CA - Gibson Energy Offers A 7.6% Divided Yield With A Sub-65% Payout Ratio

2024-01-13 11:40:00 ET

Summary

- Gibson Energy Inc. is an overlooked oil infrastructure play with a strong operating history and low payout ratio.

- The recent acquisition of the South Texas Gateway Terminal should provide a significant contribution to Gibson's EBITDA in FY 2024.

- The company's distributable cash flow is expected to increase, allowing for a well-covered dividend yield of 7.6%.

Introduction

As describer in a previous article, Gibson Energy Inc. ( GEI:CA , GBNXF ) is an overlooked oil infrastructure play with a robust operating history and strong contracts in place. The company was generating a substantial amount of free cash flow ("FCF") and paid a generous dividend with a relatively low payout ratio.

{kind=link}

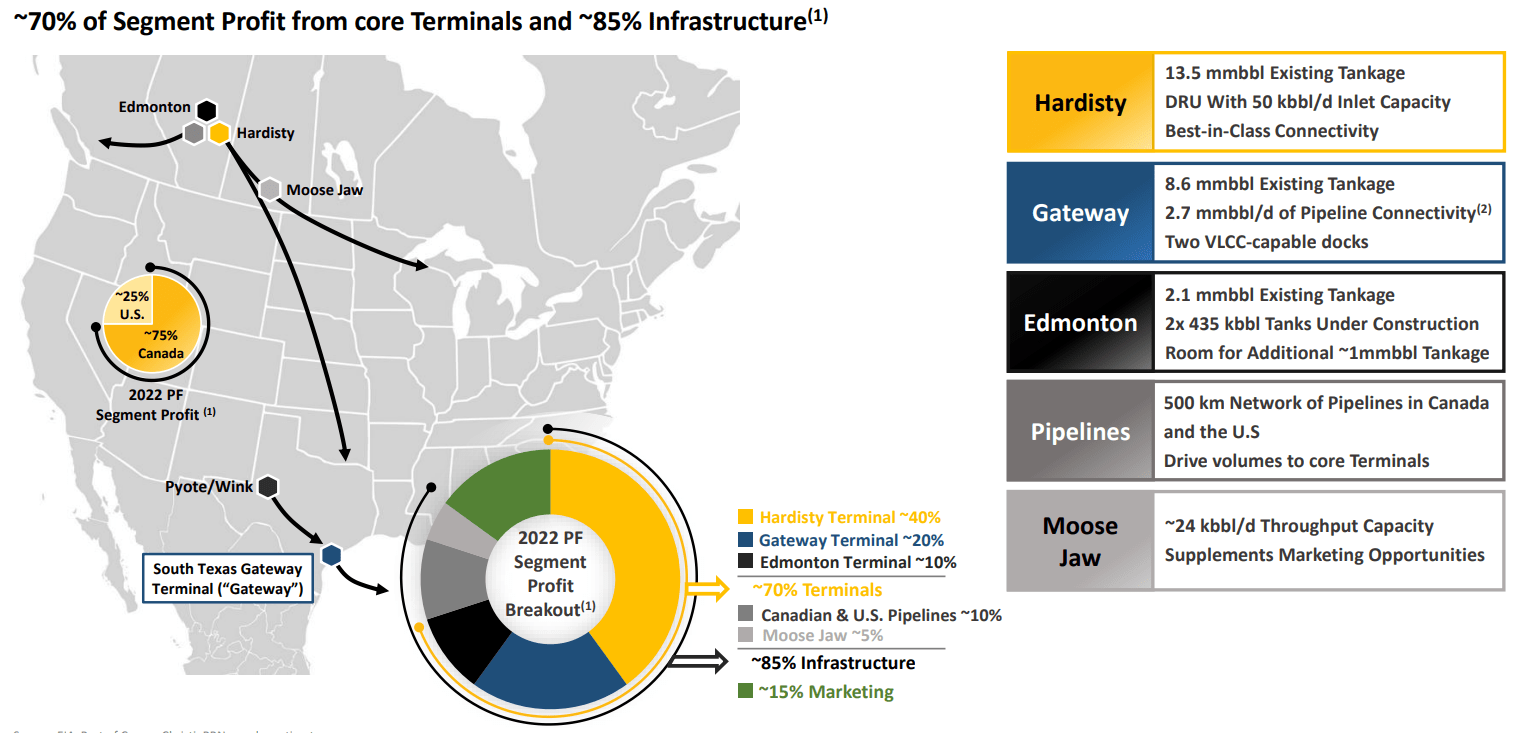

And although I wasn’t very impressed with the multiples it bought the C$1.46B South Texas Gateway Terminal for, that acquisition does provide an interesting diversification away from being a pure Canadian player.

Gibson’s 2023 will be very encouraging

As Gibson only closed the acquisition of the South Texas Gateway Terminal on August 1 st , the EBITDA contribution from the acquisition to the Q3 results remains limited to two months . This means the fourth quarter of 2023 was the first quarter wherein the recently acquired C$1.46B terminal will provide a full contribution.

