GPRO - GoPro: The Turnaround Story Is Over

2023-10-30 21:12:44 ET

Summary

- GoPro's recent decision to drop camera prices is hammering its gross margins while not producing meaningful lifts in subscription revenue.

- Its subscription program is heavily discounted in the first place, making it unlikely to be a major profit generator in the future.

- Though the company previously succeeded in downsizing, its headcount is growing again, which is leading to larger losses.

- Downgrading GoPro to strong sell, especially in this high interest rate environment.

- The next catalyst for the stock is Q3 earnings on November 7.

Amid incredibly tough macro conditions for most stocks, it's easy to see why markets have sold off so dramatically over the past few months. With interest rates topping 5%, it doesn't make much sense to put cash toward speculative plays - and GoPro ( GPRO ), at least at this moment, is nothing but speculation.

Once a scion of Silicon Valley startups, GoPro has already gone through a boom-and-bust cycle. It managed a temporary resurgence amid the pandemic when the company decided to downsize its headcount and focus on subscription offerings. Now, however, recent trends aren't showcasing much improvement as this brand starts to fade.

I last wrote on GoPro in August, giving the stock a sell rating before it released its second-quarter earnings. Since then: results have come in terribly, profitability has been kicked to the wayside, and the continued upward march of interest rates makes it even more ludicrous to consider investing in a stock as risky as GoPro.

Q3 earnings are also up soon, on November 7. In my view, I think we'll continue to see margin shrinkage and weak sales, which will draw more pessimism for the stock. In light of these conditions, I am downgrading GoPro to a strong sell. At one point, I championed the company's maturity in choosing to shrink its headcount to focus on its core business: but today, I see headcount and opex continuing to trickle upward while subscription revenue, though growing, can't contribute enough to the top line to make up for decaying hardware sales.

These are the two core red flags I see in GoPro going forward:

- Better products mean longer replacement cycles. A GoPro buyer is already a niche customer since we already all travel with cameras in our pockets everywhere we go. Ostensibly, GoPros also get used infrequently (unless you're a daily surfer or skydiver). It's not difficult to posit, then, that as GoPro continues to upgrade its technology, replacement cycles get longer and longer as upgrades become more minimal and older products last for longer.

- Subscriptions won't ever become a meaningful business for this company. Already barely a tenth of overall company revenue and slowing to a ~20% growth rate, GoPro's subscription offering is unlikely to become a meaningful contributor to the bottom line - especially when the company is utilizing deep discount tactics to pad its subscriber count.

Steer clear here: I don't see this company as a long-term investment that will muster enough resources to make a second comeback.

