CA - Great Panther Mining: A Bleak Future

- Great Panther Mining released its Q2 results last week, reporting quarterly production of ~16,600 ounces at all-in sustaining costs of $3,299/oz.

- The company noted that it made a transformational sale of its Mexican mines, but the transaction hardly improved the investment thesis, with GPL still owning marginal assets (1 vs. 3).

- Although production and costs will improve in the second half, Great Panther's balance remains weak and I don't see a path towards consistent sub $1,500/oz AISC in an inflationary environment.

- So, with significant share dilution likely on deck over the next 12 months to add to the mountain of share dilution we've already seen and limited cash flow generation, I see the stock as un-investable.

It's been a mixed Q2 Earnings Season for the Gold Juniors Index ( GDXJ ), but Great Panther ( GPL ) has at least remained consistent, boasting some of the worst cost margins sector-wide (Q2 2022: (-) 1,434/oz). The company noted that the sale of its Mexican assets was transformational, which I would argue is a huge overstatement, given that it only does a little to bandage up the weak balance sheet, and GPL goes from having three marginal assets (GMC, Topia, Tucano) to one. Given Great Panther's weak balance sheet, inferior margins, and single-asset status, I continue to see the stock as un-investable.

{kind=link}

Tucano Mine (Company Website)

I wrote on Great Panther just over five months ago, noting that its FY2022 guidance was disappointing with a sharp decline in production on deck and all-in sustaining costs [AISC] guided at $1,650/oz for the mid-point. However, the most disappointing part about this guidance is that this was preliminary guidance, and the company has a track record of missing by a wide margin. Six months later, we've seen a $600/oz increase in cost guidance at the mid-point, with costs now expected to come in at $2,250/oz and cash costs expected to come in at $1,450/oz. Combined with a weaker gold price, there's little surprise the stock has been halved since February.

{kind=link}

Great Panther - Revised Guidance (Company Filings)

Mexican Asset Sale

As Barrick's ( GOLD ) CEO, Mark Bristow, stated in his Q2 results , big inflation periods or global economic crises are always worse than they seem and take longer to come out of but can be survived with highly skilled workers, world-class assets, and diligence. Diligence and highly skilled workers go a long way. Still, it's high-quality assets that benefit from economies of scale that are able to protect against highly inflationary periods like we're in with persistent headwinds (labor tightness, supply chain headwinds).

For the Mexican asset sale ($8 million in cash, ~$8 million in shares, $1.5 million in deferred payments) to be transformational, it would have needed to give Great Panther a world-class asset or completely patch up the balance sheet. This is not the case. The reason is that the consideration paid for its Mexican assets offers only $8 million upfront (shares are subject to a 4-month, 8-month, 12-month hold period) vs. debt of ~$40 million, suggesting the seemingly never-ending share dilution is likely to continue.

Meanwhile, this deal does not add a world-class asset that Great Panther could certainly use to survive; it simply subtracts two assets that would probably be better off in care & maintenance anyways. Hence, the word transformational used in the press release is a stretch, given that it doesn't change Great Panther from being an un-investable company. This distinction is related to it being a single-asset producer in a Tier-2 jurisdiction (Brazil) with AISC margins below 25% at a conservative $1,750/oz gold price. Let's look at the Q2 results below:

