GO - Grocery Outlet: Low-Risk Growth Through Intriguing Strategy

2023-10-31 02:02:44 ET

Summary

- Grocery Outlet operates independent grocery stores with a focus on low-price groceries.

- The company's strategy is intriguing as it relies on independent store operators but centralized CapEx and corporate functions, as well as central sourcing.

- Grocery Outlet's business model is highly resistant to macroeconomic turbulence because of the low pricing and a low-risk grocery market industry.

- The stock seems to be priced fairly when considering Grocery Outlet's prospects.

Grocery Outlet Holding Corp. ( GO ) operates independent grocery stores in the United States. The company focuses on providing low-price groceries through independently operated grocery stores, making Grocery Outlet an incredibly low-risk stock. The company is focusing on growing through new store openings. As a very low-risk stock, Grocery Outlet’s investors aren’t going to look at a very high return. In this text, I analyze the stock’s valuation through a DCF model to determine whether the current risk-to-reward seems intriguing.

The Company & Stock

Grocery Outlet differentiates itself from competition with aggressive pricing. The company’s strategy revolves around extreme value – Grocery Outlet prides itself in providing good value to customers through a well-structured purchasing team. The company has good long-term supplier relationships with suppliers such as General Mills, Nestle, Unilever, Chosen Foods, Quest Nutrition, and Chobani; the suppliers are a mix of well-known and emerging names.

Grocery Outlet's Pricing Strategy (Grocery Outlet August Investor Presentation)

{kind=link}

The company’s operating model relies on independent store operators. Grocery Outlet is responsible for corporate expenses, rent, central inventories, sourcing, real estate, logistics and initial pricing. On top, Grocery Outlet is responsible for capital expenditures in the process of a store opening, making the company’s growth quite CapEx-heavy. On the other hand, Grocery Outlet’s chosen independent operators are responsible for daily operations in a store – for example, the operators take care of hiring, operating working capital, local marketing, managing inventories and modifying pricing as well as a specific store’s product offering. The business model makes Grocery Outlet’s operations adaptive to a single store’s local market, but creates benefits of scale through central sourcing and corporate functions.

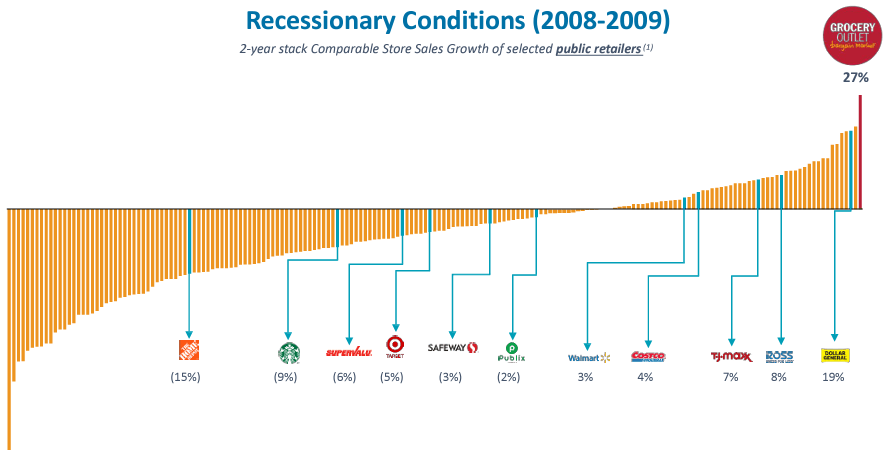

I believe that the defensiveness is a highly valuable prospect as the economy remains very uncertain. Grocery Outlet’s business model is highly resistant to macroeconomic turbulence, making the stock interesting. The company’s competitive pricing creates demand for the company in recessions, in addition to an already defensive grocery market industry. Demonstrating the defensiveness, Grocery Outlet’s performance in the great financial crisis was exceptional:

{kind=link}

After an IPO in 2019, Grocery Outlet’s stock hasn’t performed very well. The stock has fallen by about -17% in price, despite the company not paying any dividend :

