GLASF - Glass House Brands: Worth Keeping An Eye On

2023-12-09 05:44:21 ET

Summary

- Glass House Brands Inc. has attractive gross margins, yet is currently forced to pay taxes under 280e.

- They expect to have additional production capacity come online in Q2 of 2024.

- The cannabis industry faces potential catalysts from both rescheduling and the adoption of some version of the SAFE Banking Act.

- With a forward EV/EBITDA of 16.4x, and a Price/Cash Flow of 26.03x, I view the company as presently overvalued.

- I currently rate GLASF a Hold.

Thesis

I have been researching cannabis companies since the industry-wide rally in early 2021. With most of the industry unable to find positive cash flow through the 280e tax obligation, a majority of the operators in the United States have been unable to find positive cash flow or net income.

Glass House Brands Inc. ( GLASF ) has been increasing its revenue and gross profits. They have managed to find positive cash flow for the last three quarters, and came close to positive net income this most recent quarter. This distinguishes them as one of the few cannabis companies in the United States which appear to be investible. After looking over their financials and valuation, I presently rate Glass House as a Hold.

Company Background

Glass House is a vertically integrated cannabis company which operates in California. They maintain 6 large greenhouses with a total of 5.5M sq.ft. of cultivation footprint. In addition to selling wholesale, they also maintain 10 retail storefronts . They were founded in 2015 and are headquartered in Long Beach, California.

Long-Term Trends

The California legal cannabis market is expected to grow at CAGR of 12.2% through 2030. The United States cannabis industry is expected to experience a CAGR of 14.2% until 2030.

Guidance

Their most recent earnings call transcript indicates that they believe the DEA may make an announcement about rescheduling before the end of the year.

{kind=link}

Guidance 1 (Q3 2023 Earnings Call Transcript)

They are operating under the framework that pressure to reschedule will rise leading into the 2024 presidential election.

{kind=link}

Guidance 2 (Q3 2023 Earnings Call Transcript)

They are also expecting that public sentiment will encourage interstate commerce.

{kind=link}

Guidance 3 (Q3 2023 Earnings Call Transcript)

