GRBK - Green Brick Partners Is A Very Attractively Valued Top-Rated Stock

2023-07-15 00:44:31 ET

Summary

- Green Brick Partners' stock is very highly graded stock by Seeking Alpha Quant, and my in-depth analysis suggests it is fair.

- The company's latest quarterly earnings exceeded consensus estimates, with a 15% YoY revenue growth and adjusted EPS expanding from $1.20 to $1.37.

- Despite a massive year-to-date rally, Green Brick's valuation remains attractive.

Investment thesis

Green Brick Partners (GRBK) stock has a very high Seeking Alpha Quant grade, which is why the stock grabbed my attention. After I dug down into the details, I can conclude that the stock is a "Buy". I think so because the company demonstrates solid financial performance with stable profitability metrics and steadily improving free cash flow. Most importantly, the valuation looks very attractive at the current stock price level.

Seeking Alpha

Company information

GRBK is a diversified homebuilding and land development company. The company acquires and develops land and builds homes through eight brands of builders in several states across the U.S. Green Brick Partners is engaged in all aspects of the home-building process. This includes land acquisition and development, entitlements, design, construction, title and mortgage services, marketing, and sales.

The company's fiscal year-end on December 31. GRBK has three reportable segments - Builder operations Central, Builder operations Southeast, and Land development. Builder operations Central is the company's largest and most profitable segment, according to the latest 10-K report .

Compiled by the author based on the latest 10-K report

According to the Seeking Alpha Quant grades, the company is number one in the Homebuilding industry.

Seeking Alpha

Financials

Over the past decade, Green Brick demonstrated impressive revenue growth, compounding at 24% yearly. Gross margin stagnated and decreased between FYs 2013 and 2019, but it has been on the expansion path in recent years. The levered free cash flow [FCF] margin has been mostly negative over the decade, but in FY 2022, the company delivered a break even.

{kind=link}

An operating margin above 20% looks stellar, but I would like to emphasize that it has little potential to expand other than enjoying the economies of scale effect. The reason is that the SG&A to revenue ratio is already low, and I think the upside potential from operating expenses optimization is minimal. The only way to improve operating profits was by increasing the scale, but here we also see a nine-fold increase in scale over the past decade did not help much to improve the gross profit.

Now let me narrow down my financial analysis to a quarterly level. The latest quarterly earnings went live on May 3, with GRBK smashing consensus estimates. Revenue grew about 15% YoY, indicating strong momentum. Adjusted EPS expanded YoY as well, from $1.20 to $1.37. The gross margin was almost flat YoY, and the operating margin softened slightly due to the inflationary environment. I would like to underline that despite a substantial YoY increase in revenue, inventory increased moderately by 3%. To me, this indicates the management's proactiveness in navigating the challenging environment of high uncertainty, especially regarding the demand.

The upcoming quarter's earnings are expected to be released on August 2, with revenue projected at about $394 million and EPS at $1.15 vs. revenue of $525 million in Q2 FY 2022. Of course, the demand is softening, which was announced by the management. But, it is also important to remember a $551 million backlog at the end of Q1, which increased 49% sequentially, according to the latest earnings call .

Seeking Alpha

The company's financial position is in good shape. Leverage and liquidity metrics are prudent and the cash position is also decent.

Seeking Alpha

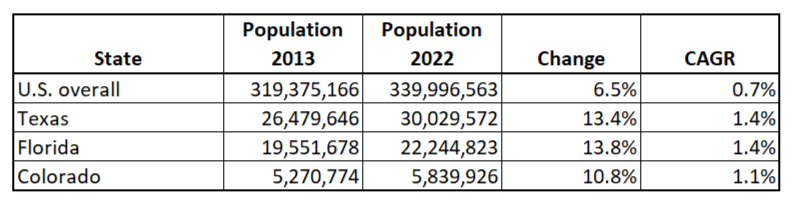

Despite the challenging environment, I am convinced that headwinds are temporary and not secular. On the contrary, according to Argus Research, there is a shortage of homes after over a decade of underbuilding following the Great Recession. And the issue of underinvestment in residential construction is multiplied by another massive secular tailwind. The vast "Millennial" generation enters the market. I think Green Brick Partners is well-positioned to absorb these favorable secular factors. Actually, the company is likely to outperform the industry because its business is focused on the sunbelt and sunbelt adjacent states, including Texas, Colorado, and Florida. In the table below, you can see that population of these states grew about two times faster than the U.S. average CAGR. It is significant considering a ten-year horizon.

