GCO - Genesco: Promising Initiatives But Upside Is Limited

2023-09-07 10:33:33 ET

Summary

- The company's revenue decreased by 2.3% YoY, while adj. operating loss (% of revenue) reached 1.9%.

- The decrease in growth rates and profitability in the main segment (Journeys Group) continues to have a negative impact on the consolidated financial results.

- I expect the company's financials to continue to be under pressure in the coming quarters, while the stock valuation no longer looks cheap.

Introduction

Shares of Genesco ( GCO ) have fallen 28% YTD. Despite the fact that the company's financials look better than expected under pressure from macro headwinds, I believe that at the moment the upside potential of the quotes is limited.

Investment Thesis

First, I think that the pressure from macro headwinds will continue to have a negative impact on consumer spending and, accordingly, the dynamics of revenue growth in the coming quarters. Secondly, despite the fact that the company's management has announced a number of initiatives to improve operating and financial performance in the Journeys segment, I think that we can see the results from innovations only next year, while in the coming quarters I expect additional pressure on operating profit due to reduced economies of scale and additional marketing costs. Thirdly, stock quotes have grown strongly over the past 4 months, as a result, the company is already relatively not cheaply valued in accordance with multiples.

Company Overview

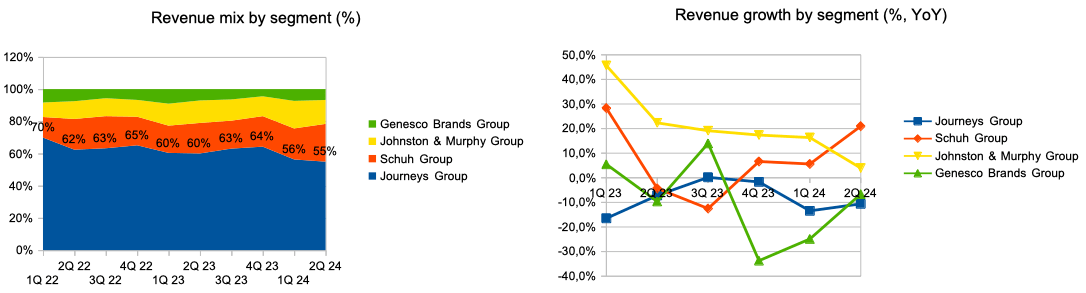

Genesco sells apparel, footwear, and accessories. The main segments are Journeys Group (55% of revenue), Schuh Group (23% of revenue), Johnston & Murphy Group (15% of revenue), and Genesco Brands Group (7% of revenue). The main sales channels are online and offline. At the end of the quarter, the company operates 1,375 stores. The company operates in the US, Canada, UK, Republic of Ireland, and Puerto Rico markets.

FQ2 2024 Earnings Review

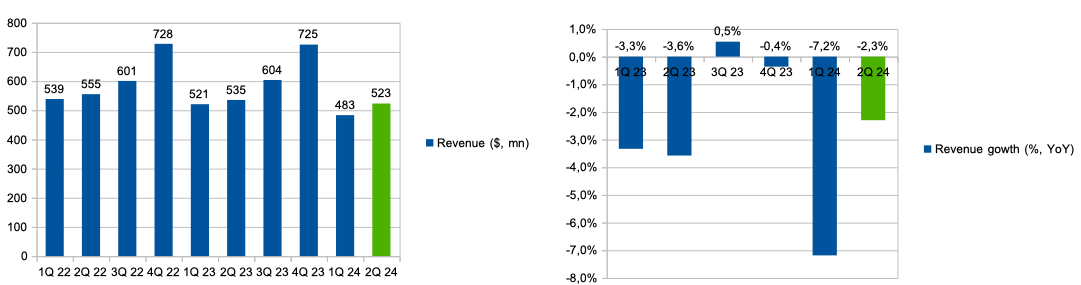

The company's revenue growth continues to be in the negative zone due to pressure on the consumer from macro headwinds. Despite the fact that some of the company's brands (Schuh, Johnston & Murphy) continue to show both an increase in traffic and an increase in the average check in the network's stores in the face of macroeconomic uncertainties, the main Journeys brand (about 56% of total revenue) is facing a decrease in both traffic and average check.

{kind=link}

Thus, the negative impact from the Journeys brand has the greatest impact on the dynamics of the company's financial performance. At the moment, management has already announced a number of initiatives (launching a loyalty program, expanding categories, increasing marketing spending, using social media to increase brand awareness) that are aimed at repositioning the brand in an ever-changing consumer behavior, which can help restore momentum, growth in sales, and operating margin in the segment.

