GPRO - GoPro: Avoid Ahead Of Earnings

2023-08-01 04:37:26 ET

Summary

- GoPro's stock price has declined 20% this year, and the company's fundamental turnaround story is at risk.

- Risks for GoPro include longer replacement cycles for its products, channel compression, and potential failure of price cuts to stimulate sales.

- Margins are already under pressure, and the company's Q1 earnings showed a decline in revenue and profitability. Price cuts in Q2 may worsen this problem.

Amid broad enthusiasm in the markets this year, the few stocks that have been holdouts in the rebound rally are unsurprisingly dealing with deep fundamental challenges. And though many of these downtrodden names represent attractive value opportunities, each has to be carefully analyzed if they are worth the risk.

GoPro ( GPRO ) sits squarely in this risky bucket. The action camera maker has seen its share price decline -20% year to date. Now, many investors had already written off GoPro a long time ago, but the company actually staged a turnaround during the pandemic amid strong demand and a focus on cost controls that allowed GoPro to generate healthy profits. Now, however, that fundamental turnaround story is at risk.

Ahead of GoPro's earnings later this week, I am cutting my recommendation on the stock to bearish . Though I admired GoPro's turnaround plan and sentiment-free downscaling over the past several years that briefly allowed the company to turn a profit, I'm more concerned now that we are seeing a demand problem for GoPro.

Here are the key risks, in my view, for this company:

- Better products means longer replacement cycles. A GoPro buyer is already a niche customer, since we already all travel with cameras in our pockets everywhere we go. Ostensibly, GoPros also get used infrequently (unless you're a daily surfer or skydiver). It's not difficult to posit, then, that as GoPro continues to upgrade its technology, replacement cycles get longer and longer as upgrades become more minimal and older products last for longer.

- Channel compression. GoPro has touted its mix shift into its direct channel as a win for margins. And while this is true, what may also be true is that GoPro resellers are pulling back on inventory amid tight macro conditions. Fewer points of sale advertising GoPro products may result in a contraction for GoPro's brand awareness.

- Price cuts may not pan out. Amid revenue contraction in the start of 2023, GoPro's principal strategy is to reduce prices in order to stimulate unit sales and hopefully encourage more people to sign up for a GoPro subscription. Given GoPros are infrequent and specialty purchases, however, it may be possible that buyers aren't really elastic about this product at all, and GoPro may not see the lifts it's hoping for.

- Subscription attach rates may decline. And because subscription prices aren't changing, the fact that subscription spend as a percentage of hardware spend will increase once GoPro cuts hardware prices may cause a dip in overall subscription attach rates.

In my view, it's better to stay on the sidelines here: especially after GoPro releases its Q2 earnings print that shows the first quarter of results after its broad price drop, I think the stock has further downside to go.

