GPRO - GoPro: Solid Performance And Sound Business Fundamentals

Summary

- GoPro's pivot to a subscription-based business model is a significant high-margin growth opportunity.

- GoPro has sound business fundamentals with a strong balance sheet to weather the current challenging macro environment.

- GoPro management's commitment to profitability and cash generation makes it a good stock to invest in at the current price.

Editor's note: Seeking Alpha is proud to welcome Ramkumar Raja Chidambaram as a new contributor. It's easy to become a Seeking Alpha contributor and earn money for your best investment ideas. Active contributors also get free access to SA Premium. Click here to find out more »

GoPro's ( GPRO ) success in pivoting toward a subscription-based model will help it grow revenues after the company becomes profitable for a fourth consecutive year on a non-GAAP basis. Moreover, as GoPro's paying subscribers exceeded 2 million in 2023 with $100 million in annual recurring revenue at 70%-80% gross margins, the company has succeeded in building brand recognition that will create competitive advantages. Accordingly, my recommendation for investors with shares of GoPro in their portfolio is to hold them; for investors who do not, my recommendation is to buy them for the long term.

About GoPro

GoPro, headquartered in San Mateo, Calif., develops and sells cameras and wearable accessories, subscription services, and software in the U.S. and globally. The company was founded in 2002 as Woodman Labs and changed its name to GoPro in February 2014.

GoPro targets consumers and professional users interested in capturing high-quality photos and videos for personal or professional use. The company's primary business model is selling its hardware products, such as cameras and accessories, directly to consumers through its website and retail channels. GoPro also generates revenue from licensing its technology and user-generated content to third-party companies. Additionally, the company offers cloud services and subscription plans for accessing and sharing footage captured on its cameras.

In the last 30 days, GoPro's share price has witnessed an appreciation of 10.9%. However, the share price declined by 11.9% on Friday, Feb. 3, after the earnings report.

One-month Price movement (NASDAQ)

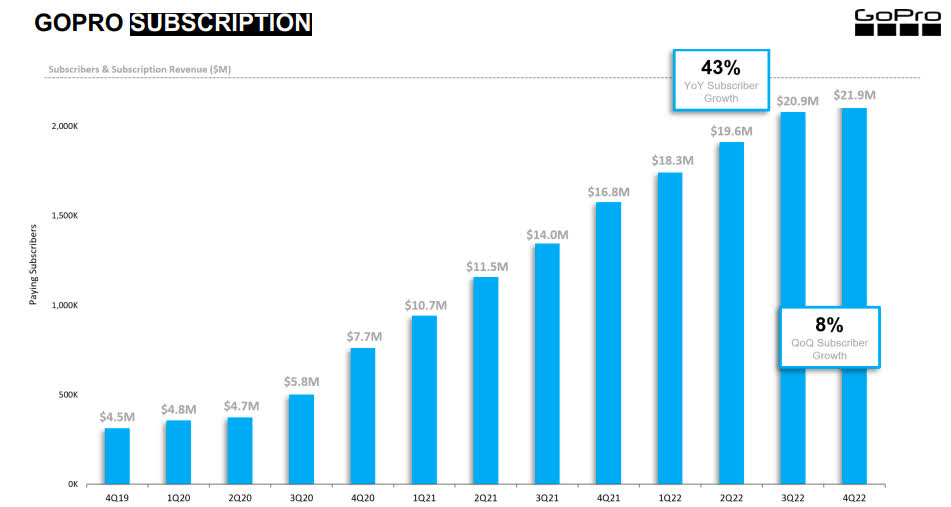

On Feb. 2, the company released its earnings summary for Q4 2022 . It posted impressive subscription revenues that went from $20.9M in Q3 2022 to $21.9M in Q4 2022, which was growth of 20.6% in subscription revenues. Furthermore, it had subscriber growth of 8% QoQ from Q3 2022 to Q4 2022.

