CA - Going Into 2023: Where We Are In The Oil Cycle What's My Best Pick - Cathedral Energy

Summary

- The recent mini-crash in oil prices has shaken the confidence of many oil longs. It's thus time to reassess where we are in the current oil cycle.

- We should also think about what type of oil stocks are poised to deliver extraordinary gains without exposing investors to excessive volatility going forward, as we enter 2023.

- I reason below that it's an opportune time to be greedy for those who know where to find the advantageous risk-reward profiles. Cathedral Energy Services is a good case in point.

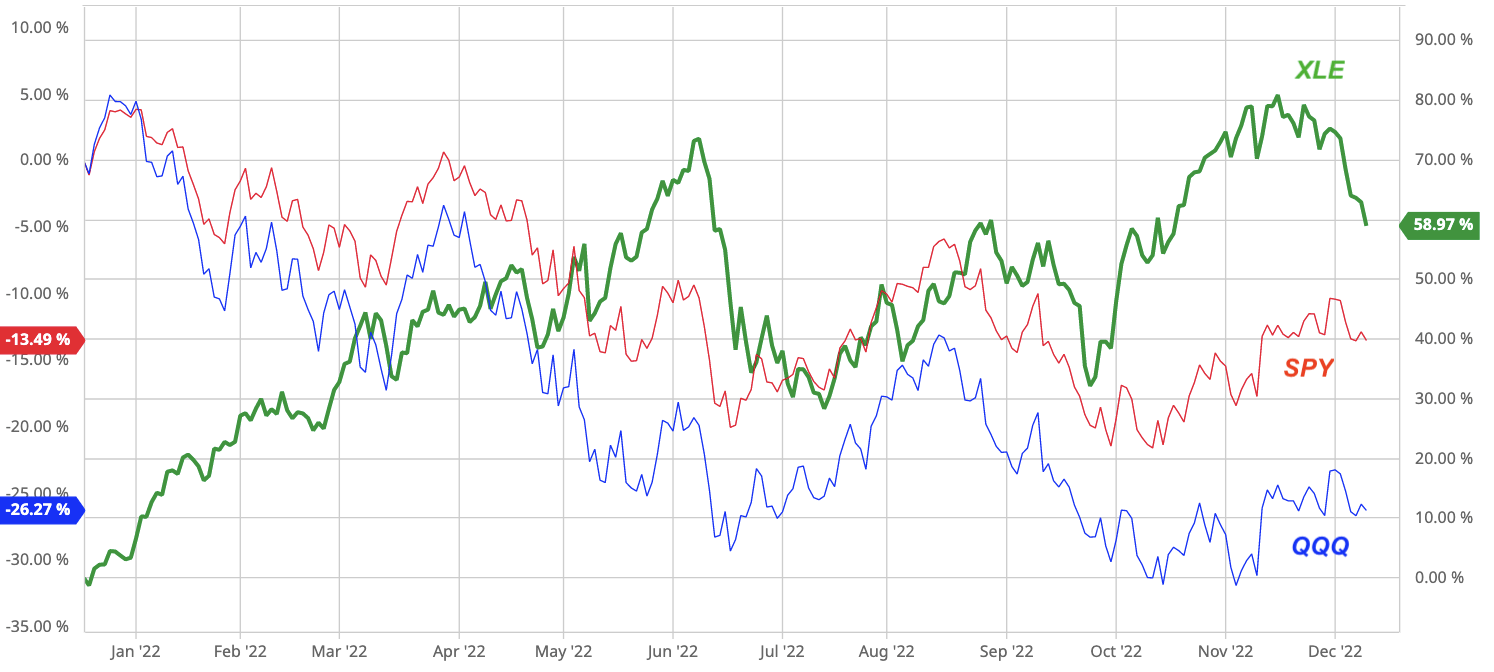

Oil and gas stocks have been some of the best performers in 2022, as shown by a comparison of Energy Select Sector SPDR ETF ( XLE ) with SPDR S&P 500 Trust ETF ( SPY ) and Invesco QQQ ETF ( QQQ ). Year to date (December 9, 2022), XLE gained 44.49%, while SPY and QQQ lost 17.67% and 29.78%, respectively (Fig. 1).

