NVDA - GSI Technology: Q1 Earnings Preview And Product Positioning Relative To Nvidia

2023-07-27 02:37:57 ET

Summary

- GSI Technology has seen a significant rise in its stock, possibly due to its development of the Gemini APU, a processing unit for IT workloads that enables faster computations.

- GSI's APU allows for simple computations on large datasets, which is key for AI applications.

- Despite optimism around the Gemini II and potential applications in areas such as edge computing and autonomous driving, GSI's revenue has decreased by 11% in 2023, raising concerns about its growth potential.

- There are opportunities, but there is a need to watch out for progress in the forthcoming earnings call.

- The comparison with Nvidia is helpful to position the stock in AI-enabling chips space.

GSI Technology ( GSIT ) stock's astronomical upside started on May 10 seems with the only major event which happened around that period being the publication of its fourth-quarter 2023 financial results some days before. Another noteworthy observation as charted below, is its stock (in blue) benefiting from a much higher price appreciation than even semiconductor giant Nvidia's (NASDAQ: NVDA ) 53%.

Now, since GSI operates in the IT sector, more particularly in the semiconductor industry, my objective with this thesis is to uncover potential AI-related opportunities, namely through differentiation between Nvidia's A100 and H100 GPUs or Graphics Processing Units.

At the same time, given the high expectations which seem to be priced in the stock, I also provide insights into what specifically to look for when GSI reports its first quarter 2024 financial results on July 27.

I start by providing a product overview which helps to explain part of the reason why the stock instilled such enthusiasm among investors.

GSI's APUs Vs Nvidia's GPUs

This is a company that has about twenty years of developing high-performance RAM (random access memory) chips in the form of SRAM where the S stands for Static. For investors, there are the conventional memory chips or DRAMs produced by the likes of Samsung ( SSNLF ) and Micron (NASDAQ: MU ) where the data is lost when the computer is suddenly powered off whereas static RAM is still available. As such, GSI’s SRAM has found applications as embedded components in remote devices both in the commercial and military fields.

{kind=link}

More importantly, and this is where the comparison with Nvidia makes sense, the company has developed a new processing unit for IT workloads called the Gemini APU or Associative Processing Unit . This is about in-memory processing or running applications inside the memory system itself instead of making them move to and forth from the processor. As a result, more rapid computations become theoretically possible.

Detailing further, standard CPUs like those produced by Intel (NASDAQ: INTC ) are very efficient at performing complex computations on small data sets. However, with larger datasets, there are bottlenecks due to the limited passage (bandwidth) between the CPU and the memory.

This problem has been solved by companies like Nvidia whose GPUs are able to process some of the data together with CPUs in what is termed as parallel processing. This also requires high bandwidth memory produced by the likes of SK Hynix in order to support resource-intensive applications like ChatGPT. However, there are higher energy costs which are associated with such architectures.

Another approach is to use GSI’s APU which makes possible simple computations on large datasets. The key here is to use in-memory processing and GSI's proprietary data transfer technology, which enables higher performances while consuming relatively less power.

www.gsitechnology.com

Therefore, both Nvidia and GSI enable something called " massive parallel processing " which is the key to enabling AI applications to run.

To obtain an idea of the performance difference between their processors, I considered that the peak compute provided by the APU was 25 TOPs , with Nvidia's A100 providing 75 TOPS. Furthermore, Nvidia's latest H100 PCIE GPU enables superior performances of 3200 TOPs and above. Now, TOPs rates the capacity of an AI accelerator, but this is not a like-to-like comparison in the sense that conditions (load and duration of the tests) vary plus GSI's APU ratings date back to July 2020. In the meantime, it has progressed with the faster Gemini-II chips.

Areas of Applications for GSI's Chips

However, the above comparison has the merit of showing that behind the stock’s sudden appreciation, there is genuine technological progress in the form of the Gemini APU that can at least be compared to one of the world's most sophisticated AI chips currently available, not just a highly promising design document. For this purpose, in the same way as the one trillion dollar company, GSI intends to outsource the manufacturing of its next-generation Gemini-II chips to Taiwan Semiconductor Company ( TSM ). However, in contrast with Nvidia which is produced using a 4 nm (nanometer) manufacturing process, GSI's chip will use a 16nm process as it also includes SRAM.

Furthermore, the executives displayed optimism about the latest Gemini which should offer “ 15 times the memory bandwidth of the state-of-the-art parallel processor for AI.” Also, with more development (as included in the product roadmap), GSI's APUs should be able to support the LLMs or large language models which are required for applications like ChatGPT to function.

Consequently, looking at the commercial applications, I would not consider GSI to be Nvidia's competitor at this stage. The reason is that the giant chip play is at a more advanced stage as its A100 has already proved instrumental to ChatGPT’s rapid adoption and it is now shipping the even more powerful H100 series. These are being purchased mostly by service providers like Microsoft (NASDAQ: MSFT ) who by upgrading some portions of their cloud offerings to be AI-enabled, can then propose AI-as-a-Service to thousands of corporations.