{kind=link}

Financials

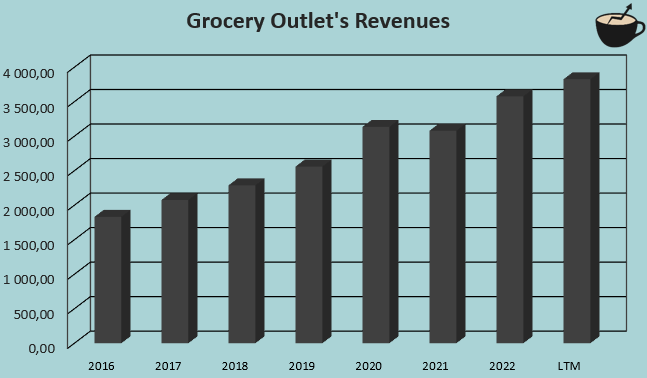

Grocery Outlet has achieved a good amount of growth in the company’s medium-term history. From 2016 to LTM figures as of Q2/2023, the company’s achieved compounded annual growth rate has been 12.0%:

{kind=link}

The achieved growth is completely organic, as Grocery Outlet doesn’t have any cash acquisitions in the company’s public financial history. Still, the achieved growth does tie up the company’s cash flows – although Grocery Outlet’s net working capital has stayed relatively stable, the company has a significant amount of capital expenditures with a trailing figure of $138 million.

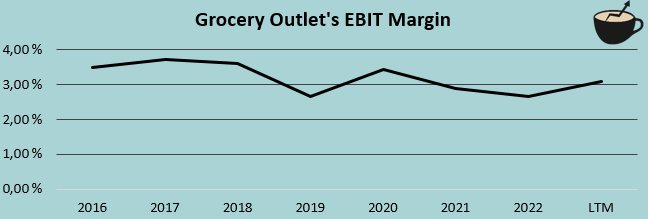

Grocery Outlet has had a very stable EBIT margin in the company’s history. From 2016 to 2022, the company’s average EBIT margin was 3.2%, with a high of 3.7% and a low of 2.7%. The margin is very thin, and has stayed surprisingly stable in the company’s history with only a single percentage point of variance.

{kind=link}

Valuation

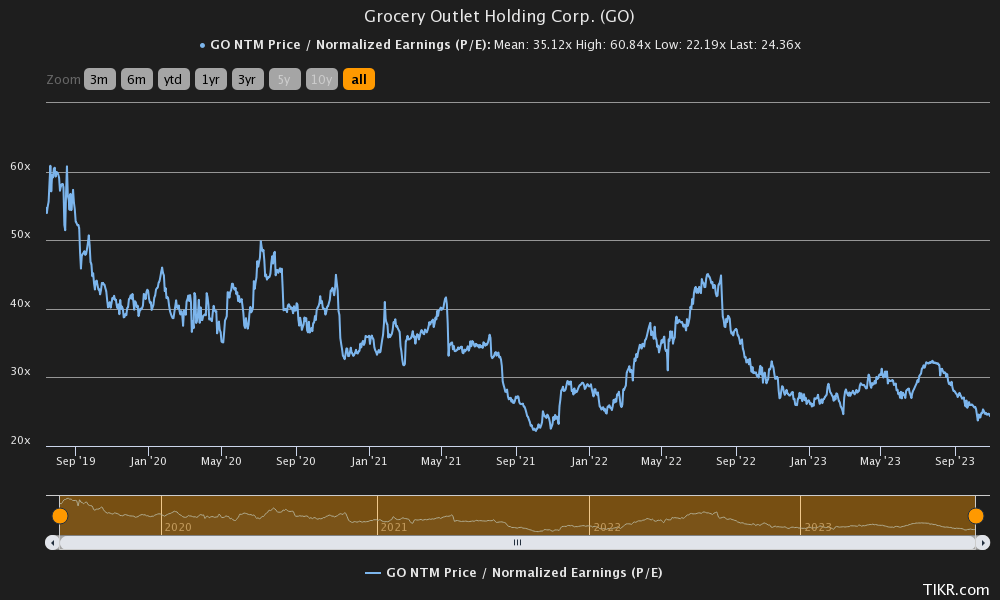

At first glance, Grocery Outlet seems very aggressively priced. The stock currently trades at a forward P/E of 24.4. Although the current ratio is below the company’s historical average, the P/E still seems high compared to most small cap companies.

{kind=link}

I believe that the P/E ratio doesn’t tell the whole story, though. Grocery Outlet’s operations are very low-risk in their nature, and the company has achieved a good amount of growth in its history through a large amount of capital expenditures.