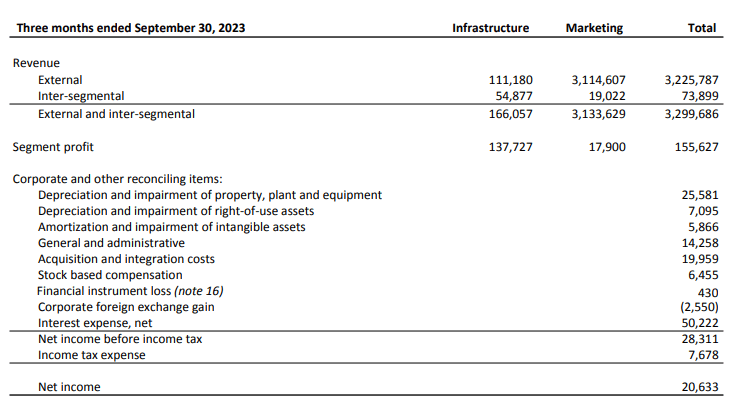

As explained in my previous articles on Gibson, you shouldn’t be too worried about the very low gross profit margin of just around 4%. The total revenue (and cost of sales) are skewed by the marketing segment , where the gross profit margin was just over 0.5% during the third quarter.

{kind=link}

And it’s not the marketing division, but rather the infrastructure division, that is the real moneymaker. That also explains why you shouldn’t really look at Gibson’s net profit of just C$20.6M considering this includes relatively high depreciation and amortization expenses as well as a non-recurring $20M acquisition and integration cost. The main metric you should use for Gibson is the distributable cash flow result.

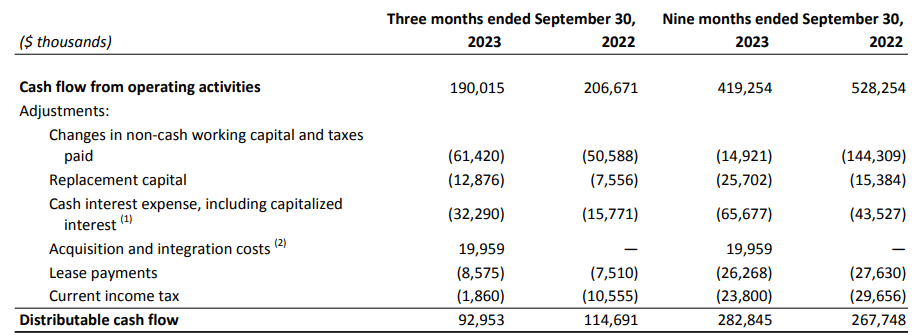

We know the company generated C$190M in operating cash flow, but this includes a very substantial working capital release. As you can see below, that working capital release gets adjusted while the company also deducts the sustaining capex, lease payments and interest payments. And the almost C$20M in acquisition-related expenses are added back to the equation to calculate the ‘normalized’ distributable cash flow.

