AAWH - Green Thumb Industries Is Not The Best Way To Invest In Cannabis

2023-12-24 09:06:10 ET

Summary

- Green Thumb Industries is a popular cannabis stock that has rallied 54% since July.

- GTI's revenue has increased by only 2% in 2023, but its operating cash flow has improved.

- Analysts expect GTI's revenue and adjusted EBITDA to increase in 2024 and 2025.

- The stock seems expensive to peers.

I have followed Green Thumb Industries (GTBIF) since it went public in 2018, and it is one of the 26 cannabis stocks on my Focus List. I do not include it in either of the model portfolios I share with my investing group. It's very popular with investors.

I last wrote about the company on Seeking Alpha in July, saying it wasn't yet time to buy the stock. In fact, it may have been, since the stock has subsequently rallied 54%. Of course, many cannabis stocks have rallied since then, and some have rallied even more due to the potential rescheduling of cannabis and the potential elimination of 280E taxation.

In this review, I discuss the company's 2023, assess the outlook, look at the chart and assess the GTI valuation. I find the stock to have less upside than many of its peers and a lot of downsides relative to some ancillary stocks and some Canadian LPs.

GTI's 2023

In the first three quarters of the year, GTI revenue has increased just 2% to $776.3 million. Analysts project that Q4 will be up 4% from a year ago and leave overall revenue above $1 billion again. Operating income has declined 19% to $134.3 million as operating expenses have increased as gross profits have been only slightly higher. The gross margin in 2023 has been 49.4%, down slightly from the 50.1% in the first three quarters of 2022. Adjusted EBITDA has increased about 2% to $235 million.

Operating cash flow in 2023 has been better so far, with cash flow from operations of $153.9 million in the first three quarters compared to $88.2 million in the first three quarters of 2022. At the same time, though, capital spending has grown from $119.9 million to $183.6 million, leaving free cash flow negative (-$29.7 million). While the increase in income tax payable is not nearly as bad as some peers, it has increased from $4.4 million to $16.1 million.

The GTI balance sheet has remained better than peers. The company ended Q3 with tangible equity of $565.2 million. Adjusted for in-the-money options, it would be $583.1 million. This is far better than every other large MSO, especially Curaleaf ( CURLF ), which has a very negative tangible book value. Having tangible assets in excess of liabilities can help with extending debt, so GTI is safer than peers in negative scenarios. The company has less net debt than peers at $162 million. Its total debt outstanding of $299 million is below its tangible equity. It is due in April 2025.

While the company hasn't been growing its top-line very rapidly, the company has been expanding. Its retail business has grown 3% to $582.4 million. The company at the end of Q3 had 85 stores in operation, up 10% over the past year. It currently has 89 stores after its recent Florida expansion. Its wholesale business (which it calls Consumer Packaged Goods net of intersegment eliminations) has expanded less than 1% to $194.0 million. This has been in the context of both Maryland and Connecticut legalizing for adult-use.

The Analyst Outlook

Analysts currently expect 2024 revenue to increase 7% to $1.116 billion, according to Sentieo. This is slightly more than what they had expected before the Q3 report. The adjusted EBITDA is expected to increase 6% to $331 million. Before, they had expected it to be $335 million, and this was down a lot from the $362 million ahead of the Q2 report.

For 2025, 7 of the 17 analysts are providing estimates, up from 5 ahead of the Q3 report. The revenue is expected to increase 10% to $1.231 billion, down slightly from the prior expectation ahead of the Q3 report. Adjusted EBITDA is expected to rise 15% to $379 million, also down slightly from the prior expectation. This is a 30.8% margin.

The big driver for the financials will be whether 280E goes away. This will have no impact on adjusted EBITDA, as taxes are excluded, but it will impact cash flow and EPS. GTI is one of the few MSOs that reports positive EPS, with analysts projecting $0.18 in 2023, $0.25 in 2024 and $0.37 in 2025.

