GO - Grocery Outlet: A Defensive Growth Grocery Stock

Summary

- I expect value retailers to continue capturing share from traditional grocers.

- GO has a unique supply chain and operating model that is hard to replicate.

- I see GO as a defensive stock in this inflationary environment that should continue to benefit in the near-term.

Overview

My recommendation is to go long Grocery Outlet Holding ( GO ). I believe the current environment is an alignment of the stars for GO, in which it stands to benefit from raising prices and capturing share from traditional grocers. Recent quarter performance has also demonstrated the momentum that I expected from GO. So long as management does not mess up on execution, I think GO should do well in the near-term

Business description

Grocery Outlet Holding Corp. retails grocery products. GO is a differentiated, high-growth, off-price retailer of branded consumables and fresh products sold through a network of stores.

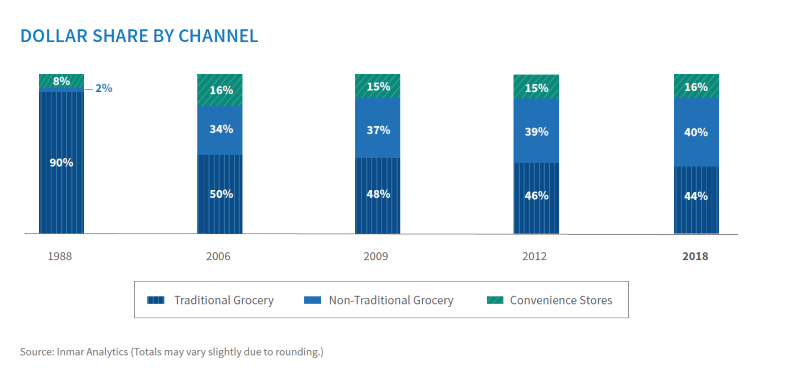

Value-oriented concept taking share in the large grocery industry

In my opinion, Grocery Outlet will continue to prosper as a result of the growing emphasis on cost-effectiveness among American shoppers. Because of this, discount stores are gaining market share across the retail industry, including in the grocery sector. The data may be a little stale, but it still shows that people prefer to shop at discount stores. The National Retail Federation reports that 89% of consumers regularly shop at discount stores. Traditional grocery player dollar share has decreased from 90% in 1988 to 44% in 2018, further indicating that traditional retailers are losing market share to non-traditional grocers (including discount retailers). These numbers, in my opinion, indicate that shoppers are actively seeking out different options, which is good news for the proliferation of discount retailers.

{kind=link}

Unique flexible buying model is the core of GO competitive advantage

GO's ability to source and distribute products quickly and cheaply sets it apart from more traditional retailers and helps it satisfy customers. Why GO can do this so well is largely due to how quickly it works. In the eyes of its suppliers, GO is an ideal business partner because of its reputation for swift decision-making, large-scale purchases, and innovative approaches to resolving suppliers' inventory problems. To elaborate, GO procure goods at steep discounts due to things like cancellation of orders, excess production, changes in packaging, and impending expiration dates.

I think this tactic is vital because it complements GO "WOW!" deals with everyday necessities to make shopping more convenient. In my opinion, this is important because it guarantees that GO provides its customers with a "whole product," meaning that they won't need to go anywhere else to get basic necessities. GO successfully keeps customers coming back to its stores and raises average purchase amounts, which is great for profits. Equally compelling is the value proposition GO provides to its supplier community. GO's model has become a preferred partner for CPG companies because it allows for the efficient and low-cost disposal of surplus and discontinued inventory without affecting brand positioning in traditional distribution channels.

Underneath these is GO's purchasing strategy, which is intentionally fluid so that the company can respond quickly to emerging opportunities. Its centralized sourcing team, which has worked closely with the industry's top consumer-packaged-goods manufacturers for decades, is responsible for carrying this out.

Independent operator model works is unique and hard to replicate

Individual GO locations are owned and operated by enterprising local businesspeople. To encourage aggressive business expansion and considerable economic upside for Independent Operators [IO], GO typically splits store-level gross profits 50/50. In order to function more effectively, IOs rely on GO's economies of scale in procurement, advanced back-end systems, and field support. In addition, while GO sets prices for all goods centrally, IOs have some leeway to modify those prices in-store based on factors like product demand and customer preferences. In terms of cost, the IOs shoulder the bulk of the store's expenses, relieving the pressure on the GO's fixed costs and protecting the business as a whole from wage inflation. I believe GO's purchasing power and corporate resources, combined with local autonomy, create a "small business at scale" model that is challenging for rivals to imitate.

