GTBIF - Green Thumb Is Widening Its Lead Over The Rest Of The Sector

Summary

- The first large cannabis company in the United States to find a business model that is profitable.

- Still cash flow positive despite negative -$0.22 EPS.

- Well positioned to adapt to the coming price war that rescheduling will bring.

Thesis

Of all the vertically integrated multi-state operators in the United States, Green Thumb Industries Inc. ( GTBIF ) is one of the very few that has actually found a business model that is capable of making profits through the 280e tax obligation. When cannabis is rescheduled and the barriers to moving cannabis across state lines goes away, the producers are all going to start undercutting each other. I am assigning a Buy to Green Thumb because they have already found viability in the current market environment and are in a better position to adapt to the coming price war than most of their competition.

Company Background

Green Thumb Industries was founded in 2014 and is one of the largest cannabis companies in the United States. The company is headquartered in Chicago, Illinois and operates in several states where cannabis has been legalized for medical and/or recreational use, including Illinois, Pennsylvania, Ohio, Massachusetts, Maryland, New Jersey, and others. Their dispensaries come in a variety of brand names, including Rise, Essence, and The Clinic.

Green Thumb has a vertically integrated business model, which means they control every aspect of the cannabis production process, from cultivation to distribution. It also means that in each state they want to operate in, they have to set up both dispensaries and in state growers to support them.

The Coming Price War

When the Department of Health and Human Services and the Attorney General make their announcement about the rescheduling of cannabis in the United States, two very important things will happen. The removal of 280e will be a boon for most of the sector, and cannabis will be allowed to be shipped across state lines as most of the 50 separate markets all become one market. States like Washington, that currently have laws that ban the sale of cannabis that is grown out of state, have already set up protections for their local industry. Most of the rest of the country has not.

A majority of the cannabis industry in the United States is unprofitable because of the 280e tax obligation. It is widely held that once this goes away, most of the sector will be able to find net profits, but that's simply not true. All the vertically integrated multi-state operators are used to operating as quasi-monopolies, where they have significant but not total control over both supply and price.

