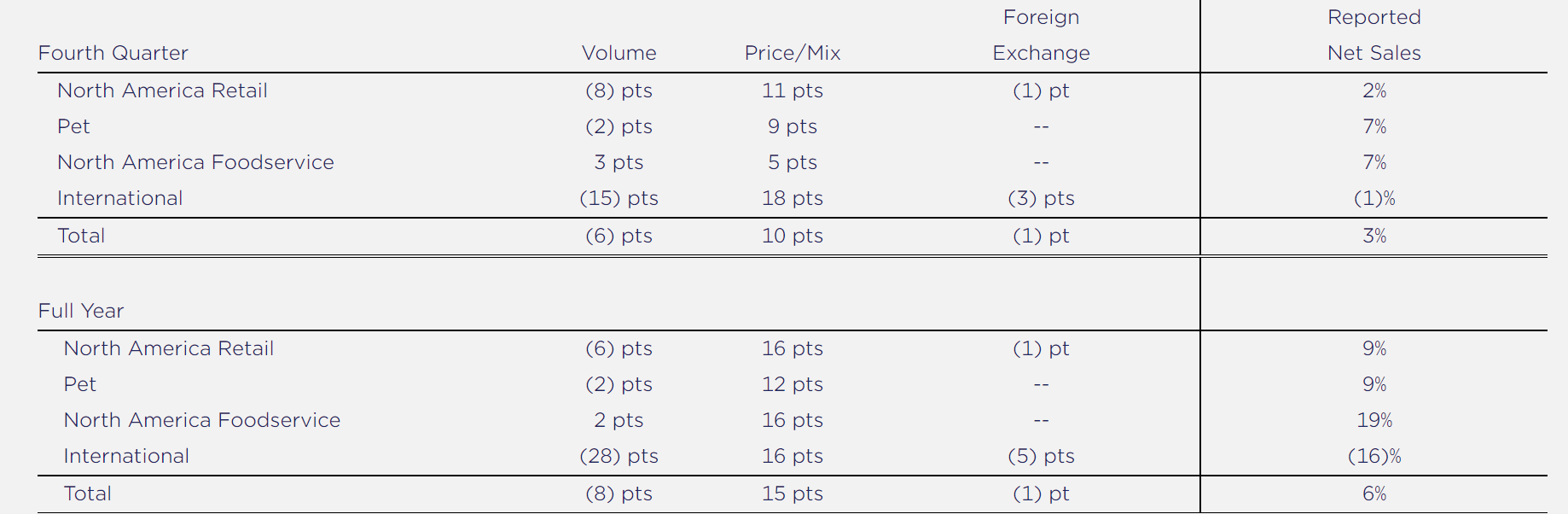

Even though General Mills stated that net sales were up 10% full year and 5% for the quarter, the company saw flat to negative sales volume growth with most products when taking out price increases. For the full year, the company saw a 28-point drop in net international sales volume using constant currency that the 16-point increase was not able to offset. The company's full year net sales volume growth in North America Retail was negative 6 points, while net sales growth in North American Food service was also minimal at 3 points for the year. General Mills has been relying on price increases to increase earnings, and the company continues to see net sales volumes be flat to negative in most segments of the business.

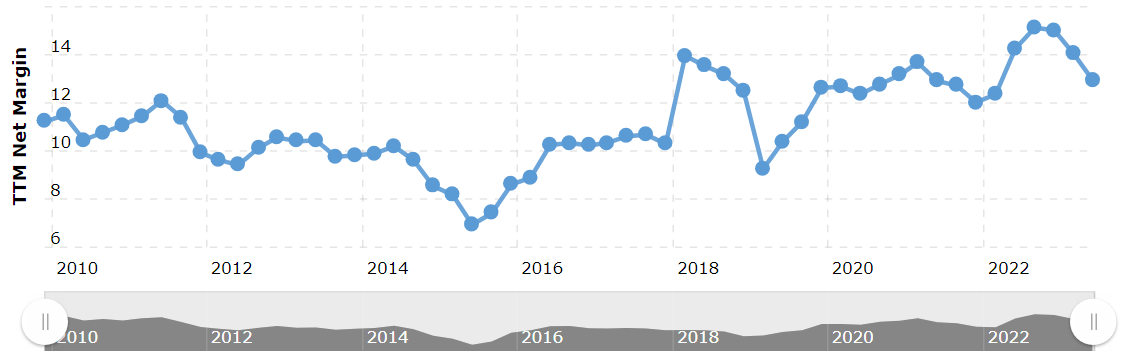

The company's reluctance to further raise prices even as net margins have now declined for three straight quarters also shows management thinks the company's pricing power is reaching a limit. The food maker's margins were lower again, for the third straight quarter. Management stated that gross margins were down 180 basis points to 34.2%. General Mill's net margins have continued to decline as well.

{kind=link}

A chart showing General Mills net margins (macrotrends)

The company's net margins have fallen from 15.13% a year ago, to 12.91% in this past quarter. The fact the leading food maker also report flat to negative organic net sales volume growth in most core segments of the business also shows that the company's pricing power has limitation, management has no plan to deal with the consistent and significant margin compression.

