GPRO - GoPro: Fundamentally Flawed But Close To Value

2023-03-24 12:08:43 ET

Summary

- Revenue has stagnated, with the company struggling to break out of its niche.

- Services revenue is improving but is only a small portion of sales, lacking the scope for significant improvement.

- Margins can be attractive but are highly sensitive to cyclical swings, which are currently also depressing demand.

- GPRO's valuation does not allow for any upside, given the short-term headwinds ahead.

- As its market cap approaches book value, we could see value.

Investment thesis

Following an almost 95% decline in share price since its ATH, GPRO has many suggesting it could represent value. Our objective is to do a deep dive into the business from a financial perspective, assessing the fundamental quality of GPRO.

Company description

GoPro, Inc. (GPRO) develops and sells cameras, mountable and wearable accessories, and subscription services and software internationally.

The subscription service includes the Quik app, cloud storage, camera replacement, and damage protection; the Quik subscription offers access to editing tools for both pictures and videos.

Share price

GPRO's share price has experienced a monumental decline since it first joined the stock market, as the company has failed to develop and consistently grow its revenue, arguably further behind than it was a decade ago.

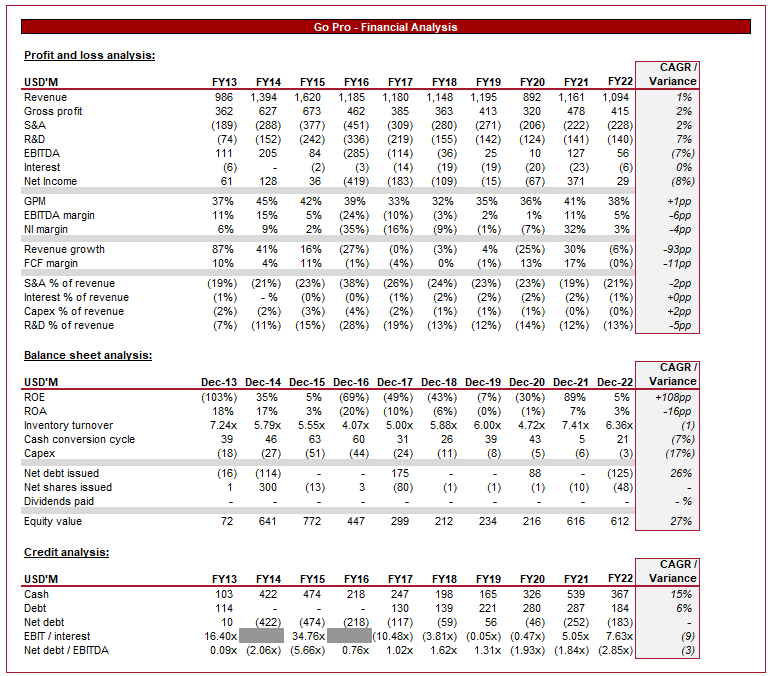

Financial analysis

Go Pro Financials (Tikr Terminal)

{kind=link}

Presented above is GoPro's performance for the last decade, which can be best summarized by the word stagnation.

Revenue has grown at a CAGR of 1%, with GPRO significantly below its peak levels in FY14/15. There are numerous reasons for this in our view. Firstly, the initial rise of popularity was driven by hype, as GPRO offered a high-quality product that was historically reserved for professionals or was in a price bracket consumers could not afford. For those looking to capture activities, the cameras are perfect due to their durability, quality, and versatility. The problem with this, however, is that GPRO failed to capitalize on this hype. The brand became synonymous with activities, rather than selling the quality of the product.

Furthermore, expanding on the target audience piece, our view is that GPRO has done a poor job of transitioning to the mass market. Most companies come to a market with a specific USP/niche, before transitioning toward catering to the most people possible, as a means of increasing their potential customers. GRPO has attempted this, as the following screenshots suggest.

GPRO Google Searches (Google) GoPro website (GoPro) GoPro GoPro

{kind=link}

{kind=link}

{kind=link}

The reason we think the company has failed in this effort is due to the current market dynamics. Mobile cameras are becoming extremely good and in many cases comparable to professional cameras, while now incorporating action technology such as Stabilization. Why would a consumer pay several hundred dollars for a product which does not materially improve upon their mobile phone? For this reason, GPRO is arguably further away from the mass market than it was several years ago.