Q2 Production

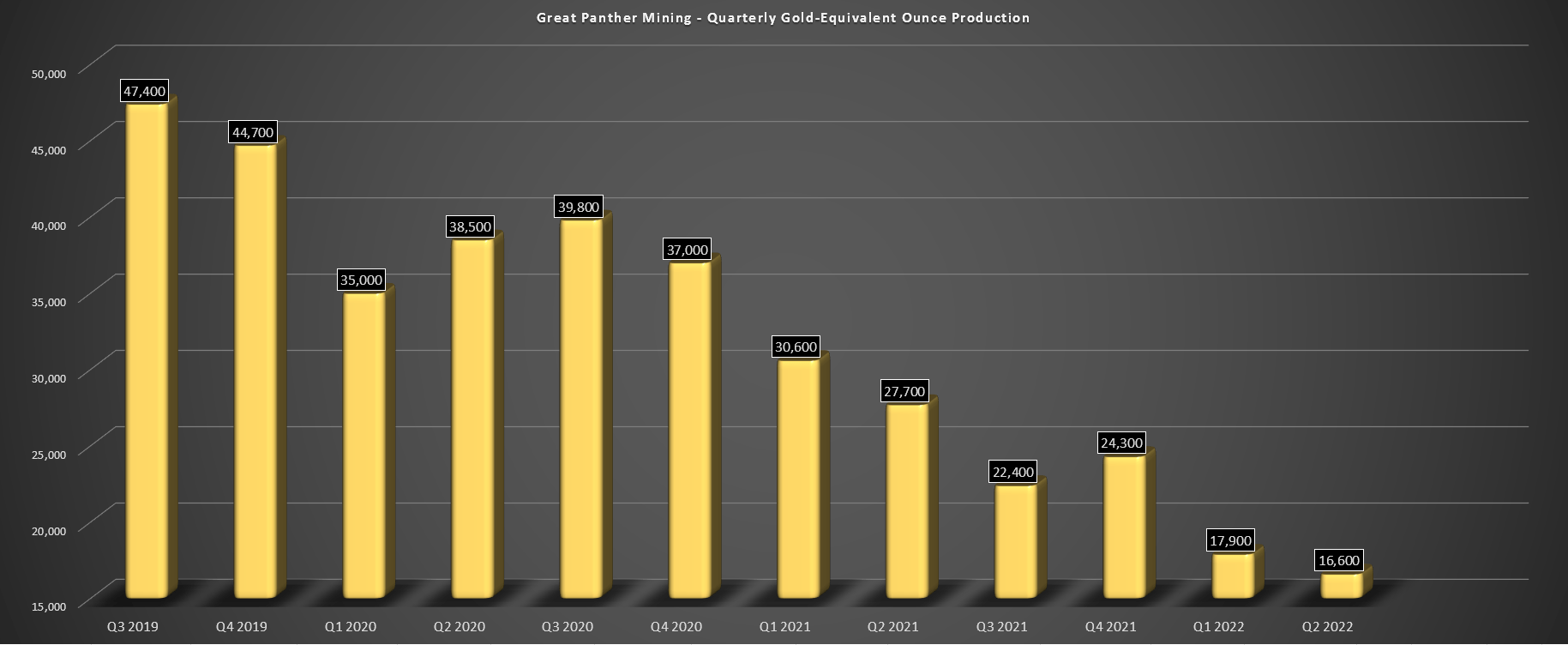

Great Panther reported its Q2 results last week, producing ~16,600 ounces of gold, a 20% decline from the year-ago period. This was related to a focus on waste stripping to prepare the TAP AB pit, resulting in much lower grades processed in the period (0.69 grams per tonne of gold vs. 0.81 grams per tonne of gold). The lower grades combined with the asset and GMC previously being placed in care & maintenance have continued a trend of sharply declining gold-equivalent ounce production, with output down 65% vs. Q3 2019 levels.

{kind=link}

Great Panther Quarterly Production (Company Filings, Author's Chart)

As it stands, Great Panther is tracking at less than 40% of its annual production guidance mid-point (85,000 to 100,000 ounces). Fortunately, it expects a much better H2 and continues progressing studies on an underground opportunity at Urucum North. While this is good news and certainly points to a meaningful sequential improvement in production and costs, I am less optimistic about the underground opportunity. The reason is that developing a new mine will be costly even if permitted, and Great Panther doesn't have the cash flow nor balance sheet to fund this internally.

So, while this might translate to a longer mine life and lower costs, Great Panther's production per share will continue to plummet, driven by its steady share dilution at 52-week lows. This is the only metric that investors should pay attention to, and in cases where production per share is declining, one is better off just owning the physical metal itself or the gold ETF ( GLD ). Therefore, for investors hoping to be bailed out by the underground opportunity, I think this potential is overshadowed by the dilution that will come with exploiting this if the company can't start generating free cash flow.