{kind=link}

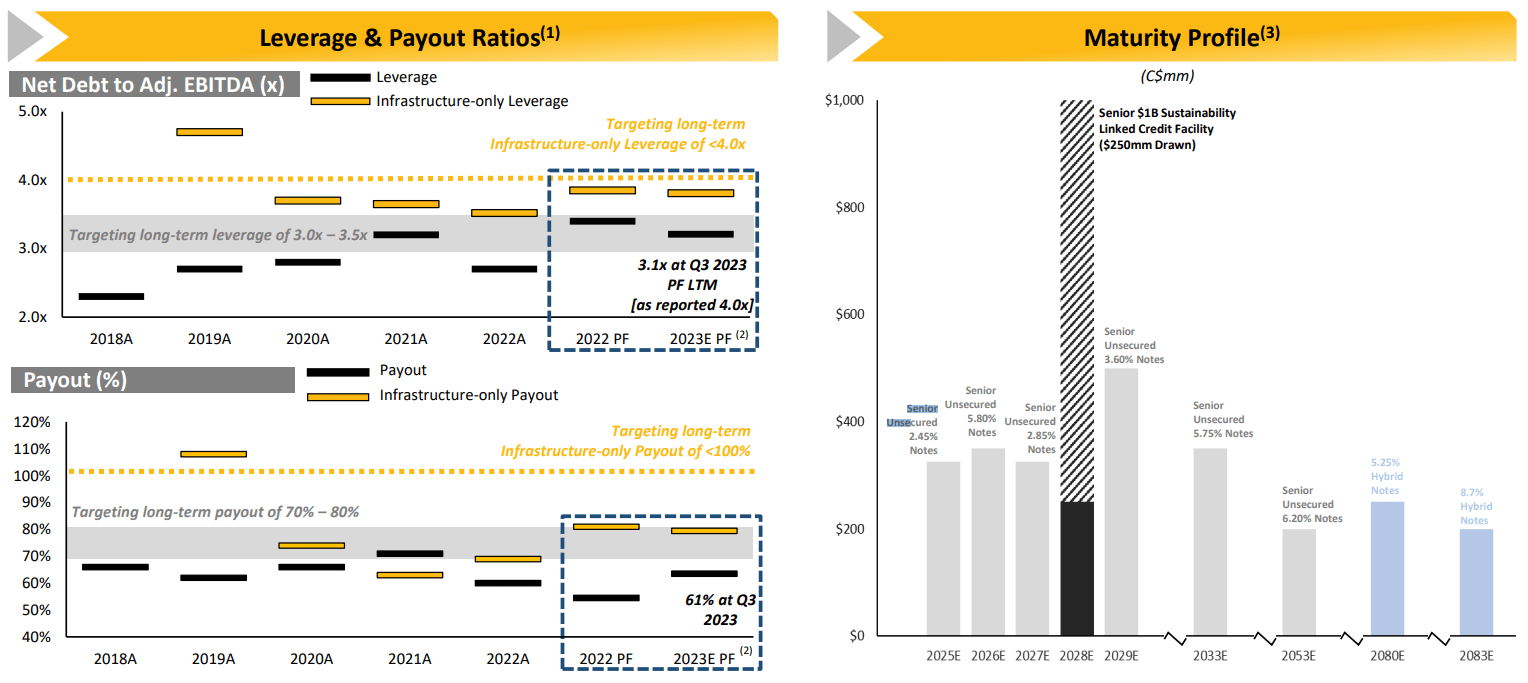

That came in at just under C$93M. There are currently 161.7M shares outstanding, resulting in a net distributable cash flow of C$0.57 per share. Note: this should increase on a going forward basis, as the Texas Gateway terminal generates approximately C$10-12M per month in distributable cash flow. Adding another full month to the equation should further boost the quarterly distributable cash flow to in excess of C$0.60. As the company is currently paying a quarterly dividend of C$0.39, its 7.6% dividend yield is currently very well covered.