{kind=link}

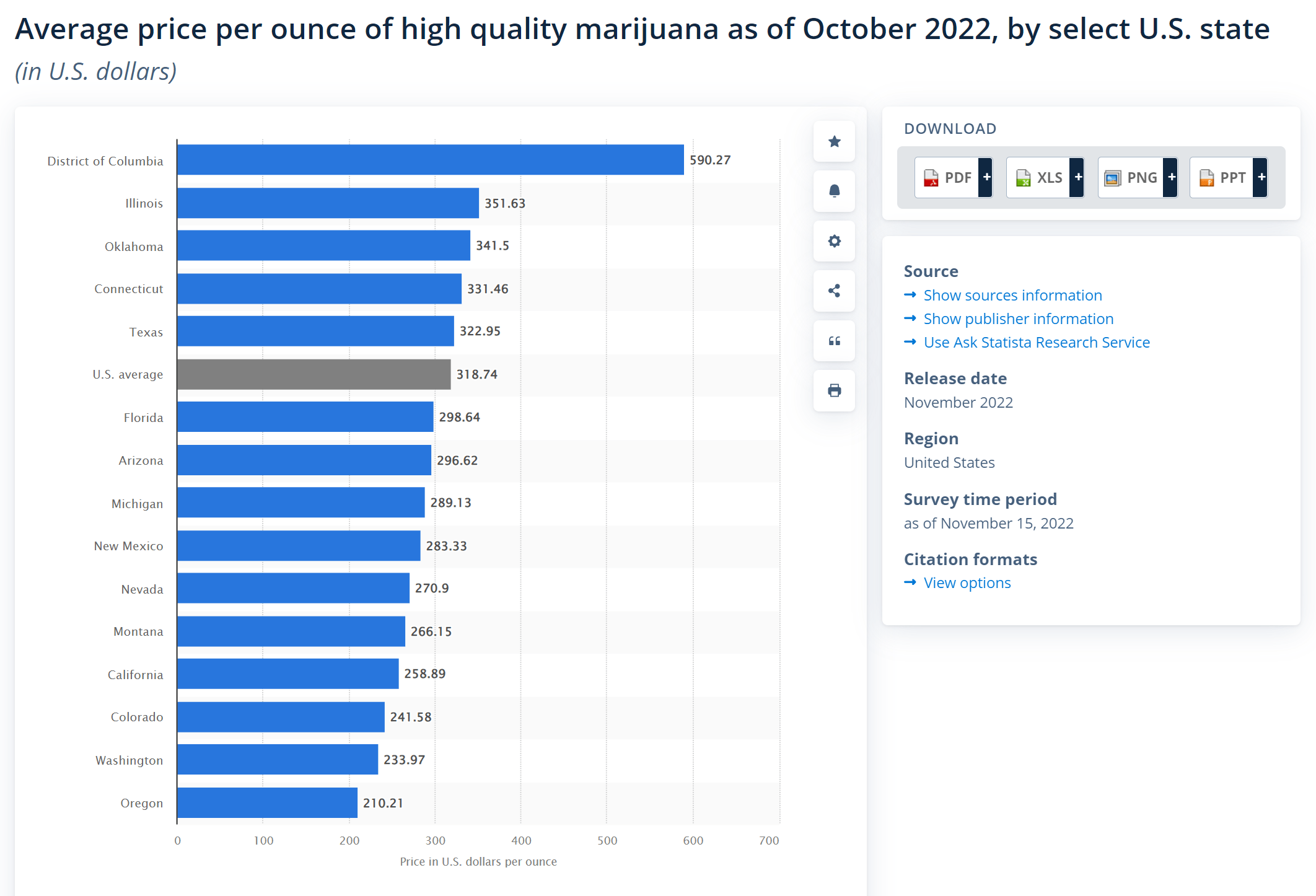

As soon as it's allowed to be shipped across state lines, wholesale cannabis in the United States is going to be pushed down toward Oregon's prices. What do you think is going to happen to the revenue of operators in a state like Illinois when the price drops from $351 per ounce to around $210? How well do you think they are going to do when the product they grow and sell is now suddenly worth 40% less than what they are used to?

In Canada, consumers are already paying $75 USD per ounce for high quality flower. If competition gets fierce enough, it's going to make the United States market start to look like the Canadian market. Things get even worse if the Canadians are allowed to ship their cannabis into the United States. How well do you expect all these vertically integrated companies to perform when the retail price of cannabis is below their present cost of production?