Although such a stark difference in performance is expected as part of the revenge of the old economy , it might have surprised many people, especially those who used to have a blind faith in either the supposedly secular-growth technology sector or passive index investing.

{kind=link}

Fig. 1. A comparison of three ETFs, namely, Energy Select Sector SPDR ETF ( XLE ), SPDR S&P 500 Trust ETF ( SPY ) and Invesco QQQ ETF ( QQQ ). (modified from Barchart and Seeking Alpha)

At this juncture as we are about to enter 2023, many investors wonder how they should navigate through the new year, whether it is too late to hop on the energy equity bus, and what oil and gas stocks to buy.

In this article, I attempt to answer these pressing questions using the investment approach as I discussed in detail in the 2021 and 2022 Seeking Alpha interviews, and present a small-cap best pick that I believe may deliver extraordinary gains at relatively moderate risks in 2023 and beyond.

Where we are in the oil cycle

Although nobody can precisely pinpoint by which month an oil up-cycle will kick off nor in which year it will end, to trained eyes there are observable signs that can give hints as to roughly where we are in an oil cycle.

- Typically, during a down-cycle and the early phase of an up-cycle, gun-shy oil producers slash expenses and cut capital spending, which leads to less drilling and lower production, which in turn results in supply deficit and global crude oil inventory draws. As oil prices recover, a conservative capital program helps generate a lot of cash; much of the free cash flow is directed toward debt repayment and shareholder rewards, rather than reinvestment in finding and developing oil and gas reserves.

- In the latter half of an oil cycle, the oil prices have risen to and seemingly sustain at a high level that stokes the animal spirit of the oil industry. Oil companies feel more confident such that they begin to expand their capital programs to replenish reserves and ramp up production, organically or via M&A, supported by reinvested cash flow and debt leverage. They spend more on oilfield services as these services become increasingly expensive, which leads to margin contraction. Eventually, oversupply of oil results in the build-up of inventories, and another oil crash is produced.

These days, oil companies are reluctant to allocate capital to finding new reserves and expanding production, not only because that is what western policy-makers and investors want but also because, according to Goehring and Rozencwajg , it is a rational thing to do. Why would an E&P company spend capital on finding reserves that governments are determined to make stranded? No investors want to keep handing in capital to help a producer chases production growth for the sake of mindless growth without being properly rewarded?