Further, the company is a victim of its R&D success. Its products are very good and have a long replacement cycle, which means consumers have little need to upgrade for an extended period. This is fine for a company like Apple ( AAPL ), as they will sell a consumer multiple other products in the years between every MacBook. GRO on the other hand has little more to sell, so relies on new customer generation.

A final factor we attribute to the stagnation of revenue is the lack of product transitioning. GPRO has focused on launching new and better cameras (rightly so), however, has not launched any accompanying products beyond accessories. The problem with this is that the company is essentially a niche player in a market that is far less "required" for consumers due to cameras in phones. GPRO did attempt to expand into the Drone market, a great strategy in our view, but completely failed with execution. The product had a "terrible launch" ( Quote from GPRO's founder) and the sales reacted accordingly. With the company substantially smaller, the ability to innovate from here is likely limited.

{kind=link}

In the most recent quarters, adjusted for seasonability, revenue has been declining. This is likely driven by worsening economic conditions. With the inflationary pressures faced in the West, consumers are experiencing a decline in discretionary income, leading to reduced non-core spending. GPRO is arguably a premium product that most can go without. GPRO is overly exposed to this as weakening conditions could lead to reduced travel, which will also mean lower demand for its products. It would not be surprising to see the company see further declines in FY23.

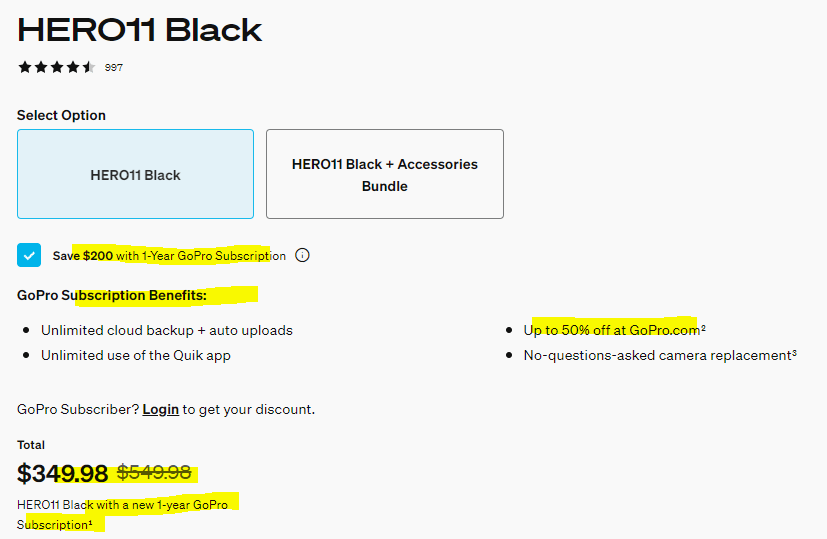

Not only are sales declining but margins too. GPRO has engaged in greater discounting, likely to support sales numbers as demand falls. This has contributed to a 3 ppts. fall in GPM between FY21 and FY22. The following is a screenshot of the current sale offered on the Hero11, with a similar level across GPRO's other products.

Hero11 discount (GPRO)

{kind=link}

One area of improvement is GPRO's expansion into services. Several years ago, GPRO launched a services offering, which currently provides consumers the following.

GoPro subscriptions (GoPro)