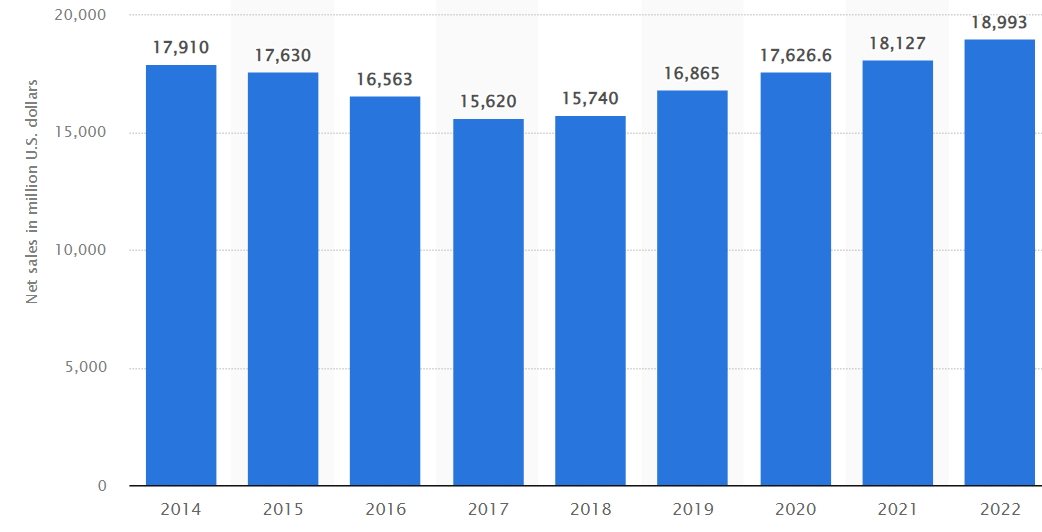

General Mill's net sales volume declines in the international business is also concerning since the company's overall international revenue growth has been minimal for some time.

{kind=link}

A chart showing General Mill's international revenues (statista)

General Mill's international revenues have barely grown since 2014, and the company's international revenue growth this year was also minimal.

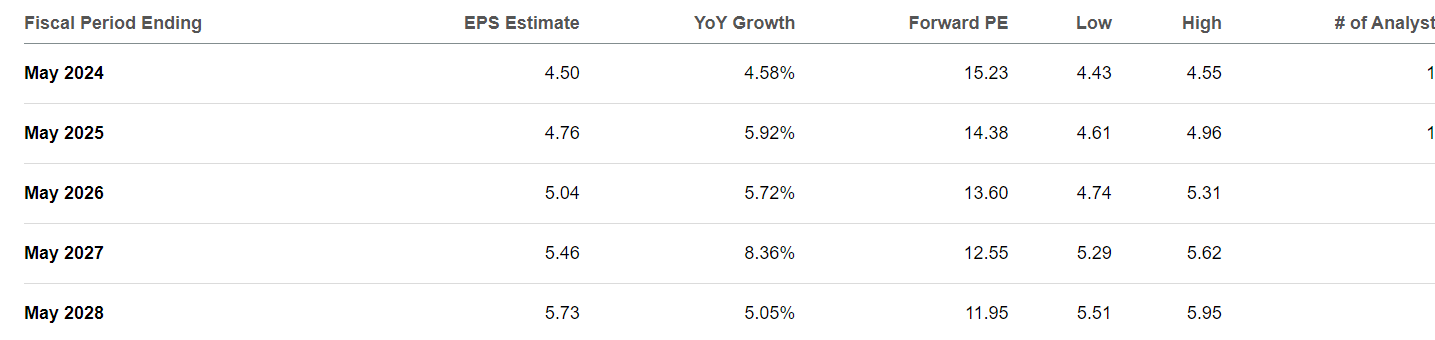

This is why the stock looks overvalued at the current valuation of 15.27x expected forward GAAP earnings. Analysts are only projecting this food maker to grow earnings at 5-7% over the next 5 years, and the company's continued margin compression and struggles growing net sales suggest these estimates are likely at least modestly too high.

{kind=link}

A chart showing analyst's earnings expectations for General Mills (Seeking Alpha)

A company struggling to grow earnings at more than a mid-single digit rate should not trade at more than 12-13x forward earnings. Even though General Mills obviously has many iconic brands and the company's core business model isn't that cyclical, management's pricing power clearly has limitations even in the US, and the company's international sales growth has been unimpressive for some time. Most of General Mills' core brands have reached a saturation point in the US because of how well-known these products are as well. While there is a scenario where General Mills could outperform if input costs were to come down, or the company were to develop a better plan to grow international sales, management has not articulated a plan to deal with the company's main challenges right now.

Iconic companies don't always make strong investments, and while General Mills has focused on shareholder returns by consistently raising the company's dividend that is currently at 3.45%, the current yield is minimal with the rate of inflation still above 3%. General Mills' pricing power is showing limitations, and management still has no clear plan to reverse the margin compression and slowing sales volume the company has struggled with for multiple quarters. Investors should be able to find better alternative investments right now.

For further details see:

General Mills: Upside Will Likely Be Limited At Current Levels