UBER - Grab Holdings: The Super App With Untapped Potential For Long-Term Growth

Summary

- Grab's super app strategy and early lead in key markets make it a dominant player in the Southeast Asian tech ecosystem.

- The company's focus on profitable verticals like food delivery and ride-hailing, coupled with the potential of its fintech platform, makes it an attractive investment opportunity.

- Grab's strong management team, strategic partnerships, and significant cash reserves provide a solid foundation for growth.

Executive Summary

Grab Holdings ( GRAB ), Southeast Asia's leading super app, is an attractive investment opportunity with multi-bagger potential. Grab has already established itself as the leader in its core markets of ride-hailing and food delivery, and is expanding into new areas such as digital payments and financial services. With over 70 million MSMEs in Southeast Asia that are underserved by digital technologies, Grab has a significant growth opportunity to capture this market (Source: Grab Form F-1 ). Moreover, Grab's strong unit economics, market-leading positions, and a high potential for profitability make it an attractive business model at scale.

Company Overview

Grab Holdings, originally known as MyTeksi, is a ride-hailing and delivery services platform that was founded in 2012 in Malaysia by Anthony Tan and Tan Hooi Ling. The two entrepreneurs met while studying at Harvard Business School and bonded over their shared experiences of growing up in Southeast Asia. They recognized a gap in the transportation industry in the region and set out to create a platform that would connect passengers with reliable and affordable rides. Since its founding, Grab has expanded its offerings to include food and package delivery, digital payments, and financial services with a broad reach that spans over 400 cities in 8 Southeast Asian countries, including Cambodia, Indonesia, Malaysia, Myanmar, the Philippines, Singapore, Thailand, and Vietnam.

Through its single "everyday everything" super app, the company has formed partnerships with over 25 million consumers, more than 2 million merchants, and over 5 million driver partners (Source: Grab Form F-1 ). The app allows users to order food, groceries, or packages, hail a ride or taxi, make online payments, and access a variety of services, including lending, insurance, wealth management, and telemedicine.

The company reports results from four major segments.

Mobility

The mobility segment refers to the service of providing transportation solutions to individuals, typically through the use of vehicles such as cars, taxis, and motorcycles. In the context of Grab Holdings, the mobility segment includes ride-hailing services such as GrabCar (car and taxi rides), GrabBike (motorcycle rides), and GrabShare (shared rides). The company's super app allows users to book and pay for rides, and matches them with available drivers or riders. The mobility segment is a key part of Grab's business and has helped to transform transportation in Southeast Asia, providing convenient and affordable options for millions of people. Grab holds a dominant position in the mobility market across Southeast Asia, with the exception of Indonesia, where it shares the market with Gojek in roughly equal measure.

Delivery

The delivery segment, also known as the on-demand delivery or last-mile delivery segment, refers to the service of transporting goods or packages from one location to another, typically from a retailer or merchant to a consumer. In the context of Grab Holdings, the delivery segment includes the delivery of food, groceries, and other goods, as well as package delivery services. Grab's delivery segment allows customers to place orders through its super app and have the items delivered to their doorstep by a Grab driver or delivery partner. This segment has become increasingly important in the e-commerce era, as more consumers are shopping online and demand for home delivery services has surged.

Grab is the leading player in all markets within this segment, except for Vietnam where it is a close second. The company has generally been gaining market share across these markets. However, it is worth noting that ShopeeFood, a newer entrant into the regional oligopolies, poses a potential disruption to the market equilibrium. Sea's strong historical execution and super app ecosystem make it an important player to monitor.

Financial Services

The fintech and digital banking segment of Grab's business encompasses several revenue streams, including payments, insurance/investment referrals, remittances, and buy-now-pay-later services. The company primarily generates revenue from digital payment processing fees charged to its merchant partners based on the total payment volume processed through the Grab platform. It is estimated that the payment volume is split 60/40 between on-platform and off-platform, with off-platform expected to grow 1.5-2x faster over time (Source: Grab Annual Report ). Fintech also includes revenue from effective interest earned on loans and advances provided to merchant partners, driver partners, and consumers, as well as fees for wealth management and insurance distributions. Grab is also setting up digital banks in Singapore and Malaysia, which is expected to further increase user retention and engagement. Despite being in the early stages of fintech/digital payments, there is still ample market opportunity, and super apps like Grab have structural advantages in customer acquisition, retention, and engagement.

Enterprise and Other

The non-core businesses and new initiatives of Grab fall under this segment, with the largest revenue drivers being advertising and anti-fraud services for financial institution partners, as well as on-demand delivery relationships. GrabAds, which was utilized by 46% of the company's merchant partners in 2020, is particularly profitable due to its high-margin revenue stream, estimated to be around 90% gross margin.

Opportunity To Digitize Financial Products

The large unbanked and underserved population in SE Asia presents a significant opportunity for Grab's financial services segment. The demand for digital financial services is high in the region due to the limited access to traditional banking services and cash being the primary mode of payment. As a result, Grab's digital financial services can overcome some of the structural challenges faced by traditional financial institutions, such as the relative lack of physical infrastructure outside major cities and the limited availability of public registers and reliable credit information.

Moreover, over 40% of the population over 15 years old in SE Asia is unbanked, and around 39% of the banked population is underserved, with limited access to credit cards, checking or savings accounts. This presents a significant opportunity for Grab's financial services to serve this untapped market and gain market share. Additionally, Grab's focus on expanding access to financial services through its super app ecosystem can help drive customer acquisition, retention, and engagement, further enhancing its growth potential in the region.

