GPRO - GoPro Hold Rating: A Pragmatic Stance Amid Pricing Pressures

2023-10-19 06:05:48 ET

Summary

- GoPro's pricing strategies are crucial for maintaining unit sales and generating revenue amidst market competition.

- Despite a notable market share of 37.1%, GPRO faces significant competitive pressures, impacting its profitability.

- A simple multiples-based valuation analysis suggests a theoretical share price of up to $6.14 per share, assuming GPRO attains profitability.

- However, my "hold" rating reflects a blend of cautious optimism grounded in past revenue trends from 2021 and 2022 while still recognizing GPRO's prevailing market challenges and unprofitability.

GoPro ( GPRO ) fundamentally hinges on its pricing strategies, which are crucial for maintaining its unit sales while generating revenue amidst market competition. The valuation analysis suggests a theoretical value of $6.14 per share should GPRO's revenues turn profitable. However, I believe adopting a 'hold' rating with measured optimism is more pragmatic at this juncture. This stance acknowledges the potential upside GPRO holds while also considering the competitive challenges and pricing pressures it faces. This balanced outlook is drawn from GPRO's demonstrated potential as a viable investment in 2021 and 2022, although, at present, the bullish scenario largely remains speculative. A "hold" rating, I believe, offers a more grounded assessment while leaving room for potential pricing improvements.

Business Overview

GoPro is a well-established player in the action camera industry, chiefly known for its mountable and wearable action cameras and its proprietary video-editing software. The company has made a name for itself in extreme action video photography. Its robust product line includes the HD HERO range, enabling users to document high-definition footage of life’s exhilarating moments. The product suite extends to mounts, accessories, and digital solutions like desktop applications and mobile apps, facilitating a seamless process to capture, manage, and share content. GPRO’s revenue model is two-pronged: the sale of physical hardware like cameras and accessories and a subscription service offering cloud storage and enhanced access to editing software.

I believe GPRO’s main strategy has been through effective marketing that resonates well with outdoor enthusiasts and adventure seekers, leveraging its strong brand recognition to maintain a competitive edge. However, the recent relatively high pricing of GPRO products compared to competitors like DJI and Sony hinders GRPO’s allure for budget-conscious consumers, which somewhat limits its customer base and hurts overall revenues. Thus, GPRO's narrow product range has primarily focused on action cameras , which could be a vulnerability given the changing consumer preferences and the highly competitive nature of the action camera market. Thus, GPRO’s market pricing pressure essentially dictates the company’s results, which shows that so far, GPRO hasn’t truly developed a differentiated product to build a lasting business moat.

Source: Precedence Research.

On a positive note, the growing global affinity towards outdoor activities and adventure sports provides GPRO with a lucrative opportunity to extend its market reach and product offerings. In particular, the action camera market is expected to grow at a CAGR of 9.1% to 16.7% , so it’s undeniable that GPRO should benefit from ongoing secular tailwinds. Moreover, exploring collaborations, especially with drone manufacturers, has further diversified GPRO's product offerings, integrating its high-quality cameras for aerial photography and videography, which is also an area growing in popularity.

GPRO's Strategic Challenges and Pricing Maneuvers

GPRO has multiple challenges that significantly shape its business outlook. A primary concern is the inadequate competitive barriers within the action camera sector. However, since the action camera market is about $2.8 billion (see image above), GPRO's 2023 revenue estimates of $1.04 billion imply a notable market share of roughly 37.1%. So evidently, the entry of cost-effective alternatives from rivals presents a serious threat. Also, GPRO's strategy towards cost management is another area of concern. Initially, a partnership with the Taiwanese Foxconn was perceived as a pathway toward more cost-efficient manufacturing. However, the need for a formalized agreement has directed GPRO towards smaller contract manufacturers like Chicony Electronics. I believe this tactic hasn’t effectively improved GPRO’s costs because it might not have provided the economies of scale that Foxconn could offer. This shift seems to have led to higher per-unit production costs, only further exacerbating the declining gross margins of 2023.

