GPRO - GoPro: A Value Trap With Turnaround Potential

Summary

- GoPro has been a poor performer since its 2014 IPO.

- The company has struggled with revenue growth and profitability.

- But over the past few years, management has started a turnaround.

- I think the core business is a value trap. But a new focus on direct sales and subscriptions may create the stability the company needs.

Investment Thesis

GoPro ( GPRO ) has been a consistent underperformer for many years. Sales have declined since the company's IPO, and profitability has been very poor.

But the company is attempting a turnaround. Management is focusing on direct-to-consumer sales and subscription offerings. This may be the boost the company needs to finally stabilize. There is a lot of risk here, but the valuation is cheap enough that I think the risk to reward is favorable.

A Broken Growth Story

GoPro has been a declining growth story for most of the past five years. The company showed promise as a "disruptive" innovator after its IPO . But it soon became clear the company could not deliver consistent growth. The company struggled with profitability and free cash flow as sales stagnated.

The prevalence of smartphone cameras limited the company's potential market. The company unsuccessfully tried out other product types, including a failed entrance into the drone market .

Shares cratered from a high of over $98 to a low of just $2. The price is still down more than 93% from its all-time highs.

Even after a decent year, the company's revenue has been flat since 2017. Sales are also down significantly from 2015 highs. The lack of revenue and profit growth makes up the primary bear case for the company. Right now, we're seeing a decrease in consumer electronics spending . On their last earnings call , management acknowledged that retailers are reducing inventory levels. It's clear to me that the company's core business is not a strong performer. But GoPro has started to reorganize its revenue streams into a more sustainable and profitable model.

Is Direct Sales The Key To A Turnaround?

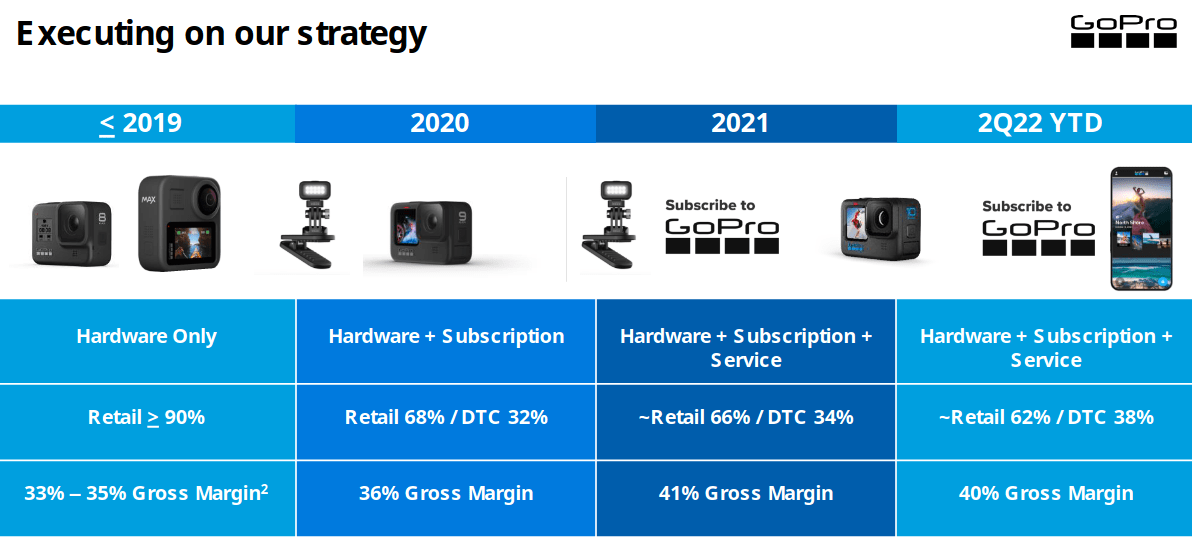

GoPro has been showing signs of a potential turnaround. The key to this renewed growth is the company's direct-to-consumer segment. Most of these sales take place through the company's website, GoPro.com. I think GoPro's clear focus on this single channel is helpful. The company's lack of direction has been a key problem for the last decade.

Sales through GoPro's website provide more control over how they sell their products. This allows the company to more efficiently upsell accessories, subscriptions, and services.