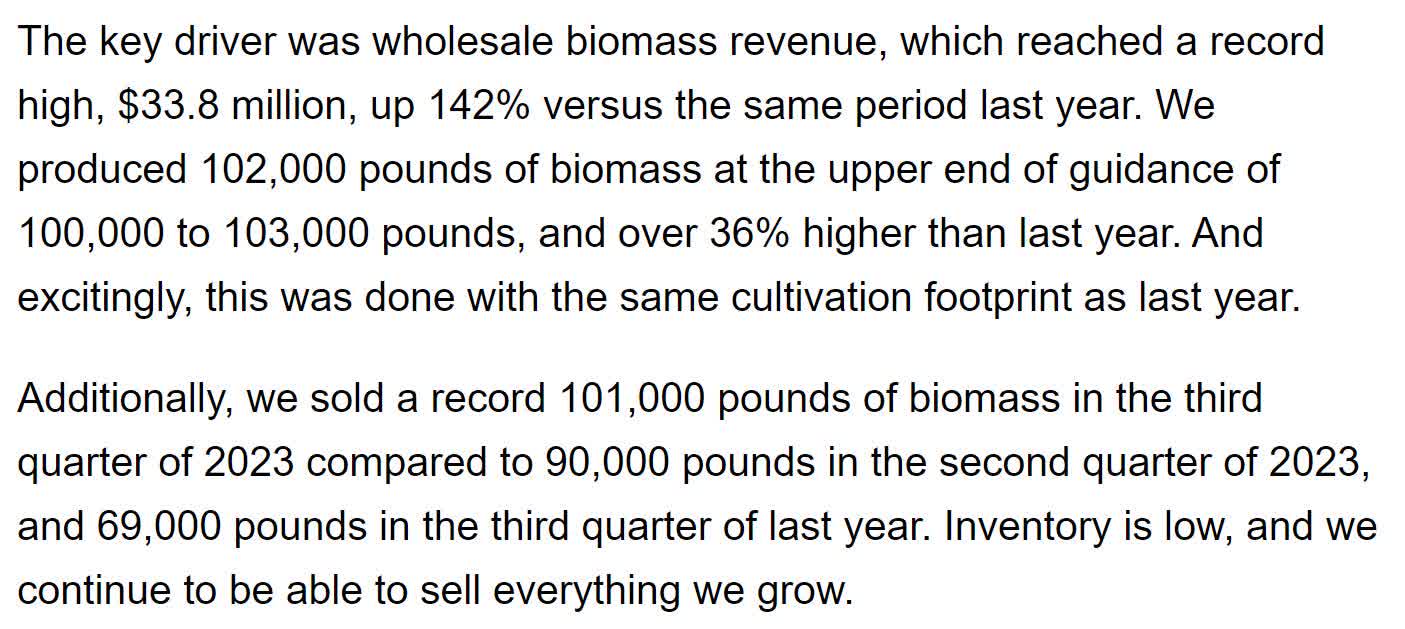

Their revenue from biomass has risen significantly over the last year.

{kind=link}

Guidance 4 (Q3 2023 Earnings Call Transcript)

They believe they will be able to realize additional cost efficiency improvements.

{kind=link}

Guidance 5 (Q3 2023 Earnings Call Transcript)

Wholesale gross margins fell by 1% to 60%, and retail gross margins increased 2% to 56%.

{kind=link}

Guidance 6 (Q3 2023 Earnings Call Transcript)

They attribute a majority of their Adjusted EBITDA improvements to higher volume of wholesale biomass.

{kind=link}

Guidance 7 (Q3 2023 Earnings Call Transcript)

Their cash balance had increased to $37.9M at the end of the quarter. Their preferred equity raise produced $10.9M in inflows from the first round. They have received an additional $1.9M from the second one, with another $1.6M of inflows in the time between the quarters end and the earnings call. They expect to attain an additional $0.6M, and for the total amount raised from preferred equity to end up at $15M.

{kind=link}

Guidance 8 (Q3 2023 Earnings Call Transcript)

The number of active cultivation licenses in California has been in decline. They expect that the pace of decline will slow.

{kind=link}

Guidance 9 (Q3 2023 Earnings Call Transcript)

Total market sales in California fell 11% compared the third quarter of last year. Flower declined 15%, pre-rolls fell 1%, and the vape market fell 10%.

{kind=link}

Guidance 10 (Q3 2023 Earnings Call Transcript)

They project that their Q4 revenue to come in lower next quarter, ending up between $38M and $40M. While lower than this quarter, their projected Q4 revenue is still 21% higher than the previous Q4. With the lower projected revenue for Q4 and estimated $5M in taxes, they expect to have between -$2M and $5M in operating cash flow and an Adjusted EBITDA between $5M and $7M.

{kind=link}

Guidance 11 (Q3 2023 Earnings Call Transcript)

They still expect for the expansion of Greenhouse 5 to stay on schedule and to have it operational in time to make their first sales from its production in Q2, 2024.

{kind=link}

Guidance 12 (Q3 2023 Earnings Call Transcript)