Costs & Margins

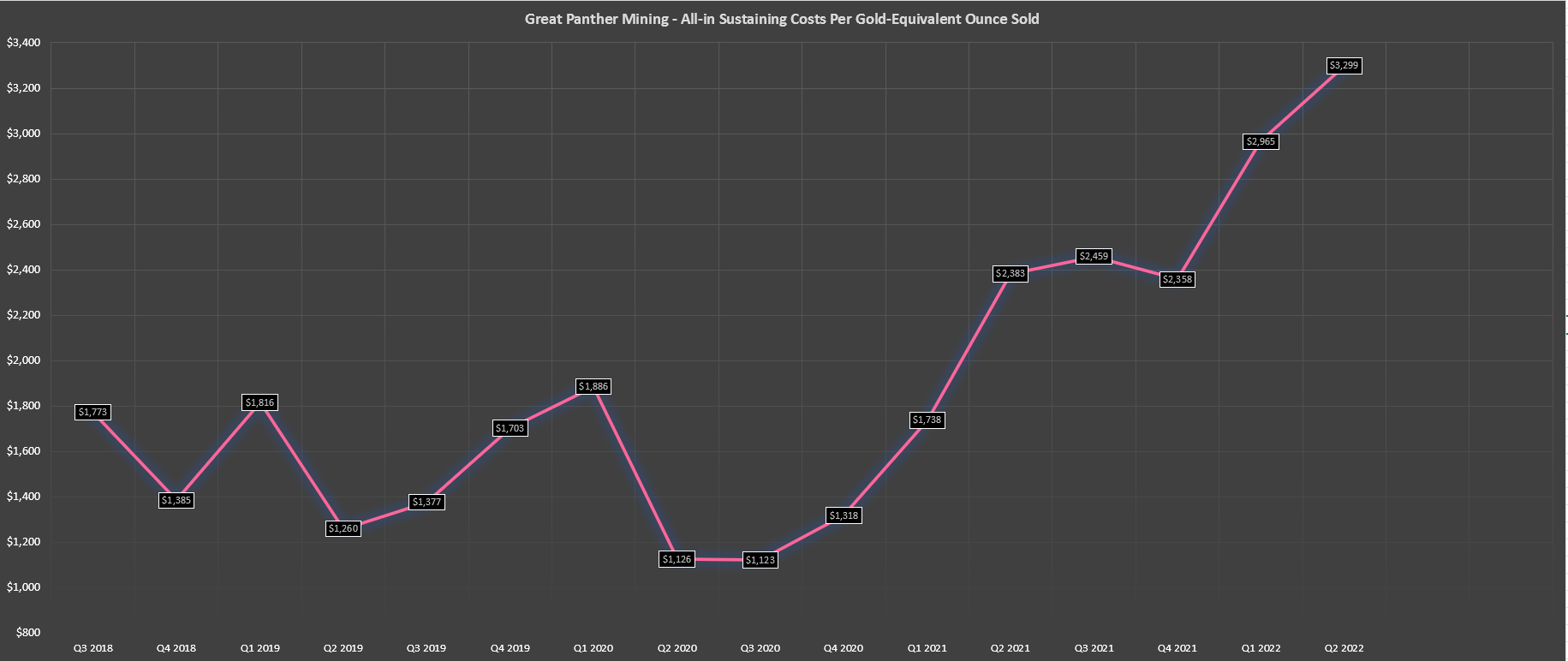

While the production results left a lot to be desired, with just 30,700 ounces of gold produced in H1 (down 30% year-over-year), the costs were even more disappointing. In fact, Great Panther's quarterly cost profile is beginning to look more like a chart of European gas prices than the cost profile for a gold producer. This is because all-in sustaining costs [AISC] have nearly tripled since Q3 2020 levels ($3,299/oz vs. $1,123/oz) and are sitting at ~$3,400/oz on an all-in cost basis when including exploration expenditures. The current cost profile doesn't inspire much confidence, with the gold price lower than Q2 2022 levels and Great Panther reporting an AISC margin of (-) $1,434/oz last quarter.

{kind=link}

Great Panther - All-in Sustaining Costs (Company Filings, Author's Chart)

The good news is that Great Panther incurred significant costs in H1 related to accelerated spending on the tailings facility (~$360/oz) and elevated stripping activity (~$450/oz). This means that the actual AISC adjusting for these temporary items is closer to $2,400/oz. When adjusting for a higher denominator (increased production), we could see all-in sustaining costs dip below $1,550/oz. That said, Great Panther has a history of bombing guidance, and inflationary pressures remain sticky. So, investors must be careful to assume that the company can meet its suggested guidance mid-point, which calls for an average quarterly production profile of ~31,000 ounces to finish the year.

The guided ~31,000-ounce quarterly average production profile is based on subtracting year-to-date production (~30,700 ounces) from the 92,500-ounce mid-point provided earlier this year and reiterated in the Q2 results.

Given the inflationary pressures experienced and true to form, Great Panther raised its FY2022 AISC guidance to $2,250/oz at the mid-point vs. $1,650/oz previously. This was partially related to accelerated spending to fast-track the Tucano TSF, but I don't think the company guided nearly conservative enough for inflationary pressures or the risk of strength in the Brazilian Real. So, while investors can look forward to more respectable costs in H2, AISC margins are still likely to come in at (-) $425/oz this year vs. an average realized gold price of $1,825/oz.

Valuation

Based on an estimated ~57 million fully diluted shares (year-end estimate vs. 50 million currently) and a share price of $1.10, Great Panther trades at a market cap of ~$63 million. This would appear to be a dirt-cheap valuation for a ~100,000-ounce producer, but only one has to look at the cost profile, the balance sheet, and the gold price to understand why the stock is valued at such a discount vs. its peer group. At conservative gold price assumptions ($1,700/oz), which should be used when assessing the viability of any ultra-high cost producer, I don't see any clear path to Great Panther generating any meaningful free cash flow.

