CA - Gran Tierra Energy: E&P Play Offers Attractive Valuation And Exploration Upside

2023-11-02 16:59:47 ET

Summary

- Gran Tierra Energy is an independent energy firm focused on South America, with quality assets trading at a low valuation.

- The business offers good visibility and can sustain its exploration programs and support future growth.

- GTE trades at a significant discount to NAV, and at nearly 1x EV/EBITDA 2025e.

We present our note on Gran Tierra Energy (GTE), a Canadian independent energy firm, focused on South America, with a Buy rating. We are drawn by the attractive valuation, hefty discount to net asset value, top-tier assets, growth pathway, and exploration upside. We will provide a brief description of the firm and its activities, analyze core assets and the business plan, discuss key value drivers, and value Gran Tierra’s shares.

An overview of Gran Tierra

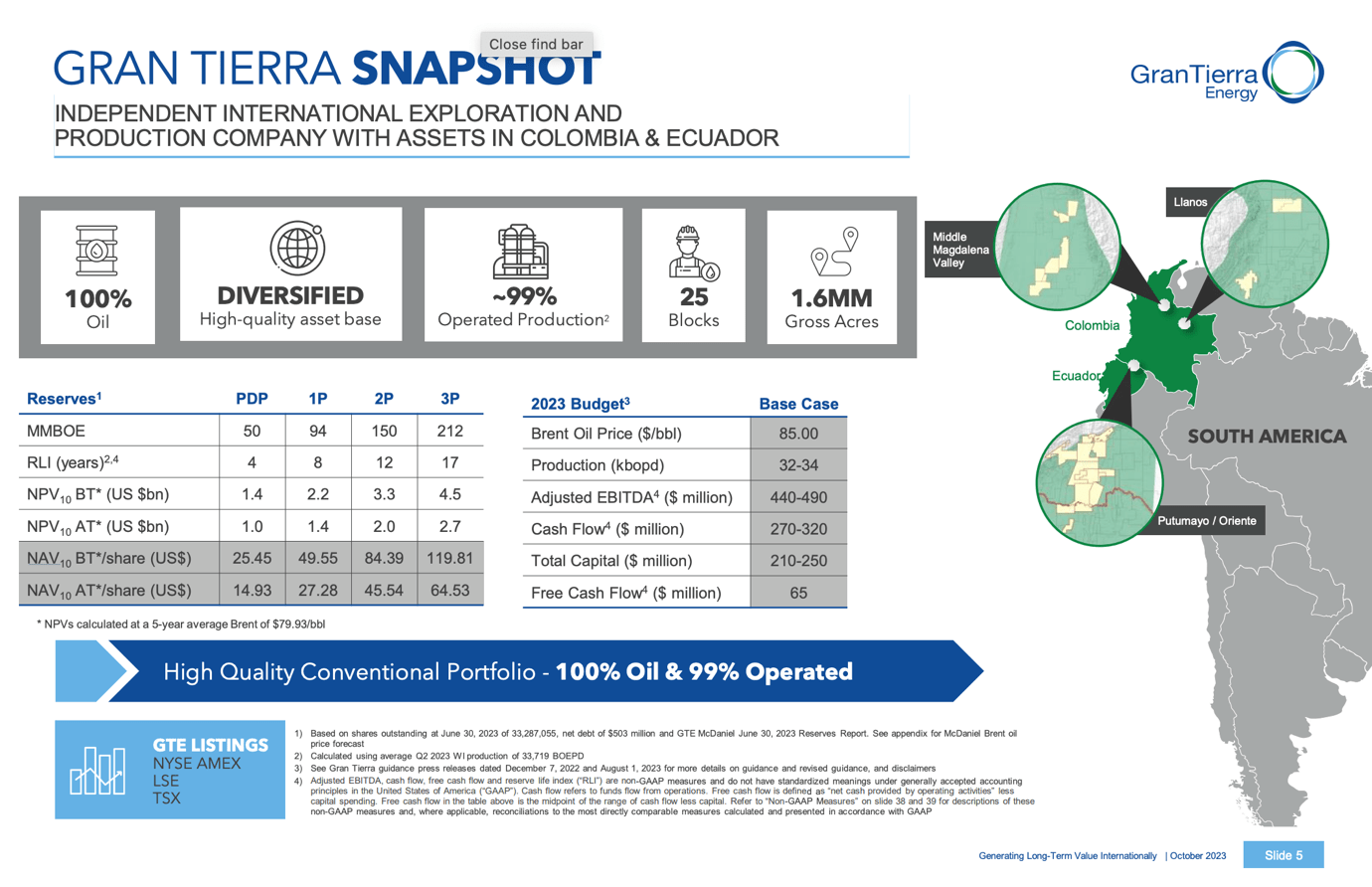

Gran Tierra Energy is an independent oil & gas exploration and production company, with assets in Colombia – representing ca. 99% of the firm’s production – and Ecuador. Reserves and production are primarily located in the Middle Magdalena Valley (including the Acordionero field) and the Putumayo basin (including the Chaza block and Suroriente block). The company has a strong track record of material production and reserves growth and operates a high-quality portfolio of oil assets at different stages of maturity spanning 25 blocks across 1.6 million acres with 94MMboe of proven reserves and a daily production of ca. 33kboe. Gran Tierra has a smaller operation in Ecuador. The company is listed on the NYSE, London Stock Exchange, and Toronto Stock Exchange and has a current market capitalization of $200 million.