This signifies that Nvidia's GPUs are finding wider usage in data centers, while for GSI things are different.

First, it is working more towards offering high-speed computing in the form of embedded AI as its Gemini chips consume less energy, and their all-in-one architectures (by containing both processor and memory) make them more portable. As such, its products are finding traction in edge computing where a lot of processing power is needed at the user's location itself. There are other use cases, namely with autonomous driving, ships, satellites, or aircraft as listed in the table below. Noteworthily, applications for military purposes are helped by the fact that GSI's devices have radiation tolerance properties with the company also intending to develop search capabilities in a SaaS format, somewhat similar to Open AI , ChatGPT's developer.

Table Prepared Using Data from (www.seekingalpha.com)

While many of these are at the testing phase, revenue-generating opportunities have begun to emerge as exemplified by the $1.25 million research contract signed recently for the Gemini-II by the Air and Space Force Missions. Moreover, product distributors have been added to expand market access beyond America to Europe while there are also prospects for licensing opportunities with strategic partners.

However, no guidance has been provided but rather optimism expressed about generating modest revenue from APUs in fiscal year 2024.

Valuing the company

In these circumstances, in order to come to a value, I first consider the finances.

In this case, it is found that full-year 2023 revenues of $29.7 million have actually gone down by 11% with respect to 2022 with little change as to the operating loss-making status. The only positive is gross profit margins increasing by more than 4% which is explained by a better product mix .

Annual Revenue and Profitability (www.seekingalpha.com)

{kind=link}

Going into details, the company obtains most of its revenues through SRAM and has one reportable business segment which is the design, development, and sale of integrated circuits. Furthermore, as seen below, most sales activities (85% or 23,023/29,691 as per the table below) are carried out through distributors which means that expanding the distribution channel is the appropriate option to rapidly cover a wider geographical area without having to employ additional salespersons.

SEC Filings (seekingalpha.com)

Therefore, with a product that is appropriately positioned and by augmenting the sales channel, GSI could harvest some opportunistic wins with its APUs as 80% of CIOs believe the AI will help their organization make better use of data. In this context, with the ease of use of ChatGPT, OpenAI has in some way democratized the technology which was previously associated with complexity and a high barrier of entry. Moreover, with everyone talking AI, GSI does not have to spend on marketing to get visibility, and together with some previous operating cost cuts, this augurs well for profitability.

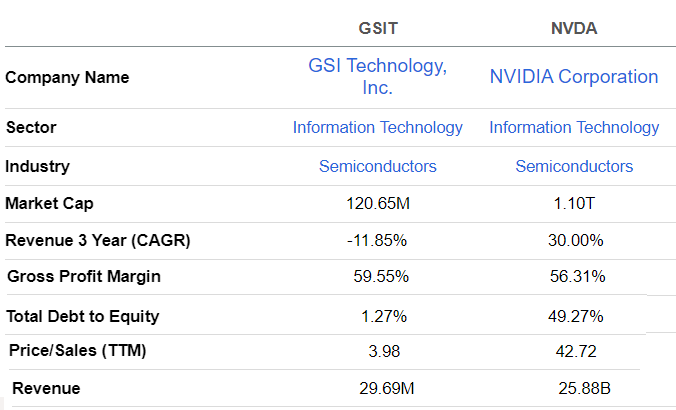

In these circumstances, the trailing price-to-sales multiple of 3.98x, which remains above the median for the IT sector by 39% can still be justified, especially given that the share price is significantly down from its $9 peak level, implying that a lot of the hype which was priced in the stock could have gone. In the same breath, its P/S is ten times less than Nvidia's as tabled below while delivering higher gross margins compared , and this, despite having a much lower revenue base to spread its fixed cost, which also points to better production efficiency. Also, with a low Debt-to-Equity ratio, GSI is a Hold for now.

Comparison of Key Metrics (www.seekingalpha.com)

{kind=link}

To justify my position, it has a revenue growth problem, and unless it is able to license its technology, sales are likely to increase only modestly, meaning that investors may get impatient as sales opportunities take time to materialize, and dump the stock in case of adverse market news.

What to look for during Earnings

For this reason, for those who are holding onto the stock and wondering what to do next, or others who are thinking of investing after the retrenchment to the $4.71 level, it is important to focus on the first quarter 2024 results expected on July 27 . Now, items to watch out for are first, developments around the plugin for search purposes which could be a boon for sales if delivered rapidly. Second, R&D contracts that can bring a stable revenue stream while more sizeable sales prospects materialize are also something investors want to scrutinize. Third, it is important to be on the lookout for any partnership for licensing their APU technology as this is a rapid way to scale. Fourth, developments, around the distributor ecosystem for market access are key both for the APU and SRAM. Fifth, any guidance would help to value the stock more precisely.

Finally, by providing insights into the company's products while performing a comparison with Nvidia, this thesis has shown that GSI could benefit from opportunistic AI-related contracts. This means that in addition to the hype factor, there are some real opportunities, but a lot will depend on how the management executes.

For further details see:

GSI Technology: Q1 Earnings Preview And Product Positioning Relative To Nvidia