{kind=link}

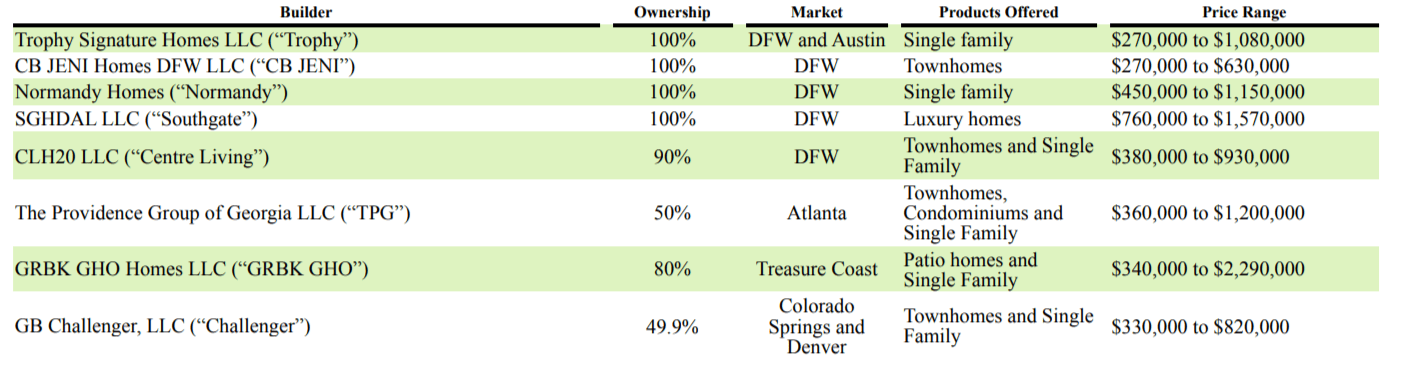

Another big reason GRBK is well-positioned to benefit from the favorable secular tailwinds is its diversified portfolio of brands aimed at very diverse groups of customers. Some of the builders owned by the company offer single-family houses with prices below $300 thousand, while other builders under the GRBK's umbrella offer luxury homes with a price tag above $1.5 million.

{kind=link}

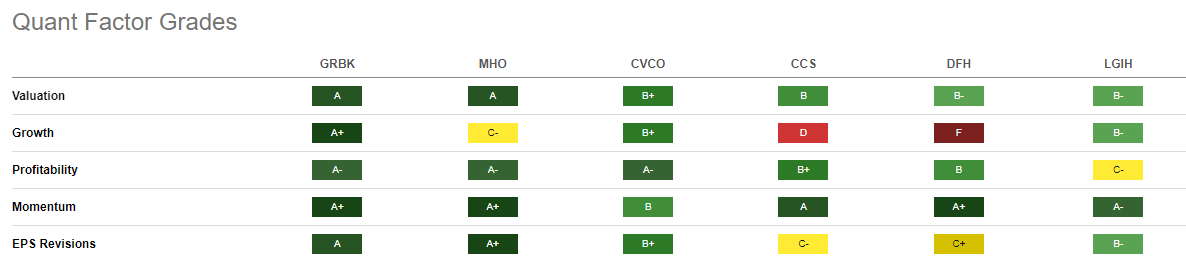

As mentioned in the "Company Information" section, GRBK is rated number one in the Homebuilding industry by Seeking Alpha Quant grades. The company is the best in class across key Quant Factor Grades. As we see below, the closest rivals in the Quant Grades are M/I Homes (MHO) and Cavco Industries (CVCO).