Gran Tierra's Investor Presentation

{kind=link}

A high-quality asset base and ambitious targets

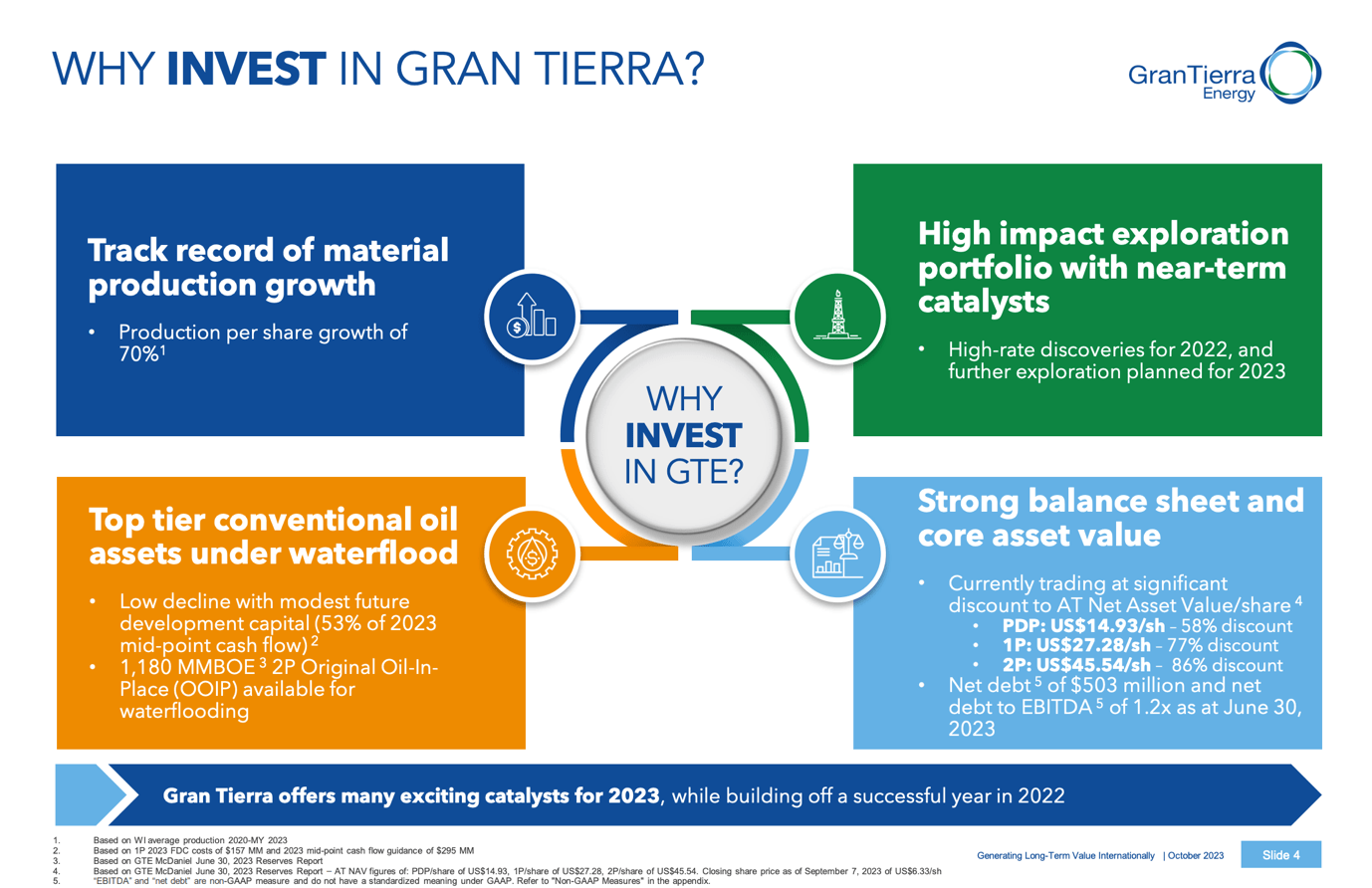

Gran Tierra owns top-tier conventional oil assets with a low decline ratio requiring modest development capital. The basins are underexplored, and exploration programs are focused on large prospect inventories. GTE’s diverse portfolio of production and exploration at various stages allows for significant exploration upside and high production growth. GTE offers good visibility on reserve and production growth. The full exposure to spot prices (due to a lack of hedges) allows GTE to fully reap the benefits of the present environment and the firm is set to benefit from the current oil tailwinds resulting in significant cash generation and deleveraging of the balance of sheet as well as capital returns to shareholders. Presently, the company can fund itself from operating cash flow and can sustain multi-year exploration programs leading to significant value creation.

GTE is particularly focused on asset optimizations through the improvement of recovery factors and cost management. This is reflected in operational performance and enhanced project economics. Moreover, there is access to established infrastructure including large spare capacity in pipelines, trucks, and barges leading to stronger pricing, short cycles, and speedy access to global markets.

Q3 results

Gran Tierra reported solid Q3 results in line with expectations. Production was robust at 33.9kboe / day and confirms guidance and our forecasts. This, combined with a capex reduction, resulted in a free cash flow of $36 million, further strengthening the net financial position of GTE. Management announced that the next phase of development drilling at Acordionero and Costayaco will commence in December and likely finish in Q1 next year. Moreover, the bond exchange was completed thus reducing leverage and GTE announced a 10% share buyback, effective 3 rd of November. Overall results came in strong and confirm our constructive outlook.

Valuation and investment case

Similar to other names in the sector, we value Gran Tierra Energy using forward EV/EBITDA multiples, NAV analysis, and FCF yields.

In line with sell-side analyst consensus, we forecast $900 million of net sales and $550 million of EBITDA in the next fiscal year.

The current equity value implies a forward EV/EBITDA ratio of just 1.4x and an EV/EBITDA 2025e of around 1x. The multiples are too punitive and fail to reflect the production longevity and growth, and upside from exploration.