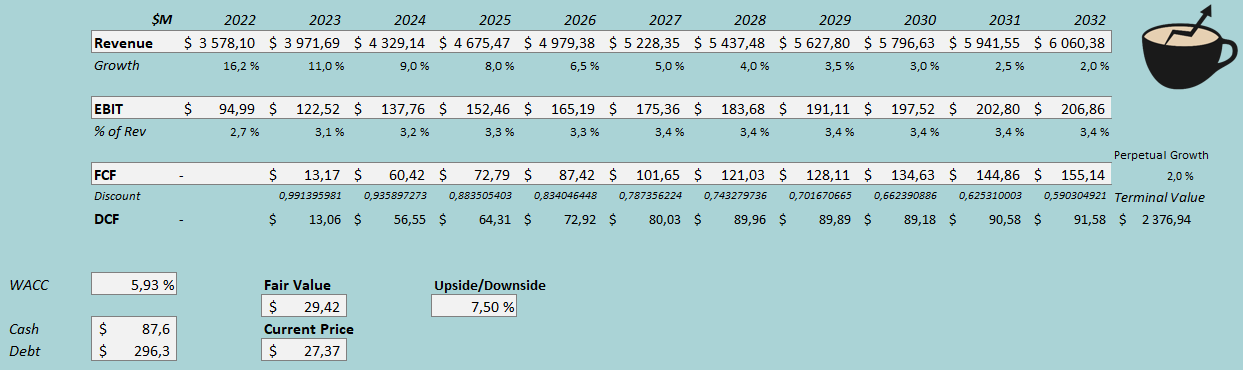

To estimate a rough fair value for the stock, I constructed a discounted cash flow model in my usual manner. In the model, I estimate a growth of 11% for the current year, in line with the company’s outlook. After the year, I estimate growth to slow down in steps into a perpetual growth rate of 2%. The estimated growth represents a CAGR of 5.4% from 2022 to 2032. Although the estimated growth is well below Grocery Outlet’s target of a 10% annual store growth, I believe that the estimate is fair – in combination with decreasing growth, I estimate the company’s capital expenditures to shrink, improving cash flows.

For the company’s margins, I don’t see a significant amount of pressure into either direction. I still estimate a very slight amount of operating leverage in the future as Grocery Outlet’s operations scale – I approximate the margin to rise into a level of 3.4% from the estimated 2023 figure of 3.1%. Grocery Outlet operates at thin margins due to the aggressive pricing and independent store operators, so I don’t see a significantly higher margin as likely.

I estimate Grocery Outlet’s cash flow conversion to start improving as the growth slows down. For 2024, I still estimate the cash flow conversion to be quite poor as I estimate a growth of 9%, requiring a significant amount of capital expenditures. The cash flow conversion improves in steps into a good one as store growth slows down into mostly a halt in the model. The mentioned estimates along with a WACC of 5.93% craft the following DCF model with a fair value estimate of $29.42, 7.5% above the price at the time of writing:

{kind=link}

The used weighed average cost of capital is derived from a capital asset pricing model:

CAPM (Author's Calculation)

In Q2, Grocery Outlet had $6.2 million in interest expenses. With the company’s current amount of long-term debt, the company’s interest rate comes up to an annualized figure of 8.33%. Compared to Grocery Outlet’s very low-risk operations and stable cash flows, the company leverages debt very conservatively. For Grocery Outlet’s long-term debt-to-equity ratio, I estimate a figure of 15%.

For the risk-free rate on the cost of equity side, I use the United States’ 10-year bond yield of 4.90% . The equity risk premium of 5.91% is Professor Aswath Damodaran’s latest estimate for the US, made in July. Yahoo Finance estimates Grocery Outlet’s beta at 0.08 , demonstrating the company’s very low-risk operations. Finally, I add a liquidity premium of 0.5% into the cost of equity, crafting the figure at 5.87% and the WACC at 5.93%. Notably, the CAPM estimates Grocery Outlet’s cost of debt to be higher than the company’s cost of equity.

Takeaway

Grocery Outlet’s business model is very intriguing. The company’s independent store operator model has positioned the company for revenue growth through significant capital expenditures. As Grocery Outlet’s operations aren’t affected by macroeconomic turbulence in a notable manner, I believe the stock is very low in risk. The current price reflects the low risk and growth, though; as my DCF model estimates the stock to be nearly fairly valued, I have a hold rating for the time being.

For further details see:

Grocery Outlet: Low-Risk Growth Through Intriguing Strategy