GRBK - Green Brick Partners: Should You Move Into The Preferreds?

2024-01-16 16:00:00 ET

Summary

- GRBK's Series A preferreds offer an 8% yield on cost and are trading at a 29% discount to their liquidation price of $25 per share.

- The company's common shares are trading near all-time highs, with a record high gross margin and strong earnings.

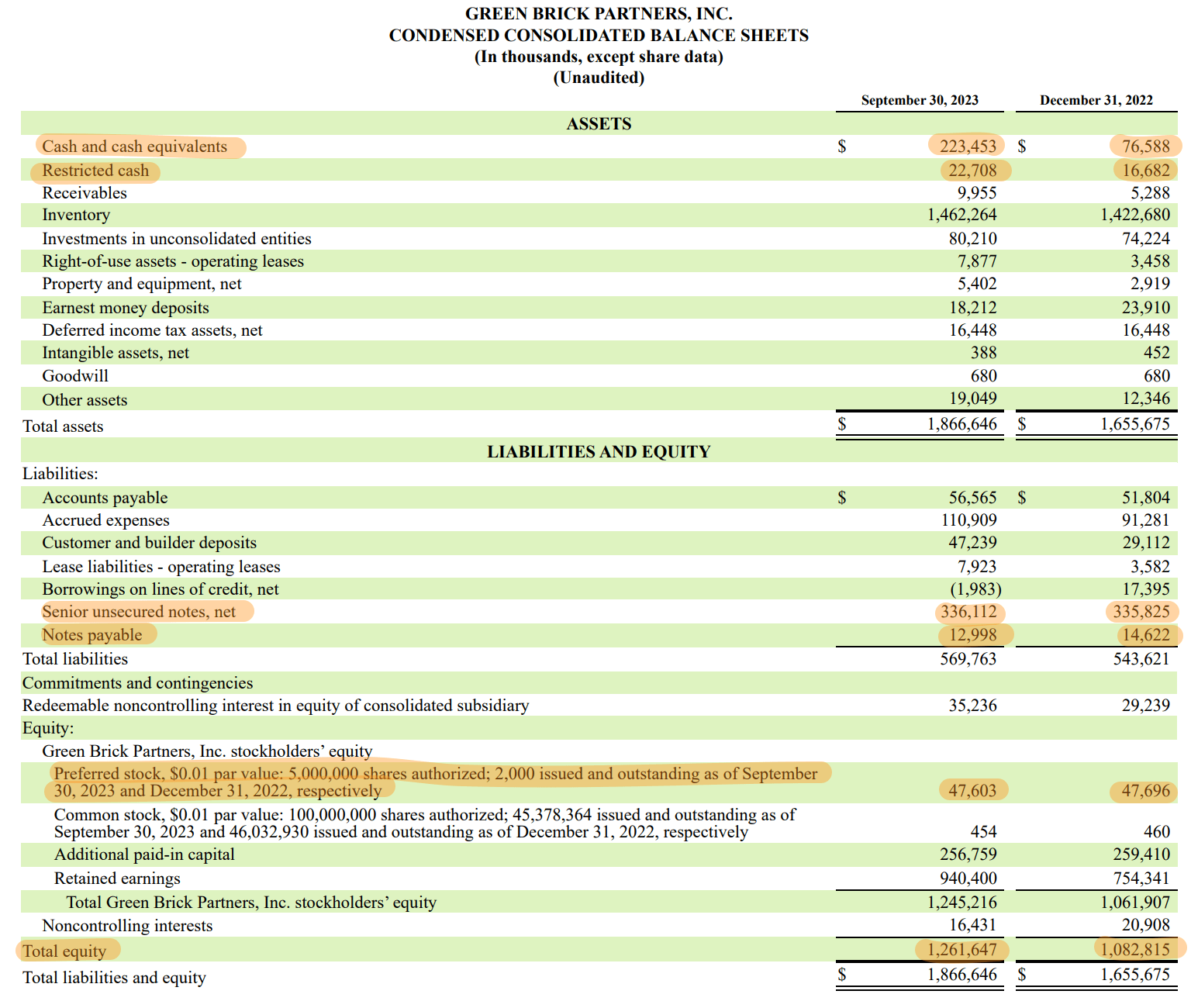

- Cash and equivalents of $223.45 million means a material level of coverage for the preferred payments with GRBK also materially delivering its balance sheet.

Diversified homebuilder Green Brick Partners ( GRBK ) has expanded rapidly over the last five years with revenue up by a 22% compound annual growth rate from 2019 as demand for homes in its core markets continues to expand at a breakneck pace. GRBK's largest markets in Dallas and Atlanta continue to benefit from strong in-migration with Dallas increasingly attracting Wall Street banks and asset managers looking to capitalize on cheaper labor costs and space to build bespoke campuses. The area now has more finance workers than Chicago.