Margins are already under pressure; the brief pandemic limelight is fading

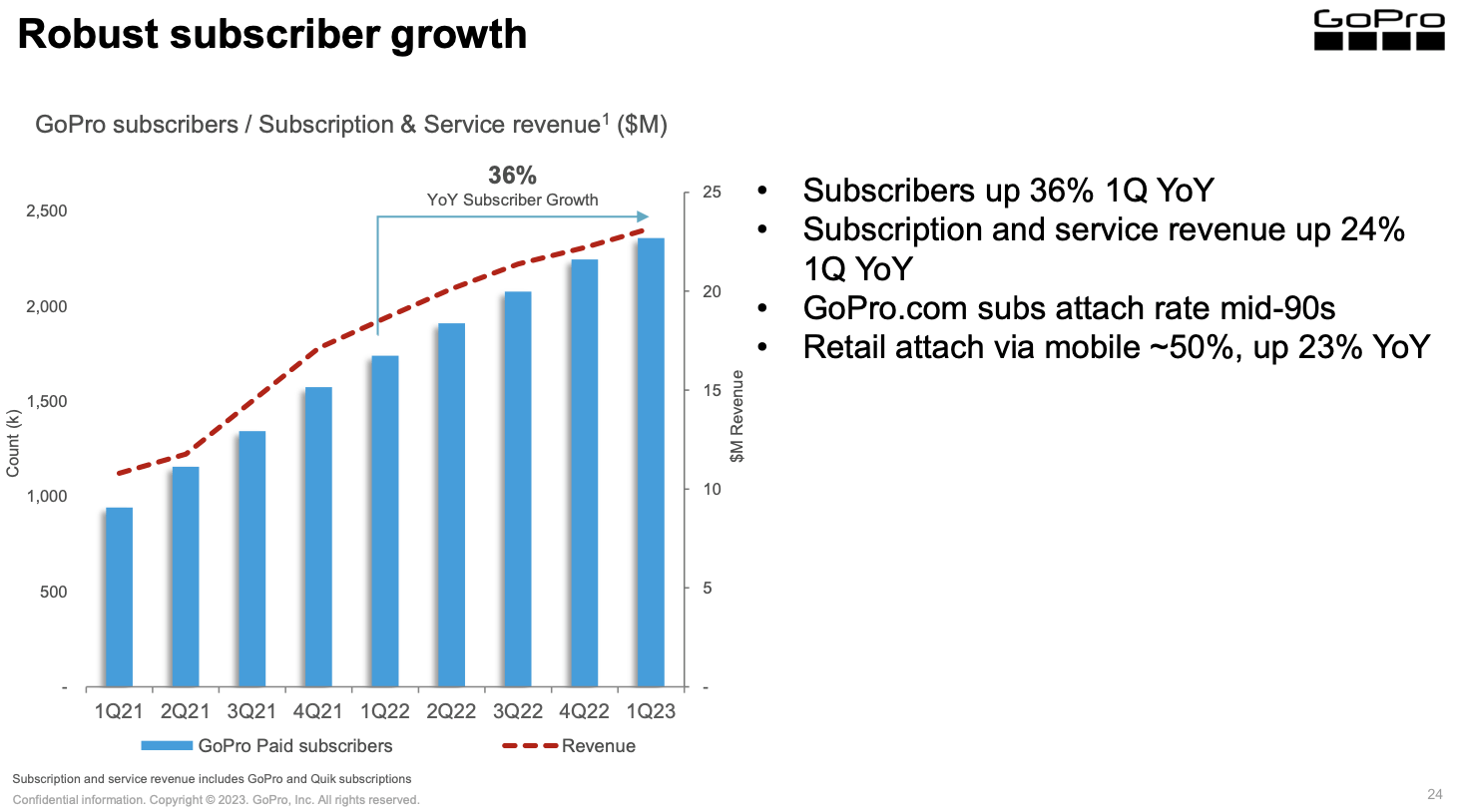

In GoPro's most recent quarter, overall revenue of $175 million declined -19% y/y. Hardware revenue was the main drag here, while subscription revenue continued to grow at a 24% y/y pace to $23 million, or 13% of the company's total.

GoPro continues to tout its subscription story, which to its credit is quite impressive. Subscribers in Q1 grew 36% y/y, with attach rates for customers buying on the GoPro.com site at a sky-high "mid 90s" percentage.

{kind=link}

The company has two subscription offerings. Its core subscription is a $50/year offering that offers $100 off new cameras and has a damage warranty plus unlimited cloud and video storage (one could argue this "subscription" is actually a huge price subsidy on its own, given the upfront camera discount and the fact that it comes at a discounted $25/year for the first year with a new camera purchase). It also offers a $10/year "Quik" subscription that offers cloud storage without hardware incentives or warranties. The company is planning on unveiling a third "premium" subscription tier later this year.

To spur hardware sales and improve subscription attach, however, the company has decided to slash prices - which will take impact in the Q2 earnings print. Per Founder/CEO Nick Woodman's remarks on the Q1 earnings call:

The key points of our updated go-to-market strategy, which we kicked off this week, include restoring pricing of our products to 2019 levels with an MSRP reduction of $100 for our flagship HERO11 Black, HERO11 Mini, HERO10 Black and HERO9 Black cameras. Reductions in inbound freight and product costs along with an improved supply chain are helping to enable this price adjustment from a margin perspective, as will the introduction of new, higher-priced, higher-margin SKUs in the future.

Re-introducing an entry-level price point SKU with HERO9 Black to drive meaningful volume and subscriber growth.

Restoring our world-class presence at retail by increasing global distribution to best-in-class retailers.

And eliminating camera discounts at the time of purchase at GoPro.com. Thanks to the strength of in-app subscriber conversion of retail consumers as well as improvements in subscriber retention, we believe we can generate more subscribers with growth in retail sales than if we continue our pandemic-driven strategy of focusing primarily on GoPro.com sales for subscriber growth.

As I mentioned, we believe this improved strategy will drive unit sell-in and sell-through to an improved 3.2 million units in 2023, 3.5 million to 4 million units in '24, and above 4 million units in 2025.

We believe GoPro subscribers will grow to 2.45 million to 2.6 million in 2023, 2.7 million to 2.8 million subscribers in 2024, and 2.9 million to 3.1 million subscribers by the end of 2025."

Again, the impacts of these price moves are relatively unknown - but I'd argue that demand for GoPro is likely to be quite inelastic (unresponsive to price changes), since these are infrequent purchasers who aren't likely price-comparing different options (GoPro has few competitors in the specialty action-camera market).

