PIPR - Greenhill: Weak Investment Bank With Downside Risk

2023-05-11 17:19:18 ET

Summary

- Greenhill & Co. is an independent investment bank that provides financial and strategic advisory services.

- Greenhill has been unable to grow in the last decade, seeing volatility in earnings and margins declining.

- The current bear market will only make things worse, with advisory work down and continuing to slide.

- When compared to peers, Greenhill is one of the weakest performers.

- Greenhill's current valuation suggests further downside is possible.

Investment thesis

Our current investment thesis is:

- Greenhill (GHL) has struggled to grow and gain market share in the last decade, essentially trading sideways while experiencing margin declines.

- The lack of Managing Director recruitment is a problem going forward, as it suggests the current performance will continue.

- The current bear market will act as a drag on performance. Analysts think growth will occur in FY23 but we are skeptical.

- Greenhill's forward valuation suggests it is adequately valued but we think further downside is possible if estimates are missed.

Company description

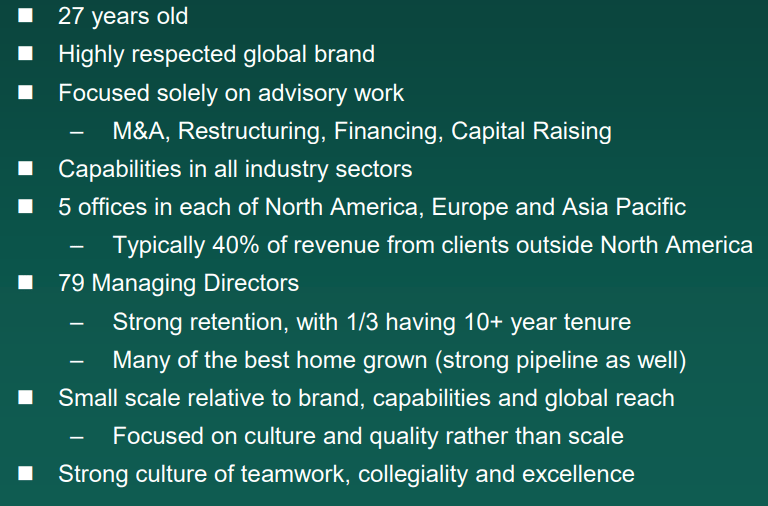

Greenhill & Co. is an independent investment bank that provides financial and strategic advisory services. Services include mergers and acquisitions, restructurings, financings, divestitures, and private capital raising.

Greenhill describes its business as follows.

{kind=link}

Share price

Greenhill's share price has lost value in the last 10 years, losing more than 80% of its value since 2013. This is a reflection of the company's inability to achieve consistent market share growth, remaining a small player in a large industry.

Financial analysis

Greenhill Financials (Tikr Terminal)

{kind=link}

Presented above are Greenhill's financial results for the last decade. As the share price reflects, the company has been unable to achieve growth, faced volatility, and has a poor bottom line.

Revenue

Greenhill's revenue has declined when comparing FY12 to FY22 but has seen periods of strong growth and decline in between. The company has been susceptible to project wins impacting the annual performance. FY21 was the peak year for the company and even if we compare growth up until that point, it is unimpressive. To contrast this, Advisors such as Houlihan Lokey ( HLI ), Evercore ( EVR ), and others have grown at over 10% annually.

It is difficult to assign a definitive answer as to why the business has underperformed for the period it has but one reason is certainly a lack of Managing Director, or MD, growth. In 20212 Greenhill had 66 MDs , a growth of 13 in 10 years. By contrast, Houlihan Lokey had 115 in 2012 and 289 by Mar22. Quality MD recruits can be highly accretive for a business, essentially "adding" a significant level of profitability each year which in theory will grow. The lack of growth in this segment has put greater pressure on the current MDs to win additional work while being able to service current clients.

In conjunction with the point above, we have seen Greenhill struggle with growing its client base. The number of >$1M clients has remained flat across the period, only breaking out of the 45-66 band once. Further, the total number of fee-paying clients has remained equally as flat. New clients in the top 10 suggest a strong ability to win work but it looks offset by churn. This supports the idea that current MDs are struggling to win in addition to the prior year's level.

{kind=link}

Both these factors are not going to change overnight, making it difficult to argue the next 10 years are not going to be like the last.