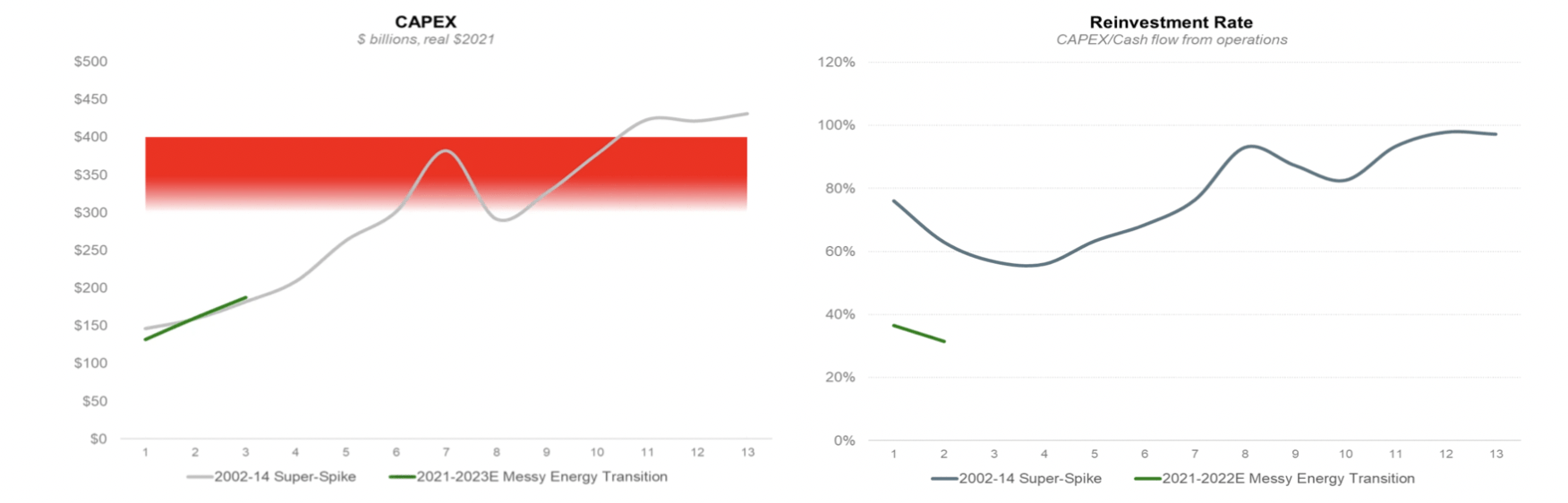

Capital spending by the oil industry is still low relative to previous oil up-cycles; so is the rate of reinvestment, which suggests the industry cycle is still in the early innings of a multi-year up-cycle (Fig. 2).

{kind=link}

Fig. 2. Oil industry CapEx and reinvestment rate, as compared with the previous up-cycle in 2002-2014 (Arjun Murti)

Thanks to the under-investment since 2014, OPEC+ has only ~2 MMbo/d of spare capacity. To conserve that spare capacity, the group decided to cut its production quota in October 2022, much to the dismay of the White House; OPEC+ already began to implement the production cut in November 2022. Meanwhile, U.S. shale producers have not been energetically ramping up production over the last couple of years and, judging from the 2023 capital budget just released by industry leaders ExxonMobil ( XOM ) and Chevron ( CVX ), they are probably not going to expand capital budget much beyond what inflating OFS costs require to maintain a flat production (Fig. 3), even though the drilled but uncompleted (or DUC) wells - essentially another form of spare capacity - have declined to the 2014 levels. Under sanctions and G-7's oil price cap, it is only a matter of time before Russian oil exports materially decline. With the exceptions of Canada and Guyana and a few other isolated cases, worldwide oil production is poised to stagnate in the foreseeable future.

Fig. 3. Weekly average U.S. oil production (Laurentian Research based on EIA data)

On the demand side, it is important to remember that global oil consumption has been in a secular growth mode for decades as driven by continual population growth and urbanization, only occasionally interrupted by flash crashes - due to recessions or pandemic - that were invariably followed by strong recoveries (Fig. 4). Global oil consumption grew at 1-2% per year in the last 20 years, which is unlikely to come to an abrupt end even under optimistic assumptions of automobile electrification. Notably, oil consumption in emerging economies grow much faster than in the OECD countries; for example, Indian oil consumption is growing at 3% per year , while air travel booms in Mexico and Thailand.

- In the near term, China is in the process of reopening from its zero-Covid policy, which had plunged the world's second largest economy into rolling lockdowns for the last three years. There will be a spike of Covid infection in the wake of the reopening; however, mass immunization is expected to occur before summertime, by which time ~2 MMbo/d of extra demand will have to be met.

- The U.S. SPR "emergency" release is coming to an end although congress-mandated SPR draws will continue; the SPR, which had been drained to the lowest level since 1983 (387 MMbo as of December 2, 2022), may be refilled at spot WTI prices of low-$70s , said the White House. It is also worth noting that U.S. commercial liquids inventories continued to draw even while SPR releases had been going on.

Fig. 4. A chart of WTI benchmark oil prices, shown with major events (Laurentian Research)