Additionally, GPRO's venture into the media domain via the GPRO Network hasn’t reaped the anticipated financial benefits, notwithstanding the uptick in viewership. Utilizing external platforms like YouTube for content hosting has negatively impacted revenue generation as YouTube's revenue-sharing model takes a significant cut. In my assessment, the GPRO Network has contributed to enhancing brand visibility, garnering over 11 million subscribers on its YouTube channel, which could potentially drive sales growth. But this hasn't alleviated GPRO's pricing pressures.

Overall, GPRO's total revenue for the quarter ending August 2023 amounted to $241 million , compared to $251 million during the corresponding period last year. GPRO reduced the prices of its products because the company initiated a strategy in the second quarter of 2023 that included restoring the pricing of GPRO cameras to lower pre-pandemic levels?. This price reduction was reflected in the pricing of their flagship HERO11 Black, which was priced at $399.99, along with other models like the HERO11 Black Mini at $299.99, HERO10 Black at $349.99, and HERO9 Black at $249.99?.

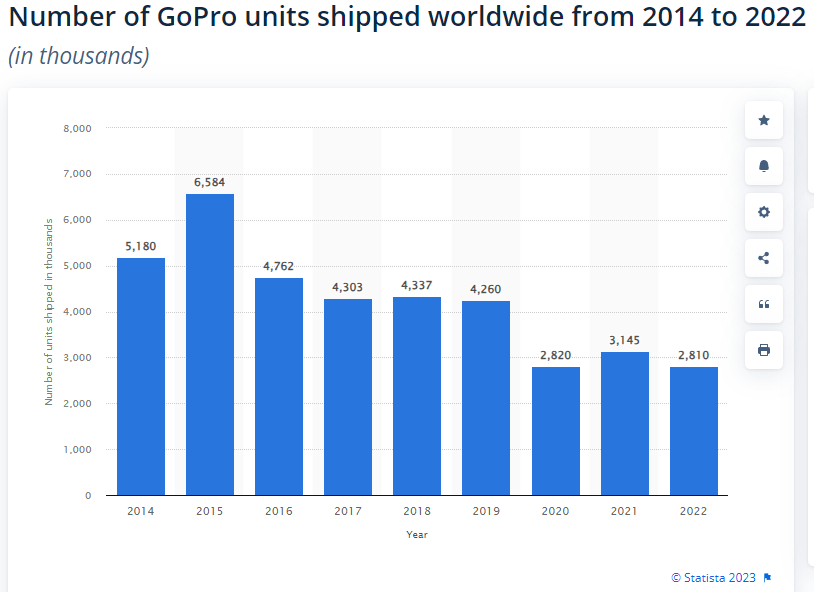

Declining unit sales reveal pricing pressures and high price elasticity. (Source: Statista.)

{kind=link}

The price reduction came after an earnings miss and a revenue decline, which led to the decision to drop prices on their cameras. The CEO conveyed enthusiasm about returning to these price points, suggesting optimism towards this pricing strategy. However, despite lower prices, the increase in retail sales did not compensate for the decline in GoPro.com sales, leading to a revenue drop. Various factors , including product mix and the effects of price protection, influenced this situation. Furthermore, significant price changes were announced in their lineup, including for the GoPro Max, in response to missing revenue estimates??. The pricing strategy aimed at possibly increasing sales volumes by making the products more affordable, but it appears that the lower pricing led to lower revenue, even if sales volumes remained steady or increased.

However, that pricing strategy, while potentially driving sales, didn’t translate to increased revenue, possibly due to the lower price points not compensating for the cost of production and other operating expenses. To correct this situation, GPRO increased the price of its GPRO Max camera to $499. This move came after GPRO initially lowered the price to $399 to stimulate demand. However, as the demand surged significantly, GPRO reverted to its pre-pandemic pricing strategy, elevating the GPRO Max's price back to $499. But overall, GPRO’s main issue remains how many units it sells and at what price rather than its cost structure.

Future Prospects

GPRO is expected to report a modest uptick in unit sales, with an estimated 2.9 million cameras to be sold in 2023, slightly outpacing the sales figures of 2022. However, a recent adjustment in pricing strategy is projected to pull overall revenue beneath the previous year’s mark, approximating a 5.3% year-over-year revenue downturn. This scenario underscores the dichotomy in GPRO's market dynamics, where the financial repercussions of pricing concessions overshadow an increase in units sold.

