GO - Grocery Outlet: Strong Trends But High Valuation

2023-06-21 07:20:16 ET

Summary

- Grocery Outlet continues to demonstrate solid business growth and operating margins.

- Decreasing food inflation could put pressure on revenue growth rates throughout 2023.

- I believe that at the moment Grocery Outlet stock is still highly valued relative to peers and do not see additional growth catalysts.

Introduction

Shares of Grocery Outlet Holding ( GO ) have fallen 1% YTD. While the company is showing both strong top-line growth and operating margin growth, I don't think this is the best time to buy due to the company's relatively high valuation on multiples.

Investment thesis

In my personal opinion, the company is still fairly valued relative to historical data and peers. I believe that the current share price already includes quite optimistic financial forecasts, so at the moment I do not see additional catalysts for growth that could drive the share price higher. However, I can't stick to a Sell recommendation at the moment, as the company is showing solid and strong results, and industry trends or management comments do not indicate significant risks to growth or a decrease in profitability.

Company overview

Grocery Outlet Holding is an extreme value retailer of fresh products. According to the results of the 1st quarter of 2023, the company operates 444 stores. The company operates in the US market in such states as: California, Washington, Oregon, Pennsylvania, Idaho, Nevada, Maryland and New Jersey

1Q 2023 Earnings Review

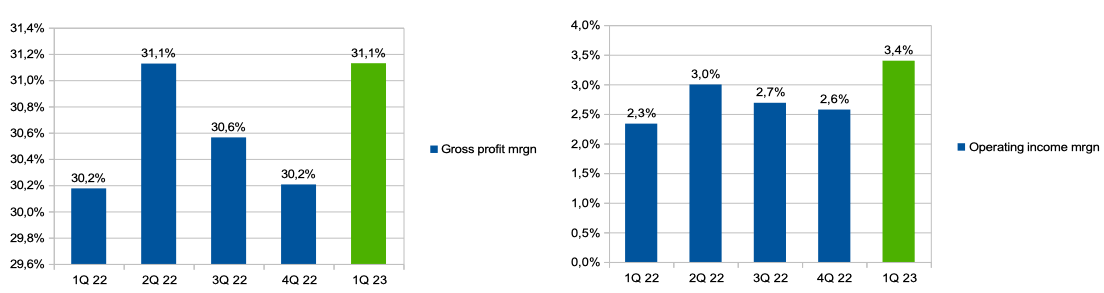

The company's results for the 1st quarter of 2023 turned out to be better than investors expected. The company's revenue increased by 16.1% YoY to $965.4 million driven by a 12.1% increase in comparable sales due to a 7.9% increase in the number of transactions and a 3.9% increase in average ticket. In addition, we see an increase in gross margin from 30.2% in Q1 2022 to 31.1% in Q1 2023.

The company's operating expenses (% of revenue) decreased from 27.8% in Q1 2022 to 27.7% in Q1 2023. Thus, operating margin increased from 2.3% in 1Q 2022 to 3.4% in 1Q 2023. You can see the details in the chart below.

{kind=link}

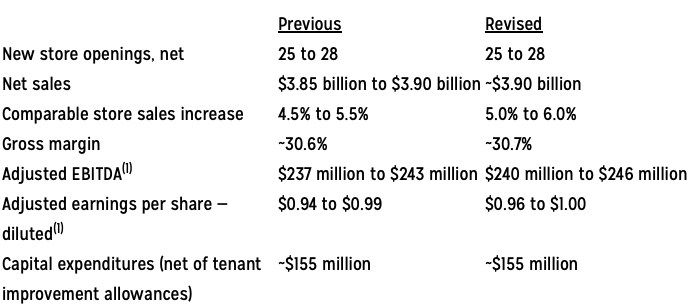

In addition, the company slightly revised its guidance for 2023 upwards. You can see the details in the chart below. I like that the company has raised its expectations for comparable sales and gross margins.

{kind=link}

My expectations

In line with management comments during the Earnings Call following the release of Q1 2023 results , the company expects inflation to slow during 2023. Despite the fact that the main growth driver of comparable sales is the growth of traffic in the network's stores, I believe that the decline in inflation may lead to some pressure on the growth rate of revenue and the attitude of investors, since the company's shares are valued quite expensive relative to peers.

