CA - Gran Tierra Energy Remains A Buy As More Positive Catalysts Emerge

2023-04-17 23:20:17 ET

Summary

- Oil price rally points to more upside ahead for Gran Tierra.

- Recent operational results indicate the company is on-track to deliver 2023 production targets.

- Heightened geopolitical risk in Colombia remains a threat but its impact on Gran Tierra is overblown.

After being priced for bankruptcy during the 2020 pandemic and then buffeted by a range of geopolitical and regulatory risks, small-cap intermediate oil producer Gran Tierra Energy (GTE)(GTE:CA) has finally started unlocking value for investors. Despite the positive turn of events the driller has still lost a whopping 46% of its market value over the last year and only gained a modest 4.7% since my February 7, 2023 article . That sharp decline in value over the last year occurred despite Gran Tierra reporting record 2022, funds flow from operations, free cash flow and net income. Recent events show more positive catalysts are emerging indicating that GTE stock remains heavily undervalued, creating an opportunity for risk-tolerant investors.

Latest developments

Gran Tierra reported strong 2022 results toward the end of February 2023. That impressive performance included record funds flow from operations which grew by a whopping 96% year over year to $366 million. Annual 2022 net income also soared to a record $139 million which was an incredible 3.3 times higher than the 42.5 million reported for 2021. Then there was the 253.5% year-over-year spike in free cash flow to a record $129.4 million. EBITDA also experienced robust growth rising by 117% compared to 2021 to be $471.7 million. Gran Tierra also reported a solid operating netback of $48.43 per barrel of crude oil sold, which was 43.5% higher than a year earlier.

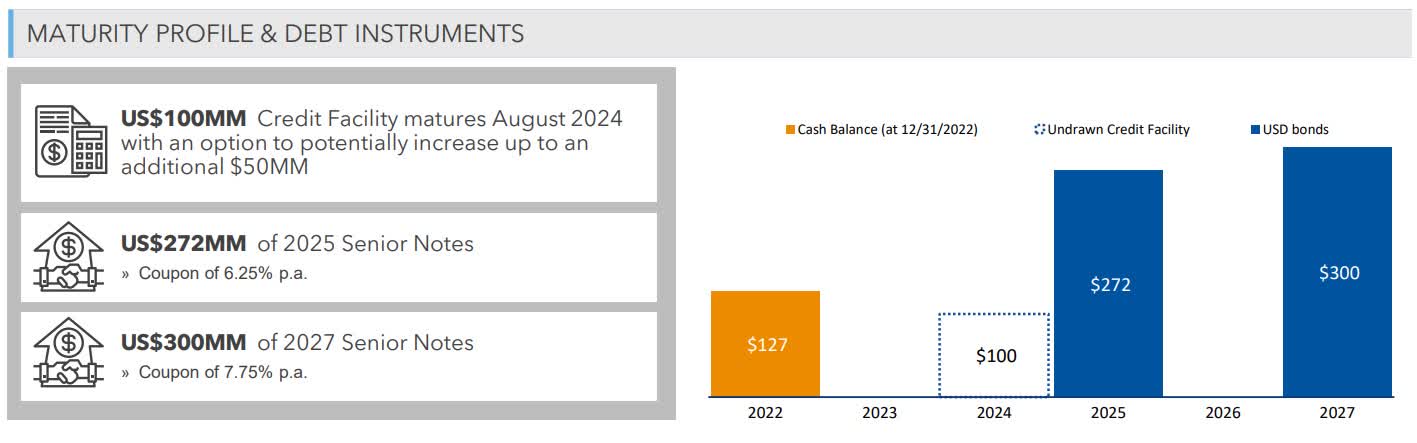

As a result of those strong numbers Gran Tierra’s financial position improved. Cash and cash equivalents soared nearly fivefold to $126.9 million while net debt at the end of the fourth quarter 2022 was 40% lower than it had been at the end of the second quarter 2021. That stronger balance sheet has gone a long way to mitigating much of the earlier risk associated with investing in Gran Tierra when it was struggling with bloated debt and sharply lower oil prices as it emerged from the pandemic. This is further aided by a well-laddered debt profile with the first major debt repayment totaling $272 million falling due during 2025 and then another $300 million in 2027.

{kind=link}

Gran Tierra’s notable 2022 performance can be attributed to the significant spike in global oil prices that occurred after Vladimir Putin’s invasion of Ukraine and Washington along with its allies restricting Russia’s energy exports. Despite those strong numbers and record results Gran Tierra’s market value declined sharply since April 2022, losing 48% over that one-year period.