{kind=link}

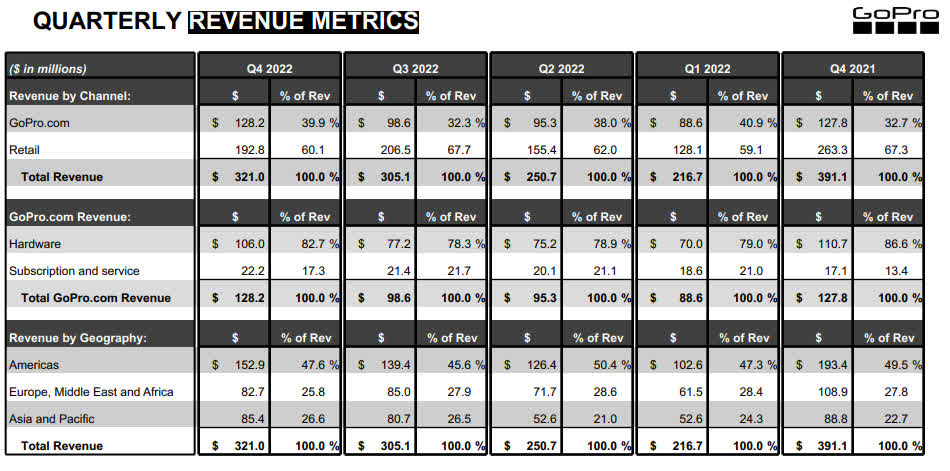

The company shipped 850,000 cameras in Q4 2022, an increase of 29.4% from 797,000 cameras in Q3 2022. Additionally, GoPro posted impressive 22.5% QoQ revenue growth, from $305.1 million in Q3 2022 to $321 million in Q4 2022. Though the company's gross margins declined from 38.2% in Q3 2022 to 35.1% in Q4 2022, its revenue mix from GoPro.com as a percentage of overall revenues has improved from 32.3% in Q3 2022 to 39.9% in Q4 2022. The Americas continues to be GoPro's biggest market, with 47.6% of its revenues coming from the U.S.

However, its revenues across geographies decreased this year, with Europe decreasing by 24%, the Americas decreasing by 21%, and APAC decreasing by 4% annually due to macroeconomic factors and a strong U.S. dollar. Nevertheless, on an annual basis, APAC was the shining light growing at 9% as most regions in APAC emerged from 2021 lockdowns.

{kind=link}

GoPro's D2C revenues are 40% of its overall revenue in Q4 2022 and 38% in 2022, up from 33% and 34%, respectively. Another positive factor is that its GoPro.com business posted 5% growth in 2022 over 2021, driven primarily by 52% growth in subscription and services revenues.

GoPro closed 2022 with revenues of $1.09 billion with 9% EBITDA, generating $95 million in EBITDA. In addition, the company plans to utilize $40 million of its EBITDA proceeds for share buybacks to cover its stock compensation expense.

Despite the strong USD, GoPro's latest results demonstrate the strength of its subscription-based business model's strong execution. According to the Founder, CEO, and Chairman of GoPro Nicholas Woodman :

Our high-margin subscription business is a powerful financial engine, contributing meaningfully to our bottom line and, significantly, building LTV into our model as the GoPro subscription is becoming increasingly synonymous with being a GoPro camera owner.

For GoPro, driving subscriber engagement is their crucial focus, supporting retention and LTV. Again, as per the CEO:

New features that enhance capability and convenience are key drivers of engagement - like automatic highlight videos sent to subscribers after their footage auto-uploads to their GoPro cloud accounts and the automatic clearing of the camera's SD card once that upload is complete.

These new features helped subscribers connect their HERO11 cameras to the cloud and have contributed to an increase in camera usage among its customer base, resulting in a 58% increase in subscribers annually. As per Woodman:

We believe these features also contributed to increased camera usage amongst our broader customer base - in 2022, camera usage increased 15% year over year to approximately 15 million unique cameras connecting to our app.

The company managed to grow its subscriber base by 43% last year, with its subscriber count exceeding 2.25 million. Thus, GoPro's subscription currently generates more than $100 million in annual recurring revenues with an impressive gross margin of 75%. The company believes its future lies in a subscription-based business model and is laser focused on pursuing this significant high-margin growth opportunity.

Furthermore, its Quik model subscription that serves non-GoPro-owning customers has grown 26% annually, reflecting the company's commitment to engaging and retaining customers that don't own a GoPro. The company treats these customers as an important TAM-expanding opportunity and plans to target them further with its upcoming premier-tier desktop app launch.

