GPRO - GoPro: Recent Rebound Is Difficult To Trust

2023-11-30 06:55:16 ET

Summary

- GoPro's Q3 earnings release led to a 40% rally in its stock, but despite a revenue beat we haven't yet seen true sell-through performance of the new HERO12 camera.

- GoPro stock is additionally rallying on expectations of a margin increase in FY24, but this is predicated on new products that have not yet launched.

- Subscription adds also slowed in Q3, while renewal rates are weak - highlighting concerns on the viability of the subscription business to revitalize GoPro.

An unlikely winner has emerged from the Q3 earnings season: GoPro ( GPRO ), the action-camera maker that was once one of the most lauded hardware makers in Silicon Valley.

I last issued a strong set opinion on GoPro in late October when the stock was trading closer to ~$2.50 per share. Admittedly, my timing was off - GoPro's Q3 earnings release has spurred more than a 40% rally since then. But the question for investors now is: can GoPro continue rallying to recoup lost ground?

In my view, the answer is no - I remain very bearish on GoPro especially as its subscription trends slow down and weak renewal rates emerge.

What's driving the stock upward? Strong revenue and bullish FY24 commentary

It would be remiss not to start with where GoPro excelled in Q3, which drove expectations higher and spurred a rally in the stock. First - the company launched its latest flagship camera, HERO12, in September. Though the third quarter (ending on September 30) is not really indicative of sell-through data for a product that only launched on September 30, it's worth noting that GoPro's revenue beat expectations in Q3, which is a testament to strong inventory buildup/channel fill on the new product.