As discussed in my February 7, 2023, article, Gran Tierra experienced solid reserves growth during 2022 which saw the after-tax net present value or NPV for short of its 1P and 2P reserves grow leading to a higher 1P and 2P net asset value or NAV for short. In that article, I determined that Gran Tierra had an after-tax 1P NAV of $2.53 per share or 2.8 times greater than its market value at the time of writing and a 2P NAV per share of $3.99 which is 4.3 times higher than the current share price. Those numbers indicate that there is considerable upside ahead and a solid margin of safety for investors.

Recent positive catalysts

Latest developments, concerning Gran Tierra’s operations and performance point to the company continuing to strengthen its position. The driller’s April 2023 operational update demonstrated that first quarter 2023 production had risen 8% year over year to 31,700 barrels daily. This was driven by the Acordionero oilfield, a core asset holding 44% of Gran Tierra’s 2P reserves and the driller’s primary producing field, pumping 20,000 barrels per day during the quarter for the first time since the second quarter of 2019.

During the period Gran Tierra drilled 14 wells including six production wells and four water injection wells with a remaining four production wells spudded and to be completed during the second quarter 2023. Those numbers bode well for Gran Tierra to continue growing production during 2023 thereby increasing the likelihood of the driller achieving the targeted average annual production of 32,000 to 34,000 barrels per day.

Gran Tierra also continued with its share buyback during the first quarter 2023 acquiring 13 million shares during the period. This means that the driller’s share count has been reduced from 346,151,157 outstanding shares to 333,151,157 shares. Gran Tierra’s management also repurchased $8 million from the company’s 2025 notes reducing its debt burden. A lower share count coupled with reduced long-term debt means the value of Gran Tierra’s after-tax net asset value per share or NAV is climbing.

Using the same methodology applied in my February 7, 2023, update on Gran Tierra where the after-tax net present value, or NPV, of the company’s 2022 reserves was used, I have recalculated the 1P and 2P NAVs per share to reflect current numbers.

This includes:

- a lower count of 333,151,157 outstanding shares;

- reduced long-term debt of $581,593,000; and

- cash and cash equivalents of $126.9 million as per Gran Tierra’s December 2022 results.

This, as per the chart below gives Gran Tierra an after-tax 1P NAV of $2.54 per share leaving value only $0.01 higher than the $2.53 per share calculated for the February 7, 2023, update.

Calculations Table (Gran Tierra and Author's own work)

Gran Tierra’s indicative fair value rises to $3.74 per share, as the chart below shows, when calculating its after-tax 2P NAV per share, although that is 6% lower than the $3.99 calculated in my earlier article.

Calculations Table (Gran Tierra and Author's own work)

The 2P after-tax NAV per share is essentially the industry accepted standard for determining an intermediate oil producers indicative fair value. On this basis, Gran Tierra certainly appears heavily undervalued after considering the driller’s after-tax 2P NAV per share is four times greater than its market value. This also indicates that there is a considerable margin of safety for investors.

The sharpy discount of Gran Tierra’s market price compared to its after-tax 2P NAV per share can be blamed on an overblown perception of risk relating to its operations in Colombia. The Andean country’s first ever leftist president Gustavo Petro plans to end contracting for hydrocarbon exploration although he has committed to honoring all existing contracts.

Another positive development for Gran Tierra was the company’s ability to successfully renegotiate with Colombia’s national oil company Ecopetrol ( EC ) the duration and terms of the contract for the Suroriente Block in Putumayo Department. Gran Tierra, which is the operator, owns a 52% interest in the Suroriente Block. The block holds 2P reserves of 2 million barrels and pumped an average of 8,167 barrels per day, of which 4,247 barrels are attributable to Gran Tierra, during the first quarter 2023 the highest output since 2015.

Gran Tierra successfully extended the duration of the contract for Suroriente by 20 years from the effective date of the contract with an agreement to invest $123 million over a three-year period also from that date. The effective date of the contract has yet to be determined because the deal requires regulatory approval from Colombia’s Superintendence of Industry and Commerce. While regulatory approval has yet to be received the agreement with Ecopetrol provides greater clarity around the future of the Suroriente Block and strengthens Gran Tierra’s position in the Putumayo Basin, Colombia’s second most important oil basin.

Conclusion

The latest news regarding Gran Tierra’s operations coupled with solid full year 2022 results points to the company’s strengthening position and improving ability to unlock value for investors from its existing assets. This is particularly important to note when it is considered that the ongoing share buyback and focus on reducing debt has resulted in Gran Tierra’s after-tax 2P NAV rising to $3.74 per share. That is four times greater than Gran Tierra’s market price at the time of writing indicating that not only is the company heavily undervalued and offering considerable upside for investors but that there is a considerable margin of safety. These positive developments coupled with the surge in oil prices after the surprise OPEC Plus production bode well for further price appreciation for Gran Tierra’s shares.

For further details see:

Gran Tierra Energy Remains A Buy As More Positive Catalysts Emerge