Moreover, we apply FCF yields as a sanity check. We forecast $150 million of adjusted Free Cash Flow in FY2024e, implying a 20% FCF/EV yield or a ca. 75% FCF/Market Cap. yield. Given the characteristics of the portfolio, we find the yield too high, and the valuation too low. More importantly, we consider the NAV as disclosed in the investor presentation. At a 10% discount rate, the PDP (proven, developed, producing) NAV stands at $1 billion, implying a P/NAV of 0.2x. At a 10% discount rate, the 1P (proven reserves) NAV stands at $1.4 billion (assuming oil prices remain at the average of the last 5 years). This implies a price-to-NAV ratio of 0.15x. The 2P (proven and probable reserves NAV) stands at $2 billion, implying an excessively low P/NAV ratio.

GTE’s E&P peers in Latin America trade at significantly higher EV/EBITDA multiples and lower discounts to NAV. We believe that Gran Tierra should eventually trade closer to peers given the visibility and duration, production growth, reinvestment opportunities, and ability to self-fund. The current valuation fails to reflect any of these.

Gran Tierra's Investor Presentation

{kind=link}

We value GTE at an exit multiple of 2.5x 2025e EBITDA and discount back to the present using a 12% discount rate. We obtain an EV of $1.25 billion, or a discounted EV of $1 billion today, and an equity value of $450 million implying more than 100% upside today or a share price of close to $14. We can look at GTE’s valuation from different angles and utilize different methodologies but it’s evident to us that the shares are excessively cheap and should rerate as the company executes, deleverages, and delivers capital returns.

We believe Gran Tierra is attractively priced and has a compelling risk/reward.

Risks

Downside risks include but are not limited to weaker macroeconomic conditions, lower than expected oil and gas prices resulting in lower sales and earnings, political instability in Colombia (especially given the current left-wing government) and Ecuador, unfavorable legal and regulatory changes, lower than expected exploration upside, higher than expected capital expenditure leading to lower returns on investment, delays in exploration and production, operational underperformance, higher than expected operational costs, foreign exchange risk, misallocation of capital to low IRR projects or acquisitions given the decline in leverage and potential for M&A, climate change risk, accidents, and weather events.

Conclusion

We find GTE’s investment case compelling, and we recommend building a long position on Gran Tierra Energy shares.

For further details see:

Gran Tierra Energy: E&P Play Offers Attractive Valuation And Exploration Upside