GO - Grocery Outlet: Defensive With Growth Initiate At Buy

2023-06-21 13:40:12 ET

Summary

- Grocery Outlet reported strong Q1 earnings with comp sales growth of 12.1% YoY, beating expectations with an EPS of $0.27.

- The company raised its guidance for the year, expecting comp sales growth of 5.5% and an EPS of $0.98 at mid-point.

- Its strong sourcing ability and IO model allow it to offer deep value to its customers while growing at a much faster rate.

- GO's gross margin stability and performance during recessionary periods contribute to a bullish outlook.

Investment Thesis

Grocery Outlet Holding ( GO ) is a high growth, off-price retailer focused on a varied range of consumable products offering 40-70% discounts compared to the conventional retailers. It operates 440+ stores in 8 states through a differentiated model of Independent Operators (IO) who run the stores providing personalized customer service and a localized product offering. We believe GO's high growth and deep value for money deals (through its unrivalled sourcing ability and sustained traffic), while outperforming its peers, should continue driving sustained earnings. we initiate it at Buy.

Earnings Roundup

GO reported a strong Q1 with comp sales growth of 12.1% YoY driven by increase in customers (+7.9%) along with an increase in transaction size (+3.9%). This is a stark contrast to the challenging environment that other grocery retailers seem to grapple with, as a result of weather and pullback from customers due to adverse impact of tax refunds and SNAP benefits. Gross margins improved 95 bps YoY at 31.1% driven by favorable buying and robust supply chain execution. SG&A per store increased 7.2%, a deceleration from 7.4% in Q4 22 while SG&A as % of sales remained largely unchanged, down 10 bps primarily on account of fixed cost leverage. Robust sales and improved gross margins led the company to beat the earnings expectations with EPS of $0.27, much higher than consensus expectation of $0.23.

It raised its guidance for the year following a strong quarter with sales expected to be at the higher range of its initial guidance driven by comp sales growth expected to be at 5.5% at midpoint, compared to 5.0% earlier, despite lapping a 12% comp growth in 2022. With the moderating inflation, it expects its gross margins to improve 20 bps YoY (up 10 bps than its earlier guidance) and EPS of $0.98 at midpoint (vs $0.95 guided earlier).

Why are we Bullish?

Gross Margin Stability

Food inflation has been moderating the past couple of years and is expected to moderate further down. However, GO has been able to maintain its gross margins maintaining improved sales despite challenging inflationary headwinds as a result of its superior sourcing and product pricing.

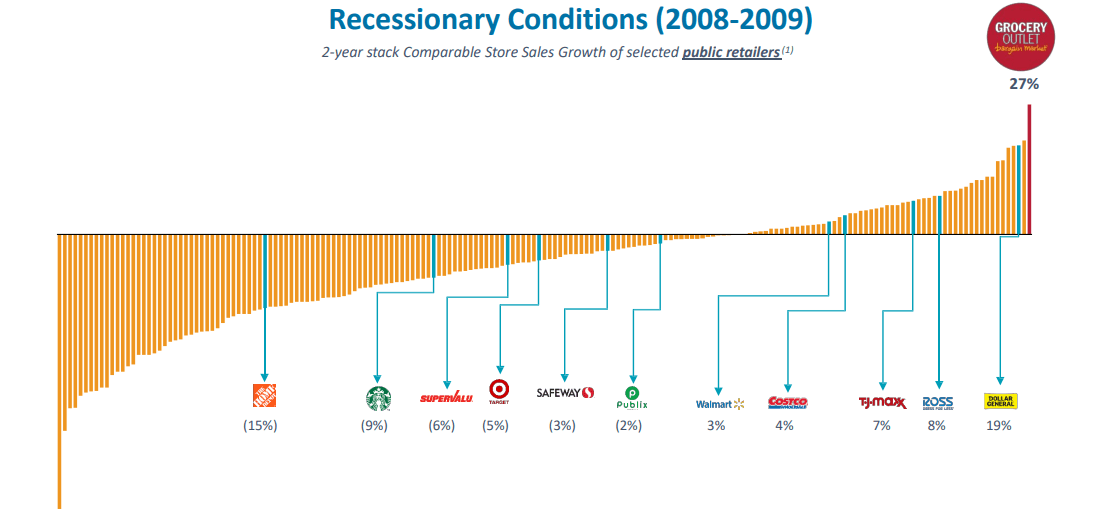

Performance during Recessionary Periods

GO has demonstrated strong performance during recessionary conditions primarily due to its off-price retail model providing consumers better value for money. It has reported comp store sales growth of 27% (on a 2 year stack basis) during the 2008-09 period, outperforming its peers by a huge margin.

{kind=link}

Sourcing Excellence

GO's flexible sourcing acquiring merchandise at substantial discounts that regularly arise from order cancellations, manufacturer overruns, packaging changes and approaching “sell-by” dates allows them to procure at substantial discounts to other retailers. It perfectly complements its WOW deals with everyday staples providing a convenient shopping experience.

Unique Independent Operator Model

GO's stores are owned and operated by individual entrepreneurs providing tailored product offering and personalized customer support sharing 50% of store level gross profit. GO's strong sourcing ability along with advanced back end and field support enables to create small business at scale model which makes it unique and difficult to replicate. In addition, the model is insulated from store labor related variability as IOs employ the store workers directly resulting in lower corporate fixed costs providing further protection during inflationary period or periods of economic uncertainty, like the current times.

Significant Whitespace Opportunity

GO's current presence is relatively smaller at 440+ stores limited to 8 states. However, it has immense growth potential as it densifies its network globally with a long term market potential of 4,800 (more than 10x of its current network) which can potentially have a significant impact for growth going forward. Its benign cost of ~$2 mn for cash investment to operate a store with a payback period of 4 years bodes well for the growth at scale.

Valuation

GO trades at a premium to food staples players while slightly in line with another set of larger consumable players such as Walmart (WMT) and Costco (COST).

We believe the premium valuation is justified due to its strong operational execution and unique business model with its ability to generate higher growth. Initiate it at Buy.

Risks to Rating

Risks to rating include 1) GO operates in a highly competitive food and discount retail industry and any competitive pressure would hurt sales and its ability to defend margins 2) GO's strength remains in product sourcing and any disruption among the supply chain would have a significant impact on the company's positioning and offering better value for its customers 3) its ecommerce business is materially insignificant and a consumer shift to e-commerce for groceries would have an adverse impact on the sales 4) the IO model is relatively unknown beyond the few states it operates in and it may face significant challenge attracting new IOs as it expands in newer states

Final Thoughts

GO operates in a grocery retail setting through a differentiated IO model with an excellent sourcing model, enabling them to offer ~40% discounts on its products compared to other retailers - deepening its customer base. Its performance during recessionary periods remains phenomenal as it attracts consumers who are looking for better values as demonstrated during 2008-09 period. We initiate this at Buy given GO's unique and hard to replicate IO model, opportunistic sourcing abilities delivering value and consistent margins and significant unit growth opportunity as it densifies outside of the 8 states that it currently operates in.

For further details see:

Grocery Outlet: Defensive With Growth, Initiate At Buy