{kind=link}

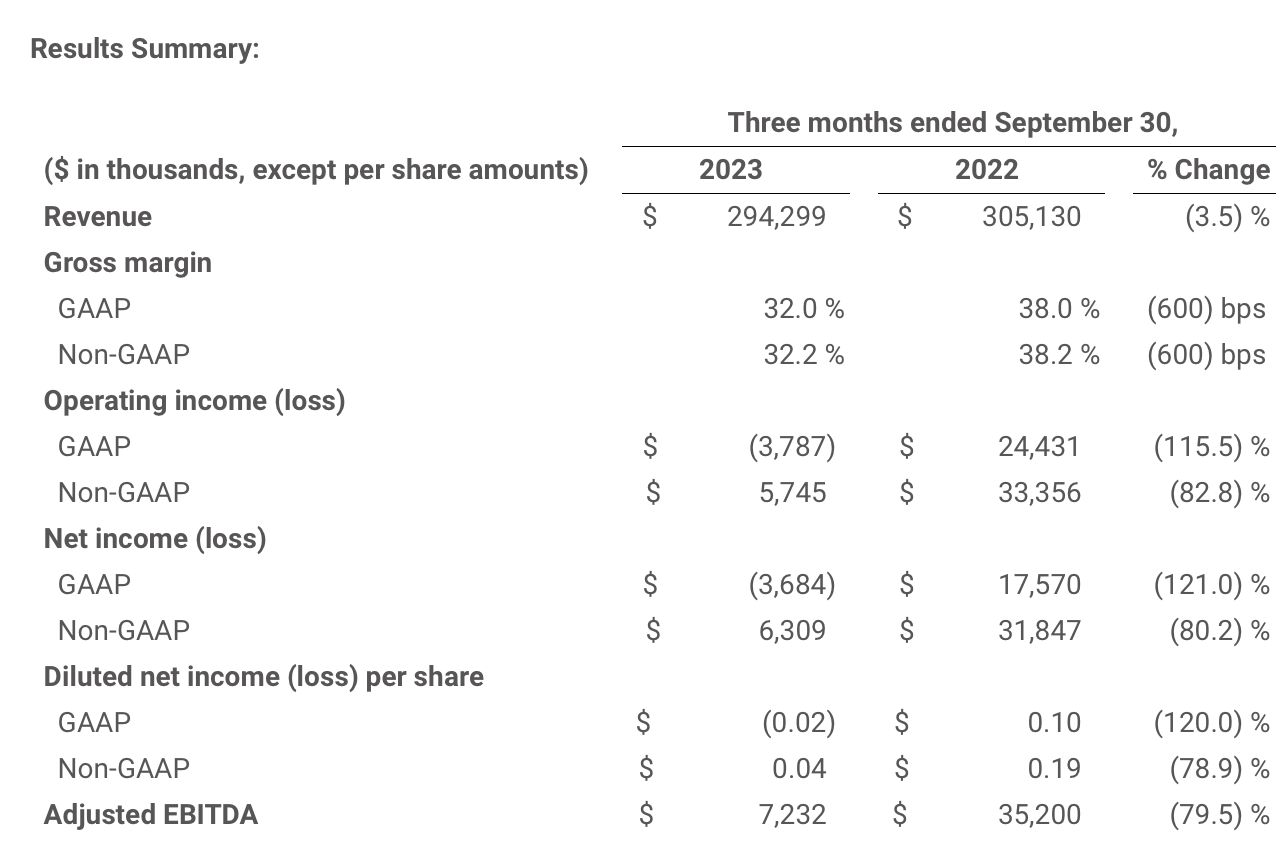

GoPro's Q3 revenue declined -3% y/y to $294.3 million, but that's ahead of Wall Street's expectations of $281.5 million, which would have represented a -8% y/y decline or five points worse.

The company notes that outperformance, in part, was driven by retail door expansion. GoPro had initially targeted to add 2,000 new doors by the end of 2023; as of the third quarter, GoPro has already blasted through that target with 2,500 adds.

The second bright point for GoPro: the company is working to diversify its product lineup in a way that will improve margins starting from FY24, in which it is hoping for 500bps of gross margin expansion to 37%. Per CEO Nick Woodman's remarks on the Q3 earnings call :

To further leverage our growing retail network, we're going to expand our TAM. Over the next two years, we plan to introduce several new types of cameras beginning in the second quarter of 2024. We believe each of these new camera SKUs will address distinct use cases and will be built at improved margin profiles, which we expect to contribute materially to revenue and earnings in 2024 and 2025"

CFO Brian McGee, meanwhile, provided the margin outlook:

We expect to improve gross margin of 32% in 2023 to 37% plus or minus 50 basis points in 2024, driven by the following factors: by approximately 230 basis points from the introduction of our lower cost entry level product in Q2 2024; 150 basis points from price protection incurred in 2023 for the strategic price move; approximately 80 basis points from identified product component cost savings; and approximately 70 basis points from subscription growth and other improvements. We expect operating expenses to grow modestly from $365 million in 2023 to approximately $385 million in 2024."

I would take each of these positive drivers with a grain of salt, however. First - sell-through data on HERO12 is not yet clear, and revenue outperformance in Q3 might reverse in Q4 if holiday sales are weak. Second, surrounding the potential margin gains from new products - what has worked for GoPro over the past few years has been a reduction in price to get more subscribers in the door. It's unclear how the company intends to build this new product at a higher margin, unless cost savings are going to be substantial enough to prevent any price upticks.

The bottom line here: GoPro's ~40% rally counts a lot of chickens before they're hatched.