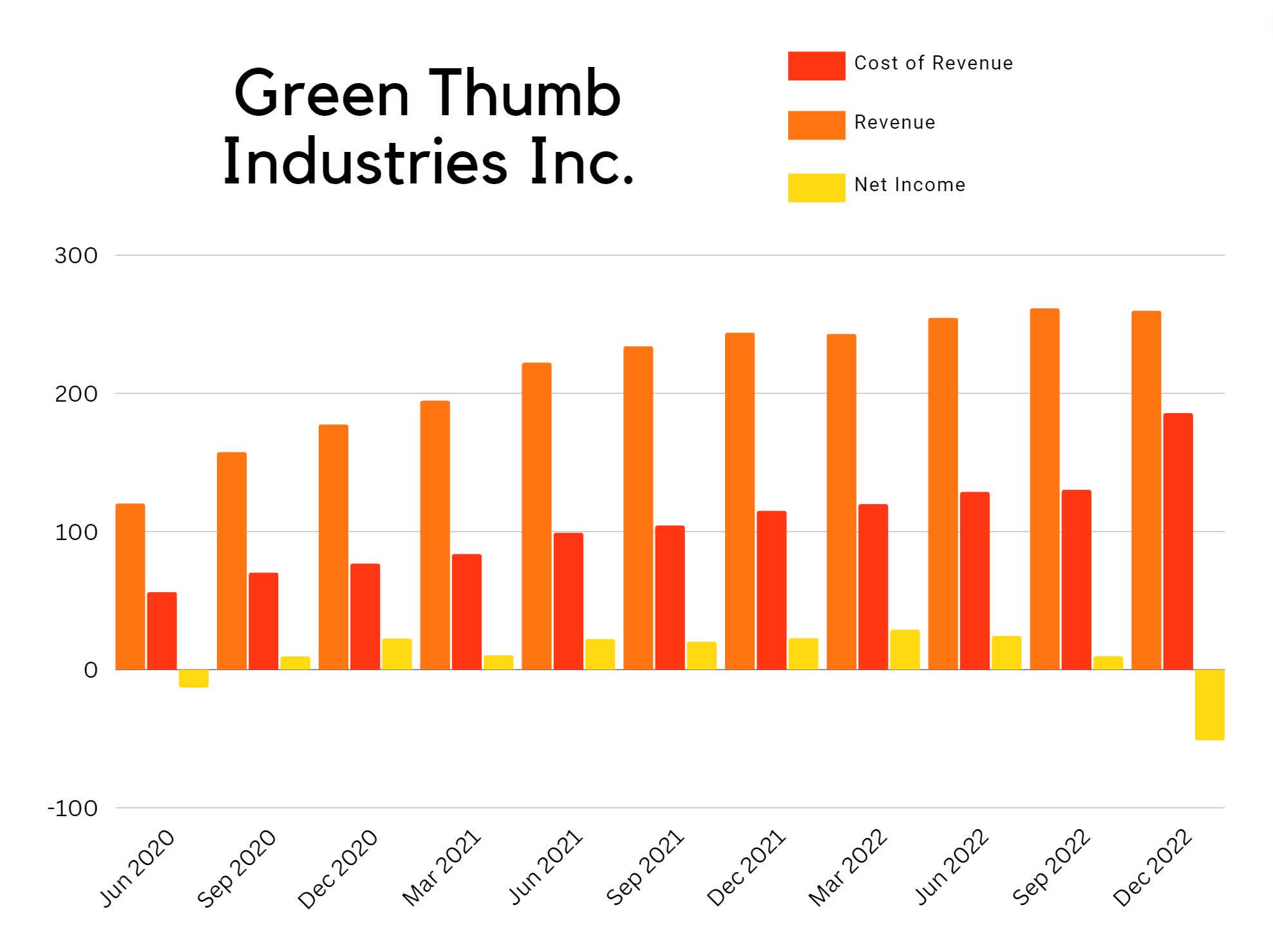

Green Thumb Industries Quarterly Revenue (Blake Downer)

{kind=link}

Financials

Fortunately for Green Thumb, they have already found a profitable business model and are in a better position to adapt than most of their competition. As of Q4 2022 , the company has $177.7M in cash on hand, generated $124M of quarterly gross profit, has $352.4M in assets, and $275.7M in debt. During 2020 and most of 2021, the company saw steady growth, during 2022 revenue growth began inflecting down as it approaches flat growth. This last quarter, the company saw a significant increase in its costs and posted a loss of $51.2M due to an $88.5M charge related to its Nevada operations.

Green Thumb Industries Q4 2022 Earnings Report

{kind=link}

Valuation

As of March 1st 2023, this company had a market cap of $1.95B and was trading at $8.40 per share. Within the last 24 hours, a new earnings report has switched this company from positive EPS to negative EPS. Because of this significant change in net income, I am disinclined to try and produce an estimate for fair value at this time. Looking over the financials and profitability, it's clear that this company is operationally viable with good margins, positive EBITDA, and steady cash flow.

GTBIF Valuations (Seeking Alpha) GTBIF Profitability (Seeking Alpha)

{kind=link}

{kind=link}

Risks

I am expecting the United States to reschedule cannabis to somewhere in the 3-5 range, but if they give it the same treatment as Tobacco or Alcohol and remove it from the list of controlled substances then Canadian producers will immediately flood the United States market with their ultra cheap cannabis and the results will be devastating for all of the US based producers.

If it gets rescheduled into the 3-5 range, then I am expecting prices in the United States to drop down toward Oregon's price levels. This should take several months to play out.

Catalysts

The removal of 280e is huge for this industry. The entire sector will immediately become more profitable.

I want to list this in the Catalysts, but really it's an anti-catalyst. The longer the US government takes on rescheduling, the better it is for Green Thumb. The company is already one of the very few that have found viability. As most of the rest of the sector is struggling in the current environment, Green Thumb has the ability to extend its already considerable operational advantage into an even further lead over the rest of the sector.

Conclusion

The company still has healthy EBITDA and cash flow. Since the $88.5M was a one time expense, any dip in perceived valuation it causes represents a buying opportunity.

If I believed that the laws and regulations in the United States were going to perpetually remain the way they are today, I would already have a significant position in Green Thumb. When the news of rescheduling hits, it is almost certainly going to cause another sector wide rally and large amounts of outside money will flow into the industry. Companies like Green Thumb are going to receive more attention because they have better fundamentals.

What Is My Plan With GTBIF?

When the news of rescheduling hits, I am going to be buying LEAPS call options on a couple of the cannabis ETFs, and also specifically on this company. Because the price war is going to take time to play out, the removal of the 280e tax obligation is going to cause a couple of extremely lucrative quarters for Green Thumb. I fully expect this company to post some incredibly impressible EPS increases, and I expect the share price to reflect that. As the price of wholesale cannabis falls, I will be watching for the sector to encounter revenue declines and margin contractions, and then I will close out my calls.

For further details see:

Green Thumb Is Widening Its Lead Over The Rest Of The Sector