{kind=link}

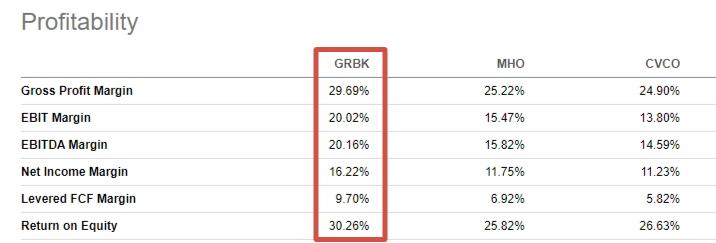

GRBK's revenue is slightly lower than CVCO's and more than two times lower than MHO's. But despite the smaller scale, Green Brick Partners demonstrates substantially higher profitability than competitors. It is a bullish sign, meaning the company is more efficient than its competitors. We should also remember that GRBK can improve its profitability metrics once the company reaches MHO's scale.

{kind=link}

I think doubling the scale is a matter of time because of the significant reasons I described above. We have an overall secular trend at the "Heart" of the U.S. economy moving South, described by Alice Wright .

Valuation

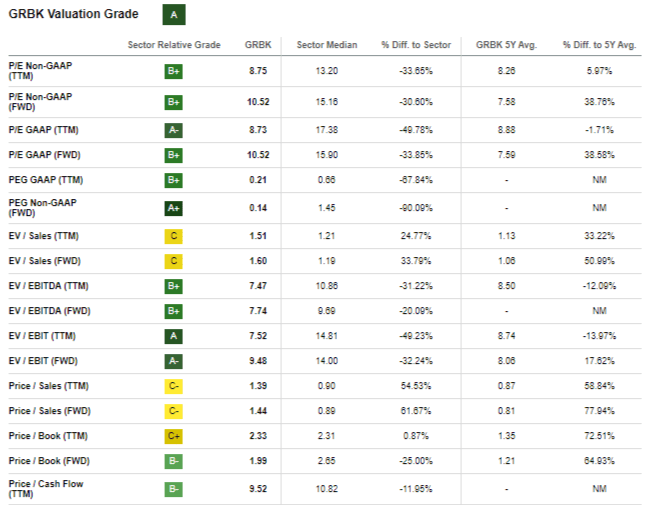

The stock is on fire this year with a 124% price appreciation year-to-date. Seeking Alpha Quant assigns the stock a stellar "A" grade because of low valuation multiples compared to the sector median. If compared to the company's historical averages, multiples look high. The picture is mixed from a valuation ratios perspective, and I need to implement another approach to cross-check.