Subscription metrics continue to be concerning

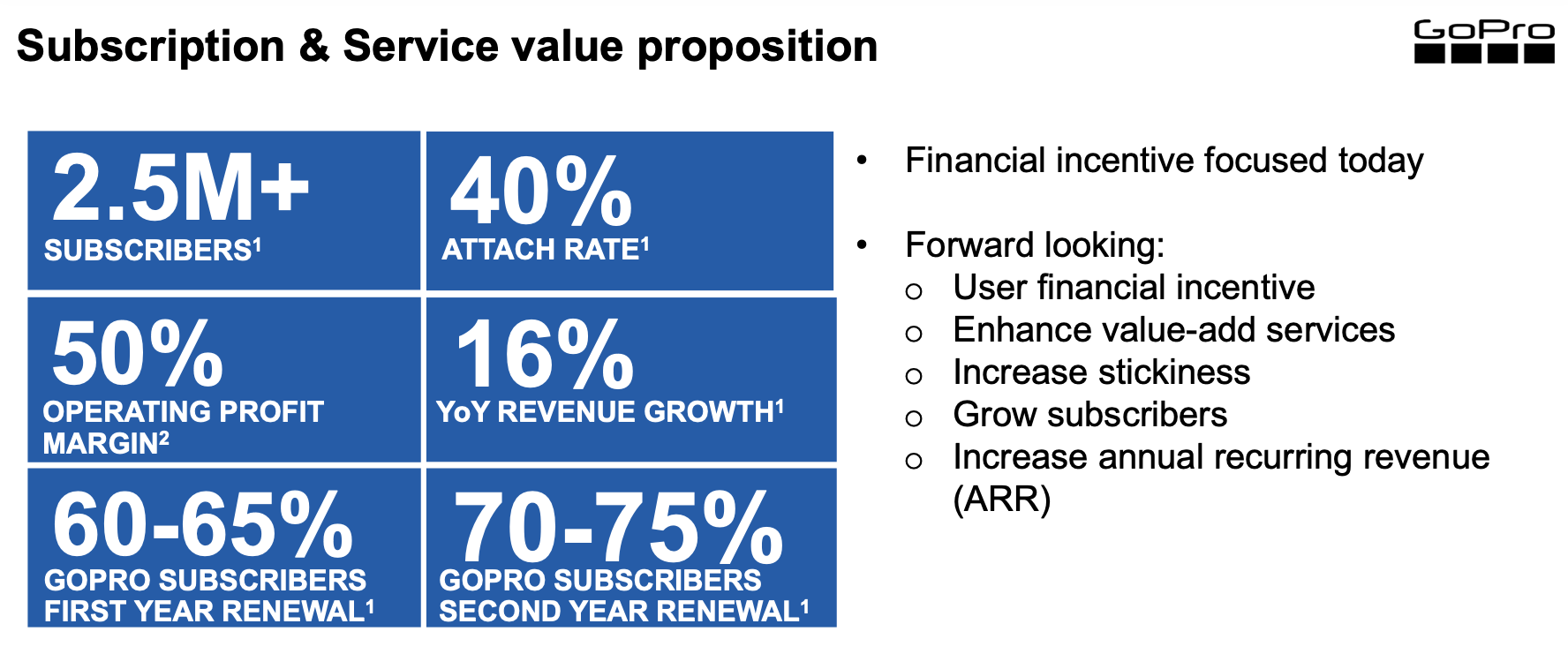

The tentpole of GoPro's turnaround strategy over the past year has been to build its subscription offering. Yet even today, subscription revenue at 9% of total revenue is still a small contributor.

