GPRO - GoPro Needs A Growth Catalyst

2023-05-25 08:33:39 ET

Summary

- GoPro has a strong product and a loyal user base. Competition has not been able to encroach on its position.

- GPRO has become much more efficient in its operations. It has become profitable and able to provide value to shareholders.

- The company is seeing itself stagnate. The biggest question is, what will drive growth going forward?

I have watched GoPro ( GPRO ) for some time as I am a personal user of their products and have always been a satisfied customer. The company has had some good times and also bad times. The company seemed to falter around for a while as it tried to find a direction as a company. It had some failed products and was not operating at a profitable level. It was not being managed efficiently either. I think it found its place as a company. It is operating at a good size and has become much more efficient as a whole. The company has a strong product with a strong user base that despite competition is not threatened. The launch of its subscription was a game changer for the business as well. It has become a consistently profitable company.

It seems to be a common theme but most companies seem to be adjusting to the changes that have come along since the pandemic. All businesses were affected during COVID. Some in different ways and more than others, but it had an effect on everyone. GoPro is no different. It grew in certain ways during COVID and now is going through an adjustment to get its business to a post pandemic position. I think the company will continue to be profitable. While it is great to be profitable I wonder where the growth will come from for the company? The company has stalled and is now just treading water.

GoPro Product Strength

One of the biggest benefits that GoPro has is its brand name and its strong user base. GoPro really built the market for action cameras and has been able to hold the market. Electronic hardware always has stiff competition in the market. It is easy for other hardware companies to rip your product off. Despite that fact it seems that GoPro has built itself a moat between itself and the competition. Not to say that there are no other makers of action cameras, but they are little known in comparison. DJI is the biggest competitor. Garmin ( GRMN ) had a line of action cameras and seemed to be the most potent competitor for GoPro, but it seems to have discontinued that line of products, really letting you know the lack of success the product had. I know for myself I recently purchased a new GoPro and I never even bothered to look at competitor products. I just looked at which version of the GoPro I wanted.

The company has helped to establish this moat with its subscription and software. The company's subscription service includes full access to the Quik app, unlimited cloud storage supporting source video and photo quality, camera replacement and damage protection, access to a high-quality live streaming service on GoPro.com as well as discounts on GoPro cameras, gear, mounts and accessories. The HERO5 Black and newer cameras automatically upload photos and videos to a subscriber's GoPro account at the highest possible quality, while HERO7 Black and newer cameras can access the live streaming service. Their subscriptions have seen strong growth. It is not only providing a good revenue driver but it helps to build customer loyalty. A user of the company's apps and software does not want to learn new software or get a new account with another company. They are much more likely to continue using GoPro products. It helps retain that user on a go forward basis.

The company has worked on building an ecosystem of products that keeps users around. This is very similar to what Apple has done with its products. It sells a great phone but there are other great phones in terms of specs out there. They have built out their own ecosystem that makes changing to a competitor much more work. I am not saying that GoPro is comparable to Apple or trying to make a massive stretch between those two. I don't want that to be misunderstood. I am only referring to the ability to provide the hardware and companion products or software to keep you coming back to them each time you want an upgrade. Now users can always use the video editing software regardless of having a GoPro but it is much more seamless for the company's hardware. I think this building of an ecosystem of products has been the best move for the company. It has allowed it to produce much more consistent results and retain its customers.

Financials

The company has found itself on some solid footing the last few years. It has become a consistently profitable company. It generates solid cash flow and has used that to repurchase shares. The company also has a strong cash position with $370 million at the end of 2022. The latest quarterly report was an exception to this. The company provided fairly detailed information on why the drop occurred and the estimates for the rest of the year. In short there is a transition going back to retailers after moving mostly online during COVID. I think the company provided good color around this situation and clarity on expectations for the rest of the year and go forward years. I will give the company the benefit of the doubt on their financial estimates for the rest of the year, which show a return to profitability for the year. You can read the prepared remarks here .

Gross margins were a big part of the negative on the quarter. Gross margin was only 30% during the quarter. This is down significantly from 41% during 2021 and 37% for 2022. This is expected to rebound more towards the second half of the year. Part of this is due to input costs decreasing. Overall expectations are for a 33% GM for 2023. This will have a drag on the company for most of the year. It does estimate that GM will increase to 36% to 40% in 2024 and 2025. Which is really back to where it was during 2021. I think some of this increase in GM will be due to the increase in subscription and services revenue. The company does not break out the margins for this business line but does note that it is "high-margin".

The company expects to increase sales in cameras with its adjustment back to retailers. It expects to sell 3.2 million in 2023, 3.5 million in 2024, and 4 million in 2025. This is growth in the number of cameras of 10-14% each year. This growth will be partly offset by a lower margin on the products.