No confidence in subscription offering

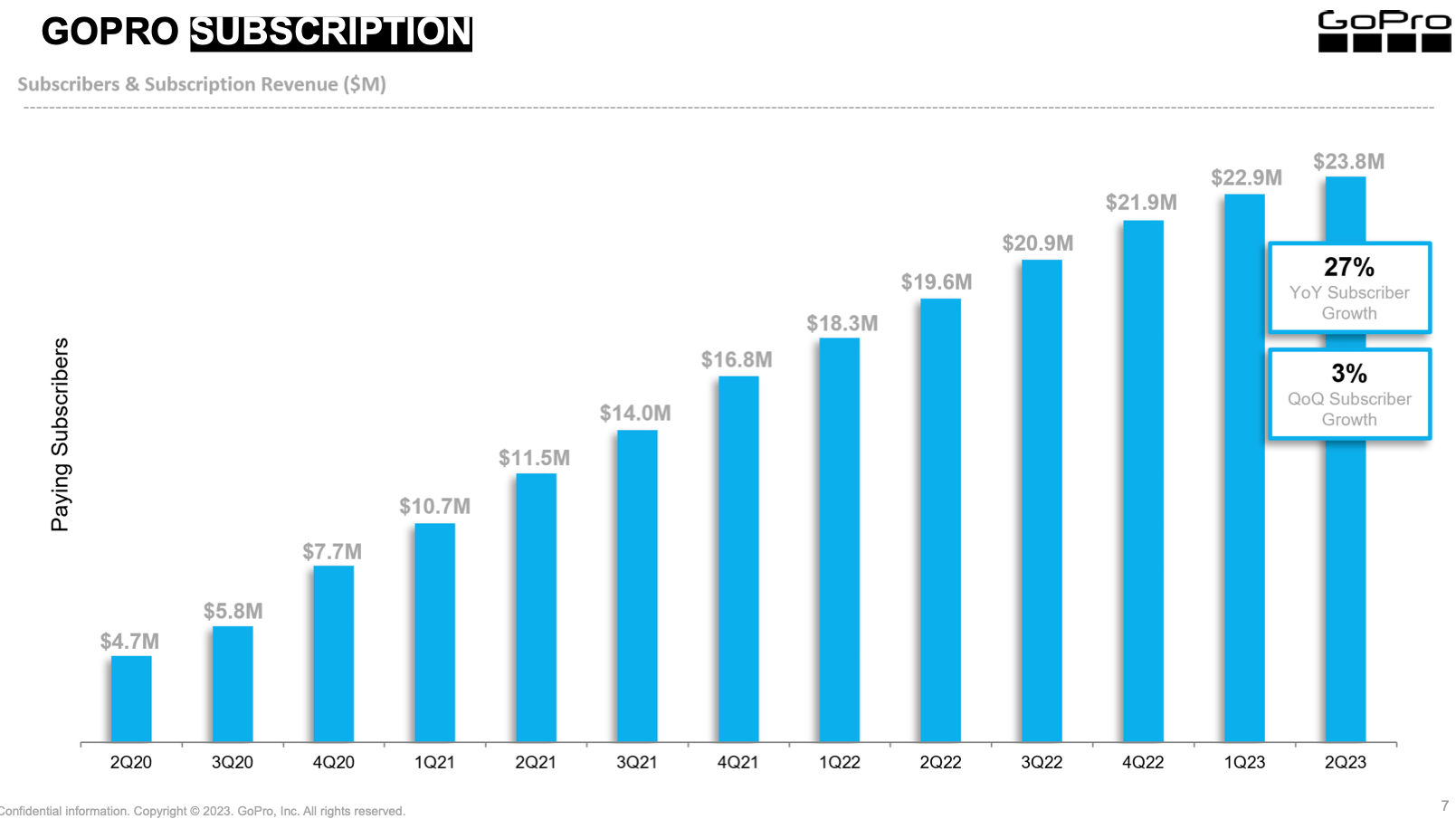

For the past two years, GoPro has banked the entire company on its subscription program. As of its most recent quarter, GoPro had amassed 2.44 million subscribers, up 27% y/y, while subscription revenue grew 21% y/y to $24 million in Q2.

GoPro subscription metrics (GoPro Q2 investor deck)

{kind=link}

Yet even though hardware revenue is declining while subscriptions are growing double-digits, subscription revenue is still less than 10% of overall company revenue of $241 million.

Recall that GoPro earlier this year made the decision to slash camera prices in order to stimulate growth in the install base and spur subscription sales. Street ASPs, or the average price of a GoPro on the market including reseller list prices, declined -13% y/y in the second quarter to $342. The drop in camera prices also had a stark impact on GoPro's gross margins - more on that in the next section.

Despite this, quarterly subscription revenue run rates have barely increased by more than $2 million since the start of the year - the company had much better run-rate increases in 2021 and 2022, without price drops.