Seeking Alpha.

In my view, this recurrent narrative accentuates a fundamental market positioning issue. The theoretical premise that an elevation in price points could significantly bolster GPRO’s financial performance holds merit, given that a higher price, coupled with substantial unit sales, can potentially escalate revenue. Yet, this proposition seems to border on the elusive, as the current market conditions and GPRO’s historical performance narrate a different tale. A crucial element that appears to be missing is the actualization of economies of scale, which remains unattained despite the passage of considerable time. This, coupled with the evident pricing pressures, signals a lack of meaningful product differentiation, which casts a shadow on GPRO's ability to either escalate its prices or markedly broaden its market share.

Valuation Perspective

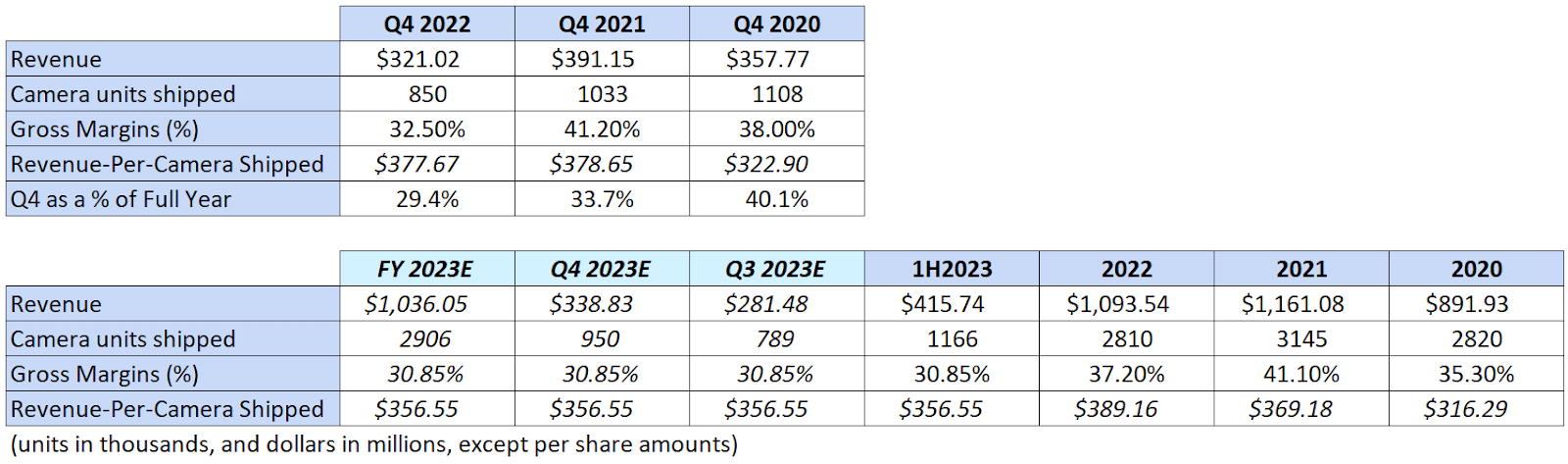

Therefore, from a valuation perspective, realizing that GPRO is usually unprofitable is vital. So, a typical DCF analysis is probably not the best approach here. Instead, a multiples-based valuation approach is likely better. For this, analysts expect GPRO to report revenues of $281.48 million and $338.83 million in Q4, respectively. Also, based on GPRO’s revenues and units sold in 1H2023 so far, I’ve derived a revenue-per-unit sold metric that I’ve used to estimate GPRO’s full-year units sold. So far in 1H2023, GPRO has $356.55 in revenue per camera sold.

{kind=link}

So, the portrayal of GPRO as a purveyor of niche products to a specialized user base rings true. However, its revenues are seemingly tethered to cyclical costs and demand fluctuations, portraying a business model with limited elasticity to transfer cost increments to its consumer base without triggering a significant sales downturn. This scenario, in my opinion, denotes a relatively less appealing business venture with a marked vulnerability to pricing pressures. Consequently, I believe such revenues should be priced, at best, in line with the sector’s multiples.

