GRBK - Green Brick Partners: Not Just Another Brick In The Wall

2023-06-12 01:10:46 ET

Summary

- Green Brick Partners is a Texas-based homebuilder and land development company that has seen a 125% increase in 2023, outperforming the homebuilder index.

- GRBK reported strong Q1 results with record home closings revenue and a high homebuilding gross margin of 27.6%, making it a good buy for investors.

- Risks include a potential recession and rising mortgage rates, which could impact the housing market and GRBK's performance.

All in all, you're just another brick in the wall."

- Pink Floyd

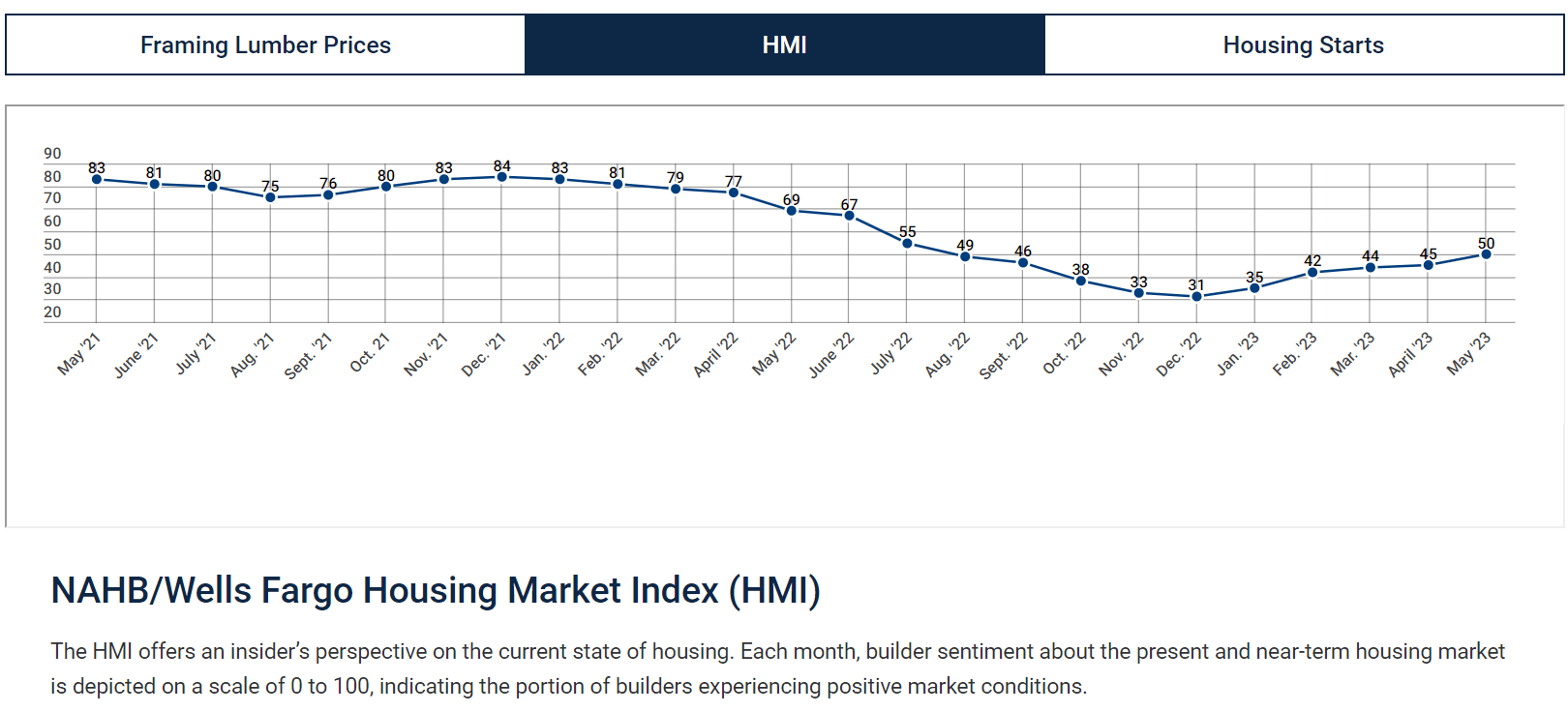

The US homebuilder industry struggled mightily in 2022 when inflation began raging out of control and interest rates shot up from the near zero rates where they had been hovering for several years prior. According to the NAHB , the HMI index declined steadily from December 2021 where it reached a high of 84 down to a bottom in December 2022 where it reached a low of 31. In 2023, there has been a slow recovery as home prices have stabilized and buyers are beginning to return to the market, despite still relatively high mortgage rates around 7%.

