CA - Granite REIT: Solid Performance But Still Not Our First Choice

2023-06-06 10:00:00 ET

Summary

- Granite REIT has delivered solid returns over the years, while diversifying away from Magna.

- Leverage has crept a bit and the REIT has more risks as we likely head into a recession.

- We tell you what we like more.

All values are in CAD unless noted otherwise.

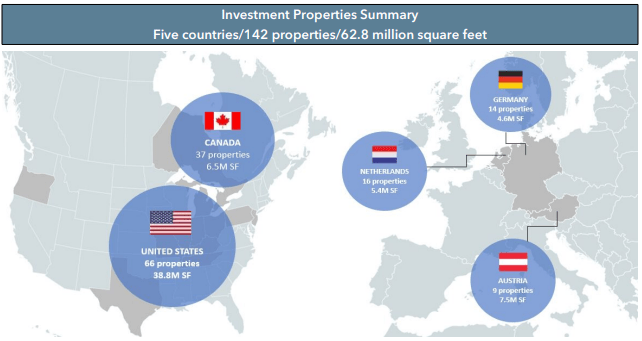

Based in Canada, Granite Real Estate Investment Trust ( GRP.U ) ( GRT.UN:CA ) owns and manages properties, spanning over 62 million square feet in North America and Europe.

{kind=link}

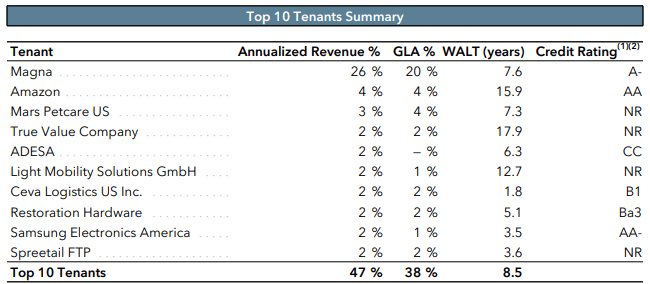

Of the 142 properties, 133 are income producing and the balance are a combo of properties and land under development. The income producing properties are for industrial in nature and serve as logistics, distribution warehouses, and manufacturing properties. Magna International Inc. ( MGA ) is the source of 26% of the REIT's revenue and consequently its largest tenant.

{kind=link}

While this is a lot of dependence on a single tenant, keep in mind that when the REIT began operations in 2012, MGA occupied 93% of its gross leasable area or GLA. Although there has been no change to the GLA or revenue concentration since 2022, Granite has done a great job in reducing this dependence since its inception. What does not hurt is that this tenant is bestowed with an A rated, investment grade rating by the credit agencies of S&P, Moody's and DBRS.

Prior Coverage

We have always been impressed by the management in our previous coverage, staying out most of the times only because it was too expensive for our taste. The last time around , in November 2022, it was trading at a discount to its NAV. As evident below, that did not happen very often.

We still chose to remain on the sidelines due to the amazing bargains at the time and the comparatively lower yield from this REIT. The discount to its book value has closed since then and the dividend yield is slightly higher. Granite has also kept its investors afloat during this time.

Seeking Alpha

Let's dig into the recent results to get granular on Granite.

Q1-2023

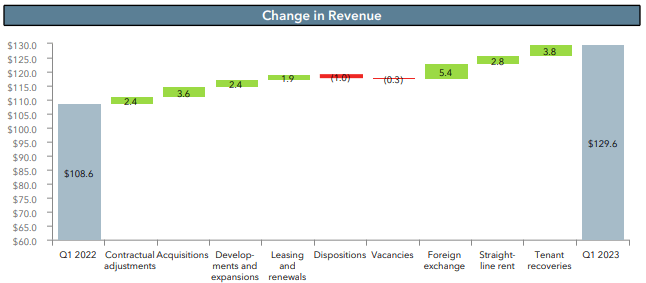

While contractual rent escalators, 2022 acquisitions, development completions, accretive leasing and renewals, and tenant recoveries, all had a hand to play in higher year over year revenue, the star of the show was foreign exchange.

{kind=link}

With bulk of its properties outside of Canada, Granite benefited from the strong Euro and US Dollar. The higher revenue numbers flowed down resulting in Q1-2023 beating the comparative quarter numbers.

{kind=link}

What foreign exchange giveth, it also taketh (but to a smaller extent). We are talking about the interest expenses.

In comparison to the prior year, the euro was 2% stronger and U.S. dollar 7% stronger, resulting in a positive $0.06 impact to FFO per unit. Offsetting the favorable Q1 2023 NOI relative to Q4 is the effect of higher interest costs resulting from interest on Granite's secured construction facility, which commenced to being expensed in January 2023 upon the substantial completion of Granite's Houston development and foreign exchange on euro-denominated borrowings and current income tax.