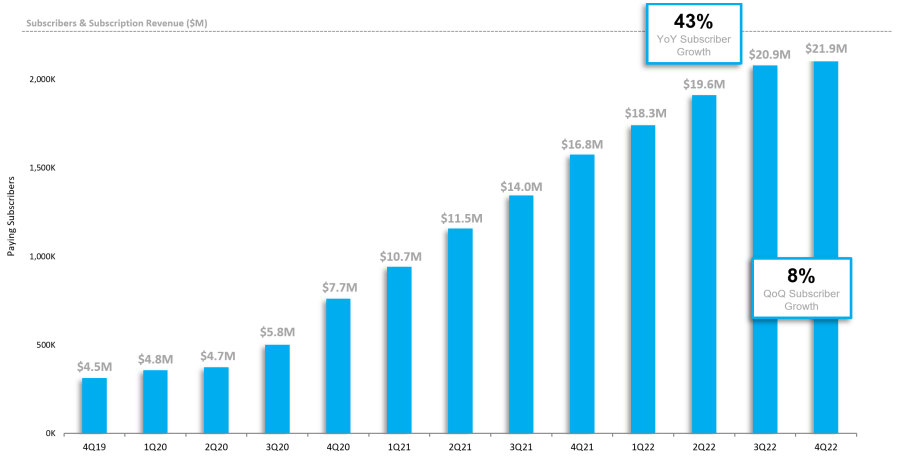

Although this is not a whole new product launch, this is a fantastic move by Management to create some level of recurring revenue. The marginal cost to provide this service is minimal, while the development of value for consumers has also come at an acceptable cost in our view. Cloud storage is a simple offering while discounts encourage recurring purchases, with the subscription income offsetting the discount. Many have heralded this as the driving force behind the resurgence of GPRO but we do not see it. The following graph illustrates the growth in revenue since Q4-19. From a glance, it looks great but if you look at the numbers, the issues emerge. Based on this, the company generates 7.4% of revenue from this segment, with growth slowing.

GPRO subs revenue growth (GoPro)

{kind=link}

The reality is, this segment is just not moving the needle. Further, the subscription model is directly tied to the success of the hardware, it is not an independent offering. Yes, a consumer in theory may want GPRO's editing software but in 2023, when editing software and Adobe exist, this is highly unlikely. As a result of this, subscriptions will only grow if hardware sales do. This is why we like this expansion but do not see it as a game-changer.

GPRO's operational investment is also an area of underperformance, with S&A and R&D growth exceeding revenue. R&D is understandable if the products developed were driving greater revenue but this is not the case. The company has faced some inflationary pressures from a cost perspective but nevertheless, this is an underperformance in our view.

The net impact of these factors is a decline in bottom-line margins. Current GPRO has an EBITDA margin of 5% and FCF margin of nil. In our view, this is quite unattractive. On a normalized basis, the company can achieve slightly higher levels but the volatility in itself is unattractive.

Moving onto the balance sheet, the slowing demand is reflected in a decline in inventory turnover, which has fallen 14%. This is one of the contributing factors to the decline in FCF. This could result in further discounting activities, although the current levels remain above the historical average.

Management has made a shrewd decision by limiting its use of debt, with the company having a negative net debt balance. For this reason, we do not consider there to be any liquidity or solvency risk currently.

GPRO's current equity position is $611M, including $146M in goodwill. With a market cap of c.$760M, the company is almost trading at its asset value. This could make the company an attractive takeover target and in our view, represents a "bottom" for the business. Even if it stops growing, the company was still profitable over a whole economic cycle.

Outlook

GPRO outlook (Tikr Terminal)

Presented above is Wall Street's consensus view on the business.

Analysts hold a similar commercial view of the business we do, expecting continued growth stagnation. Interestingly, margins are expected to improve rapidly, primarily driven by improvements in GPM. Our view is that this would be driven by improving economic conditions, resulting in fewer discounts required. As GPRO has reached these levels prior, we consider this reasonable.

Market comparison

When assessing financial performance, it is useful to compare companies to peers, as it allows for a relative view. Many in the consumer electronics space are struggling with demand currently and so we can compare the relative delta.