{kind=link}

The year started out with a cooling housing market partly because of the Fed's fight against inflation leading to significantly higher mortgage rates. Buyers were scared off by the increasing home prices that finally cooled off in February as home prices dropped year over year for the first time in 11 years. Home sales finally began bouncing back in recent months leading to a resumption in price increases.

Home sales are bouncing back and forth but remain above recent cyclical lows," says NAR Chief Economist Lawrence Yun. "The combination of job gains, limited inventory and fluctuating mortgage rates over the last several months have created an environment of push-pull housing demand."

Of course, not all regions of the US are experiencing the same patterns and trends. For example, in Texas, some of the hottest real estate markets are in desirable areas like the suburbs of Dallas and Austin. Over the past decade, Texas has had some of the strongest home price appreciation rates in the country.

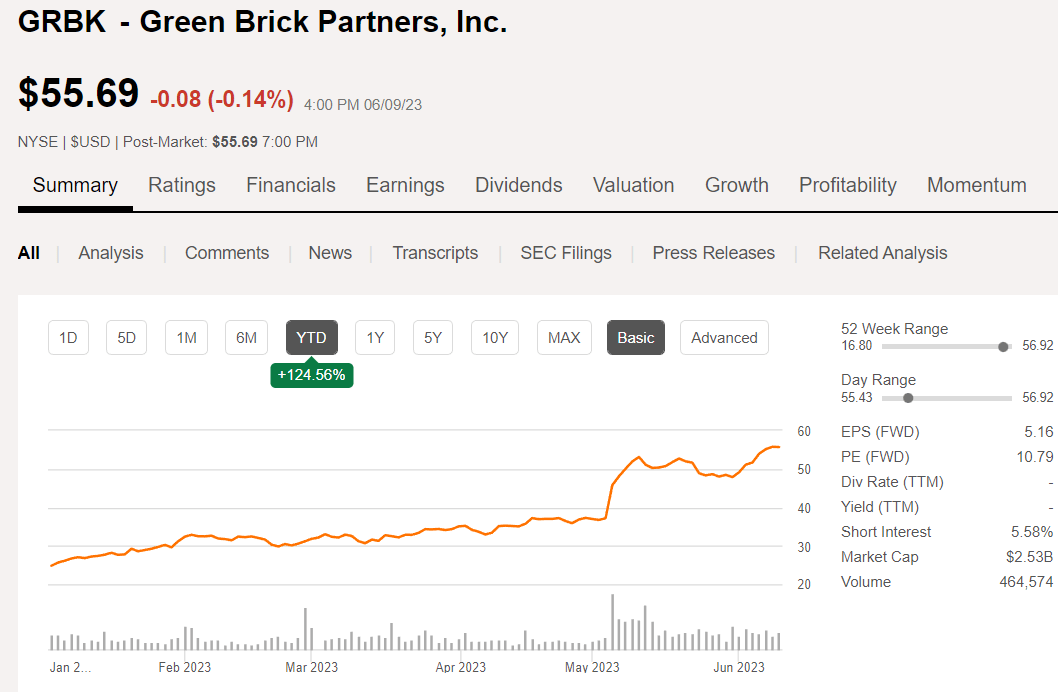

Green Brick Partners ( GRBK ) is a Texas-based homebuilder and land development company that operates in Texas, Georgia, and Florida, and has a non-controlling interest in a Colorado homebuilder. Overall, these are some of the fastest growing real estate markets in the country. While homebuilders overall are starting to show signs of recovery in 2023 with the homebuilder index as represented by XHB up about 22% YTD, GRBK has increased by nearly 125%, yet still trades at an inexpensive forward P/E under 11.

I rate GRBK a Buy despite the recent runup in price as they are poised to continue to grow due to their high exposure to the best real estate markets, superior lot and land positions, an efficient operational infrastructure, and strong balance sheet.

{kind=link}

An additional consideration that is sometimes overlooked by other analysts covering the stock is that David Einhorn's Greenlight Capital has a substantial interest in GRBK. In fact, according to Yahoo Finance , Greenlight had this to say in their Q123 investor letter about their investment in GRBK:

Starting with the good, Green Brick Partners, Inc. , which was our largest loser in 2022, was, conversely, our largest winner in the first quarter. The shares advanced from $24.23 to $35.06. Analysts have raised 2023 EPS estimates from $3.16 to $3.34. While that might not seem significant, it reflects a reversal of the downtrend in those estimates. With the market gaining confidence that the earnings expectations had fallen too far, the shares have rerated to just over 10x estimated 2023 earnings (but still less than 6x trailing earnings). GRBK has the highest gross margins, and nearly the highest ROE, in the industry. It also has an enviable land position in some of the most desirable markets. The $3.34/share earnings estimate for 2023 would be about a 15% ROE. If that is what a down year looks like, it's hard to understand why a single digit P/E would be warranted."

