GRWG - GrowGeneration: Still Not The Best Time To Buy The Dip

2023-06-24 05:12:06 ET

Summary

- GrowGeneration shares have dropped 18% YTD, but it is not the best time to go long due to uncertainty in future trends.

- The company's focus on reducing costs and increasing profitability may not be enough to make an investment decision to buy shares, as significant optimizations were already made in 2022.

- Investors should wait for results over the next few quarters to see if the market stabilizes and if the company can demonstrate improvement in operating margins.

Introduction

GrowGeneration ( GRWG ) shares have dropped 18% YTD. Despite the fact that the shares of the company are relatively inexpensive, I believe that it is still not the best time to go long due to, in my personal opinion, the uncertainty of future trends.

Investment thesis

In my personal opinion, despite the company's strategy to improve operating margins, we may still see pressure in the coming quarters, as most of the business is still in the retail segment, where same store sales are low and fixed operating expenses are high on wages and rent can lead to a deleverage effect. In addition, the work to significantly reduce operating costs has already been done in 2022, so I do not see the potential for further cost optimization in the following quarters.

Company overview

GrowGeneration is engaged in the production and sale of hydroponics. The main revenue segment is the retail segment, however, the company also sells in the e-commerce and wholesale segments. According to the results of the 1st quarter of 2023, the company has 55 retail stores, the company operates in the US market in 17 states.

1Q 2023 Earnings review

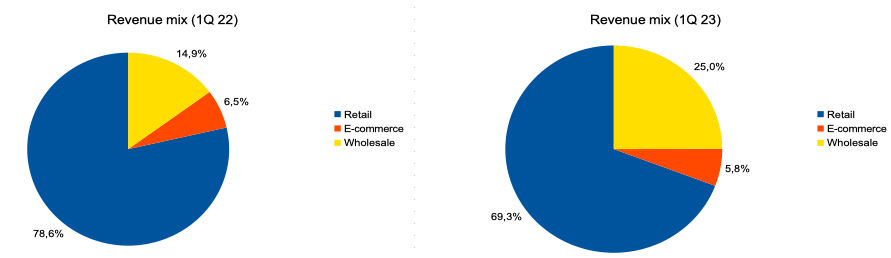

The company reported bet ter than investors expected. Revenue decreased by 30.5% YoY to $56.8 million due to a 36.6% decrease in same store sales: YoY. The retail and e-commerce segments made the largest contribution to the decline in revenue, where revenue decreased by 39% YoY and 38% YoY, respectively, while in the wholesale segment, revenue increased by 16.4%. Thus, the share of revenue from the wholesale segment increased from 15% in Q1 2022 to 25% in Q1 2023. You can see the details in the chart below.

{kind=link}

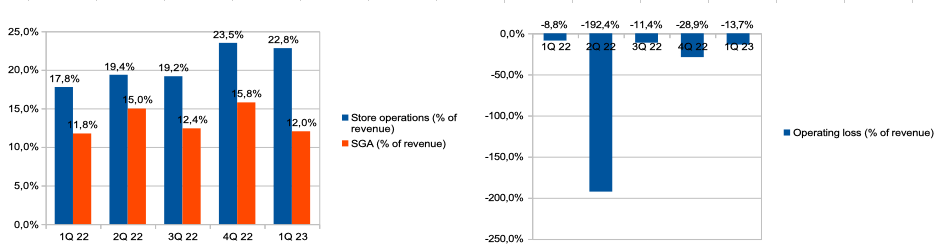

Gross profit margin increased from 27.1% in Q1 2022 to 28.7% in Q1 2023. SGA spending (% of revenue) increased slightly from 11.8% in Q1 2022 to 12% in Q1 2023, while store operations (% of revenue) increased slightly from 17.8% in Q1 2022 to 22.8% in 1Q 2023 due to reduced business scale and deleverage effect, as part of operating expenses related to stores is fixed. Thus, operating loss (% of revenue) increased from 8.8% in Q1 2022 to 13.7% in Q1 2023.

{kind=link}

According to the results of the 1st quarter of 2023, the amount of cash on the company's balance sheet is $72 million, there is no debt.

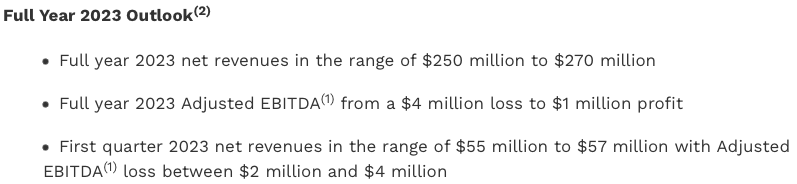

Management reaffirmed the guidance it provided earlier based on 2022 results. Management expects consistent improvement in revenue and margin dynamics throughout 2023.