{kind=link}

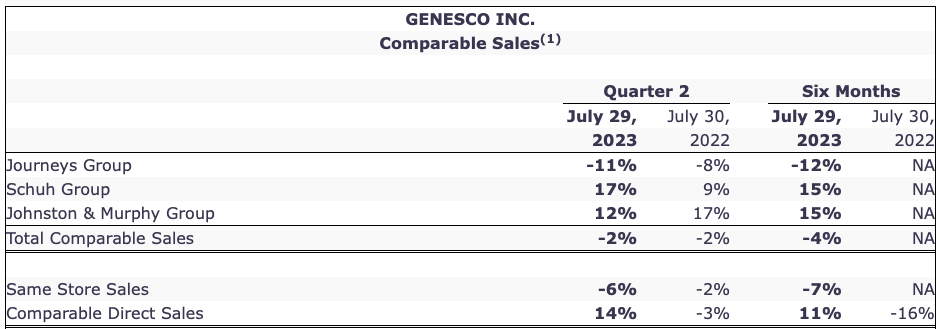

The company reported better than investors expected in FQ2 2024 . The company's revenue decreased by 2.3% YoY due to a decrease in comparable sales by 2% YoY. The biggest contributor to the revenue decline was the Journeys Group segment, where revenue decreased by 11% YoY as a result of an 11% YoY decrease in comparable sales, while in the Schuh Group segment, revenue increased by 21% YoY thanks to a 17% increase in comparable sales. You can see the details of the change in comparable sales (%) for each segment in the chart below.

Comparable sales by segment (Company's information)

{kind=link}

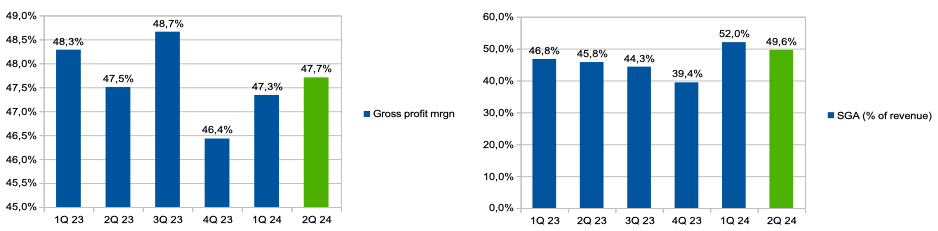

Gross profit margin increased from 47.5% in Q2 2023 (fiscal) to 47.7% in Q2 2024 (fiscal). SGA spending (% of revenue) increased from 45.8% in Q2 2023 (fiscal) to 49.6% in Q2 2024 (fiscal) due to reduced economies of scale.

Gross profit margin and SGA (% of revenue) (Company's information)

{kind=link}

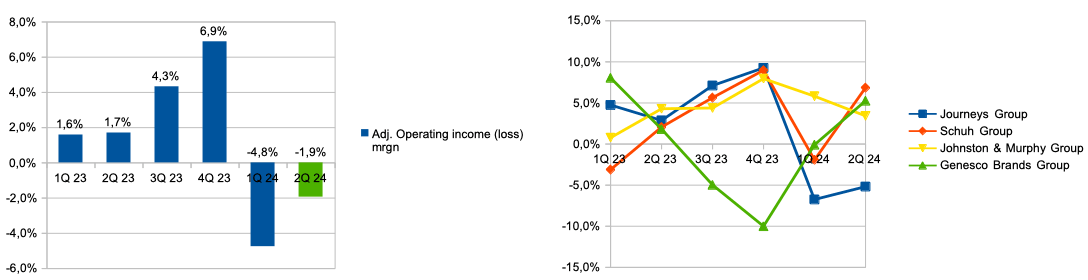

Thus, the adjusted operating loss (% of revenue) increased to 1.9%, while in Q2 2023 (fiscal) the company showed a positive operating margin of 1.7%. I am using adjusted. operating income, because in FQ2 24 the company incurred a one-off cost of $28.5 million on goodwill impairment.

The Journeys Group and Johnston & Murphy Group segments made the largest contribution to the decline in operating margins, where margins fell to -5.2% and 3.4%, respectively, while in the Schuh Group and Genesco Brands Group segments' profitability recovered to 6.9% and 5.3%, respectively.

Adj. op. income (loss) margin & by segment (Company's information)

{kind=link}

The company has confirmed its guidance for 2024 (fiscal). Thus, management expects revenue and profitability to continue to be under pressure relative to the previous year. You can see the details in the chart below.

Guidance (Company's information)

My Expectations

Although some of the company's brands (Schuh, Johnston & Murphy) posted solid growth rates, I believe that consolidated revenue growth will continue to be under pressure in the next two quarters. First, I don't expect to see a quick recovery in consumer spending as inflation continues to be relatively high. Secondly, the company's guidance for the second half of 2024 (fiscal) assumes revenue growth in the range of -3.4% to 0.2%.