Quarterly Financials

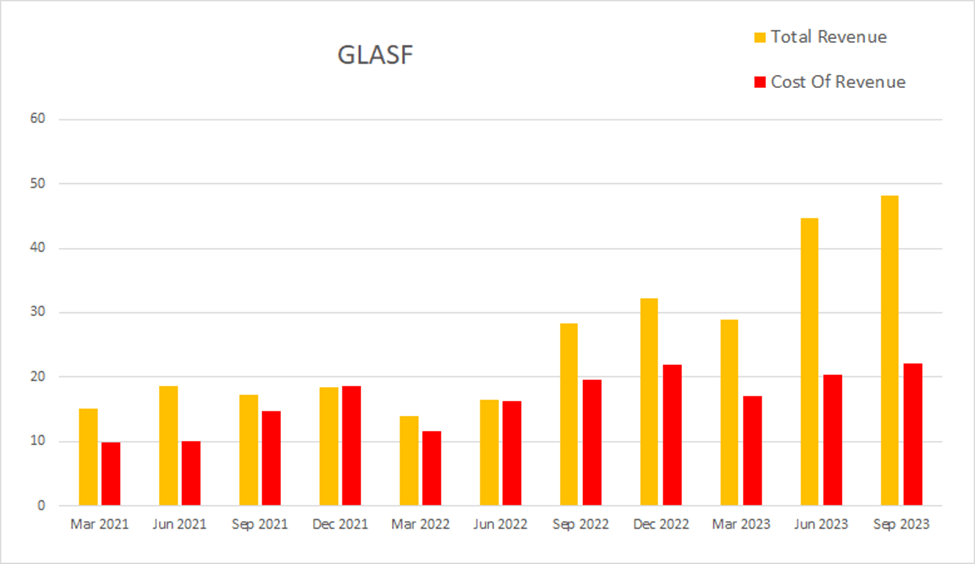

Their quarterly financials are showing revenue growth has been outpacing cost of revenue. Eight quarters ago, Glass House had a quarterly revenue of $17.2M. Four quarters ago, that had grown to $28.3M. By this most recent quarter, that had risen further to $48.2M. This represents a total two-year increase of 180.23% at an average quarterly rate of 22.53%.

{kind=link}

GLASF Quarterly Revenue (By Author)

