CA - H&R REIT: An Attractive Discount To NAV But It Needs To Fix Two Things

2023-08-13 08:09:56 ET

Summary

- H&R REIT's Q2-2023 results show strong growth in same property net operating income and modest growth in funds from operations.

- The REIT's growth was strong even on a currency neutral basis, despite the impact of currency exchange.

- We highlight two reasons why we are staying out.

Note: All amounts discussed are in Canadian Dollars.

On our last coverage of H&R REIT ( OTCPK:HRUFF ) ( HR.UN:CA ), we noted the strong positive and the valuation discount were offset by negative forces. On balance that kept us firmly in the neutral zone and refused to give it a "buy". Specifically we said,

In balance we rate it as hold/neutral, while noting that it would be very hard to get negative long term returns from this point combining the 8X FFO multiple and 50% NAV discount.

Source: Possibly The Only Office Bet You Should Consider

The picture below shows all our most recent ratings on H&R and the decision to move away from a buy on Feb 21, 2023, appears to be working. H&R has certainly bled since then.

Seeking Alpha-Returns Since February 2023 Article

We look at the Q2-2023 results to see if we can get more constructive with the REIT making more progress on its long term goals.

Q2-2023

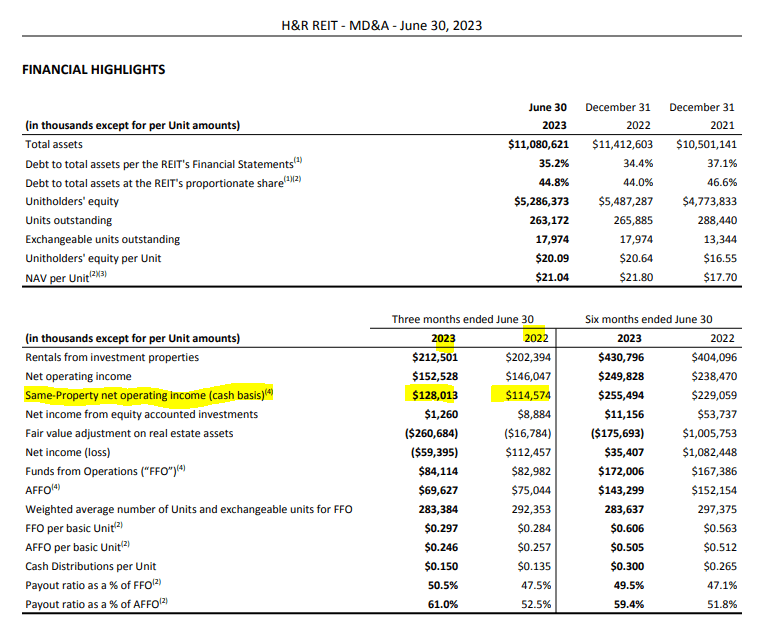

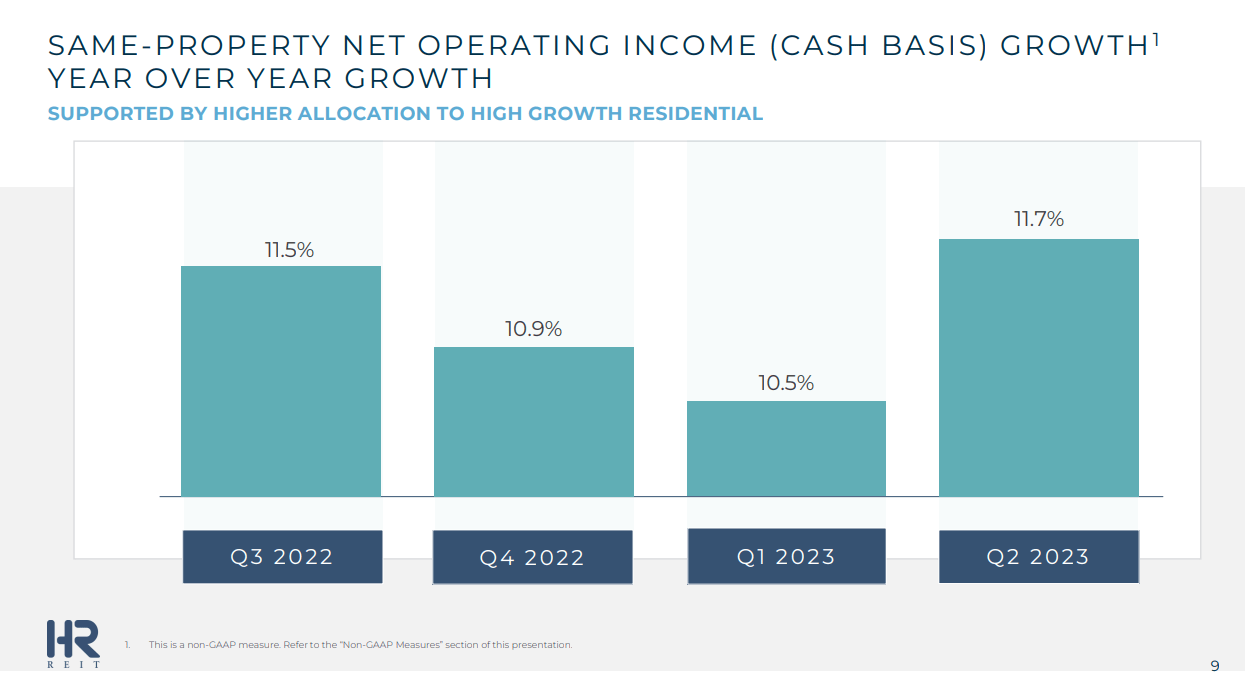

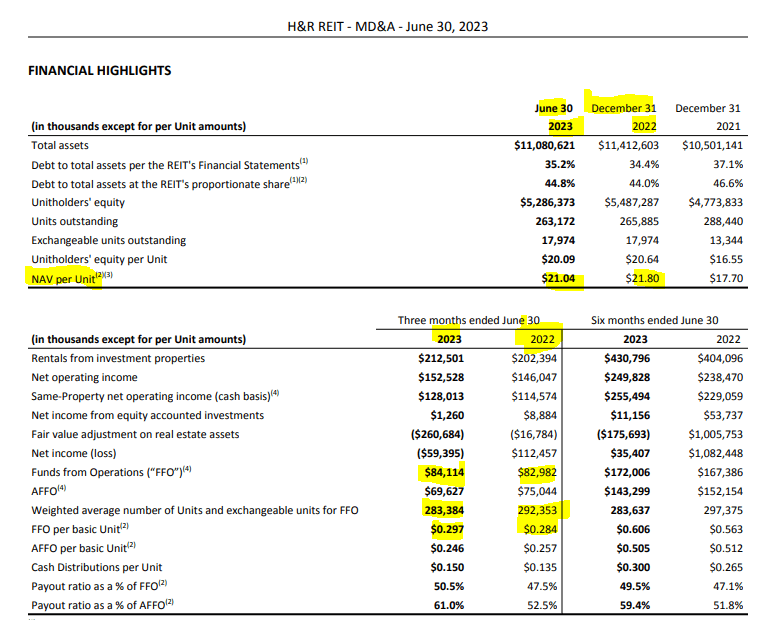

H&R's financials have been incredibly noisy with the developments coming online and asset sales in the office sector providing more sources of variance. But the first metric that is always a clean view of what is going on is the same property net operating income (NOI). That number was up very strongly this quarter once again as same property NOI increased almost 12%.

{kind=link}

H&R has been doing this rather casually for multiple quarters in a row as this metric has stayed in double digit territory.