{kind=link}

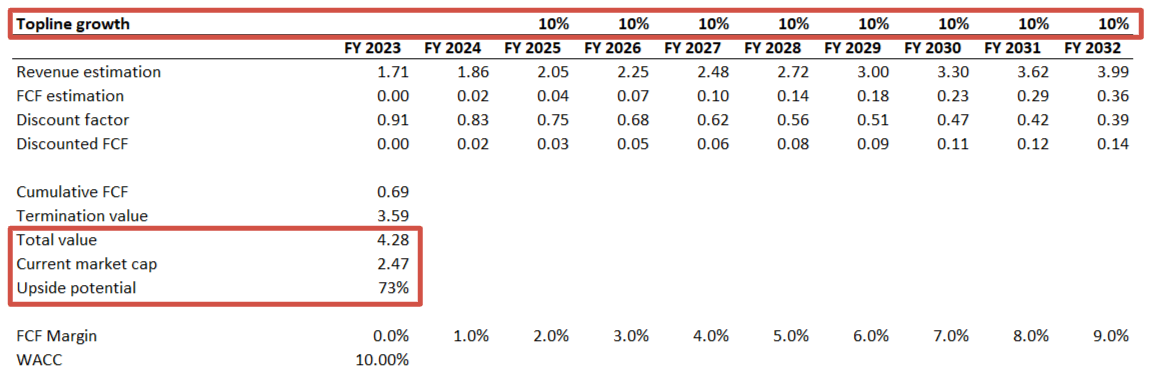

GRBK is an aggressive growth company. Therefore, the discounted cash flow [DCF] approach is proper for my valuation analysis. Valueinvesting.io suggests the company's WACC is about 10%, which I consider fair. I have revenue consensus estimates for the two upcoming years, and for the period beyond, I will implement a 10% top-line CAGR. For the FCF margin of the current fiscal year, I expect it to be zero and to expand by one percentage point yearly.

{kind=link}

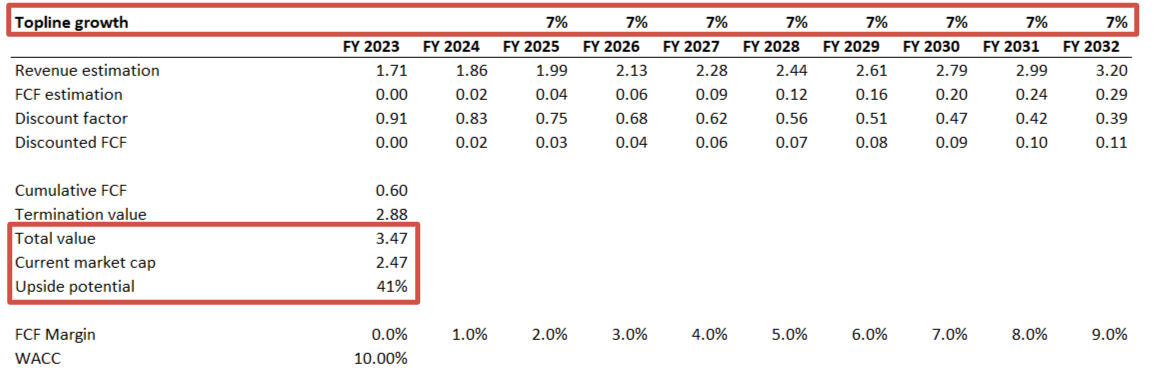

The upside potential looks very impressive with moderate assumptions. Some bears might argue that a 10% revenue CAGR is challenging to sustain over the long term. So, let me simulate another scenario with a more pessimistic growth profile. I implement a 7% revenue CAGR for the second scenario, and other assumptions will remain unchanged. Even with a much more pessimistic revenue growth projection, the upside potential is still high at above 40%.

{kind=link}

To sum up the valuation, the upside potential is very attractive. Now let me discuss significant risks that I see before the final decision is made.

Risks to consider

The company operates in a highly cyclical homebuilding industry, meaning that earnings depend on the overall health of the broader economy. Given the highest mortgage rates over multiple years since the Great Recession, the current macro environment is challenging, and demand is under pressure. On the other hand, the company can successfully navigate the challenging environment sustaining revenue growth and margin expansion. The upcoming quarter is expected to demonstrate a decrease in revenue and EPS, and investors might start to panic and sell off the stock if the company misses quarterly earnings forecasts.

GRBK is a general contractor meaning the company is highly dependent on the quality of work performed by subcontractors. Subcontractors' misconduct or low-quality performance can damage the company's reputation. It will adversely affect Green Brick's earnings.

The company's financial performance also depends heavily on the prices and availability of raw materials, meaning any disruptions in the supply chain might lead to idle time and unexpected costs.

Bottom line

To conclude, GRBK's valuation looks attractive even after a massive year-to-date rally. I like the company's clear trend of the FCF margin improvement, and I think that the execution is exemplary amid the current harsh environment. There is still plenty of room to improve the gross profit as the company continues to scale up. The balance sheet also looks solid and ready to weather the storm. Therefore, I assign Green Brick Partners stock a "Buy" rating.

For further details see:

Green Brick Partners Is A Very Attractively Valued Top-Rated Stock