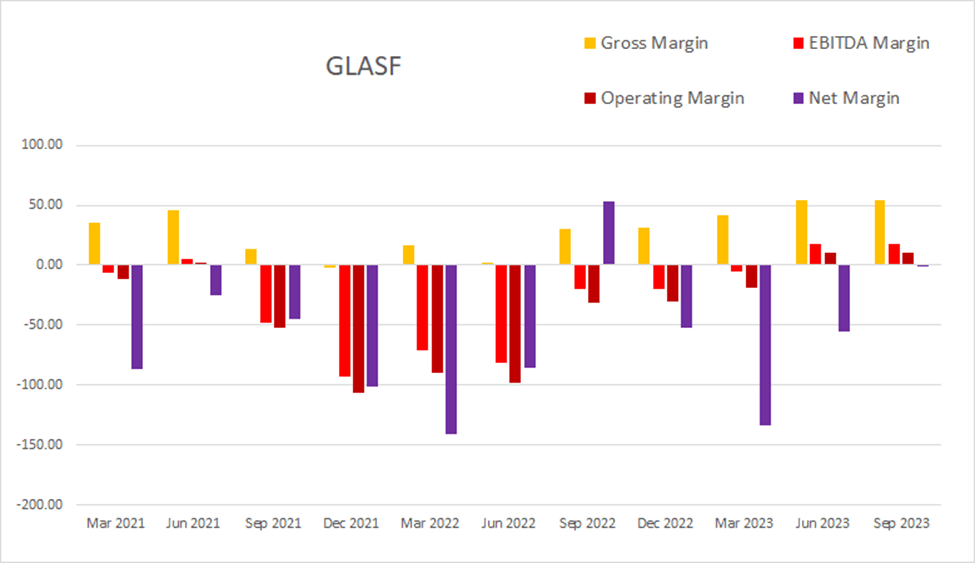

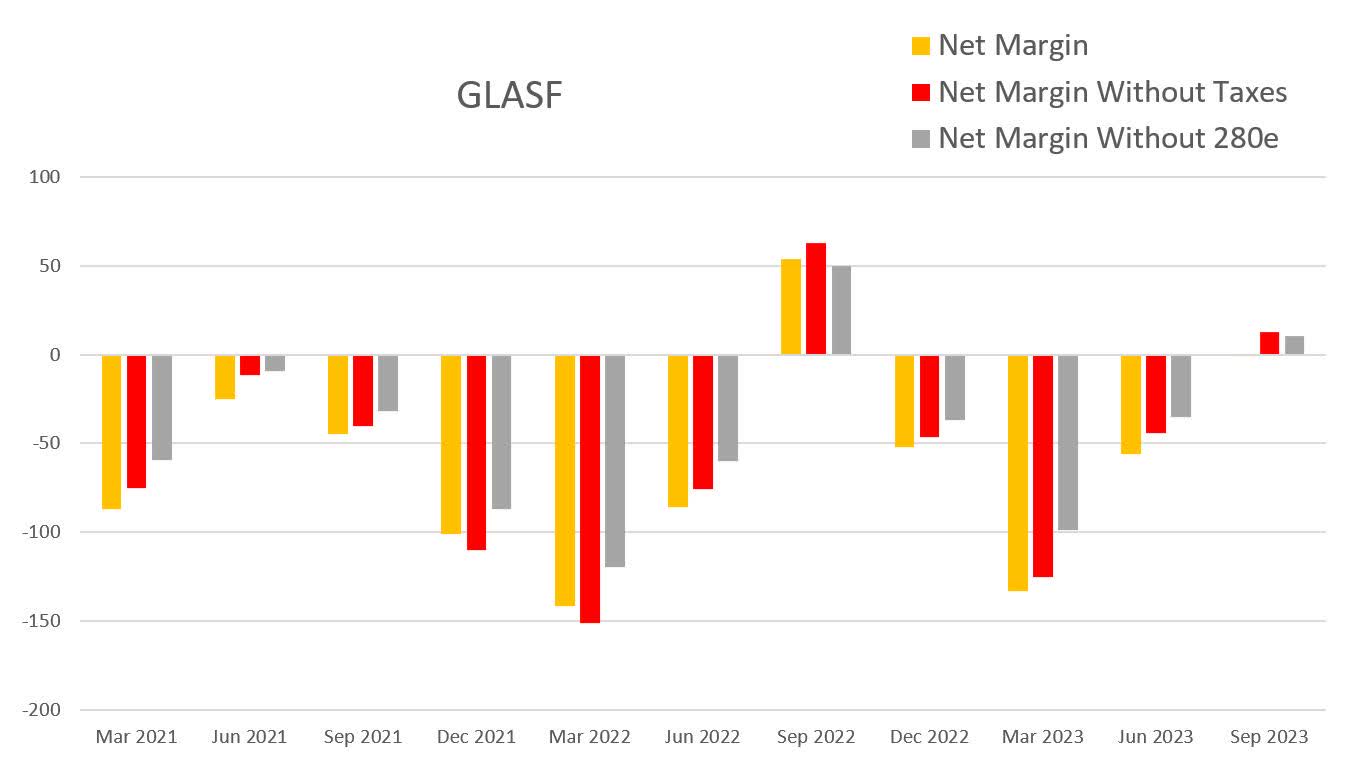

Their gross margins are significantly better than they were in late 2021 and early 2022. Both operating and EBITDA margins have been positive for the last two quarters. As of the most recent quarter, gross margins were 53.94%, EBITDA margins were 17.84%, operating margins were 10.17%, and net margins were at -0.62%.

{kind=link}

GLASF Quarterly Margins (By Author)