The company has also done a restructuring exercise by closing its camera production facilities in Mexico, incurring an $8 million restructuring charge. The company expects its production facilities in Thailand and China to meet future demand.

Balance Sheet Metrics (GoPro Earnings)

{kind=link}

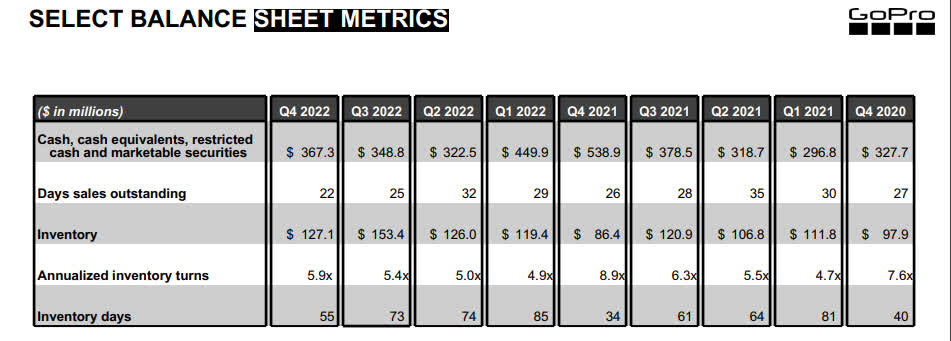

The company's balance sheet is healthy as it ended Q4 2022 with $367 million in cash reserves and $224 million net of debt. In addition, as the company pivots to the subscription model, its DSO outstanding has been reduced to 22 days. Furthermore, the company has shown prudence in managing its supply chain and inventory by ending its inventory days at 55 days.

In the future

As the macroeconomic environment remains challenging, forecasting growth for GoPro becomes difficult. Still, I will put forward my best estimate by looking at the firm's current business model and accounting for the possibility of a global recession in 2023, leading to cautious customer spending. From a demand perspective, the first quarter generally is the weakest for GoPro, and I assume that will not change in Q1 2023. The company forecast $165 million in Q1 2023, which is 45% of Q4 2022 revenues. As revenues decline, it will also result in a contraction of gross margin to 36% due to a stronger USD.

In the future, GoPro's management has decided to focus on the following priorities:

- Maintaining profitability and higher commitment to cash generation.

- Investments in quality skill force, technology and innovation to drive subscriber growth, retention and LTV.

- Growing the subscriber base leading to subscription and service revenues surpassing $100 million.

Risks

GoPro's revenues outside the U.S. are more than 50%, and any further strengthening of the U.S. dollar will impact its future earnings growth on a constant currency basis.

The subscription attach rate, which refers to the percentage of customers who subscribe to the additional product when they purchase a primary product, is a crucial metric that will determine GoPro's growth. At the current subscription attach rate of 90% , GoPro has increased the number of customers who buy cameras at GoPro retail stores and later subscribe via its app. However, any reduction in the subscription attach rate will adversely impact their subscription revenues and future profitability.

GoPro Valuation

I value GoPro looking at its recent financial numbers and going with its story of pivoting toward the subscription model. Thus, the story behind my DCF valuation will incorporate these estimates.

Before I value GoPro using DCF, I will compare GoPro with its peers to see how it performs against them. I have identified the following companies as its peers:

- Avid Technology (AVID)

- Canon (CAJ)

- Nikon Corporation (NINOY)

- Eastman Kodak (KODK)

First, I looked at the critical market multiples to understand how GoPro looks relative to its peer group.

| Name |

| P/E Ratio |

| Total Debt / Total Capital |

| Return on Equity |

| Return on Invested Capital |

| Revenue CAGR (5y) |

| Asset Turnover |

| EBIT Margin |

| Avid Technology, Inc. |

| 31.14 |

| 12.9% |

| NM |

| NM |

| -4.3% |

| 1.73 |

| 13.1% |

| Canon Inc. |

| 12.00 |

| 14.2% |

| 8.1% |

| 7.2% |

| 0.6% |

| 0.82 |

| 8.8% |

| GoPro, Inc. |

| 30.76 |

| 17.3% |

| 4.7% |

| 4.2% |

| -0.4% |

| 0.94 |

| 4.3% |

| Eastman Kodak Company |

| NA |

| 41.0% |

| 1.8% |

| 4.6% |

| -6.9% |

| 0.64 |

| 4.7% |

GoPro's ROE looks better vs. its peers and has reasonably low leverage, with its debt to total capital at 17.3%.