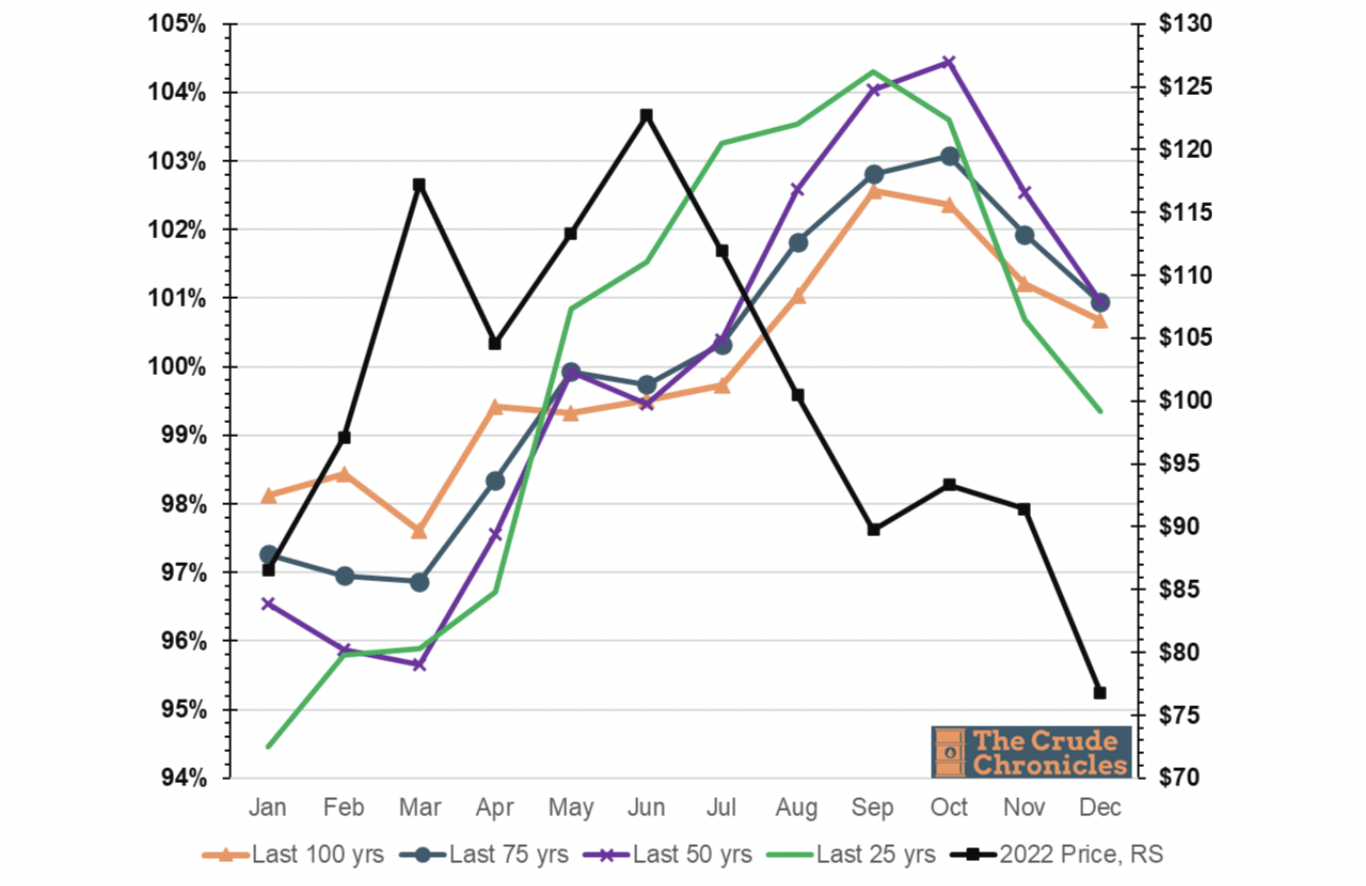

The WTI benchmark oil price dropped >42% in the last five months or 13% in the last five days. Some investors began to panic. However, let's not forget oil has been under an assault from multiple directions during this time: Chinese lockdowns, SPR releases and Russian oil price cap - all unprecedented in history - amidst lingering worries about a possible global recession induced by central bank rate hikes. Given the collective virulence of these bearish events or market manipulations, especially since June 2022 (Fig. 5), it is remarkable that WTI managed to remain above $70 per barrel, which speaks volumes of the strength of the underlying oil fundamentals.