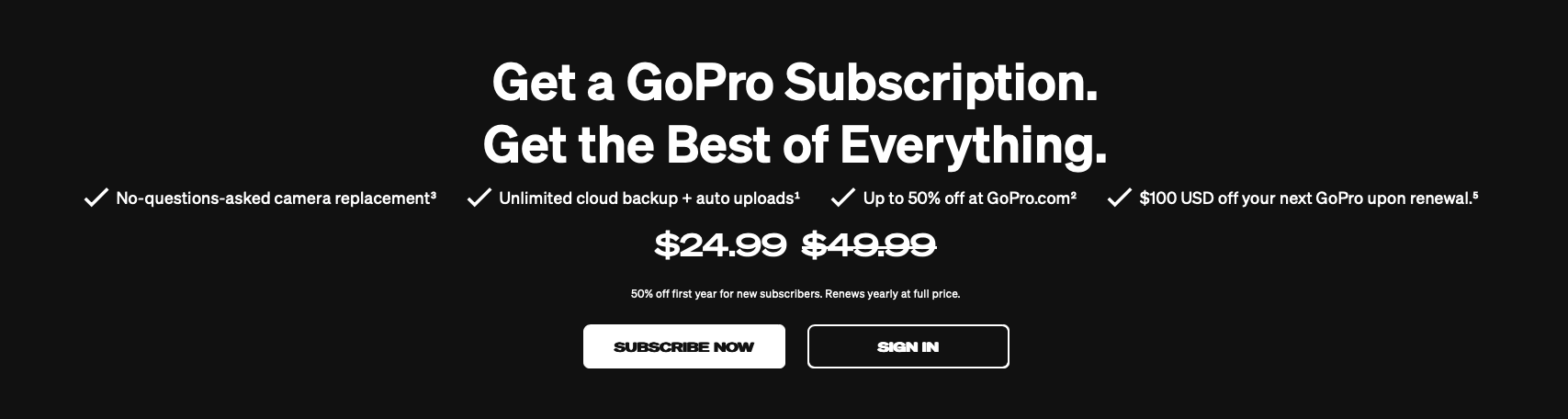

We note as well that the company has resorted to exorbitantly discounted tactics to get subscribers in the door. Note the following offers and benefits in the snapshot taken from GoPro.com below:

GoPro subscription benefits (GoPro.com)

{kind=link}

A subscriber only has to pay $25 in the first year, and $50 upon renewal, to get a $100 discount on a new camera (effectively making money across a two-year timespan). This doesn't include the subscription program's warranty benefits, heavily discounted GoPro accessories and peripherals on GoPro.com, and cloud backup benefits.

We have to ask ourselves: with such deep discounting, not only on reduced camera prices but on introductory offers on subscription plans, is GoPro effectively just bucket-switching revenue out of hardware and into services in the hopes of getting more investors on board?

I also think that weak hardware sales will eventually play out into weak subscription growth (after all, new hardware buyers are the primary captive market for services attached). In my view, Q3 results will show a similar near-flatlining of sequential subscription revenue and call greater question to the services narrative.

Financials show a slide across all metrics

The idea behind the services push, of course, is to create a more sturdy recurring revenue base and improve margins while reducing reliance on lumpy, low-profit hardware sales.

The reality is that none of these goals are coming to fruition. Take a look at GoPro's trended quarterly results in the snapshot below:

GoPro Q2 highlights (GoPro Q2 investor deck)