Another tailwind for Grab is the highly fragmented and largely offline informal MSME economy in SE Asia. The local economies in the region are largely driven by informal businesses, with MSMEs accounting for over 99% of all businesses and driving over 35% of the region's GDP, according to the company. However, less than 20% of these businesses use digital technologies to improve their productivity or expand their business, and many still lack a significant digital presence. As technology-enabled marketplace models like Grab expand their reach, these underserved MSMEs have an opportunity to expand their consumer reach beyond their limited storefront presences. In addition, these businesses have a need for financial services such as lending, which presents an opportunity for Grab's fintech and digital banking initiatives.

Who Will Be the Winner in Southeast Asia?

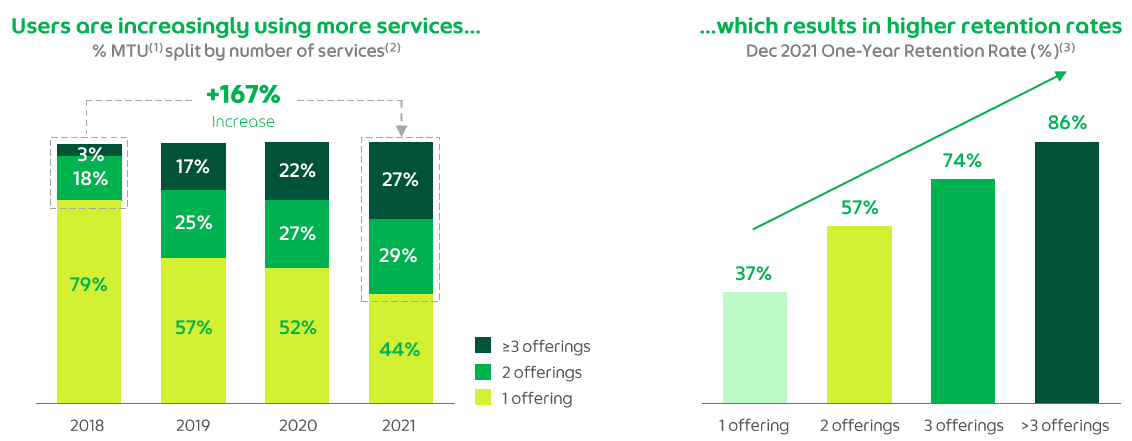

While the ultimate question of which super app will reign supreme remains, If Grab can maintain its position as the market leader in its core categories of ride-hailing and online food delivery, shareholders should do well. While its position in digital payments is more uncertain despite its early lead, the potential for multiple winners in the space, along with the disruption of traditional players, means that there is still ample room for Grab to succeed. With a strong foothold in both mobility and delivery, Grab has achieved something that has eluded its global peers, setting itself up for higher lifetime value, lower customer acquisition costs, and better retention rates. Early customer data suggests that the company's super app strategy is resonating with users, making its success in both mobility and delivery a strong possibility. This was demonstrated in Grab's 4Q21 earnings presentation.

Company slide (Grab Investor Presentation)

{kind=link}

Unit Economics

In my view, Grab has the highest potential for margin among all global businesses in the mobility and food delivery space. While the company has not provided financial guidance for its evolving financial services segment, management has set long-term margin targets of 12% in mobility and 3% in deliveries. These targets compare favorably to Uber's 10%+ mobility margin, but are lower than its global delivery competitors such as Delivery Hero and Uber Eats (5-8% margin). Grab plans to achieve segment EBITDA breakeven in deliveries by the end of 2023, although this may change depending on competition and investment opportunities.

The key driver of Grab's superior profitability profile is the success of its super app strategy compared to its competitors' pure-play approach. Grab's ability to combine mobility, food delivery, and digital payments/fintech services platforms is unique in the global market. This combination creates opportunities for higher customer lifetime value through wallet share and cross-selling, higher incremental margins, low customer acquisition costs, stronger retention and user stickiness, and more. These benefits also extend to merchants and drivers, who can benefit from the increased utilization rates resulting from the cross-platform nature of the super app. Additionally, financial services like wealth management, insurance, and lending offer further potential for monetization with little customer acquisition costs, and Grab is well-positioned to score credit risk and serve the underbanked segment in Southeast Asia.

These opportunities for incremental economics do not exist for Grab's global competitors, further contributing to its superior unit economics.

Valuation

Valuation Table (MontrealValue)

Overall, while Grab's valuation is higher than that of Sea Group and Uber, it's important to consider the potential upside in Grab's business model, particularly in financial services and the underserved MSME economy. Grab's focus on profitability and steady-state margins may make it a more attractive investment business model than its peers and earn 3x more gross profits per customer than "pureplay" businesses. Additionally, the company is outgrowing both Uber and SE - with mouth-watering revenue growth of 96% over the last twelve months. As a result of the faster pace of growth, and stronger potential unit economics, it is reasonable for Grab to command a larger multiple than its peers.

Overall, Grab's current share price offers significant upside potential with limited downside risk. Importantly, the company has a strong balance sheet with over $6 billion in net cash, which represents more than 60% of its market capitalization.

Risks

While Grab's growth prospects are promising, it is important to consider the potential risks associated with investing in the company. First, Grab operates in highly competitive markets with a number of strong players, which could limit its ability to maintain market share and profitability. Additionally, the regulatory environment in Southeast Asia can be uncertain and unpredictable, which could impact Grab's operations and financial performance.

Furthermore, Grab's expansion into financial services and digital payments carries its own set of risks, including regulatory compliance, cybersecurity threats, and potential fraud or misuse of customer data. Finally, while Grab has a significant cash position, its capital needs may increase as it continues to pursue growth opportunities, which could lead to dilution for existing shareholders.

Investors considering Grab should carefully weigh these risks alongside the potential upside and growth prospects of the company.

For further details see:

Grab Holdings: The Super App With Untapped Potential For Long-Term Growth