Personally, I maintain relatively high expectations for the company's results for the next quarter, as we see both strong traffic trends and yet no deflation. In addition, the company is successfully maintaining a stable level of operating profitability and providing investors with relatively strong guidance for 2023. However, in my personal opinion, investors are already factoring in strong expectations in their valuations, which is why the stock is quite expensive. As such, I don't see any additional significant drivers that could help the stock outperform the broad market index, so I'm sticking with the HOLD recommendation for the stock.

Risks

Revenue growth: declining inflation could put pressure on sales growth as the company operates in a traditional segment and targets price-sensitive consumers. Although at the end of the 1st quarter, the largest contribution to the growth of comparable sales was made by the growth of traffic in the stores of the network, inflation is still one of the main drivers of growth in revenue per 1 square meter of business selling space

Value proposition: in my personal opinion, companies that operate in the value retail segment provide a smaller set of SKUs than classic stores. Thus, a change in consumer preferences due to growth in real incomes or consumer confidence can have a negative impact on traffic, and, consequently, the dynamics of revenue in the stores of the chain.

Valuation: a high valuation of the company in accordance with multiples, in my opinion, creates additional downside risks in case the company demonstrates a slowdown in growth rates or a decrease in operating profitability.

Competition: increasing competition in the sector, the emergence of new players may lead to additional marketing costs or the need to invest in prices, which may have a negative impact on operating margins in the future.

Drivers

Revenue growth: expanding into new geographies, opening new stores, growing traffic in the chain's stores and the ability to pass on inflation to the end consumer may support revenue growth. In addition, the company also considers the e-commerce format as a potential revenue driver in the future, at the moment the share of sales through DoorDash, Uber Eats and Instacart is extremely low, so the company does not disclose this.

Margin: The company is planning to launch a new ordering platform later this year, which could improve operating margins by improving the efficiency of internal processes. In addition, an increase in business volumes can lead to an increase in profitability due to the leverage effect, since a significant part of operating expenses is fixed (distribution).

Valuation

Despite the fact that the company operates in a stable segment, showing growth in revenue and an increase in operating margin, in my personal opinion, the company's shares are currently valued quite expensively.

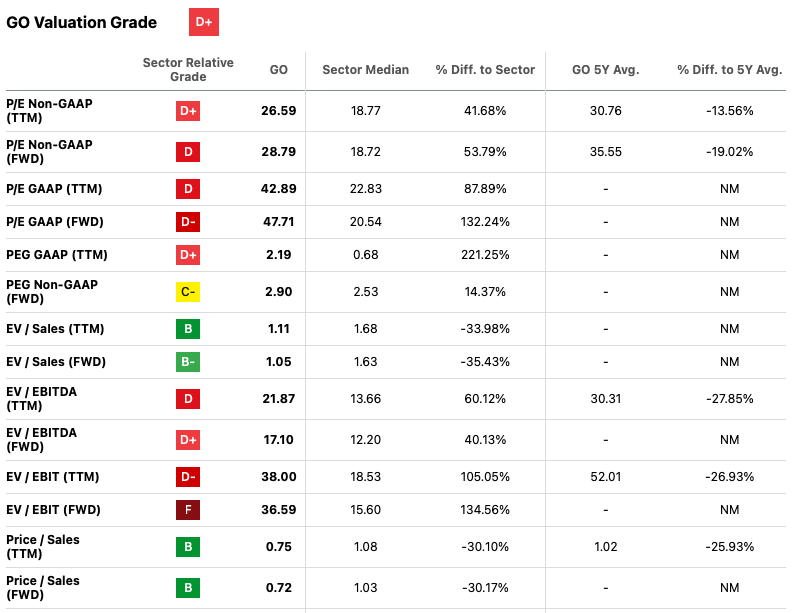

I believe that the most optimal multiples for valuing companies from the traditional sector are P/S, P/E and EV/EBITDA. So, I compared the current level of the company's valuation with the valuation of peer companies. Grocery Outlet is currently the most valuable company and I don't see any significant drivers that could push the stock price higher or outperform the broader market given the current valuation. You can see the details in the charts below.

{kind=link}

{kind=link}

Conclusion

Despite the fact that I like the company and its business model, I do not currently recommend going long. The company operates in the traditional sector, where at the moment we do not see strong pressure from macro headwinds, as the business is focused on underlying demand. Also, the business continues to outperform its competitors in terms of growth and operating margins, so I can't stick to Sell's recommendation. So, at present, my HOLD recommendation is based on the fact that although the current business model is well positioned for current trends in the consumer market, however, I believe that the market estimates future cash flows quite expensively and I see no potential for further growth in quotations.

For further details see:

Grocery Outlet: Strong Trends But High Valuation