Source: Q1-2023 Earnings Call Transcript

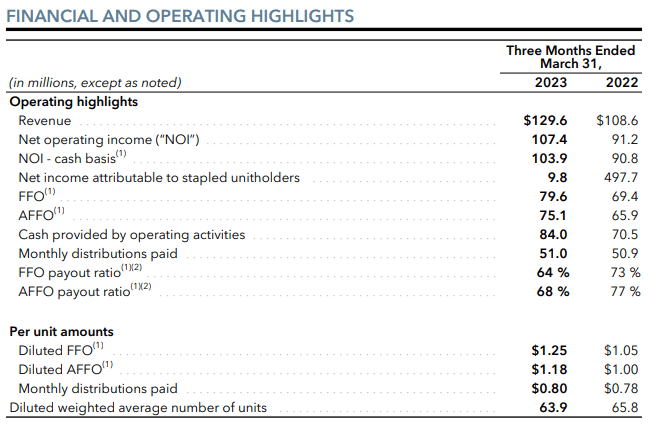

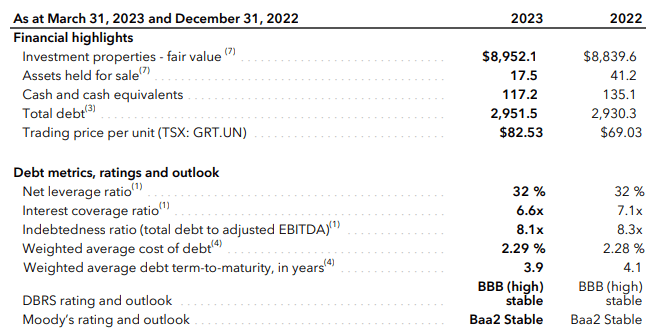

To put this increase into context, interest costs increased from $10.9 million to $17.8 million year over year. The weighted average interest rate increased from 1.59% at March 31, 2022 to 2.29% at March 31, 2023. When compared to the end of 2022, the increase in the average rate is not significant.

{kind=link}

The coverage has however taken a slight beating and a bigger one compared to the same quarter in 2022 when it used to be 7.6x. Management shed some light on their expectations of interest expense for the rest of the year during the earnings call.

On a run rate basis, we estimate interest expense will run approximately $18.5 million per quarter before factoring any new debt for additional credit facility draws other than that draw for the repayment of the construction mall.

When Granite refinances its upcoming $400 million debenture with during November this year, we expect our interest expense run rate will increase towards approximately $22 million per quarter.

Source: Q1-2023 Earnings Call Transcript

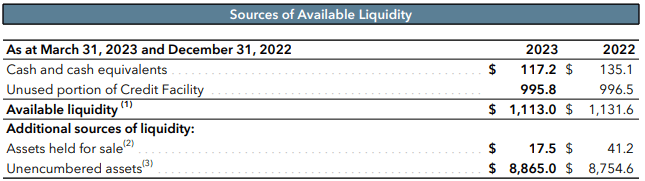

Granite has about $450 million of debt maturing in 2023,

Q1-2023 Financial Report

and more than enough liquidity for it not to pose an existential threat.

{kind=link}

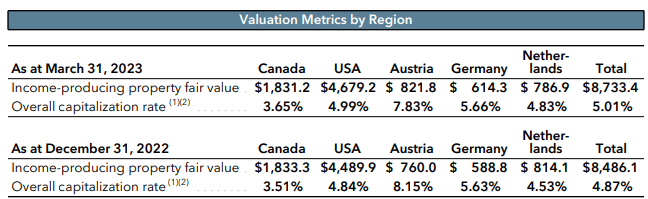

The REIT continues to slowly increase the capitalization rates of its properties, with Austria being an outlier, going the other way around.

{kind=link}

The REIT described its fair value changes as below.

The fair value losses on Granite's investment property portfolio were primarily attributable to the expansion in discount and terminal capitalization rates across all of Credit's markets in response to rising interest rates, partially offset by fair market rent increases across the GTA and selected U.S. and European markets, the renewals of three special purpose properties in Austria and Germany and the stabilization of three properties under development in Houston, Texas, which were completed and transferred to income-producing properties during the first quarter.

Source: Q1-2023 Financial Report

While these values are a bit more realistic, we are having a hard time digesting the 3.65% cap rates in Canada where GICs are yielding over 5%.

Outlook & Verdict

We expect a big slowdown in the industrial area. Supply is hitting at a brisk pace and we also think we are already in recession in the US. As such all new purchases should be conducted with an abundance of caution. Even if we decided to take the plunge, Granite would be our second choice.

Both on discount to tangible NAV and dividend yield (4% versus 5.8%), another industrial favorite of ours, Dream Industrial Real Estate Investment Trust (DREUF) (TSX: DIR.UN:CA ) comes out ahead.

Dream industrial is also trading 2 FFO multiples cheaper than Granite. We think both sets (for Dream Industrial and Granite) of cap rate assumptions, are on the optimistic side. As we go through the next 12 months, Dream Industrial has more mark to market upside on rents as it is placed within some of the hottest markets. Granite's properties are more specialized and it also has longer leases lengths. So it will have a slower jump in rents. Combining this information with the NAV discount gets us to heavily favorite Dream Industrial here. While we closed out our position in Dream Industrial after a great rally, we would look to buy this on the dip first.

Please note that this is not financial advice. It may seem like it, sound like it, but surprisingly, it is not. Investors are expected to do their own due diligence and consult with a professional who knows their objectives and constraints.

For further details see:

Granite REIT: Solid Performance But Still Not Our First Choice