From an operational perspective, GoPro's ability to generate free cash flows is better than its peers. Its lower cash-to-conversion cycle is a testament to its pivot to the subscription model.

| Name |

| Gross Profit Margin |

| Return on Assets |

| Asset Turnover |

| Cash Conversion Cycle |

| Levered Free Cash Flow |

| Avid Technology, Inc. |

| 66.2% |

| 18.6% |

| 1.73 |

| 50 days |

| 39 |

| Canon Inc. |

| 45.3% |

| 5.3% |

| 0.82 |

| 122 days |

| 785 |

| GoPro, Inc. |

| 37.9% |

| 2.5% |

| 0.94 |

| 30 days |

| 140 |

| Eastman Kodak Company |

| 13.3% |

| 0.7% |

| 0.64 |

| 88 days |

| -174 |

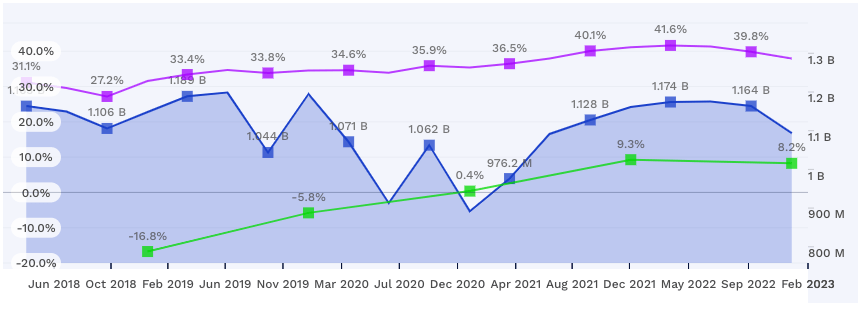

Before arriving at the intrinsic value of GoPro using discounted cash flow, I plotted a graph to understand how GoPro's gross margin and non-GAAP EBIT margin have evolved in the last five years.

{kind=link}

GoPro's non-GAAP EBIT margins became positive in 2021, and although the margins declined in 2023, the decline is due to the challenging macroeconomic factors and the strengthening of the USD. Furthermore, it's evident from management commentary that GoPro focuses on profitability and free cash flow generation.

GoPro's asset efficiency has improved due to its pivot toward the subscription model, as the asset efficiency improved from 12% in 2021 to 26% in 2022. This increase in asset efficiency implies that GoPro has effectively used its assets to generate profits and is earning a high return on its assets relative to its investment.

Author calculations

I use the non-GAAP financial measure of GoPro's financials for operating income and net income numbers for my valuation because it gives a better picture of the company's operating performance and an accurate representation of its underlying cash flows. So, in my DCF valuation, I forecast the following value drivers:

Revenue growth of 10% in the next five years and 7.1% in the next ten years. I base my estimate on the management's commentary on expanding its TAM to target non-GoPro users.

As GoPro continues to pivot toward a subscription model, its EBIT margin will expand, and I forecast GoPro's EBIT to expand from 8.3% in the current year to 10% in the next 10 years.

As GoPro continues to improve its asset turnover, I estimate its sale/invested capital to move to the industry average of 2.23. In addition, management's move to restructure its operations and close production facilities with poor utilization gives me confidence that GoPro will succeed in achieving this target.