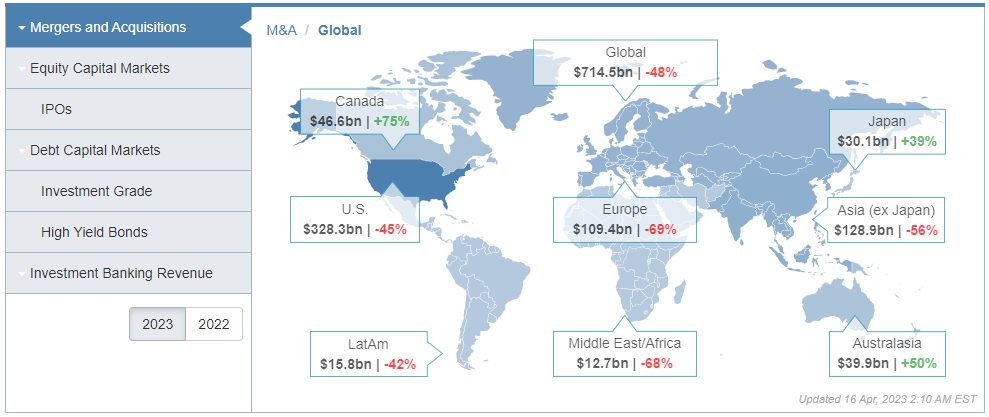

Further, Greenhill is facing market headwinds in the near term due to a slowdown in advisory activity. Inflation and recessionary fears are making investors more hesitant about transacting, and thus stringent with valuations, making getting a deal over the line far more difficult. Additionally, with interest rates rising, the cost of capital has increased, making deal financing and business financing far more expensive. Again, this acts as a deal inhibitor as investors will require compensation for the additional cost / lower valuation (future cash flows discounted at a higher rate) on the deal price. Additionally, other advisory services also take a hit due to interest rates as it becomes more difficult to finance companies, with debt markets locking many businesses out. As the following graph illustrates, M&A activity has gone in one direction since 2021.

Global M&A activity (Dealogic)

This will likely mean a further decline in revenue during FY23, with the company struggling to win work as activity declines.

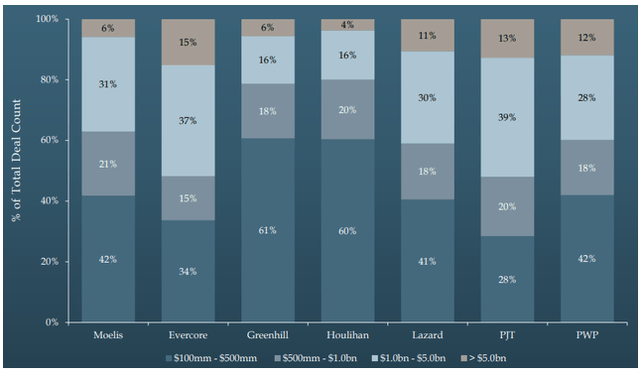

According to deal count data, Greenhill advises primarily in the $100M-$500M bracket, making it a mid-market advisor. This is generally the bucket with the most activity as the large/mega cap segment by nature has few entities that can transact and a greater amount of risk. On the other end, smaller transactions are of greater risks for other reasons, and are generally reserved for specialist investors. For this reason, the mid-market should be the most resilient.

{kind=link}

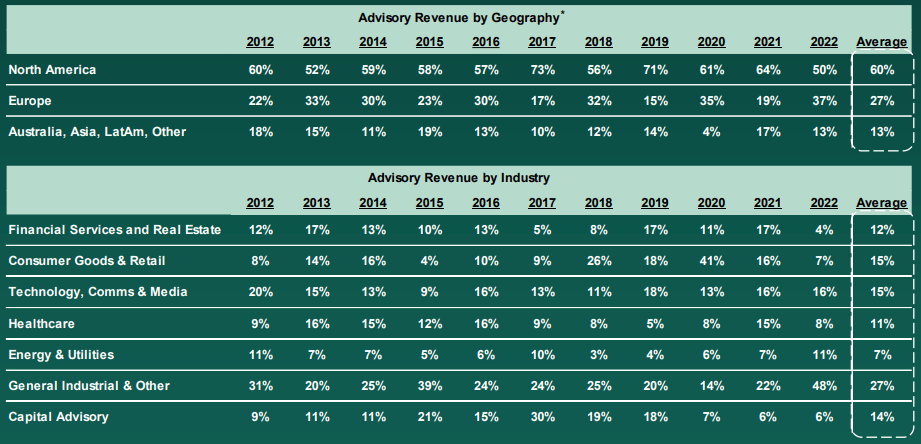

Further, Greenhill is highly diversified by industry and geography. This is beneficial as it reduces the risk of reliance on an overly exposed industry/region.

Work by geography / industry (Greenhill)

{kind=link}

As the following shows, Europe and Tech were the hardest hit by the slowdown. Both locations represent less than 30% of Greenhill's exposure, reducing the impact on the business.

M&A by region (Dealogic) M&A by industry (Dealogic)

{kind=link}

Margin

Historically, Greenhill was able to achieve strong margins, barring a few specific years. This again is a reflection of the company's volatility based on project work. Regardless, the business can achieve strong margins, despite the extremely poor results in FY22.