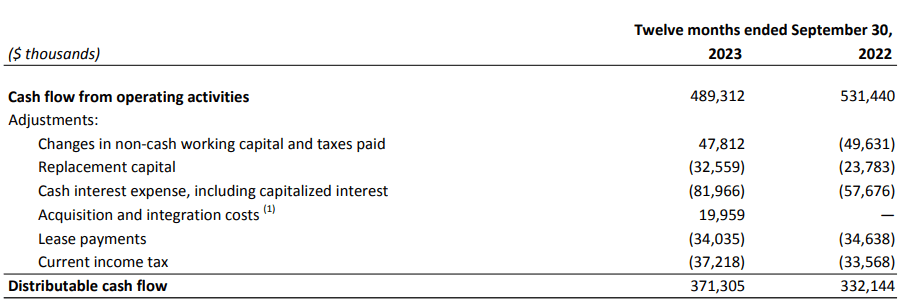

Looking at the LTM basis, the distributable cash flow was C$371M, but keep in mind this only includes a small contribution from the South Texas Gateway terminal, while this will obviously be partially offset by higher interest expenses.

{kind=link}

I think we can reasonably expect an EBITDA of C$650M next year and after deducting C$125M in interest expenses C$40M in replacement capex as well as C$35M in lease payments and C$45M in tax payments, the distributable cash flow could reasonably be expected to come in at C$405M which is approximately C$2.50 per share. That’s a little bit lower than the C$450M I was anticipating before, but I am erring on the side of being cautious when it comes to the interest payments and tax payments (during the Q3 conference call , Gibson’s management guided for a C$20-25M tax bill) as well as the C$650M EBITDA (the consensus estimate calls for an EBITDA of almost C$665M).

The initial guidance for 2024 bodes well for income investors

We know the dividend is currently C$1.56 per share, and I think it is fair to assume an increase to C$1.60, which would mean there’s approximately C$145M on the table for the company to either spend it on additional growth initiatives and/or reducing the net debt.

There is no real urgency to reduce the net debt. While the debt ratio was approximately 4 times EBITDA on a reported basis, keep in mind this doesn’t take 10 months of South Texas Gateway EBITDA contribution into account. According to the company, the debt ratio was just 3.1 times the pro forma LTM EBITDA result.

{kind=link}

This means the company is still in its preferential leverage ratio of 3-3.5 times EBITDA on a consolidated basis, while the infrastructure-only leverage has a hard ceiling of 4 times EBITDA.

As there is no real need to deleverage, even after the large acquisition, Gibson can and will invest the "excess" cash flow in additional growth. In its 2024 guidance, the company mentioned a C$125M growth capex budget . As Gibson traditionally has a ROCE in the mid-teens, I’m fine with these growth investments, as a C$125M budget can easily add C$15-20M in incremental EBITDA and C$10-15M in additional free cash flow per year.

Investment thesis

I currently have a long position in Gibson Energy, and I am still writing put options that are slightly out of the money in an attempt to get my hands on more shares below the C$20 mark. The distribution is very well covered, and as the company’s leverage will remain around the 3 times EBITDA mark, I understand its focus on growth, especially if it can generate returns in the mid-teens on the newly invested capital.

At the current share price, the Gibson Energy distribution yield is approximately 7.6% and if the distribution indeed gets hiked to C$0.40 per quarter, the yield increases to approximately 7.75%. Considering this represents a payout ratio of less than 65% even in my conservative DCF calculation for 2024, the Gibson Energy Inc. distribution should be safe.

For further details see:

Gibson Energy Offers A 7.6% Divided Yield With A Sub-65% Payout Ratio