{kind=link}

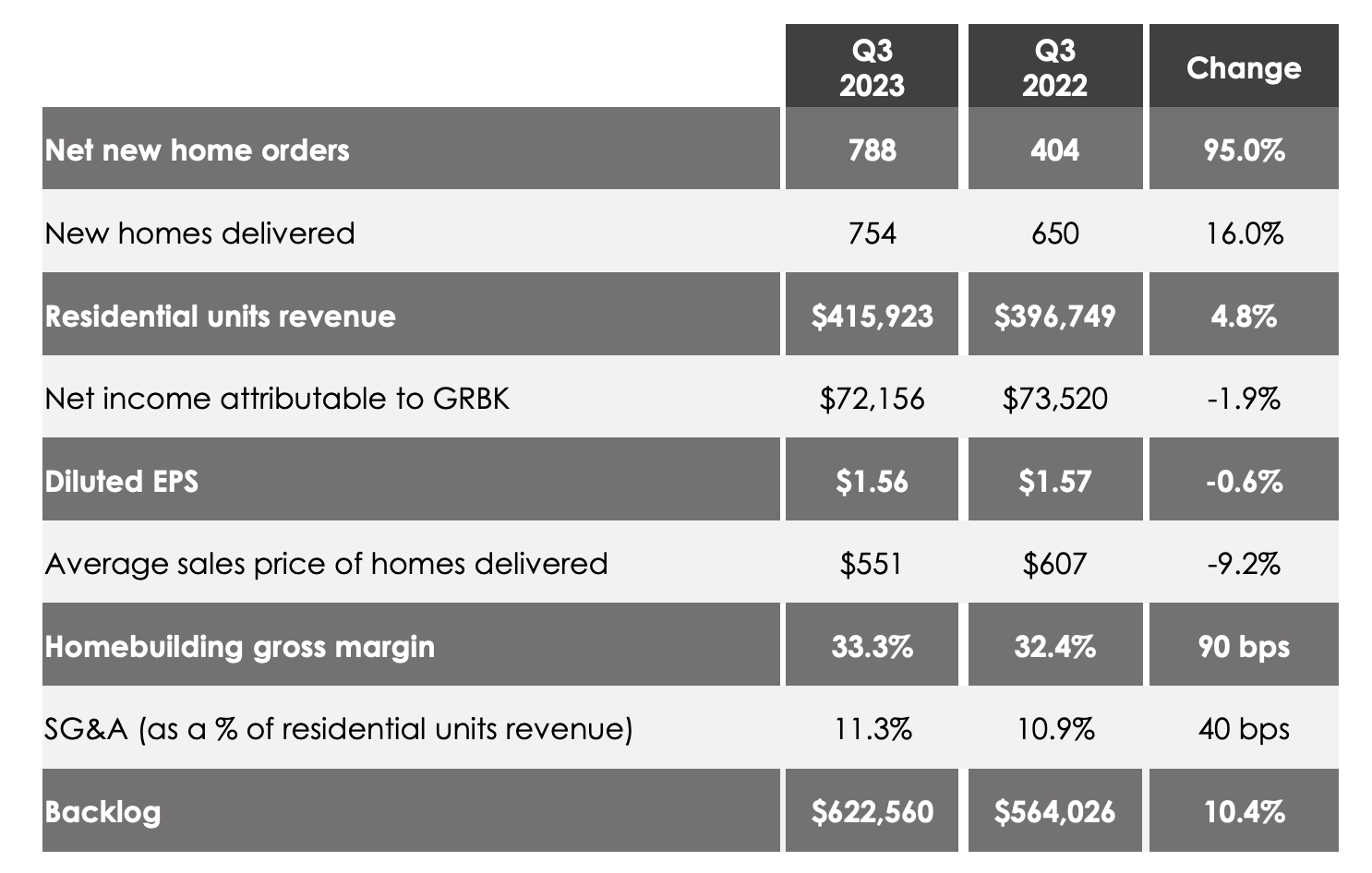

GRBK saw net new home orders of 788 homes during its fiscal 2023 third quarter, an increase of 95% year-over-year with revenue of $419.98 million up 3% over its year-ago comp and beating consensus estimates by $6.96 million. New homes delivered at 754 was up 16% over its year-ago period but with the average sales price of homes delivered down 9.2% to $551,000 due to a change in product mix.

{kind=link}

The common shares are currently trading near all-time highs with gross profit margin of 33.3% during the third quarter forming a record high and driving diluted earnings of $1.56 per share with a year-to-date earnings figure of $4.55 per share. GRBK has proved to be shrewd in its deployment of capital to jump on housing demand with its backlog value at the end of the third quarter increasing by 10% year-over-year to $623 million .

