GOSS - Gossamer Bio: Buying The Savage Dip After A Trial 'Win' May Be Unwise

Summary

- Gossamer Bio, Inc.'s lead candidate - Seralutinib, indicated for Pulmonary Arterial Hypertension - met its primary endpoint in the Phase 2 TORREY study.

- Nevertheless, investors dumped the stock - due to Seralutinib's perceived inferiority to Merck's Sotatercept.

- On a 6-minute walk test and Pulmonary Vascular Resistance, it seems Merck's candidate has the upper hand - and it is closer to commercialization.

- Gossamer has the funds - just about - to push for a pivotal trial, and if it focuses on higher risk patients, results may be reversed.

- It is a high risk strategy - but probably Gossamer's only option - bargain-hunting investors may be best off maintaining a watching brief.

Investment Thesis - When Is A Clinical Trial Success Simultaneously Considered A Failure?

There are several different answers to the above question. Unfortunately, in the case of San Diego-based biotech Gossamer Bio, Inc. ( GOSS ), most of them apply to its Phase 2 "TORREY" clinical study of lead candidate Seralutinib, indicated to treat Pulmonary Arterial Hypertension ("PAH").

The first answer to the above question is when the clinical study data is long overdue.

The TORREY study - which Gossamer announced on 6th December had met its primary endpoint of "change in Pulmonary Vascular Resistance ("PVR") at Week 24" - was initiated in December 2020. This means it has taken 2 years to complete - a long time for a 24-week study.

Management has put the delays down to COVID headwinds, which is a reasonable defense, but unfortunately other PAH therapies have stolen Seralutinib's thunder, producing superior trial data in less time.

Pharma giant Merck & Co., Inc. ( MRK ), for example, reported data from a Phase 3 study of drug candidate Sotatercept - acquired as part of Merck's $11.4bn buyout of Acceleron Pharma in November 2021, and indicated for PAH - in October. It showed that the study met its primary endpoint, which was 6-minute walk distance ("6MWD") at 24 weeks, showing a statistically significant and clinically meaningful improvement over placebo.

Since Gossamer's TORREY study did not achieve statistical significance in 6MWD, the study may also be considered a failure - and to make matters worse for Gossamer, Merck's Sotatercept had PVR as a secondary endpoint, and was able to meet it. In a prior Phase 2 study, Sotatercept achieved a 34% decrease in PVR.

Thirdly, although statistically significant, analysts and the market had made it clear that they were looking for a PVR improvement of at least 20-30%. So, in that sense, the TORREY trial once again comes up short.

Gossamer's Share Price Nosedives - Funding Become An Issue

As a result of all the above, Gossamer stock has fallen in value from $9.3, immediately before TORREY results were announced, to $2.2 at the time of writing - a decline of >76%. Gossamer's market cap now stands at $212m - prior to the results announcement, it had been close to $900m.

Even by 2022 biotech bear market standards, a >75% drop in share price value can be considered a harsh punishment for a study which meets its primary endpoint. But, with that said, the path ahead for Gossamer is a very challenging one.

First of all, Gossamer will need to conduct a Phase 3 study with limited funding and a significantly reduced ability to raise funds given its much lower share price. Management has apparently promised to begin a Phase 3 study in the second half of 2023, with 6MWD as its primary endpoint, but Gossamer only has current assets of $312m, and has made a net loss of $174m across the first 9m of 2022.

Will Gossamer be able to fund a larger scale Phase 3 that may not read out data until 2025? And even if that data were positive, would it be able to successfully launch Seralutinib into a market in which Merck's Sotatercept has established itself as a new standard of care?

PAH Market Crowded & Hard To Penetrate

Merck is by no means the only drug contending for supremacy in the PAH market. There are 4 different types of treatment available for PAH (according to Gossamer's TORREY results presentation), which are endothelian receptor agonists, Prostacyclins, oral PDE5 inhibitors, and sGC stimulators.

United Therapeutics ( UTHR ) is the current PAH powerhouse - its inhalable prostacyclin therapy Tyvaso making $258m of sales in the first 9m of 2022, whilst Remodulin, administered by infusion, earned $114m of revenues, and Orenitram - an oral therapy - earned $87.5m of revenues.

As an injectable Activin receptor 2a regulator, Merck's Sotatercept has a differentiated mechanism of action and administration route to United's therapies, and it may be that it can be used alongside them. However, United, and its founder Martine Rothblatt, has a reputation as a fearsome competitor in the PAH markets, and even Merck, with its billions of dollars of marketing spend, may find it hard to establish a foothold.