And unless GoPro gets the sharp spike in high-margin subscription fees that it's banking on, these price cuts may exacerbate the company's margin problems. Q1 pro forma gross margins fell to a multi-year low of 30.3%, down 480bps sequentially and down nearly 12 points year-over-year, as shown in the chart below:

{kind=link}

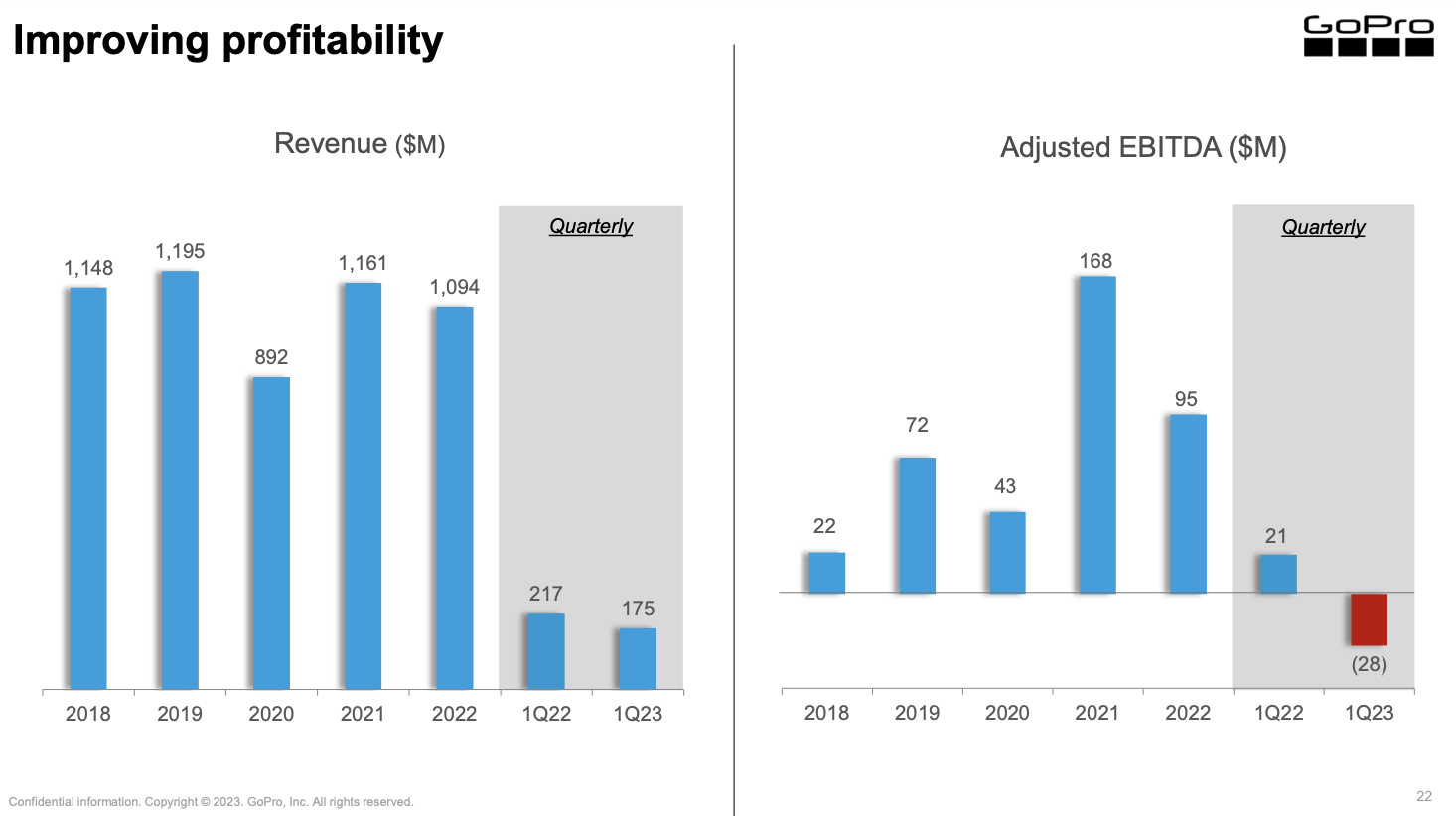

This gross margin slice, in turn, dropped GoPro's adjusted EBITDA down to -$28 million, despite a profit of nearly the same magnitude in the year-ago Q1:

{kind=link}

Key takeaways

With so many risks sitting on the horizon for GoPro, I think it's better to take our chips off the table and invest elsewhere. In my view, price cuts won't produce meaningful revenue or subscription growth for GoPro, and margins and profitability will continue their recent downward trend.

For further details see:

GoPro: Avoid Ahead Of Earnings