Before I value DCF, I capitalize the R&D expenses because R&D expenses have future economic benefits. For example, GoPro has incurred $139 million in R&D expenses. First, I convert these R&D expenses from operating expenses to capital expenditures. Then, I amortize the R&D expenses for three years. After that, I add the unamortized portion of $280 million to the balance sheet. By capitalizing on R&D expenses, I get an accurate representation of the resources GoPro have devoted to future growth and their investment in intangible assets that will help me to determine the ROIC and conclude whether GoPro earns excess returns.

| Year |

| R&D Expense (in ) |

| Unamortized portion (in ) |

| Amortization this year (in ) |

| Current |

| 139.77 |

| 1.00 |

| 139.77 |

| -1 |

| 142.59 |

| 0.67 |

| 95.06 |

| 47.53 |

| -2 |

| 136.19 |

| 0.33 |

| 45.40 |

| 45.40 |

| -3 |

| 150.69 |

| - |

| - |

| 50.23 |

| Value of Research Asset |

| 280.22 |

| 143.16 |

| Amortization of assets for the current year |

| 143.16 |

My cost of capital for GoPro is 13%, taking into account the risk-free rate of 3.86%. As GoPro gets more than 50% of its revenues outside the U.S., I account for the country's risks to arrive at equity risk premiums. As a result, my weighted ERP for GoPro is 5.92%.

GoPro has $185 million in debt, and at an effective interest rate of 4.6%, my pre-tax cost of debt for GoPro is 4.93%. At an effective tax rate of 23%, my after-tax cost of debt for GoPro is 3.79%.

The unlevered beta for GoPro is 1.61, and with 16.05% in debt to capital, the levered beta is 1.85. I derive a cost of equity for GoPro as 14.8% and a cost of capital at 13.04%.

{kind=link}

My 10-year valuation for GoPro is below:

| Estimating the value of growth |

| Value/Share |

| Value of assets in place = |

| 478.37 |

| 3.07 |

| Value of stable growth = |

| (2.38) |

| (0.02) |

| Value of extraordinary growth = |

| 482.34 |

| 3.09 |

| Value of Operating Assets = |

| 958.32 |

| 6.15 |

I arrive at the Enterprise value for GoPro at $6.15 per share. After adding GoPro's current cash reserves of $367 million and subtracting its total debt of $184 million, I derive the equity value at $1.141 billion and $7.32 per share.

As of Feb. 3 2023, GoPro trades at $5.69 per share. Thus, the stock has a potential upside of 28.6% to reach its fair value of $7.32 per share, according to my DCF calculations. Below are my estimates:

| Invested capital at the start of the valuation |

| 676.17 |

| Invested capital at the end of the valuation |

| 1,025.36 |

| Change in invested capital over ten years |

| 349.19 |

| Change in EBIT*(1-t) (after-tax operating income) over 10 years |

| 120.84 |

| Marginal ROIC over ten years |

| 34.61% |

| ROIC at the end of the valuation |

| 9.46% |

| Average WACC over the ten years (compounded) |

| 13.03% |

| Your calculated value as a per cent of the current price |

| 130.64% |

| Revenue CAGR |

| 7.11% |

| Median EBIT% in 10 years |

| 8.88% |

As a next step, I ran a Monte Carlo simulation to determine at what percentile my valuation lies. The following are my value drivers for that:

- Revenue growth

- Target operating margin

- Sales to invested capital

I used a truncated normal distribution for revenue growth with a mean of 10% and a standard deviation of 34%. I used a triangular distribution for EBIT with a minimum margin of 3% and a maximum of 10%. For sales to invested capital, I use a uniform distribution with a minimum value of 0.96 and a maximum of 2.

| Coefficient of Determination, r-squared |

| Excel RSQ, 10000 Trials |

| Intrinsic equity value= |

| Revenue Growth= |

| Target Operating Margin= |

| Sales to Invested Capital= |

| Intrinsic equity value= |

| 1.0000 |

| 0.0050 |

| 0.6056 |

| 0.2693 |

| Revenue Growth= |

| 0.0050 |

| 1.0000 |

| 0.0002 |

| 0.0000 |

| Target Operating Margin= |

| 0.6056 |

| 0.0002 |

| 1.0000 |

| 0.0001 |

| Sales to Invested Capital= |

| 0.2693 |

| 0.0000 |

| 0.0001 |

| 1.0000 |

The r-square is high between equity value and target operating margin, implying that improving margin is more important than growth for GoPro's valuation to improve. GoPro's management, with its focus on profitability and cash generation, is focused on the same metric.