Meanwhile, according to Evaluate Pharma , United is working on 2 more therapies - prostacyclin analogue Ralinepag and an endothelial nitric oxide synthase gene therapy. Merck has a second therapy in development - an inhaled guanylate cyclase stimulator - and biotechs Aerovate Therapeutics ( AVTE ), Cereno Scientific, and Resverlogix all have PAH therapies in development which have reached the Phase 2 study stage.

{kind=link}

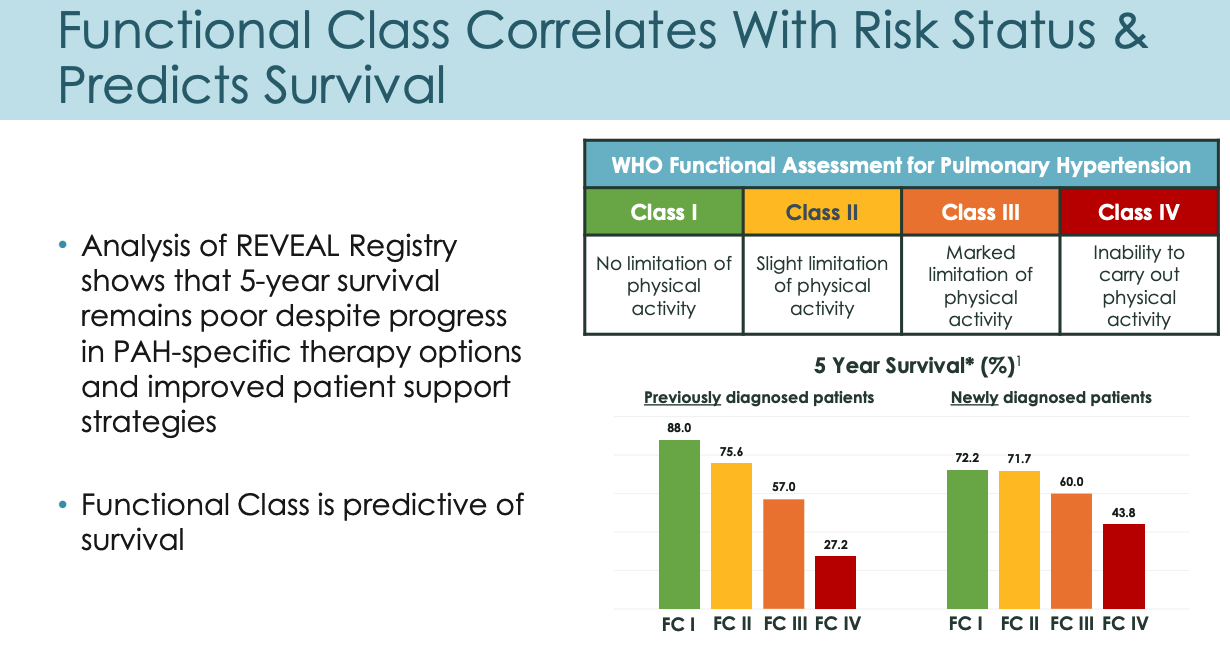

As we can see from the slide above - included in Gossamer's TORREY study results presentation - survival rates for PAH patients remain low, and especially in the case of worse-affected patients.

The disease has a prevalence of ~5-25 cases per million per annum, according to Gossamer, and the market is valued independently as being ~$6bn in size. Peak sales expectations for Sotatercept have been estimated ~$750m (by 2030), and United already drives revenues not far off $1bn per annum from its various drugs.

In theory, then an effective drug against PAH can expect to drive $500m - $1bn in annual peak sales. There are at least a few reasons why some investors may not want to give up on Gossamer and Seralutinib just yet.

Is There A More Positive Outlook For Gossamer?

Gossamer has been quick to point out that its 86-patient Phase 2 study TORREY may have included too many patients with milder forms of PAH, with its results in higher risk groups much more impressive than in the overall population. Management explained in a press release :

Enhanced effects for both PVR and 6MWD were observed in patients with more severe baseline disease, as defined by WHO Functional Class and REVEAL 2.0 Risk Scores.

In FC III patients, a 21% reduction in PVR (p = 0.0427) and 37m improvement in 6MWD (p = 0.0476) were observed for the seralutinib arm vs. placebo.

In patients with a baseline REVEAL 2.0 Risk Score of 6 or greater, a 23% reduction in PVR (p = 0.0134) and 22m improvement in 6MWD (p = 0.2482) were observed for the seralutinib arm vs. placebo.