{kind=link}

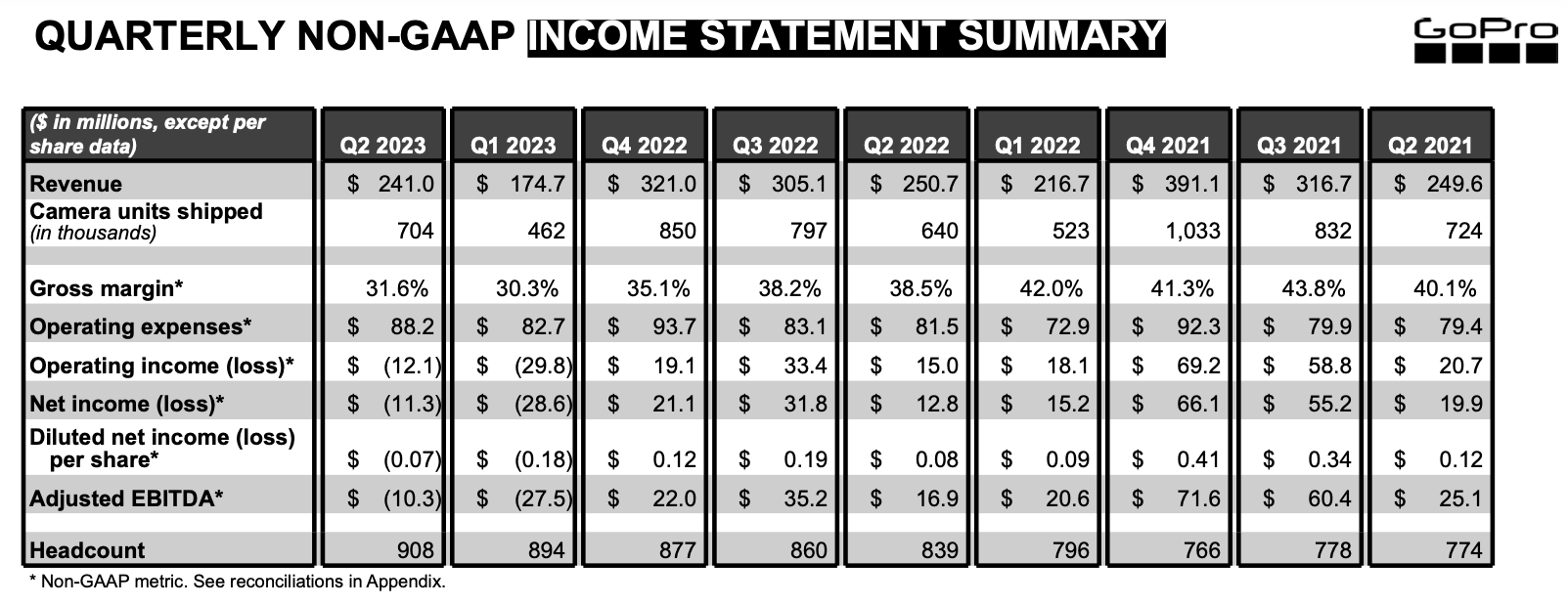

Revenue fell -4% y/y in the second quarter to $241 million. As previously mentioned, subscription revenue grew 24% y/y to $24 million, while hardware dropped precipitously.

The mix shift toward services revenue was not nearly enough to offset gross margin declines from price drops. Gross margins sank 590bps y/y to 31.6%, the second-lowest margin in two years (outweighed only by worse margins in the preceding Q1, a seasonal low for GoPro coming off the holiday quarter). Margins were also impacted by the company's decision to refocus on entry-level cameras with lower prices, again with the hopes that these buyers would be incremental to the install base and consumer services. Per founder and CEO Nick Woodman's remarks on the Q2 earnings call:

As a reminder, the key points of our Q2 updated go-to-market strategy included restoring camera pricing to lower pre-pandemic price points, and discontinuing subscription related camera discounts at the time of purchase at GoPro.com.

Reintroducing entry level price cameras to drive meaningful volume and subscriber growth, restoring our world-class presence at retail, by increasing global distribution to best-in-class retailers that can help drive awareness and sell-through, and scaling our marketing spend to pre pandemic levels over time."

We also don't like the fact that headcount crept back up to 908, an 8% y/y increase (also matched by an 8% y/y increase in opex to $88.2 million). Alongside gross margin declines and revenue drops, this led to steep deleverage in profitability, as adjusted EBITDA sank to -$10.3 million or a -4% margin, versus a 7% adjusted EBITDA profit margin last year.

Key takeaways

In my view, GoPro is trying to focus investor attention on its growing services business, but even a cursory look will tell us that services' revenue contribution is too small to be impactful, in part driven by heavily promotional pricing. With GoPro's losses mounting in the aftermath of camera price cuts and an overall weak sales environment, now is not the right time to plunk any more money into GoPro, especially ahead of a potentially triggering Q3 earnings season.

For further details see:

GoPro: The Turnaround Story Is Over