{kind=link}

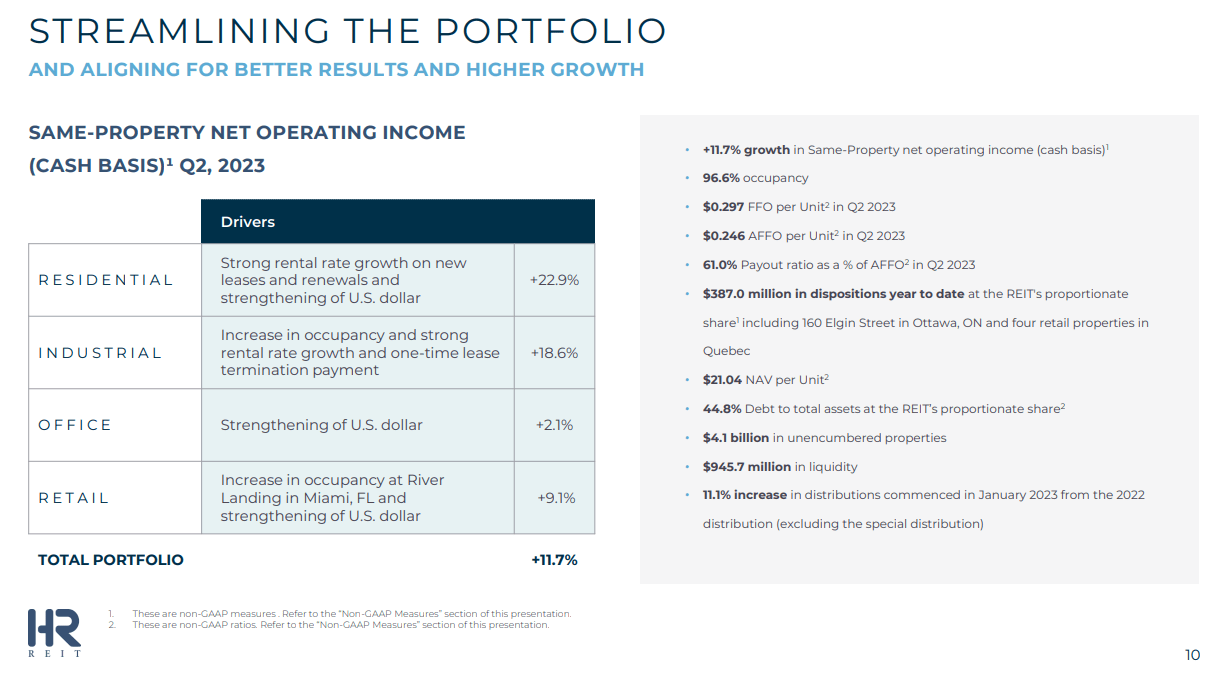

While the heavy lifting was done by the residential segment, it is hard to ignore what retail and industrials were doing in the last quarter. Even the beleaguered office segment managed to increase compared to 2022.

{kind=link}

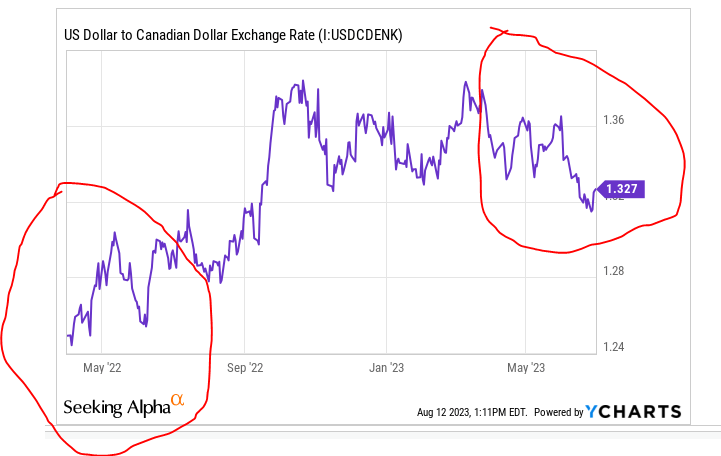

While those numbers were good, there was definitely an element of currency exchange adding some extra oomph to this mix. You will note that the strength of the US dollar was mentioned in 3 out of the 4 segments. The currency impact was still modest. USD-CAD averaged near 1.26 last year in Q2-2022. This year was near 1.34. So that is about a 6% differential.