If Gossamer had reported these results, instead of the 14.3% mean difference between placebo and treatment arm in PVR, and 6.5 meter improvement in 6MWD (~408m overall), then the company's share price may well have been soaring, rather than nose-diving.

Seralutinib's safety profile also seems to have been better than expected, and especially so given that the drug is a PDGFR, CSF1R and c-Kit inhibitor - a class of drug (tyrosine kinase inhibitor) that has been associated with significant safety issues in the past.

There were 6 adverse events ("AE") leading to treatment discontinuation in the treatment arm versus only 1 in the placebo arm, and 93% of patients experienced some kind of AE, but only 1 patient was hospitalized apparently, and the issue resolved itself rapidly.

The fact that Seralutinib has a unique mechanism of action ("MoA") can be considered a positive, as the FDA may be more willing to approve such a drug in the event that over the longer term it proves its superiority. This is potentially much less likely to happen if Seralutinib was, e.g., an injectable like Sotatercept. Its dry powder form of administration may also be advantageous.

What Happens Next?

The next thing for Gossamer to do is meet with the FDA and discuss a trial design for a pivotal Phase 3 study of Seralutinib to begin in the second half of next year.

The company's current funding will last it until 2024 based on current cash burn, and management would ideally want to raise the share price before trying to raise the further funding that would likely be required to bring a pivotal trial to a successful conclusion.

It may be hard to find patients that would suit Seralutinib in a pivotal trial - higher risk patients with more advanced disease progression - so we can expect any pivotal study to last at least 18 months, I would estimate.

Gossamer does have other products in development - candidate GB5121 is a BTK inhibitor indicated for Central Nervous System ("CNS") Lymphoma, in a Phase 1 study, whilst GB7208 - with the same MoA - is indicated for Multiple Sclerosis.

Gossamer did discontinue development of another lead candidate, GB004 - indicated for Ulcerative Colitis ("UC") - back in April this year, after a mid-stage study did not meet primary or secondary endpoints, so to lose its other frontrunner for a commercial approval would set the company back significantly, and perhaps fatally.

As such, I would expect management to continue to move forward with Seralutinib - so long as the FDA agrees to a pivotal trial - whilst emphasizing the positives to come out of the TORREY study, and perhaps using the follow-up data from weeks 24-28 - to try to find more positives that could potentially drive some share price upside.

The company needs a catalyst to try to drive the share price so it can raise cash on more favorable terms - perhaps it could come from one of its other candidates, or even interim data from a Phase 3 Seralutinib study - so as not to dilute investors too much.

If management can do that, by designing and executing a more favorable trial design, the outlook for Gosaamer and its share price may be more positive than last week's mass selloff suggests.

Conclusion - Backing Gossamer Today Is A High Risk Play Probably Best Avoided Despite The Tempting Upside In Play

In my experience following biotech stocks, it is generally rare for a company to come back strongly from a trial setback like the one experienced by Gossamer with Seralutinib.

Management may feel that it has been unlucky, however (and, objectively speaking, it is hard not to share that sentiment), and feel that it can substantially improve 6MWD and PVR in a pivotal trial by utilizing better patient selection and swapping the endpoints around. There seems to be enough evidence to support such a conclusion.

On the other hand, I am not sure the FDA will see things that way. They may discourage Gossamer from conducting a Phase 3. Despite its differentiated MoA, with so many other candidates in contention at the Phase 2 study stage or later, does the PAH treatment space truly need Seralutinib?

Counting further against the drug is the historically poor safety record of TKIs - the safety findings in TORREY may have been adequate in TORREY, but the drug class seems to be quite strongly associated with AEs.

Funding is another issue, as discussed above, made worse by the share selloff - Gossamer has traditionally been a heavily shorted stock.

Management will doubtless look at the risk reward and probably conclude that Seralutinib remains its best shot at approval by far, and that offers investors the prospect of an eventual trial success. Should that happen sometime in 2024, I believe the commercial case for an alternative to Merck's Sotarcept can be made, with triple-digit-million sales a distinct possibility.

That would certainly mean that anybody investing in Gossamer at $2 per share would likely double or triple their investment in the event of a positive readout, but will Gossamer even make it that far, let alone show data strong enough for approval?

My advice would be to stay on the Gossamer Bio, Inc. sidelines for the time being - perhaps the TORREY follow-up data will spring a surprise and open up a less risky investment opportunity at a marginally higher price.

For further details see:

Gossamer Bio: Buying The Savage Dip After A Trial 'Win' May Be Unwise