{kind=link}

Fig. 5. Seasonality of oil prices in the past and "unseasonality" of oil prices in 2022 due to artificial manipulation (modified from The Crude Chronicles)

Going forward, as such artificial manipulative measures as SPR releases and zero-Covid conclude, we will likely find tailwinds gathering strength in the near future; we may even find the woke decarbonization movement, which is losing steam (e.g., here ), actually prolongs this oil up-cycle for the benefit of the oil industry.

Therefore, I continue to believe the structural oil bull market is intact in the medium to long term, and the physical oil supply-demand dynamic remains strong in the near term in spite of the apparent weakness in the financial oil market.

For the rest of the oil up-cycle

Warren Buffett famously quipped, " be fearful when others are greedy and greedy when others are fearful. ” I believe the ongoing pullback of the oil prices has provided investors with a great opportunity to pick up quality stocks that are highly probable to deliver extraordinary gains at relatively moderate risks for the rest of the oil cycle.

At this critical time, investors should pay special attention to the following, in stock picking:

- As discussed above, capital efficiency of E&P companies tend to decline in the latter part of the oil bull market, when the (percentage-wise) steepest oil price appreciation is likely in the rear-view mirror. As producers spend capital to pad up reserves, construct higher-breakeven production capacity, and make expensive asset acquisitions, risk will inevitably increase. With costs inflating and growth getting more expensive to achieve, an investment in an E&P stock may become more of a bet on continually rising oil prices than taking advantage of operational catalysts.

- On the other hand, the CapEx of the E&P players are the revenue of oilfield service vendors. In contrast to shrinking margins for E&P players, the margins of oilfield service companies are expected to expand thanks to strengthening pricing power. That makes OFS stocks especially attractive in the middle to late phase of an up-cycle.

To that end, I presented large-cap oilfield service ideas Schlumberger ( SLB ) and Halliburton ( HAL ) in a previous article , an investment thesis that has played out well so far and remains valid. Below, I highlight a small-cap oilfield service idea that I believe is poised to deliver much more growth than those oilfield service behemoths, but that may not expose you to excessive risk.

Cathedral Energy Services

When I first presented the idea in October 2022, I said the following about Cathedral Energy Services Ltd. (CET.TSX)( OTCPK:CETEF ):

"...Cathedral Energy Services - a North American directional drilling specialist - has transformed itself into a vibrant consolidator of its highly fragmented industry. The company is at the inflection point of a hockey stick-like curve of growth. Recent acquisitions are estimated to result in imminent, explosive growth in top line, EBITDA and free cash flow.

Yet the under-the-radar stock still trades at attractive EV/EBITDA multiples, and is still deeply-undervalued relative to industry peers. The bargain stock price may not last for much longer. The neck-breaking growth and deep undervaluation could become impossible to ignore when the company reports its 3Q2022 results in early November 2022."

The 3Q2022 results announced on November 14, 2022, give us an opportunity to examine whether the investment thesis is being proven valid.

Market share expansion

Following the transformative acquisition of Altitude Energy Partners , Cathedral expanded its share in the U.S. directional drilling market from 0.8% in 2021 to 6.5% as of the 3Q2022, with room to further expand to > 10% through further consolidation. Going into 2023, the company is poised to derive some 70% of its revenue from the U.S. market.

In Canada, Cathedral has a 24.3% market share, up from 18.1% in 2021.

Operations

In Canada, activity days were up 76.6% year-over-year, from 1,875 days in 3Q2021 to 3,311 days in 3Q2022. The average day rate appreciated 49.9% to reach C$11,030, the highest level since 2018.

In the U.S., activity days increased by 840.1% to 2,839 in 3Q2022 from 302 in 3Q2021 thanks to the acquisition of Altitude, while the average day rate - converted to Canadian dollars - rose some 89% to C$25,124 in 3Q2022 from C$13,275 in 3Q2021 (Fig. 6).

{kind=link}

Fig. 6. Activity days and average day rates of Cathedral Energy Services in Canada, where there is strong seasonality, and the U.S. (Laurentian Research for The Natural Resources Hub based on Cathedral financial filings)

Financial performance

Between the sharp rise in activity days and appreciating day rates, Cathedral was able to pull in a record-high revenue of C$107.8 million in 3Q2022, posting a year-over-year growth of 435.8% (Fig. 7).