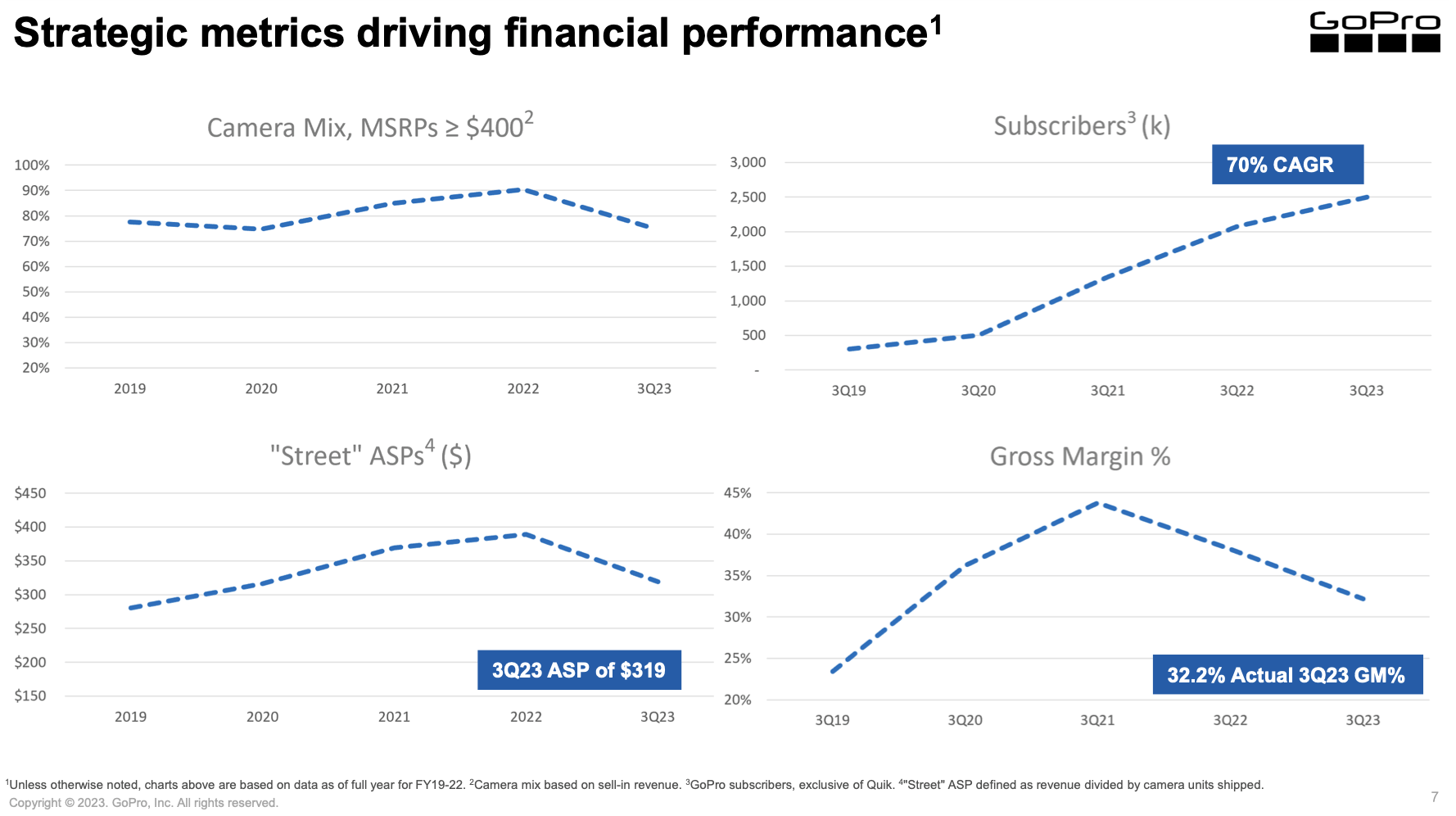

The company's strategy has been to push more entry-level cameras and bring street ASPs down to encourage more potential subscribers into the GoPro fold, where it reached a multi-year low of $319 in Q3.

{kind=link}

But alongside that, subscriber growth in Q3 slowed to 20% y/y to 2.5 million total subscribers - versus 27% y/y growth in subscribers in Q2.

Further, GoPro revealed its renewal metrics in the chart below: note that only 60-65% of subscribers renew in Year 1 after signing up, and even that cohort of customers only has a 70-75% chance of renewing for the second year:

{kind=link}

To me, this is a symptom of GoPro's highly incentivized sign-up offers, which I noted in my prior article. The company offers subscribers $100 off their next GoPro camera, as well as 50% off accessories and peripherals on GoPro.com - compared to a $25/year first-year subscription cost, and $50/year in the second year and beyond. In other words, subscribers realize instant value upon signing up for their subscriptions - which makes it a small wonder that GoPro enjoys a high attach rate, especially on entry-level camera models.

But we have to wonder - is this subscription business sustainable, especially when only 60-65% of these promotionally-incentivized signups are renewing for a full-price subscription in their second year? To me, GoPro's subscription program is financially a price cut and revenue deferral disguised in the form of recurring revenue. And with subscriber growth slowing in Q3 even amid a new camera launch, subscription revenue is unlikely to be the pillar that saves GoPro.

Key takeaways

In my view, the recent post-Q3 rally in GoPro shares is unlikely to be long-lived. We have yet to see whether HERO12 will perform in the holiday season; nor are we confident that GoPro can achieve the 5-point improvement in gross margins that it has guided to (and even at this 37% guidance, gross margins would still be several points weaker than 2022 and 2021 levels in the low 40s).

Steer clear here and maintain caution.

For further details see:

GoPro: Recent Rebound Is Difficult To Trust