Below is my distribution of values for equity values at different percentiles using the Monte Carlo simulation.

Author calculation

| Intrinsic equity value= |

| Revenue Growth= |

| Target Operating Margin= |

| Sales to Invested Capital= |

| 0.0% |

| (4.12) |

| 3.86% |

| 2.59% |

| 0.96 |

| 0.5% |

| (0.23) |

| 3.95% |

| 3.28% |

| 0.96 |

| 1.0% |

| 0.38 |

| 4.02% |

| 3.59% |

| 0.97 |

| 2.5% |

| 1.61 |

| 4.27% |

| 4.21% |

| 1.00 |

| 5.0% |

| 2.43 |

| 4.68% |

| 4.87% |

| 1.03 |

| 10.0% |

| 3.27 |

| 5.48% |

| 5.83% |

| 1.11 |

| 15.0% |

| 3.81 |

| 6.34% |

| 6.55% |

| 1.19 |

| 20.0% |

| 4.20 |

| 7.17% |

| 7.16% |

| 1.26 |

| 25.0% |

| 4.55 |

| 7.92% |

| 7.72% |

| 1.34 |

| 30.0% |

| 4.85 |

| 8.72% |

| 8.22% |

| 1.42 |

| 35.0% |

| 5.11 |

| 9.59% |

| 8.68% |

| 1.50 |

| 40.0% |

| 5.34 |

| 10.40% |

| 9.09% |

| 1.58 |

| 45.0% |

| 5.60 |

| 11.11% |

| 9.47% |

| 1.65 |

| 50.0% |

| 5.84 |

| 11.94% |

| 9.81% |

| 1.74 |

| 55.0% |

| 6.08 |

| 12.72% |

| 10.17% |

| 1.82 |

| 60.0% |

| 6.33 |

| 13.52% |

| 10.49% |

| 1.89 |

| 65.0% |

| 6.56 |

| 14.31% |

| 10.83% |

| 1.97 |

| 70.0% |

| 6.81 |

| 15.08% |

| 11.13% |

| 2.05 |

| 75.0% |

| 7.08 |

| 15.94% |

| 11.45% |

| 2.13 |

| 80.0% |

| 7.41 |

| 16.82% |

| 11.83% |

| 2.20 |

| 85.0% |

| 7.81 |

| 17.63% |

| 12.25% |

| 2.27 |

| 90.0% |

| 8.30 |

| 18.41% |

| 12.78% |

| 2.35 |

| 95.0% |

| 9.10 |

| 19.27% |

| 13.40% |

| 2.43 |

| 97.5% |

| 9.82 |

| 19.63% |

| 13.88% |

| 2.46 |

| 99.0% |

| 10.54 |

| 19.85% |

| 14.28% |

| 2.48 |

| 99.5% |

| 11.14 |

| 19.92% |

| 14.50% |

| 2.49 |

| 100.0% |

| 13.54 |

| 20.00% |

| 14.98% |

| 2.50 |

The median or 50th percentile for GoPro is $5.8/share, and its maximum price at the 100th percentile is $13.5/share. My valuation of GoPro at $7.32/share puts it between the 75th and 80th percentile, implying that my estimate of GoPro is above the median.

Furthermore, when we look at GoPro's price/book value over the last 10 years and plot it against ROIC, I see that its P/B value is decreasing and ROIC is improving.

Author Calculations

At the current market price, GoPro's P/B value is the lowest it's been in the last 10 years. At the same time, the company's ROIC has improved from -6.7% in 2019 to 9.1% in 2023. Thus, at the current market price of $5.69, GoPro looks undervalued and underpriced from an investment perspective.

While the current macroenvironment is challenging, economists predict that growth in the U.S. will rebound in 2024 as inflation ebbs further and the Fed begins to loosen monetary policy. GoPro has an effective business model and good products. Thus, GoPro's performance should improve, resulting in better earnings once the U.S. economy recovers. Furthermore, as more than 50% of GoPro's revenues come from outside the U.S., as the strength of the USD comes down, it will reflect better earnings performance in the future.

For further details see:

GoPro: Solid Performance And Sound Business Fundamentals