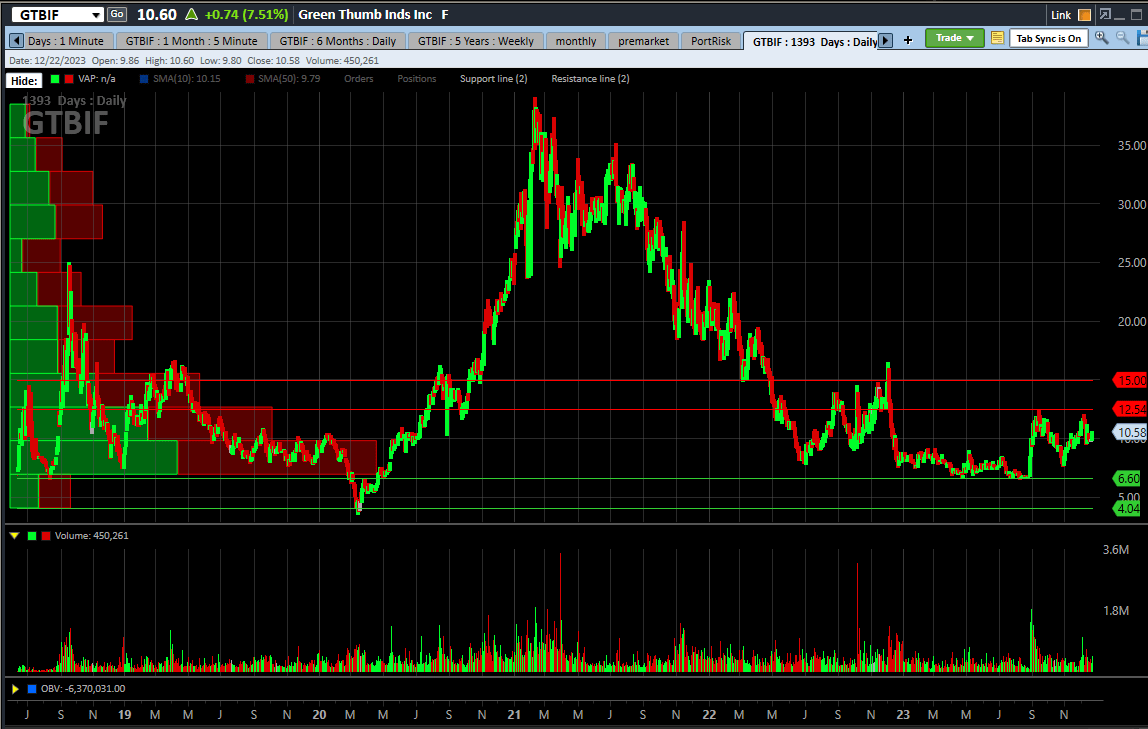

The Chart

The stock is way above its all-time low set in early 2020, which is very different from most of its peers. GTI is down a lot since its peak in early 2021, but the decline has been less than the drops by its peers:

{kind=link}

In 2023, the stock has rallied 22.7%, well ahead of the NCV Global Cannabis Stock Index, which has declined 18.2%.

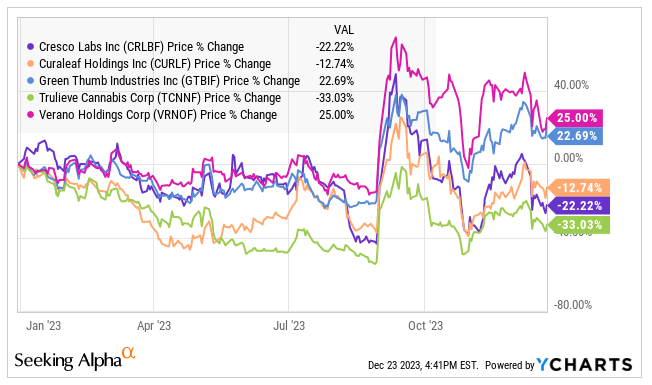

Here is how it has performed against the Tier 1 MSOs:

{kind=link}

Verano Holdings ( VRNOF ) is up a bit more, and all the rest, including Trulieve ( TCNNF ), Cresco Labs ( CRLBF ) and Curaleaf are down. Over the past three years, it is down the least:

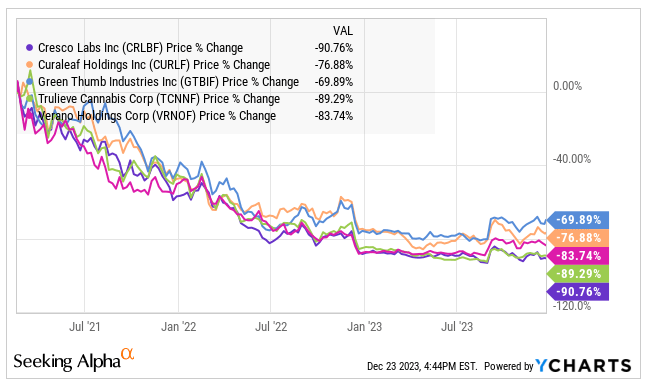

{kind=link}

One thing that investors should understand is that the AdvisorShares Pure US Cannabis ETF ( MSOS ) holds a large position of 14.9 million shares ($158 million), which represents 28.3% of the fund. If the market gets hit with another downturn and the fund sees redemptions again, it will need to sell some shares at a time when there might not be buyers.

Speaking of selling shares, two insiders recently sold a combined 1 million shares at $10 to a qualified institutional buyer in late November. I don't view this negatively, as the insiders still hold a lot of stock and as the transaction was driven by a buyer. Interestingly, the company talked about its share repurchases before it executed them quickly, and in the 10-Q it disclosed paying $9.96 for 2.5 million shares purchased on the open market in September.