Q1 2023 Results and Outlook

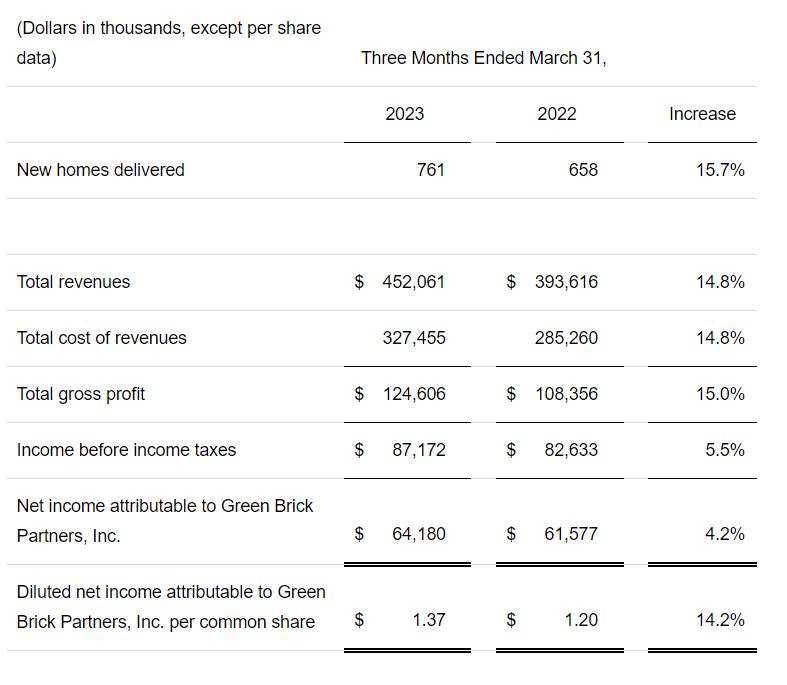

On May 3, 2023, the company reported Q1 results and had a blowout quarter with the best results in the company's history.

We are pleased to report that Green Brick kicked off 2023 with the best first quarter results in our history. We delivered 761 homes which was a record for any first quarter. Home closings revenue increased 24% year-over-year to $449 million. We were able to sustain a high homebuilding gross margin of 27.6%, which was one of the highest among public homebuilders in the first quarter and is up 140 bps sequentially," said Jim Brickman, CEO and Co-Founder. "As a result, our earnings per diluted share grew 14% to $1.37 for the quarter."

In addition, despite what he referred to as a "stormy" environment for housing, CEO Brickman reported strong sales momentum in the quarter with net sales up 78% year over year and 152% sequentially. The backlog also increased by 49% sequentially to $551 million and spec percentage of units under development decreased to a more reasonable level of 59%.

The debt to total capital ratio decreased by 500 bps YOY to 23.8% and the net debt to total capital ratio was decreased to 13.3%. The company also returned $15.4 million to shareholders in stock repurchases. The Board also approved an additional $100M in buybacks bringing the total repurchase authorization to $133 million. Results were summarized in this table that was included in the Q1 press release .