Risks And Opportunities Of The Series A Preferreds

{kind=link}

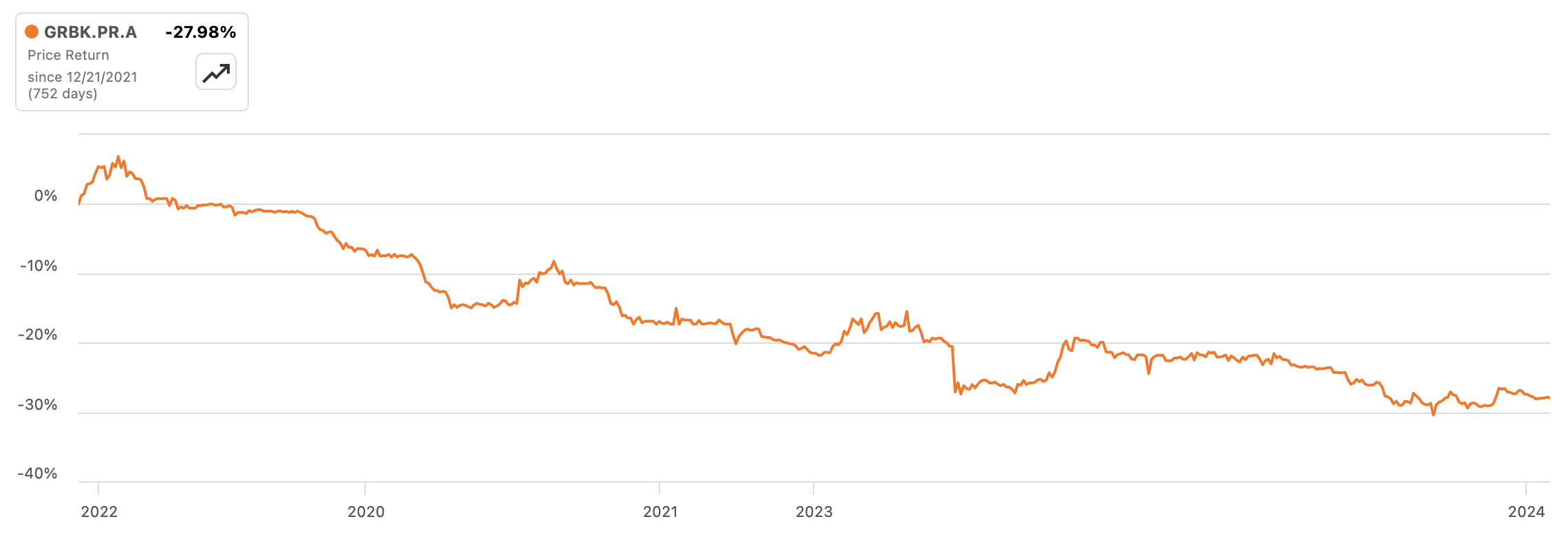

I've been buying the 5.75% Series A Preferreds ( GRBK.PR.A ). These pay out a fixed annual coupon of $1.4375 per share and are currently swapping hands for $17.86 per share. This means an 8% yield on cost for a 29% discount to their liquidation price of $25 per share. Using bond terminology, these are trading for roughly 71 cents on the dollar whilst offering a yield that's 270 basis points ahead of the Three-Month CME Term SOFR. These started trading in December 2021 when 2,000,000 shares were sold for $50 million in gross proceeds. They immediately faced duration risk as the Fed started hiking rates from the start of 2022.

{kind=link}

Preferreds are essentially hybrid securities that merge features of bonds and common equity. Hence, whilst GRBK does not pay a dividend to common shareholders, the Series A would have a higher claim on its earnings than the common shares. Whilst they rank lower than debt on GRBK's capital structure, they're cumulative and perpetual. The former means any missed payments accrue as a liability on GRBK's balance sheet for repayment at a later date. It's a feature that materially reduces the probability of missed payments even in the event the company experiences earnings volatility . Being perpetual means there's no fixed rate at which GRBK is forced to redeem them fully.

Their redemption date on 12/23/2026 provides GRBK the option to but not the obligation to buy them back for $25 per share. The company can and has already been buying them on the open market with a marginal purchase of $93,000 made in the 9 months from the end of the third quarter. GRBK's cash and equivalents position of $223.45 million as of the end of its third quarter is at its highest level in over a decade with this position further bolstered by restricted cash of $22.71 million. This combined with its highly cash generative operations means a high degree of coverage for the preferreds. Cash flow from operations during the third quarter was $20.6 million to provide material coverage of the preferred payments.

{kind=link}

GRBK is also deleveraging its balance sheet with $42 million in repayments on its lines of credit in the 9 months from the end of its third quarter. Critically, GRBK's debt-to-equity ratio is low and continues to fall. Total equity was $1.26 billion at the end of the third quarter, up 22.7% from its year-ago comp with its debt-to-equity ratio falling to its lowest level in over five years at 0.28x. This is likely set to move lower.

Hence, the current discount on the preferreds seems odd against what's a materially derisked balance sheet and a stable cash-generative business. Whilst GRBK does face recession risk, its cash position provides sufficient depth for continuous coverage of the preferreds as the company continues to chase growth. The Fed could also be set to cut rate by at least 75 basis points this year to deliver a boost to housing affordability and demand for new homes. I'm comfortable building a substantial position in the preferreds here with the commons being rated as a hold.

For further details see:

Green Brick Partners: Should You Move Into The Preferreds?