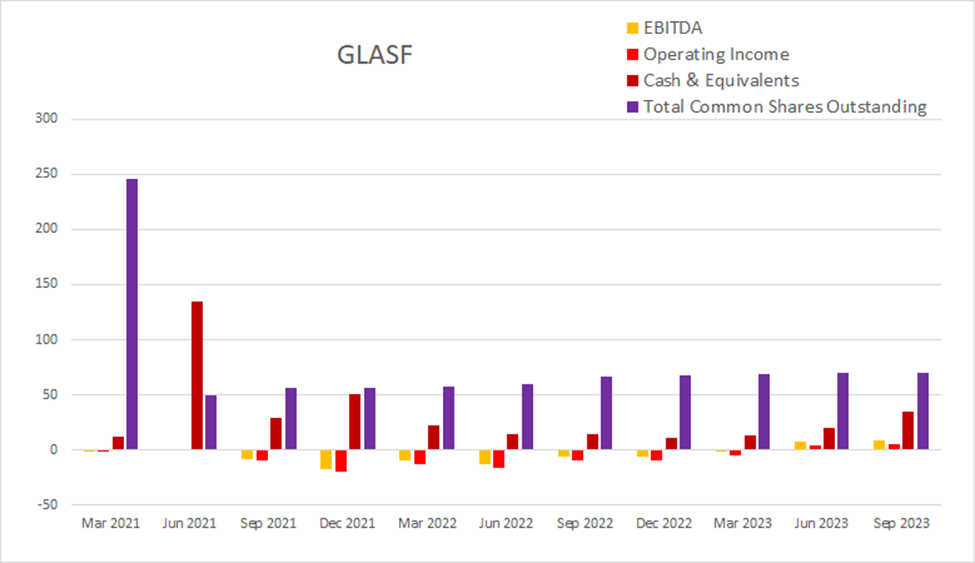

Looking only at common shares outstanding, their pace of dilution appears to have slowed. The sum of their last eight quarters of dilution comes to 21.92%; over the last four quarters this has dropped to 5.47%.

{kind=link}

GLASF Quarterly Share Count vs. Cash vs. Income (By Author)

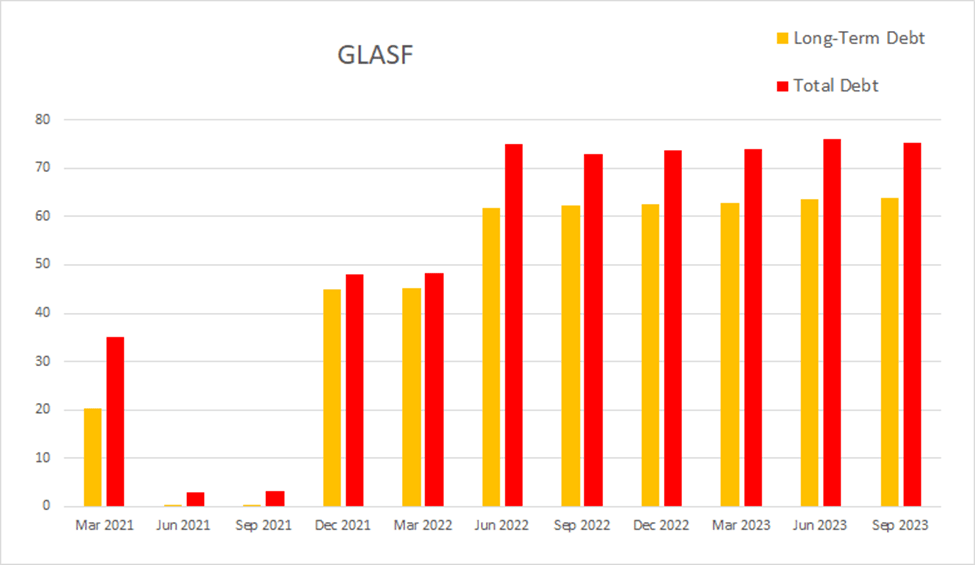

This most recent quarter, Glass House had -$2.2M in net interest expense, total debt was at $75.3M, and long-term debt was at $63.9M.

{kind=link}

GLASF Quarterly Debt (By Author)