One more reason I think this model is great is that GO can provide regional preferences without the need for extensive research. According to the model, IOs choose a large part of their merchandise based on local preferences, giving customers a one-of-a-kind shopping experience. As a result, GO's partnership with the IOs provides a robust sales model that enables it to provide customers with unmatched value and a distinctively personal touch.

Overall, I think the IOs and Grocery Outlet form a mutually beneficial partnership by sharing the gross profit. This helps to align the interests of both parties, which in turn encourages the owners to boost sales and cut expenses.

Competition

This is not a brand new field, so I think it's important to discuss the existing competition. GO is based in the midst of a supermarket industry that is notoriously cutthroat. When compared to other types of retail, grocery stores have lower profit margins and lower returns on capital due to factors such as the high cost of doing business and the prevalence of price-based competition.

I think supermarkets are at a disadvantage relative to their non-unionized competitors in the food retail industry because of their higher cost structures caused by the increased labor requirements associated with their staff turnover and high concentration of perishables goods. When compared to supermarkets, the labor part of SG&A is taken out of GO's IO model and replaced with a commission payment, which makes GO cost structure similar to a supermarket than other discounters. That said, my opinion is that this may present a margin opportunity for GO as it scales. Also, GO has an additional advantage over conventional supermarkets because it is not directly involved with labor unions.

Despite the fact that online grocery shopping is still in its infancy in the United States, its popularity is steadily expanding . I foresee that this trend will continue, and that the grocery industry's margins and multiples will be squeezed even more as a result. Since it is challenging to replicate the off-price strategy online due to inventory being less predictable and inconsistent across stores, I do not see a significant threat from e-commerce encroachment in the near future, especially for GO. However, I do realize that customers' preference for online shopping may ultimately reduce GO's long-term growth.

Strong SSS trends in 3Q22 suggest continuous momentum

Customers continue to respond positively to GO's deep value offering in the current inflationary environment, as evidenced by the company's third-quarter same-store sales report of 15.4%, which was significantly higher than the consensus estimate of 10.2%. This result was driven by both ticket and traffic, with traffic increasing sequentially.

Additionally, GO raised its FY22 guidance slightly, with net sales 2.3% higher versus the prior midpoint to $3.55 billion, driven by a 2.5 to 3.0 percentage point higher range for SSS to 11%. This was all thanks to the company's strong performance in the third quarter and its visibility into the fourth quarter. Even though the outlook for margins has gotten a little lower, the higher top line has resulted in an increase in guidance for adjusted EPS for FY22 to the $1.00 end of the prior range.

Forecast

I believe GO has a 35% upside. According to my model, it is worth $38.94 in FY24. In my opinion, GO is well positioned to benefit from this inflationary yet cautious environment. There are two positive effects here: (1) GO can raise prices due to inflation, and (2) GO can capture demand from traditional grocers because it is less expensive. The combination of both results in a strong SSS, which we saw in 3Q22 and which I expect to continue in the near future.

Using management's FY23 guidance and a flat growth rate over the next two years, I estimate GO will earn around $152 million in FY25. If we assume that GO will trade at the same forward PE multiple in FY24, the stock is worth $38.94, or 35% more.

Author's estimates

Key risks

Limitations to GO model

Until there is a critical mass of people familiar with the GO brand, it is possible that stores outside of the core market will have lower profitability. However, with its emphasis on low prices and the widespread success of similar off-price concepts in other markets, I think the idea will have broad appeal in new markets as well.

Inventory availability

The concept's unique selling proposition and potential differentiation could be harmed if not enough opportunistic inventory could be secured. A rise in the demand for clearance goods is another possible outcome of increased disruptions in the supply chains for conventional grocery products (which could push up prices for GO).

Conclusion

In my opinion, GO is in a favorable position right now, thanks to the favorable conditions that will allow it to increase prices and take market share from conventional supermarkets. The momentum I anticipated from GO has been on display in the most recent quarter's results as well. I expect GO to do well in the near future as long as management doesn't botch the execution.

For further details see:

Grocery Outlet: A Defensive Growth Grocery Stock