GRWG - GrowGeneration: Pressure On Revenue Growth And Margins Resumes

2023-09-11 05:42:17 ET

Summary

- The company's revenue decreased by 10.1%, while adjusted operating loss (% of revenue) decreased to 10.3%.

- Lower guidance for 2023 due to weak demand and lower scale effects could continue to put pressure on operating margins.

- At the moment, I do not see additional catalysts for stock price growth in the coming quarters.

Introduction

Shares of GrowGeneration (NASDAQ: GRWG ) have fallen 21% YTD. Since my post arguing that it's still not a good time to go long, stocks have risen 0.6%, while the S&P 500 has gained 2.5%. In my article, I would like to analyze the company's financial statements and update my view on the stock.

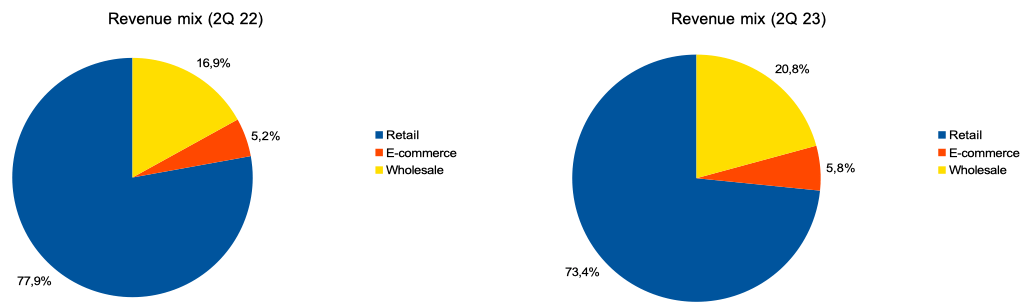

GrowGeneration company is engaged in the production and sale of hydroponics. The main revenue segments are retail (73% of revenue), e-commerce (6% of revenue) and wholesale (21% of revenue). The company operates in the US market.

Investment thesis

On the one hand, I like the company's business model, market positioning and current valuation level. Thus, despite pressure from demand, the high volume of cash on the balance sheet ($71 million), as well as low cash burn and the absence of debt load allow the company not only to invest in the expansion of new products, but also to consider potential M&A transactions. However, on the other hand, despite the relatively low valuation in accordance with multiples, I do not see additional growth drivers/catalysts in the next few quarters. As such, I expect we will see continued pressure on both revenue growth and operating margins in the coming quarters.

2Q 2023 Earnings Review

The company reported worse than investors expected . The company's revenue decreased by 10.1% YoY . The largest contribution to the decline in revenue was made by the retail segment, where sales decreased by 15% YoY due to a decrease in comparable sales by 15.1% YoY, while in the e-commerce and wholesale segments the company showed revenue growth by 1% and 10%, respectively.

{kind=link}

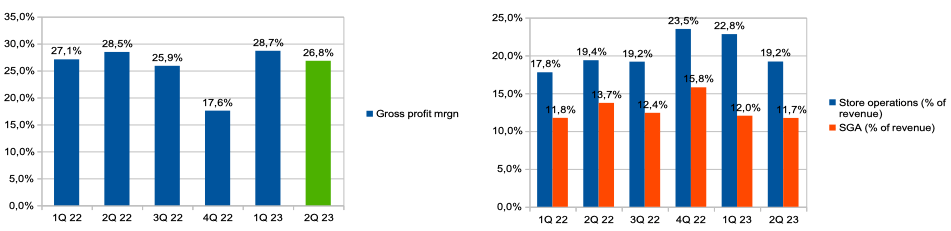

Gross profit margin decreased from 28.5% in Q2 2022 to 26.8% in Q2 2023. SGA expenses (% of revenue) decreased from 13.7% in 2Q 2022 to 11.7% in 2Q 2023, while store operations expenses (% of revenue) decreased from 19.4% in 2Q 2022 to 19.2% in the 2nd quarter of 2023.

Gross profit margin & op. expenses (% of revenue) (Company's information)

{kind=link}

Thus, the adjusted operating loss (% of revenue) decreased from 12.6% in the 2nd quarter of 2022 to 10.3% in the 2nd quarter of 2023.

adj. operating loss (% of revenue) (Company's information)

Separately, I would like to note the fact that the company’s management has lowered its guidance for 2023 due to lower expectations for sales volumes. You can see the details in the graph below.

{kind=link}

My expectations

I believe the business's revenue growth rate will continue to be under pressure because consumers continue to experience pressure from macro headwinds. Additionally, I don't think we could see a quick recovery in consumer spending if inflation slows because consumers will continue to face higher costs for interest payments, rent, and food. In the previous section of my article, I already wrote that the company lowered its guidance for 2023, but if we pay attention to expectations for the second half of the year, we will see that the current guidance implies a decrease in revenue by 17% - 21% relative to 2H22.

While we are pleased with our second quarter results, we have not yet seen the industry improvements in the third quarter to-date that we initially expected.

Additionally, I don't expect that we can see a solid increase in profitability. First, despite the fact that the company is focused on increasing the share of private labels as one of the sales drivers, I believe that this process is long-term, so I do not expect that we can see support for profitability due to the increase in share private labels in the coming quarters. The share of private labels at the end of the 2nd quarter of 2022 was 15%, while in the previous quarter the share was 16.1%. Secondly, the company will continue to face reduced economies of scale, since about 73% of revenue comes from the retail segment, where a high proportion of operating expenses (rent and salaries) are fixed.

Risks

Regulation: regulatory restrictions may slow the pace of new store openings in new states, which could have a negative impact on revenue growth in subsequent quarters.

Margin: reduced economies of scale may contribute to lower operating profitability of the business.

Macro (general risk): a decrease in real income due to high inflation can lead to both a decrease in traffic and a decrease in the average check in the chain stores.

Drivers

Margin: launching a new ERP system can allow a company to reduce logistics and freight costs in the future, which can help increase the operating profitability of the business. In addition, increasing the share of own brands can also have a positive impact on the level of gross profit margin.

Revenue: increasing sales channels, launching new products (gardening sections in stores and restoring traffic in chain stores may lead to an increase in revenue growth in the future.

Valuation & Conclusion

Valuation Grade is B. In accordance with the EV/Sales ((Fwd)) and P/S ((Fwd)) multiples, the company is trading at 0.8x and 0.9x, respectively, which implies a discount to the sector median of about 33% and a premium to sector median about 2%, respectively. Although the stock is not expensively priced, I believe the lack of clear growth catalysts (recovery in revenue growth, operating breakeven, regulation) may limit the stock's upside potential in the coming quarters.

I avoid a sell recommendation on the stock as the company is relatively cheaply priced, so I believe there is limited downside potential. However, I expect the company's financial performance to continue to be under pressure in the coming quarters, while I do not see additional growth catalysts, so I would like to maintain my hold recommendation.

For further details see:

GrowGeneration: Pressure On Revenue Growth And Margins Resumes