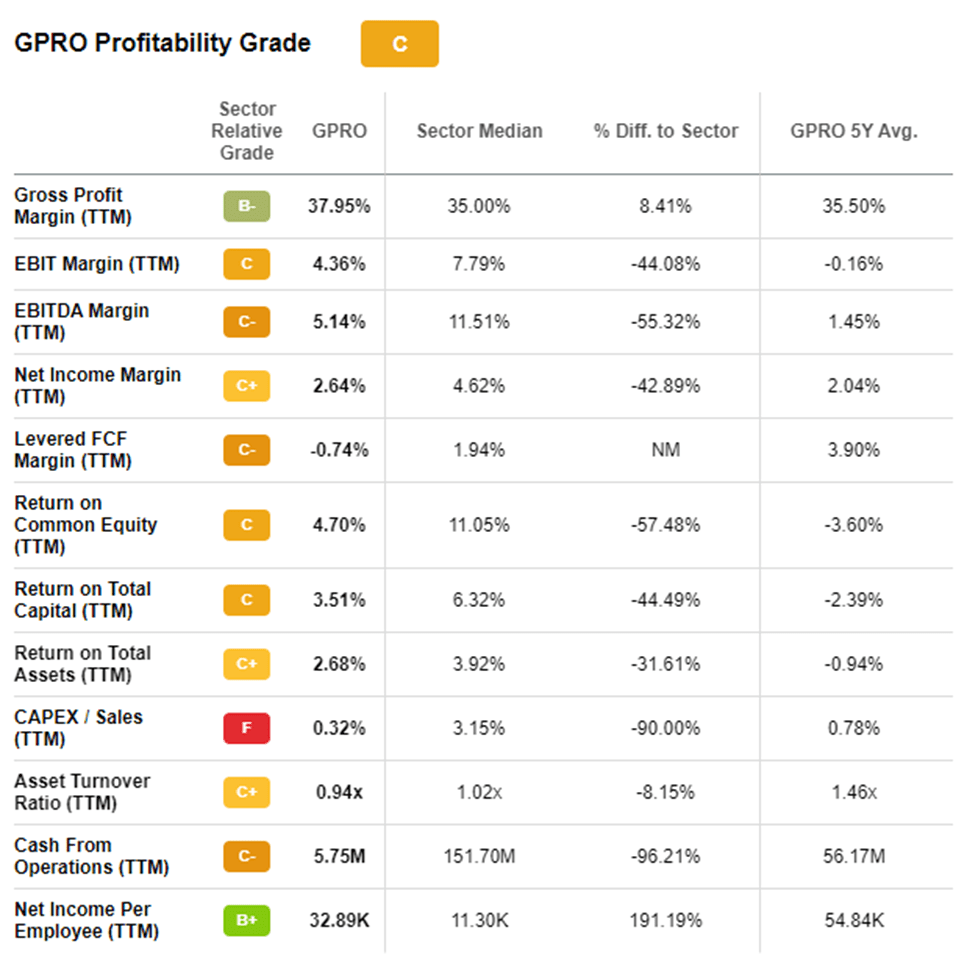

GPRO profitability (Seeking Alpha)

{kind=link}

From a profitability perspective, GPRO does quite well. The company is slightly more profitable from a GPM perspective but loses these gains on the bottom line. The driving force behind this is GPRO's large investment in R&D, which is 13% of Revenue. If this was to fall to 8% for example, GPRO's EBITDA would jump to 10%. With S&A at 21% of revenue, we see little room for it to decline, so the question is whether there is scope for a reduction in R&D. Regardless, this does suggest some value with the business and importantly, that it is arguably not worth its current equity value.

{kind=link}

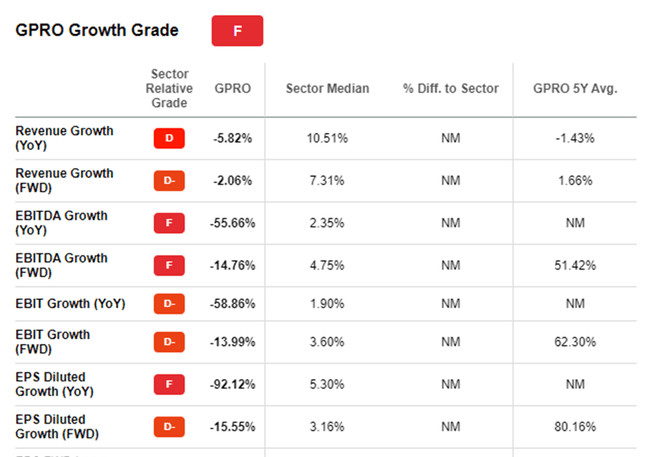

We will not repeat what we have already stated but growth is clearly the biggest issue. The company is overly sensitive to market conditions, declining when many are still growing.