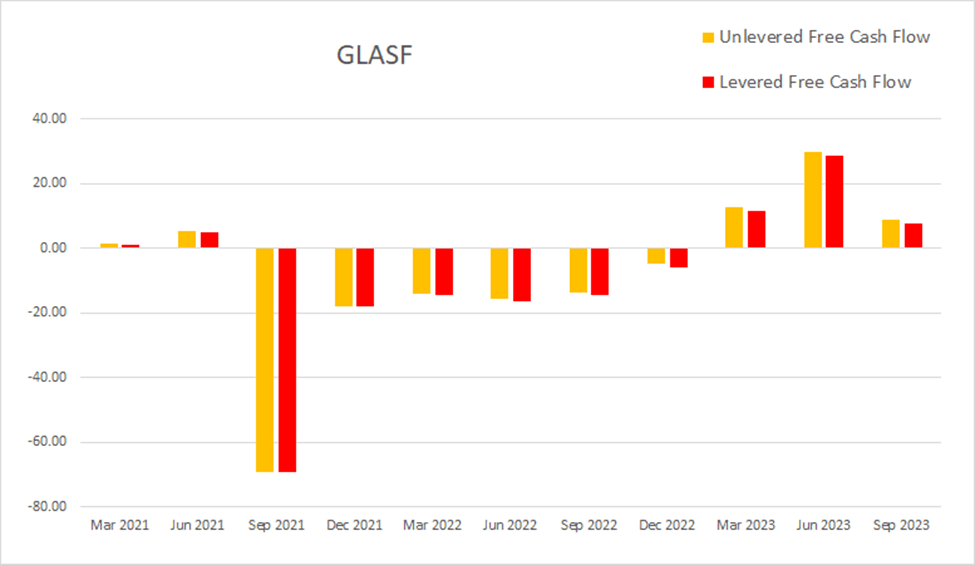

Their cash flows have been positive for the first three quarters of 2023. As of the most recent earnings report, cash and equivalents were $35M, quarterly operating income was $5M, EBITDA was $8.6M, net income was -$0.3M, unlevered free cash flow was $8.7M, and levered free cash flow was $7.6M.

{kind=link}

GLASF Quarterly Cash Flow (By Author)

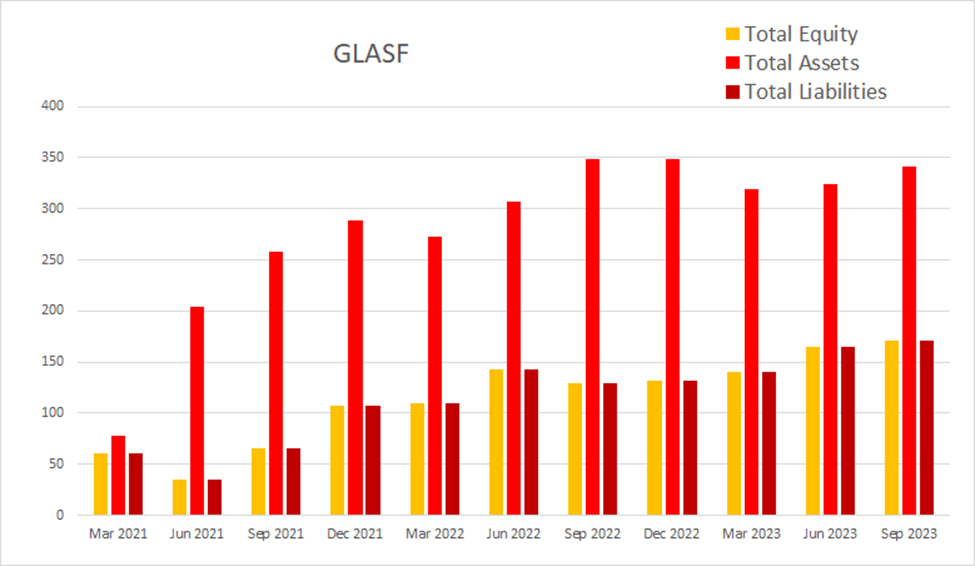

With the exception of a drop in mid-2022, total equity has been rising since Q2 of 2021.