While we were encouraged to see some pickup in trend in Q2, we believe it's prudent to stay cautious given the lack of visibility into an acceleration in consumer demand or economic improvement.

Overall, though, we're not planning for a major change in trend for the balance of the year.

In addition, I would like to separately note the initiatives that the management is implementing to improve financial performance in the Journeys segment (growth in traffic, sales, profitability), such as: launching a loyalty program , using digital channels for promotion, changing the assortment.

On the one hand, I think that the successful implementation of plans to restore the main business segment (55% of revenue) can become a solid growth driver for the shares and lead to a revaluation by analysts, however, on the other hand, I think that in the coming quarters, we will not see a significant improvement in financial performance in the segment as business transformation may take time, however, I expect that additional spending on marketing, loyalty program and investment in prices may put pressure on operating margins in the next 2 quarters.

Moreover, I think that at the moment the company has limited potential to cut costs to increase profitability, because a high part of the company's operating expenses is fixed (rent, salaries), which leads to a deleverage effect in the face of reduced business volume.

Drivers

Margin: The reduction in the number of Journeys-branded stores (planning to close an additional 46 stores by the end of fiscal 2024) could support the consolidated profitability of the business as management cuts those stores that are less efficient in line with Journeys' financial improvement initiatives.

Revenue: An increase in average ticket and traffic in the Journeys segment due to the launch of a loyalty program and a change in the marketing company can support both business growth and operating margins in the future.

Risks

Margin: Deleverage effects from business scale-down and price investments due to increased competition or high inventory levels could have a negative impact on profitability in the coming quarters.

Macro (general risk): A decline in real income as a result of high inflation could lead to lower consumer spending in the discretionary segment, which could have a negative impact on future revenue growth.

Valuation

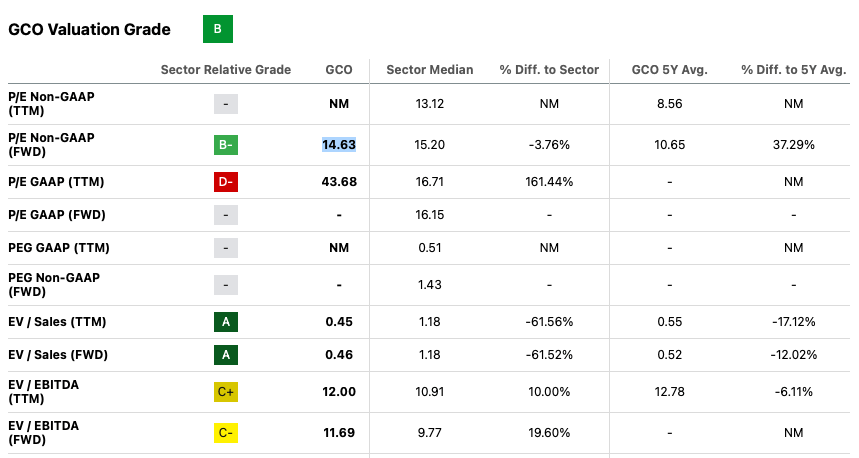

Valuation Grade is B. Based on P/E ((FWD)) and EV/EBITDA ((FWD)) multiples, the company trades at 14.6x and 11.7x, which implies a discount to the sector median of about 4% and a premium to the sector median of about 20 %, respectively.

I believe the company's shares are fairly valued, so at the moment I don't see a fundamental upside. On the one hand, according to the EV/EBITDA ((FWD)) multiple, the company's shares are already trading at a premium to the sector median, I think this is due to the fact that some of the company's brands continue to show solid growth and profitability. However, on the other hand, I believe that: 1) the company deserves a discount due to the size of the business, and 2) after the growth of prices over the past 4 months, the stock valuation does not look cheap. In addition, I do not see additional growth catalysts/drivers in the next 2 quarters.

{kind=link}

Conclusion

I expect topline and margin pressures to continue in the coming quarters as the company's shares are no longer cheaply priced by multiples. Thus, at the moment, my recommendation is hold .

I like the current initiatives for the core Journeys Group segment, so I'm happy to change my recommendation to buy when I see the first signs of less pressure on consumers and traffic growth in the Journeys Group segment. In addition, I would like to note the confidence of the company's CEO regarding plans to improve the Journeys Group.

Importantly, I want to underscore, again, the conviction I have in our ability to address Journeys' challenges and achieve success just as we have demonstrated with our other businesses.

For further details see:

Genesco: Promising Initiatives, But Upside Is Limited