{kind=link}

My expectations

On the one hand, I like the company's strategy, which focuses on revenue growth and improving business profitability. Thus, the management plans to continue increasing the share of private label brands, which should support the gross margin level in the retail segment in the next quarters. In addition, I believe that perhaps we can see new M&A transactions at an attractive price.

On the other hand, I would like to point out the following facts. First, despite improvements in the gross margin, we still see pressure on operating margins. According to the results of the 1st quarter of 2023, the share of the retail segment is about 70% of the company's total revenue, since most of the operating expenses associated with servicing the chain's stores are fixed (rent, salary). Thus, reduced economies of scale due to weak demand in the industry may continue to put pressure on the consolidated profitability of the business.

Secondly, despite the company's focus on reducing costs and increasing profitability, I do not think we will see a significant reduction in operating costs during 2023, as the company has already made significant optimizations in 2022. This is confirmed by the words of the company's management during the Earnings Call following the results for the 1st quarter of 2023.

As the company reduced its expense base by over $20 million in 2022, we are not forecasting further significant reductions in 2023.

Thus, I admit that we will see some improvement in profitability trends during 2023, however, in my personal opinion, this will not be enough to make an investment decision to buy shares.

Risks

Margin: a slowdown in the introduction of new private label brands could put pressure on the gross margin. In addition, tax increases in the industry may have a negative impact on the net profit of the business and reduce the interest of potential investors in the company's shares.

Macro (general): high inflation and a decline in real disposable income may contribute to a decrease in demand for the company's products, which may have a negative impact on both business growth and profitability due to reduced economies of scale.

Drivers

Margin: increasing the share of private label brands could boost operating margins, as management says the gross margin is higher in the private label brands category. Thus, the share of private label brands in the company increased from 10.8% in Q1 2022 to 16.1% in Q1 2023.

M&A: high cash on the company's balance sheet and lack of debt, coupled with general pressure in the industry, can provide the company with attractive M&A opportunities at an attractive price, which can have a positive impact on both business volume and market share, as well as consolidated profitability.

Volume: federal legalization of the company's products can provide significant support to both sales volumes and support the average selling price of products, however, this driver is, in my personal opinion, low-probability, and its implementation may take a very long time.

Valuation

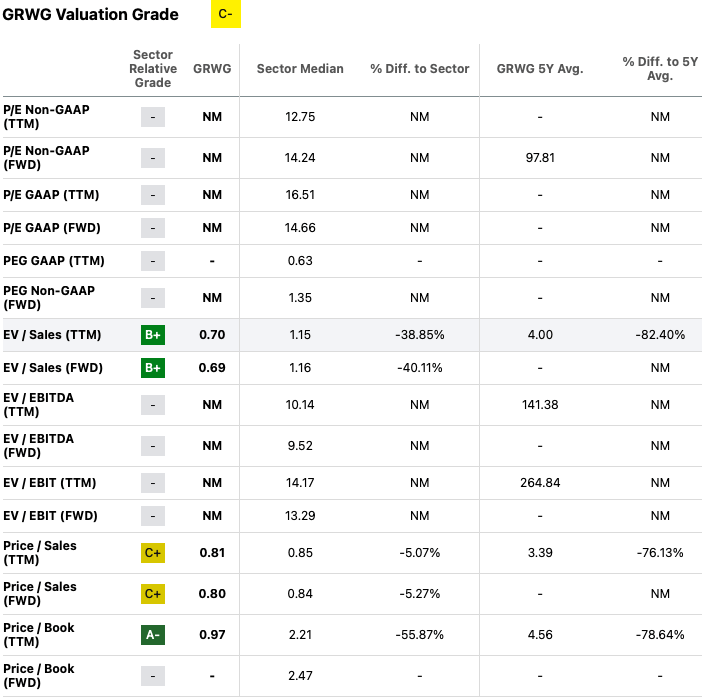

Despite the fact that the company's shares are not expensive relative to historical values, in my personal opinion, it is not worth making an investment decision to buy based only on an attractive valuation in accordance with multiples. We are currently unable to calculate major multiples such as P/E & EV/EBITDA as Net income & EBITDA are negative. According to the P/S multiple, the company trades close to the industry average.

{kind=link}

Conclusion

Thus, in my personal opinion, now is not the best time to enter long positions based solely on the company's low valuation relative to historical values. I believe that investors need to wait for the results over the next few quarters to see if the market has really stabilized at current levels and if the company is able to demonstrate an improvement in operating margins given the change in business volume. In addition, I would like to hear more details and initiatives from management on how the company can continue to improve margins in addition to growth in private label brands, as high fixed store costs could continue to put pressure on us if we do not see recovery in the industry and the growth of the company's business volumes.

For further details see:

GrowGeneration: Still Not The Best Time To Buy The Dip