The reason is that I am less optimistic that Tucano has a bright future than the company, and I would be shocked if this team keeps AISC below $1,500/oz. This is important because it's what's required to generate any meaningful free cash flow (~$1,600/oz all-in costs with exploration). Under my assumptions ($1,500/oz+ AISC), the company will likely continue diluting shareholders to clean up its balance sheet, with considerable debt even after selling its Mexican assets. Some investors might argue that the shares provided in the deal will help (~$8 million value), but they have an average hold period of ~ seven months, with none able to be sold within four months, and Great Panther in 2022, not next year.

{kind=link}

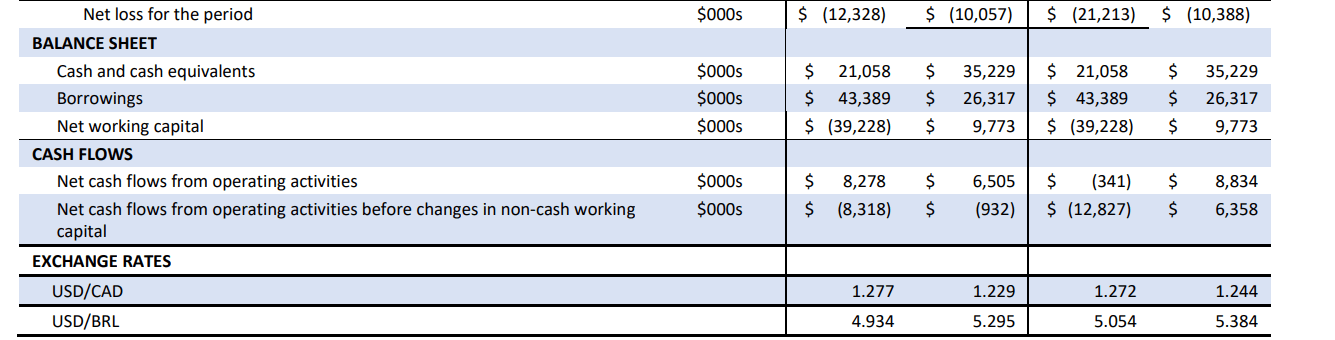

Great Panther Balance Sheet & Cash Flows (Company Filings)

Finally, we still haven't seen any resolution regarding the fine ($9 million) related to the accusations of cyanide pollution at Tucano. This is a significant figure given that it's more than Tucano will generate in a year in free cash flow at a $1,700/oz gold price if it's spending adequately on exploration. So, given the weak balance sheet and limited free cash flow generation (even when stripping is at lower levels), I think it would be naive to assume there won't be more share dilution here. In fact, the company states in its MD&A:

"The Company has determined that it will require further financing to meet long-term objectives, improve working capital, fund planned capital investments and exploration programs for its operating mines, and meet scheduled debt repayment obligations and will be considering additional equity financing (including through use of the ATM facility) and/or debt financing."

So, what would change my mind on Great Panther?

If the gold price were to increase above $2,150/oz, there might be an investment thesis here, given that the asset would look more viable long-term at this gold price ($600/oz+ AISC margins). In addition, if the company were to add another asset to shed its single-asset producer status, this would also help the investment thesis. Finally, if the company were able to exploit the underground opportunity by using free cash flow (not solely share dilution), which would require a higher gold price, this would offer a path towards lower operating costs and help the investment thesis. Assuming one or more of these things were to occur, it would be worth taking a closer look at considering a long position in the stock as a speculative idea.

Summary

As discussed for over a year now, Great Panther is the investment that keeps on taking. This shouldn't be a surprise when you've got a company that is diluting shareholders at a pace faster than 90% of its peers. While the carrot dangling on the stick is the underground opportunity, I don't see a clear path to developing this with the current balance sheet. Plus, the company could have an additional capex bill when it comes to its tailings facility in mid-2024 with more stringent regulatory guidance on existing tailings dams. Finally, an inability to defend the fine would accelerate share dilution, adding further uncertainty to the story.

{kind=link}

Permitting - Tailings (Company Filings)

To summarize, this is an extremely high-risk stock, and when several Tier-1 producers are on sale, it makes no sense to scrape the bottom of the barrel. So, while it might be tempting to buy Great Panther, buyers should be aware that some stocks on the sale rack stay there for a long time, especially when they're the proverbial runt of the litter (highest-cost producer sector-wide). Given these risks with little redeeming qualities, I think investors can do much better than GPL, with dozens of better opportunities elsewhere in the sector. Therefore, if GPL does rally sharply on improved sentiment, I would view this as a gift to exit one's position into strength.

For further details see:

Great Panther Mining: A Bleak Future