{kind=link}

GLASF Quarterly Total Equity (By Author)

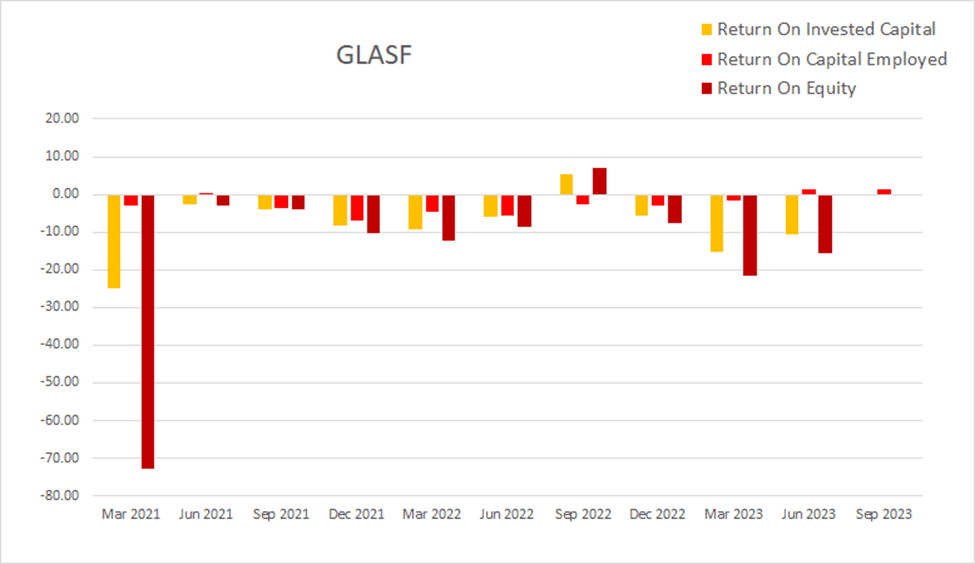

As of the most recent earnings report, ROIC was -0.12%, ROCE was 1.48%, and ROE was -0.18%.

{kind=link}

GLASF Quarterly Returns (By Author)

Post-Rescheduling

Their net margins should improve significantly once cannabis is rescheduled. By adding their income tax expense to their net income, and then subtracting a 21% corporate income tax from that sum, I can produce rough estimates for their post-rescheduling net margins. If they weren't currently operating under 280e , they would have posted a net margin of about 10.17% this most recent quarter.

{kind=link}

GLASF Post-Rescheduling (By Author)