The primary driver of this margin tightening is the stickiness of compensation. Revenue per employee has declined $203k, yet compensation has only declined $53k. Given the stronger margins during the good years, it is likely that Greenhill's compensation strategy is likely weighted toward fixed packages, giving investors a greater return for superior gains. Compensation as a % of revenue has ballooned to 74% as a result of this, having been closer to 60% for most of the decade.

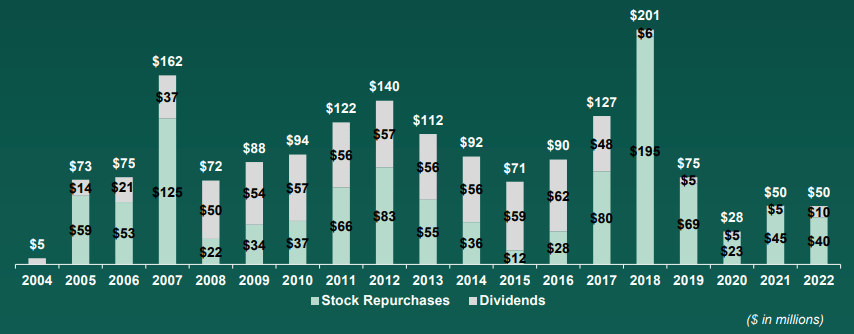

Balance sheet

Greenhill's balance sheet is fairly uneventful. The business has experienced a period of deleveraging in recent years while sustaining both buybacks and dividend payments.

{kind=link}

As the following graph illustrates, Greenhill's average diluted shares have continually declined for much of the decade.

Management's intends to maintain these distributions although it is likely that FY23 will be a soft year.

Outlook

Forecast (Greenhill)

Presented above is the consensus view on Greenhill's FY23 results. Given the uncertainty in the market, the forecasts are not to be relied on, however, can provide some directional guidance.

Interestingly, analysts are forecasting revenue growth of 23%. This goes against what the market information is suggesting. Analysts are either pricing in greater resilience in FY23, a bounce back in M&A activity, or specific deal-driven gains. The resilience could come from having a developed Restructuring practice, which is a business line that generally does well during a market downturn. If this segment can offset the soft M&A performance, growth is possible.

It should be noted that analysts had previously estimated c.$310M, with a recent downgrade in estimated value. This figure will likely continue to change.

Our view is that market conditions and the company's commercial standing imply revenue will decline further in FY23.

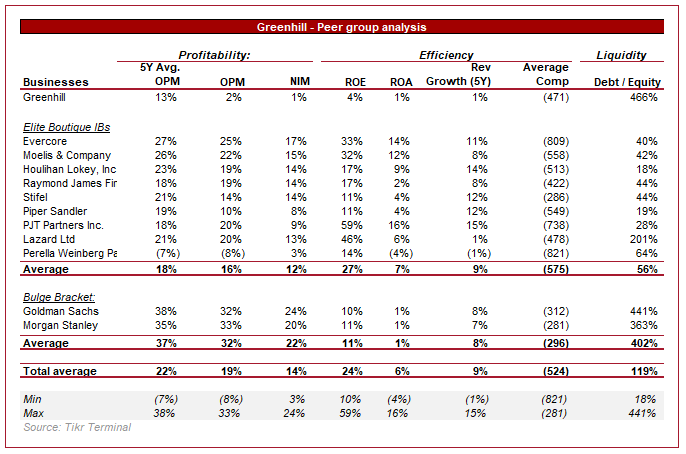

Peer comparison

Investment banks performance (Tikr Terminal)

{kind=link}

Presented above is a comparison of Greenhill to its boutique advisor peers.

Greenhill is one of the worst-performing businesses, having seen a far larger margin contraction and a lack of growth. The early decade's margins would shoot the company up the list but it remains to be seen if these levels can be reached again.

Valuation

Valuation (Tikr Terminal)

Greenhill's valuation in the LTM period has ballooned as a result of its greater-than-expected decline in earnings. On a forward basis, the company looks to be trading at a slight discount to the elite advisors, but in line with the bulge bracket. The issue we have is that the forward growth targets look difficult to achieve from our perspective, which could mean Greenhill's multiple expands but for the wrong reason.

Final thoughts

Greenhill has experienced a lost decade. While many of its peers have grown and increased market share, the company has seemingly remained flat. Further, the company has shown itself to be highly sensitive to current market conditions, grinding to a halt.

When comparing its financials to other IBs, Greenhill underperforms on every metric. Its forward valuation suggests a correct discount is applied but we are also hesitant as to whether these forward results will occur.

For further details see:

Greenhill: Weak Investment Bank With Downside Risk