GO - Grocery Outlet Holding: Splendid Q2 And Momentum Into Q3 Support Near-Term Growth Outlook

2023-08-18 02:22:05 ET

Summary

- Grocery Outlet Holding's 2Q23 performance was strong, with revenue up 12.5% and gross profit up 32.3% year-over-year.

- GO's value proposition appeals to customers across all income levels, indicating a large addressable market.

- The robust Independent Operator pipeline and high operator satisfaction bode well for future expansion and overall company health.

Summary

Following my coverage on Grocery Outlet Holding ( GO ), I recommended a buy rating due to my expectation that GO will benefit from raising prices and capturing share from traditional grocers. This post is to provide an update on my thoughts on the business and stock. I reiterate my buy rating as GO's 2Q23 performance was splendid, and forward-looking comments were also very encouraging on growth in the near term.

Investment thesis

GO's 2Q23 results were $1.01 billion in revenue (up 12.5% y/y), a gross profit of $326 million (up 32.3% y/y), and an adjusted EPS of $0.32, which was above the consensus estimate of $0.26. After this quarter, I feel even more strongly that GO's unique business model is striking a chord with consumers. SSS's continued strength is the most important piece of information. SSS for 2Q23 came in at 9.2%, driven primarily by traffic, and showed gains in both middle- and upper-income customer cohorts, as well as gains in both trip frequency and wallet share from its existing base. The thing to note here is that its value proposition doesn't just appeal to low-income groups, as GO's strong growth was seen across all income levels. In other words, this reinforces my belief that the GO addressable pool of customers is a lot larger than I expected (lower-income customers). When it comes to relatively new markets, GO has also been doing exceptionally well, with Southern California and the Middle Atlantic continuing to deliver comps better than GO on an overall basis. With the help of strategic marketing, flawless IO execution, and a greater concentration of stores, the Eastern region should also begin to show robust growth, driving top-line growth. Given the positive momentum and sustained strength in traffic that have been signaled by SSS's management, I anticipate another strong 3Q for the company.

We're really pleased with the start to the third quarter. And again you can think about comp dynamics that we saw in the second quarter really continuing to traffic continues to be very strong (2Q23 earnings results call)

The excellent SSS performance resulted in a high gross profit as well. The combination of efficient operations and a buying climate that encouraged growth across all product lines led to a 120bps y/y increase in gross margin to 32.3%. As a result of the positive performance and momentum in Q3, management raised their gross margin guidance for FY23 by 60bps to 31.3%. The increase in guidance is clearly a show of confidence and strength, in my opinion. With this kind of momentum, I anticipate continuing help with gross margin from closeout purchases as a result of supply chain difficulties and rising supply as previously forced shutdown supply lines come back online.

Independent Operator [IO], a key engine that drives GO's expansion, is holding up admirably. The average IO's net income increased by a low single digit CAGR between 2019 and 2022, while the net income of the average mature IO was over $250,000 in 2022. The rate at which GO can expand is, to some extent, dependent on IO's state of health. As a result, IO satisfaction is a strong predictor of overall health (beyond just money).

Current operator satisfaction and engagement levels are high and voluntary turnover remains consistently low. (2Q23 earnings results call)

The business also boasts a robust IO pipeline, which grew by 30,000 leads in just a single year, or a whopping >50% growth over the past 4 years. As a result, I don't think GO will have any trouble locating competent IO to launch further retail outlets. Additionally, this demonstrates that ROI>WACC can be achieved at the store level, which is crucial from an IO's point of view.

Valuation

Own calculation

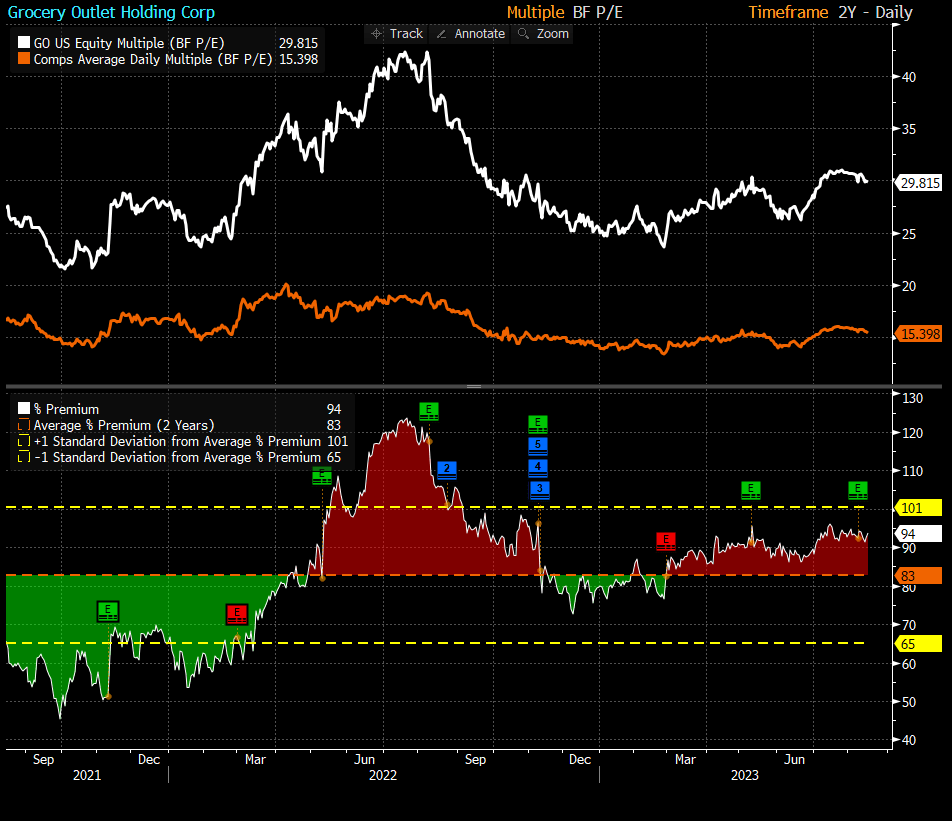

I believe the fair value for GO based on my model is $44.50. My model assumptions are that GO can continue to grow at 10% for the foreseeable future, which is consistent with how it was growing pre-covid. GO has consistently executed at this level of growth, so I do not see much variability in this, especially with current SSS momentum, new market performance, and IO health. Given this stability in growth, resiliency in this macro environment, growth potential, and lower leverage, GO should continue to trade at a premium to peers. I modeled GO to continue trading at 29x forward PE in FY24. My price target is $33.90.

Peers include Sprout Farmers, Kroger, Natural Grocers, and Albertsons Cos. The median forward PE multiple peers are trading at is 15.4x, the expected 1Y growth rate is 5% while GO is double that at 10%, and the debt to equity ratio is 1.33x while GO is at 1.17x.

{kind=link}

Risks

Both foot traffic and sales at GO could decrease if consumers cut back on their spending or if competition steps (increased promotional activity) up from low-priced retailers (like Aldi), traditional supermarkets, big-box retailers, and warehouse clubs increases.

Conclusion

My outlook for GO remains positive based on its impressive 2Q23 performance and the promising trajectory into 3Q23. The robust financials, including substantial revenue growth and elevated gross profit, reinforce the effectiveness of GO's unique business model across diverse income levels. Notably, sustained strong SSS and successful expansion into new markets, particularly Southern California and the Middle Atlantic, underscore the company's growth outlook. The management's increased gross margin guidance for FY23 reflects confidence in the ongoing momentum.

For further details see:

Grocery Outlet Holding: Splendid Q2 And Momentum Into Q3 Support Near-Term Growth Outlook