Valuation

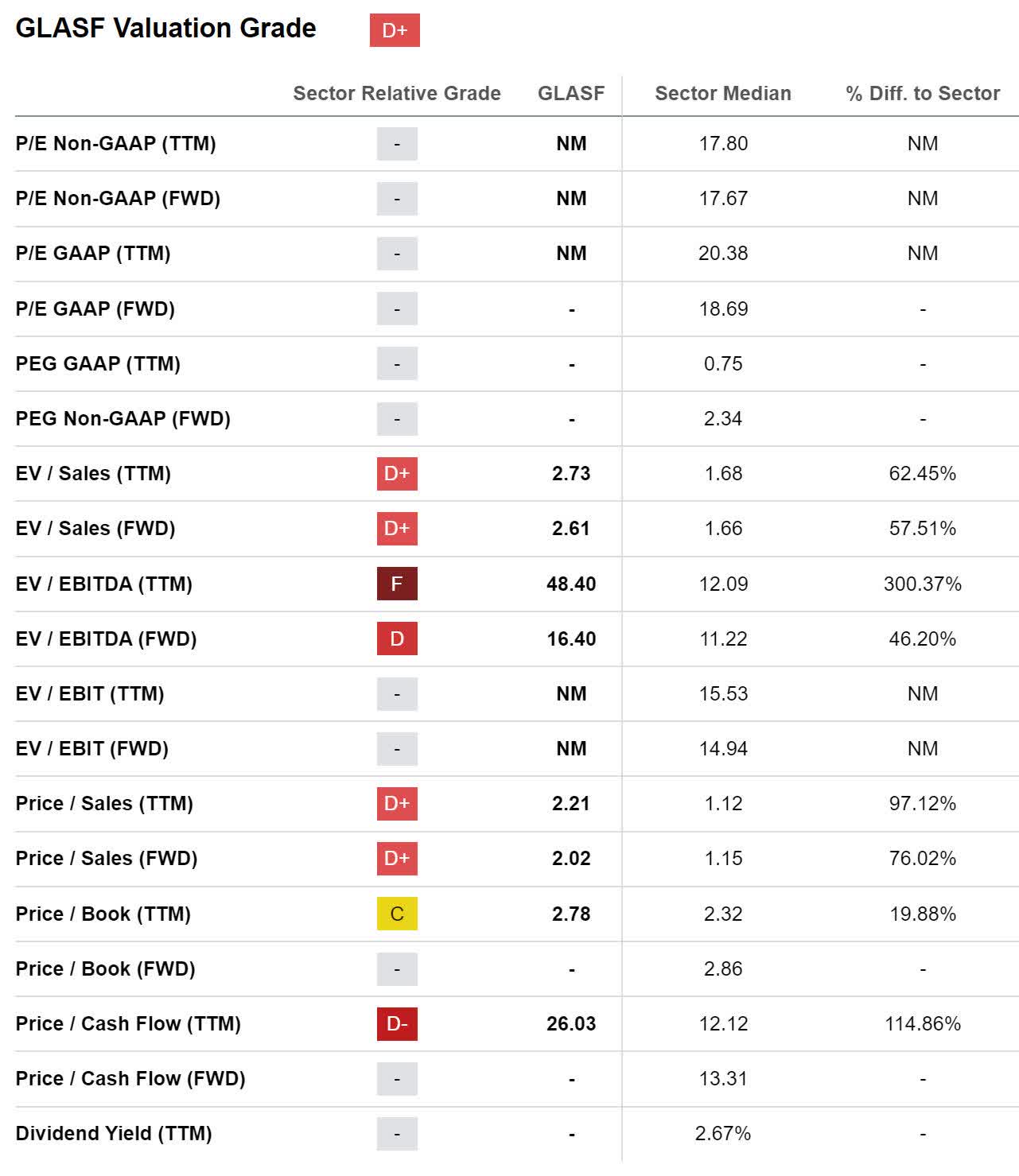

As of December 8th, 2023, Glass House had a market capitalization of $324.42M and traded for $4.58 per share. With a forward EV/EBITDA of 16.4x, and a Price/Cash Flow of 26.03x, I view the company as presently overvalued.

{kind=link}

GLASF Valuation (Seeking Alpha)

Risks

Glass House uses large greenhouses to produce their cannabis. While this gives them significant control over watering and humidity control, they are still subject to problems from extended periods of cloud cover.

Catalysts

The entire industry faces potential catalysts from both rescheduling and the passage of some form of the SAFE Banking Act . In response to Biden's request to review the scheduling of cannabis, the DHHS has already concluded it should be moved to schedule 3, but the Federal government is still waiting on the findings of the DEA before the process can continue.

If the efficiency improvements the company believes are possible are realized, it should lead to more attractive margins and returns. If those improvements are sustained, then this should lead to valuation improvements.

Conclusions

Overall, Glass House appears to be one of the more attractive potential cannabis investments. They have been growing revenue, and are working toward bringing additional production capacity online. With their valuations already rather high, and their projection that revenue will be lower next quarter, I am hesitant to hand out a Buy rating until we get next quarter's results and guidance. I suspect the additional production capacity they expect to begin coming online Q2, 2024 will allow their already attractive gross margins to pull gross profit higher. If the revenue improvements are significant enough, and gross margins are maintained at an attractive level, this may leave the company with high enough gross profit to overcome their expenses.

While I am currently placing a Hold rating on them right now, I believe this company is worth watching. When rescheduling arrives, I expect that Glass House will take part in the industry-wide rally. Even if rescheduling is delayed significantly, Glass House has positioned itself into a situation where they can expect to have improving financials in the future. If their financials improve by enough in future quarters, I will change my recommendation to a Buy rating.

For further details see:

Glass House Brands: Worth Keeping An Eye On