Author's elaboration.

Accordingly, GPRO's intrinsic value per share should be at most $6.14 if its sales metrics align with sector multiples, suggesting a notable 120% upside potential from the current PPS. However, it's crucial to note the market's realistic assessment of GPRO's ongoing unprofitability. Particularly, its gross margins, which underscores the notion that the $6.14 valuation serves more as a cap rather than a price target. Furthermore 2024, analysts anticipate about $1.15 billion in revenues. And using 2023's revenue-per-unit figures, it'd imply shipping 3.23 million cameras. This projection translates to an 11.1% YoY increase in camera sales. However, considering the low revenue-per-camera, I infer that this growth would only marginally offset the cash burn.

The Bullish Scenario

Nevertheless, the bull case lies in a higher revenue-per-camera figure of at least $370.00, a slight 3.77% increase from the present $356.55. Yet, such price hikes could feasibly propel GPRO's revenues beyond the breakeven point, thereby justifying higher valuation multiples and potentially unlocking shareholder value up to $6.14 per share. This projection, albeit speculative, is not without precedent. For context, GPRO's revenue-per-camera in 2022 and 2021 stood at $389.16 and $369.18, respectively, which were conducive to profitability.

Author's elaboration.

In my view, the profitability exhibited in these past instances should, at a minimum, set the stage for valuation multiples in line with sector averages, provided that GPRO maintains or improves upon past revenue-per-camera figures. This perspective is anchored in the historical data , which underscores a correlation between revenue-per-camera metrics and profitability. The rationale behind higher valuation multiples lies in the demonstrated capacity of GPRO to generate profits at specified revenue-per-camera levels. Hence, a repeat or betterment of such financial performance could reasonably warrant valuation multiples that mirror or surpass those of sector contemporaries.

Consequently, if GPRO were to achieve profitability, its current valuation could be perceived as markedly undervalued. However, this optimistic scenario is not the present reality, leading me to categorize GPRO as a "hold" for now. I believe this rating aptly mediates the present notable discount in shares with the potential upside if GPRO reaches profitability in the near term. This stance also considers the competitive hurdles and pricing pressures that GPRO continually faces, without becoming unnecessarily bearish.

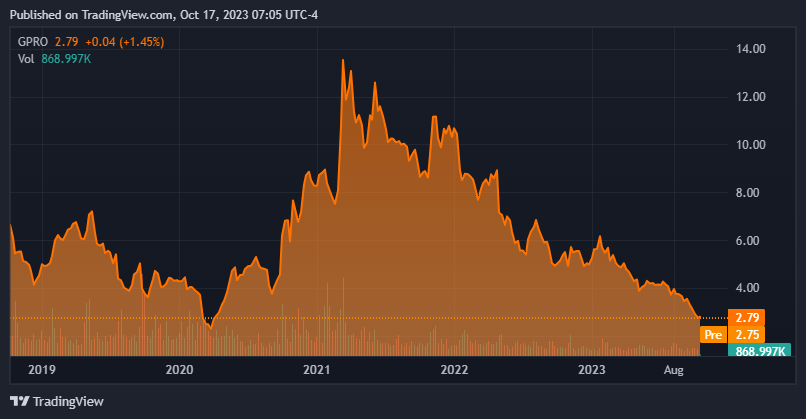

GPRO's stock price plunge reflects an overall bearish consensus. (TradingView.)

{kind=link}

Conclusion

GPRO’s pricing strategies in balancing unit sales and revenue amid market competition remain the core issue. Valuation multiples posit a theoretical $6.14 per share price, contingent on profitability, which currently eludes GPRO. Hence, my “hold” rating represents a blend of cautious optimism and pragmatic assessment, acknowledging GPRO's potential upside while considering prevailing challenges. This stance is grounded in past revenue trends from 2021 and 2022, indicating GPRO's potential viability as an investment. However, the bullish scenario leans towards speculation, necessitating a tempered outlook. The “hold” rating offers a pragmatic yet hopeful perspective on GPRO stock, especially considering that the current consensus seems overly bearish.

For further details see:

GoPro Hold Rating: A Pragmatic Stance Amid Pricing Pressures