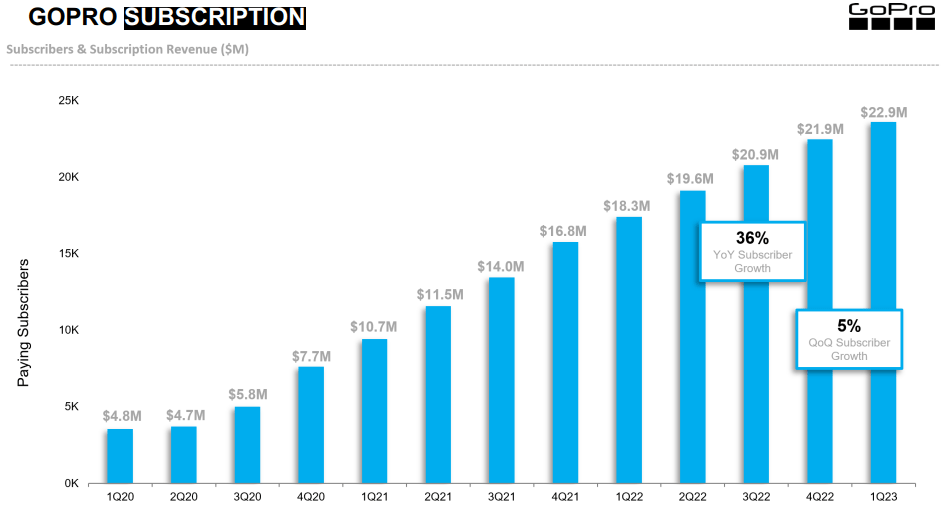

The company continues to see its subscription business grow as well. The number of subscribers grew by 36% year over year, coming to a total of 2.36 million during Q1. The revenue continued a similar growth seeing a jump of 24% year over year. It also expects to continue to see growth with subscribers coming in at 2.45 to 2.6 million by the end of the year along with $100 million in revenue from subscription and services revenue. The chart below outlines the growth that the subscription business has seen over the past three years.

{kind=link}

While this has been a bright spot, the growth is slowing. Based upon the company estimates on subscriber growth they expect to see growth of 9-15% year over year for the entire year. That is a large drop off from the 43% during 2022 and 36% from Q1. For the years 2024 and 2025 the company expects subscriber growth of 7-11%. This growth is slowing, as one would expect as it continues to get to a larger scale. The revenue estimate of $100 million is growth of 24% which is consistent with Q1. This will start to slow as well with the slowing subscriber additions. It also makes up a small percentage of total revenues for the company at 13%.

Due to the expected growth in cameras and the growth of its subscription business the company expects to continue to generate strong free cash flow and use that to repurchase stock. It expects to repurchase $70 million in stock during 2023. It plans to increase that in 2024 and 2025 to $100 million each year. At the current market value that would be 35% of the current outstanding shares. This would be a very aggressive buyback and provide some significant value to shareholders. This would be partly offset by share count increase due to employee grants. Still a significant amount to be bought.

The company has outlined a path to growth over the next few years. The number of cameras sold will partly be offset by lower margins on the products. That is going to hurt revenue. Also we can see that the subscription business is seeing a slower growth rate going forward. We have seen the company as a whole is stagnating recently. Number of cameras and revenue decreased from 2021 to 2022. It did see growth of 30% in 2021 which might explain the tough year over year comparable. Even with that comparable though, the company sold more cameras in 2020 than in 2022. It did see revenues increase by 18% during that period. That is not great growth for a two year period though. It expects to generate revenue of $1.1 billion for 2023 up from 1.09 billion, basically null growth. These numbers should see some boost in 2024 and 2025 as the company is able to generate a higher margin and increase revenue year over year. Those are also expectations which can always change. Overall I expect the company to see revenue growth, albeit not large going forward. I think the company will return to profitability and see solid cash flows as it has the last few years.

What Will Drive Growth?

While the company has been able to find itself in a profitable position, the latest quarter being the exception. I think the company will continue to operate efficiently and generate a profit. It plans to use much of that cash flow to buy back stock, and a significant amount. These are great things, but there is one overhanging problem with the stock for me. What will drive growth? The company needs a growth catalyst. The company has outlined expected growth in the next few years, but it seems to be at a slower rate.

The subscription business is seeing growth as previously discussed, but not enough to provide growth for the company as a whole. Especially considering this business line is continuing to see slowing growth. It will provide the company the ability to continue on its slow growth rate but not improve it much.

The company needs additional revenue drivers. It is developing a desktop editing experience. It will be included in the subscription service for no additional cost. This is not likely to drive revenues significantly but rather increase retention. It is also launching a premium subscription for GoPro camera owners as well as non-owners. It will be interesting to see if the company is able to produce software that those outside of the GoPro ecosystem will be interested in using. It seems the company is leaning into the software side for potential growth. This might be due to the company failing miserably last time it tried to release the drone. I am not sure if this is the revenue driver or not for the company. It will be worth watching. It is hard to invest in the company at the current price without some type of revenue driver.

It will be worth watching as the company looks to return to growth for the rest of 2023 and going forward in 2024 and 2025. They have a few different video editing software plays that they are pursuing. I am not sure those will drive a significant increase in revenues or not. It will be worth keeping an eye on for sure.

Risks

The company has seen stagnating growth lately. The latest quarter showed slowing growth and also a decreased margin. It is transitioning back to retailers following COVID. The company needs to execute on this transition. There is a risk that it is not able to achieve the higher gross margins that it achieved during the past few years. Many companies saw business increase during COVID. GoPro was no exception. This growth might not continue now that the pandemic has ended.

Conclusion

The company needs a growth catalyst to draw me into the stock. The company is a solid company that has been able to generate value for shareholders. Without new growth driver I think the stock is fairly priced. If it can execute on its expected growth and particularly the large buybacks then there could be some room for growth in the stock, not significant enough to get me to buy. I don't see enough growth in the stock to drive a significant price increase. The company is attempting to push more into software and subscriptions. Including pulling in customers that do not have a GoPro camera. It will be interesting to see if the company is able to pull in enough users to see revenue growth.

I will continue to watch GoPro from the sidelines. I think it is fairly priced and do not see significant growth ahead in either revenues or the stock price. If the company was to experience a pullback in the stock price then it might be worth taking a look. Also if the company is able to find an additional revenue driver then it might be worth a buy. Until then I will rate it a hold.

For further details see:

GoPro Needs A Growth Catalyst