{kind=link}

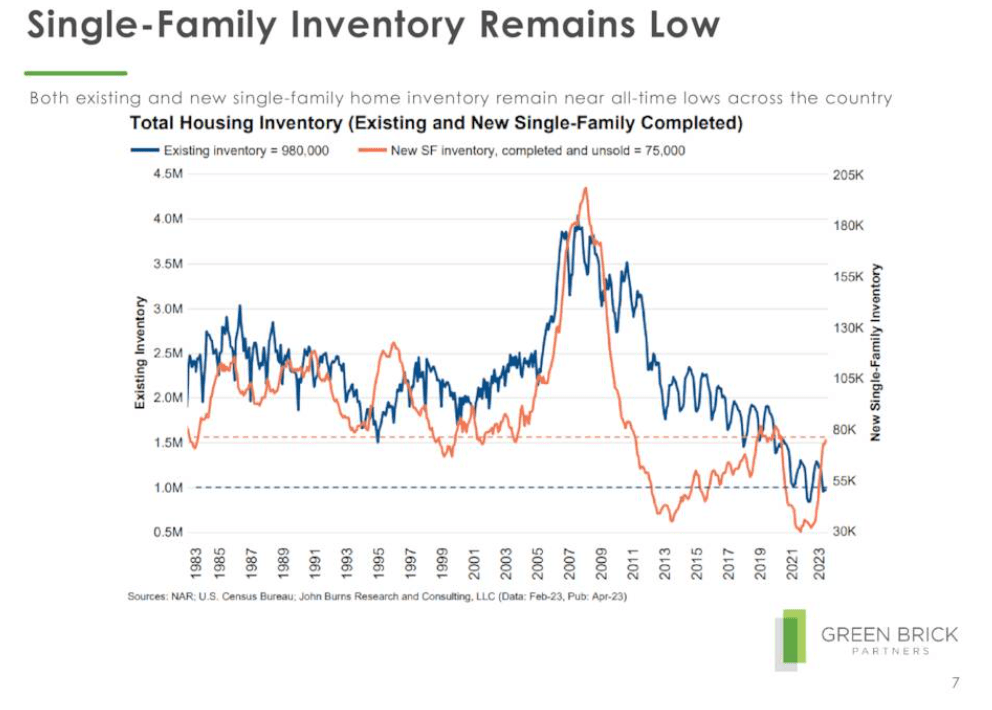

In the month following the Q1 report, the market responded by sending shares higher, yet even at a closing price of $55.69 on 6/9/23 the stock trades at less than 11x forward EPS estimates. Inventories of single-family homes remain low providing a runway for future growth as shown in this slide from the Q123 investor presentation.

{kind=link}

At the end of 2022 the company had about 6,000 finished lots and of those about 75% in 2023 are expected to be in infill locations. Because Green Brick develops the lots and land themselves, they can realize higher margins than their competitors. New communities provide ample opportunities to generate favorable sales per community, further enabling them to achieve higher margins than traditional homebuilders. Many of those lots are in the most desirable parts of the Dallas and Atlanta metropolitan areas.

Those infill submarkets require local expertise and local knowledge and therefore less competition and higher price advantages. With more than 80% of total revenues generated from infill locations in Q123, the advantages of higher margins with reduced competition are meaningful and add to the bottom line with increased profitability. Meanwhile, housing supply remains lower than demand, especially in those infill areas where Green Brick specializes. According to the earnings call, the company owns and controls about 25,000 lots and they are constantly on the hunt for new opportunities. As COO Jed Dolson stated on the call:

These lots are favorable cost basis; we believe should continue to help us generate industry leading gross margins. Due to the fallout from the banking sector stresses smaller and private builders are squeezed by rising costs and capital and tightening and financing terms. In an environment with persistently low existing home inventory, we believe we are well suited to take market share with a strong balance sheet and ample high quality finished lots in infill locations."

More Positive Indicators

Although few Wall Street analysts follow the stock, 1 has a Strong Buy rating while 3 rate the stock a Hold. SA analysts rate the stock a Buy, while the SA Quant rating gives it a Strong Buy and rates GRBK the #2 stock out of 4,708 rated. In other words, GRBK is currently one of the best possible stocks to buy out of more than 4,700 stocks rated by the quant system!

Seeking Alpha

Upward revisions to revenue and earnings estimates have been coming in over the past few months, further highlighting the strong growth and profitability of the stock. At the time of the Greenlight Capital letter, the EPS estimate for 2023 was raised to $3.34. The latest estimate for FY 2023 is for more than $5 in EPS.

{kind=link}

The current trailing GAAP P/E is just under 9 and with EPS estimates of about $5 per share the forward P/E is at about 11x earnings. For a growth stock that is seeing multiple upward earnings revisions, is capturing market share from their competitors, and increasing margins while reducing debt, I feel that the stock deserves a much higher multiple going forward. Historically, the stock has traded at a P/E under 10 for most of the past 3 years, but the stock is gaining momentum as the economy changes, and they are able to leverage their local expertise and land positions to capture additional market share.

{kind=link}

As the market begins to recognize the growth opportunity that the stock offers to investors who are willing to bet on a continued increase in margins and overall profitability, I believe that the price will rise along with earnings and a more reasonable multiple of 12 to 14 times earnings is not unrealistic. Therefore, I would assign a year end price target range of $62 to $72 per share based on the current FY 2023 EPS estimate of $5.16.

Risks and Conclusions

While the housing market is showing signs of recovery and the job market is still strong, there is an overwhelming sense that recession is still just around the corner. The broader economy could easily take another downturn in the coming months, especially if inflation does not abate quickly enough for the Fed to stop raising rates. If mortgage rates were to resume their upward trajectory above 7%, demand could further soften and GRBK may suffer as a result.

With a market cap of about $2.5B the stock is a small cap stock that trades with relatively light volume so there could be some volatility in the price action. At the current price of about $55, I rate the stock a Buy, but if the price should pull back below $50, I would increase my rating to a Strong Buy. The stock currently has momentum but that could change quickly if the overall market begins to retreat after reaching a new bull market phase in 2023. If I were new to the stock, I would start with a small position and add on dips. I currently own a few shares at a cost basis of about $50 and will look to add more if the price dips below $50 in the coming weeks.

For further details see:

Green Brick Partners: Not Just Another Brick In The Wall