GoPro Q2 2022 Investor Presentation

{kind=link}

Sales through digital channels will increase the business's gross margins. GoPro also has more pricing flexibility through these channels. All of these tailwinds should increase both topline and bottom line performance.

The company's direct-to-consumer share of revenue has grown nicely. Direct sales increased from just 12% in 2019 to 38% in the most recent quarter. The company has a decent amount of operating leverage, so small topline upsells can have a larger impact on the company's bottom line.

Subscriptions Provide Sustainability

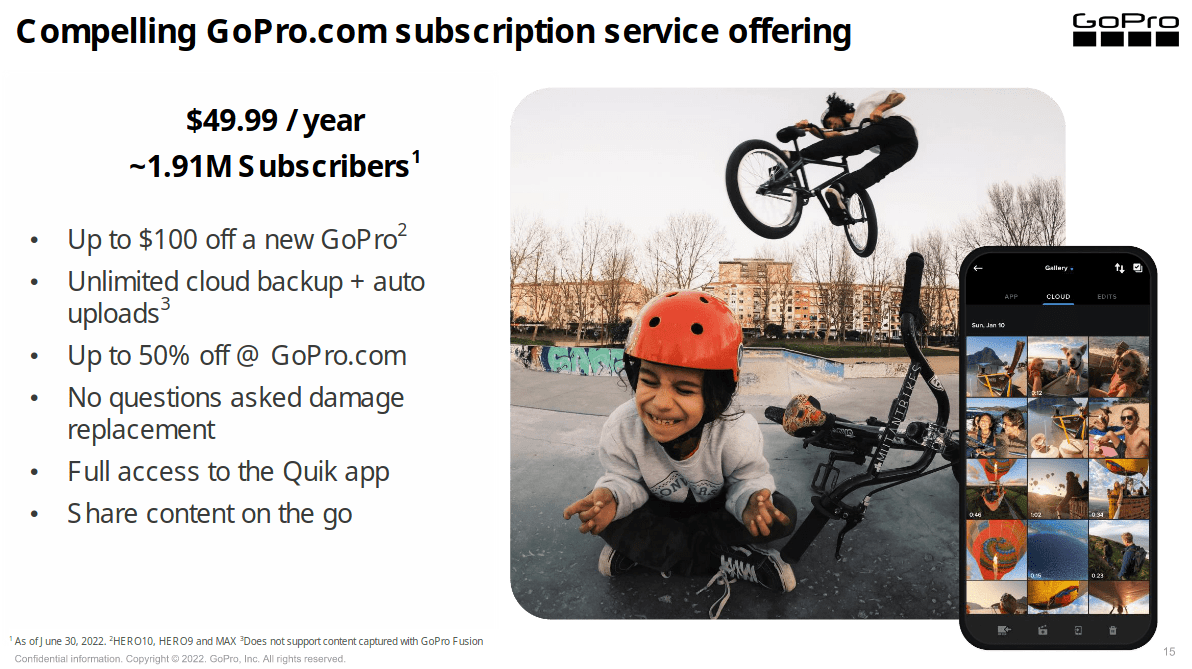

Another key turnaround driver is GoPro's subscription offering . The primary service is GoPro's cloud video subscription, which sells for $50 per year per user. Management believes this will be a key driver of future growth.

GoPro Q2 2022 Investor Presentation

{kind=link}

The service recently reached the 2 million subscriber mark . This is set to create $100 million in annual recurring revenue.