The Valuation

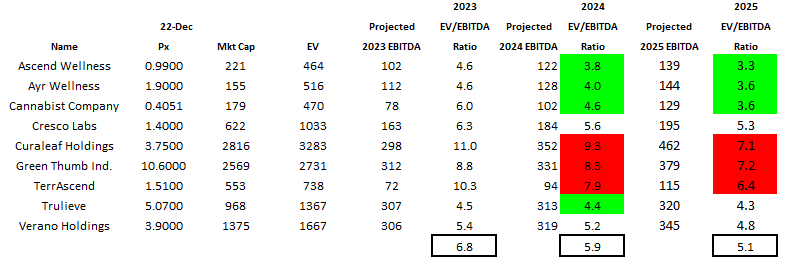

The GTI valuation isn't bad, in my view, but it is a shade more expensive than most of its peers. The table below includes the five Tier 1 names and also 5 Tier 2 names, including Ascend Wellness ( AAWH ), Ayr Wellness ( AYRWF ), Cannabist ( CBSTF ) and TerrAscend ( TSNDF ). Looking a year ahead at the enterprise value to projected 2024 adjusted EBITDA, GTI is well above the average and is second highest:

Alan Brochstein, using Sentieo

{kind=link}

GTI has the best balance sheet among these nine companies, with net debt of $162 million. The stock is one of the few that has positive tangible equity, but its market cap is 4.1X the tangible book value. The balance sheet is better in other ways too. Income tax payable isn't included in debt, and some of its peers have a lot more of it than GTI, which has just $16.1 million. Its current ratio (current assets divided by current liabilities) of 2.1X is better by far than its peers, some of which are below 1X.

How the MSOs will be valued in the future will depend heavily upon what happens to 280E. If it goes away, adjusted EBITDA won't change, but investors will be likely to buy the stocks at higher prices due to lower taxation, better cash flow and less risk of bankruptcy. I think that at the end of 2024 without 280E still intact, GTI will trade at an enterprise value to projected adjusted EBITDA for 2025 at 10X, which would be $14.97. This would be 41% higher. Of course, it could be higher than 10X, as the MSOs used to trade at 20X in the early days, but 10X seems appropriate given the lack of growth for the industry right now.

If 280E remains in place, I think that MSOs will see much lower valuations due to concerns about debt. Given its stronger financial position, GTI will trade a lot better than peers, but I think the valuation could be 5X, which works out to $7.15, a decline of nearly 33%. 5X is slightly lower than the current valuation, and perhaps it is too high, as several MSOs that are less secure financially already trade at a lower level.

For those that are confident that 280E will go away, there are MSOs with more upside. One stock that I own in both of my model portfolios, Trulieve, can go up more in my view. At 8X, which is a 20% discount to the valuation I am using for GTI, the stock would rally to $11.30, producing a gain of 123%. My favorite MSO right now given its very low valuation and potential improvement is Cannabist ((CBSTF)), which I last wrote about 12 weeks ago when it was falling but much higher in price than now. My target currently is based on a multiple of 7X in the optimistic scenario and 3X in the pessimistic scenario. These work out to $1.42 in the optimistic case, up 251%, and likely wiped out in the pessimistic case.

For those who are concerned that 280E will remain in place, there are non-MSO choices that make sense. There are Canadian LPs with no debt and lots of cash that trade at a big discount to tangible book value. Organigram ( OGI ), for example, is my favorite cannabis stock, and it trades at about 54% of tangible book value. The stock currently is valued at an enterprise value to projected adjusted EBITDA for FY25 of less than 7X. The company is federally legal!

I also see some relative value in ancillary stocks that trade on higher exchanges and can also trade a pretty good valuations. These stocks do have less downside in my view, and they could benefit from 280E going away as their customers are better able to spend. I wrote about WM Technology ( MAPS ) last week, which has no debt. It currently trades at a lower valuation relative to tangible book value than GTI, and the company, which doesn't pay 280E taxes and is listed on the NASDAQ, is trading at an enterprise value to projected 2025 adjusted EBITDA of just 4.3X.

Conclusion

I think GTI is a high quality MSO with a relatively strong balance sheet, and its valuation isn't too expensive. I don't own any in my model portfolios, because I see some other MSOs as more attractive and because I find cheaper names outside of the MSO sub-sector with very strong balance sheets. I think its holders should consider other cannabis investments.

To be clear, I would not suggest shorting GTI at this time, as there is a path higher if 280E taxation is removed. I believe, though, that many of its peers would do better in that scenario. Again, if 280E doesn't pass, I expect GTI and its peers will decline precipitously.

For further details see:

Green Thumb Industries Is Not The Best Way To Invest In Cannabis