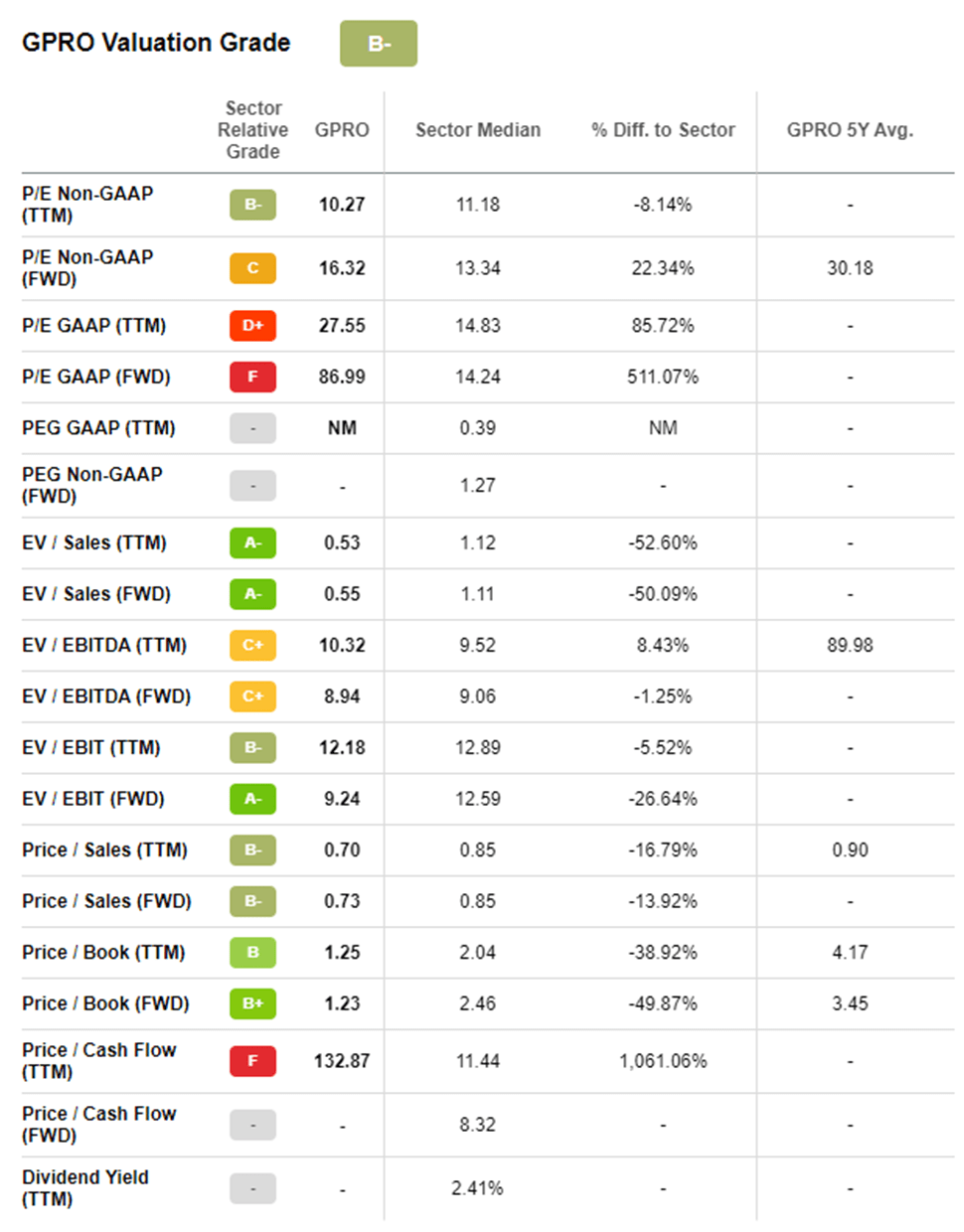

Valuation

GPRO Valuation (Seeking Alpha)

{kind=link}

With the capitulation in share price and continued profitability, GPRO is approaching the realms of being attractive, despite the poor performance. The company is slightly cheaper than its peers on an earnings and Sales ratio basis, while being slightly more expensive on an EBITDA level. Our view would be that this does not wholly reward investors for the risk they face, especially in the short term as weak conditions persist. Nevertheless, with the company hovering around its equity value, a further decline could quickly make the company quite attractive.

Final thoughts

GPRO makes a genuinely great product but this does not make it a good business. Our commercial view on the business is that revenue stagnation will continue, with the company remaining a niche player. Profitability is moderate but will fluctuate wildly based on cyclical changes.

With GRPO approaching its equity value, it could soon represent an attractive opportunity. However, currently, the company is facing economic headwinds and has no scope for upside in our view.

For further details see:

GoPro: Fundamentally Flawed But Close To Value