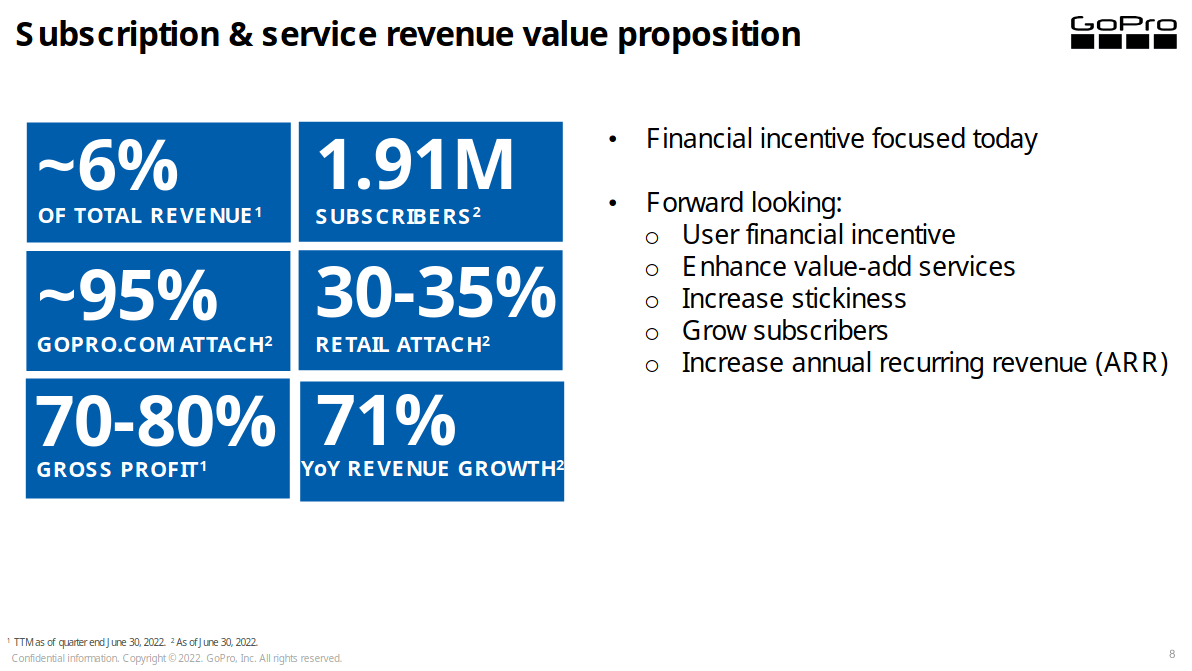

I think this segment can bring some much-needed stability to the company's finances. Management expects this offering to deliver gross margins of 70% to 80%. GoPro has struggled with profitability and cash flow generation for years. This extra profit should help boost the company's bottom line.

GoPro Q2 2022 Investor Presentation

{kind=link}

This subscription offering has clear synergies with GoPro's direct-to-consumer push. The company has seen a stellar 95% attach rate for sales from their website. This is pushing the company towards its 2022 goal of 2.2 million subscribers. As direct-to-consumer sales increase, subscriptions should move along with them.

I am cautious about the renewal rate on these services. A significant portion of subscribers hasn't had to renew yet. GoPro is offering significant discounts to new subscribers, and I want to see if its subscription service can stand alone over time. I generally believe that storage services are sticky by nature. As long as there are signs that customers are using the service, I think it should have solid retention.

A Risky Bet At A Cheap Valuation

GoPro is a risky bet, but the company is trading at a relatively cheap valuation. Shares are trading at a forward P/E of 13 and a forward EV/EBITDA of just over 5. This is what I'd be willing to pay for shares, but only if the company can retain its margins. With subscription services providing some much-needed stability to the company's finances, I think there may be some value here.

Some of my key concerns include the company's forecast for lower gross margins and declining unit volume . We're also seeing an economic pullback and a decline in electronics spending . I think GoPro may be undervalued. But a lot depends on the company's ability to offset declines in volume with higher prices and subscription revenue.

Earlier this year, GoPro authorized a share buyback of $100 million , or 10% of its market cap. I think that profitability should be the highest priority, but this should boost confidence in the share price.

This is still a turnaround play. The company's revenue is still down from pre-pandemic levels. Many of the growth headwinds haven't gone away. The broader economic environment is unfavorable. But I think the valuation is low enough that these risks may be priced into the stock.

Final Verdict

I'm bullish on the company at the current levels, but I'm still not buying the dip for the time being. The company has pushed a lot of expectations to the third and fourth quarters. I want to see if the second-half revenue and profit numbers are still solid.

I think this might be a good buy for investors with a high risk tolerance. I'm waiting for more clarity on the direction of revenue and profit growth.

For further details see:

GoPro: A Value Trap With Turnaround Potential