Benefitting from improved adjusted EBITDAS margin (26.0%, as in Fig. 8), Cathedral generated C$28.1 million of adjusted EBITDAS in 3Q2022, which reflects a year-over-year jump of 442.8%.

For the first time in five years, Cathedral turned profitable, earning C$8.7 million in 3Q2022 or C$8.1 million in the first nine months of the year (Fig. 7). Furthermore, the company generated some C$22.9 million of free cash flow in 3Q2022; the FCF in the first nine months of 2022 was C$25.4 million, up a spectacular 2,970% from the same period one year ago. It appears that Cathedral has just reached beyond the inflection point.

{kind=link}

Fig. 7. Revenue, EBITDAS and net income of Cathedral Energy Services, actual and projected from historical seasonality (Laurentian Research, based on data from Seeking Alpha and Cathedral)

{kind=link}

Fig. 8. Adjusted EBITDAS margin of Cathedral (Laurentian Research for The Natural Resources Hub based on Cathedral financial filings)

2023 and beyond

In 2023, Cathedral is expected to continue the impressive pace of growth; it is projected to grow revenue by 83.0%, adjusted EBITDAS by 94.2%, and FCF by 164.6%, before any potential acquisitions (Fig. 9). Since we are in the early innings of a multi-year industry up-cycle as I reasoned above, Cathedral may well keep the growth momentum well beyond 2023.

{kind=link}

Fig. 9. Projected 2023 revenue, adjusted EBITDAS and free cash flow, as compared with those in 2020 actual, 2021 actual and 2022 forecast (Cathedral Energy Services)

Valuation

Cathedral trades at 2.99X EV/EBITDA or 2.78X P/FCF on a 3Q2022 run-rate basis. It is valued at 2.49X of 2023E EV/EBITDA or 2.95X 2023E P/FCF. The stock is undervalued relative to industry peers, according to Seeking Alpha data .

Fast growing companies are common when their host industry enters a bull market. And it is not uncommon to come across stocks that feature a high FCF yield. However, it is really rare to find a company like Cathedral that grows profitably at a neck-breaking pace yet offers a FCF yield as high as 34-36%.

Risks

The oil industry is exposed to super-volatile oil and gas prices in this cycle, according to Arjun Murti . Although oilfield service firms such as Cathedral are spared of daily gyrations of commodity prices, medium-term commodity price variations still have an impact on activity days and day rates.

Cathedral seeks to consolidate the directional drilling industry. M&A activities expose it to transactional and talent retention risks. Cathedral needs to issue equity and raise debt to finance acquisitions so its balance sheet health is important. The company intends to keep the net debt/adjusted EBITDAS ratio ? 1.0x on a pro forma basis in any potential acquisitions. As of 3Q2022, its net debt to run-rate adjusted EBITDAS ratio was at 0.73X. It plans to reduce debt significantly in the next 12 months, using its strong free cash flow (Fig. 10). Reduced leverage will allow the company to consider capital return to shareholders and additional M&A transactions.

{kind=link}

Fig. 10. Net debt to adjusted EBITDAS ratio, actual and projected (Cathedral Energy Services)

The Cathedral team, led by executive chairman Rod Maxwell and CEO Tom Connors, has substantial skin in the game. The board and management own as much as 24.5% of the outstanding shares. Maxwell, for example, continued to buy the stock in the public market as recently as December 6, 2022.

Investor takeaways

Despite the recent mini-crash in oil prices that seems to have caused the weak hands to panic, the fundamentals suggest we are still in the early phase of a multi-year structural oil bull market. To long term-oriented investors, this is a great opportunity to pick the most promising oil stocks.

Cathedral Energy Services has reached the inflection point of a growth hockey stick in 3Q2022. Incredibly, the stock is still in deep value territory. Looking ahead, we most probably ain't seen nothing yet in terms of growth. Cathedral is expected to maintain its momentum of rapid and profitable growth in the next few years. I believe its shareholders will be richly rewarded as the oil bull market continues to unfold.

For further details see:

Going Into 2023: Where We Are In The Oil Cycle, What's My Best Pick - Cathedral Energy