{kind=link}

Also one must keep in mind that about two-thirds of the total portfolio fair value is in US. So currency impact was about 4% adjusted for this fact. So H&R's growth was quite strong even on a currency neutral basis.

The other relevant portions of the financial highlights are shown below. The NAV were unit declined by about 4%, which given the currency tailwinds shown above, was quite substantial.

{kind=link}

Overall funds from operations (FFO) and FFO per unit both grew modestly. The latter was supported with unit buybacks decreasing unit counts by about 9 million year over year.

Current Setup and Outlook

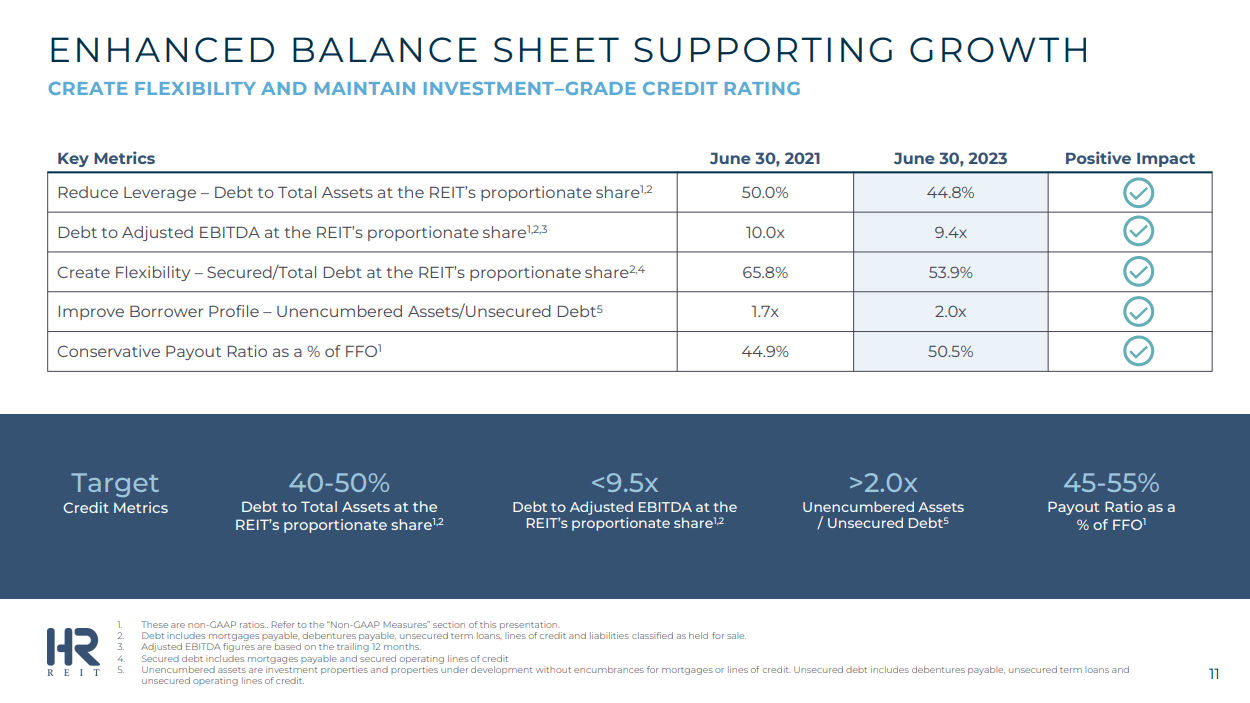

If you examine H&R through a debt to asset perspective the leverage is not too high at 44%. Debt to EBITDA though looks still unwieldly at 9.4X.

{kind=link}

Some of this is a consequence of the extremely low cap rate assets like residential and to some extent even industrial. As we have previously stated in the case of REITs like Allied Properties REIT ( AP.UN:CA ) and RioCan REIT ( REI.UN:CA ), we generally want this to be under 8.0X. But H&R has some better assets and we might be ok with a 9.0X multiple here assuming that everything else checks out. This is especially true with residential and industrial making well more than half of the total NAV.

{kind=link}

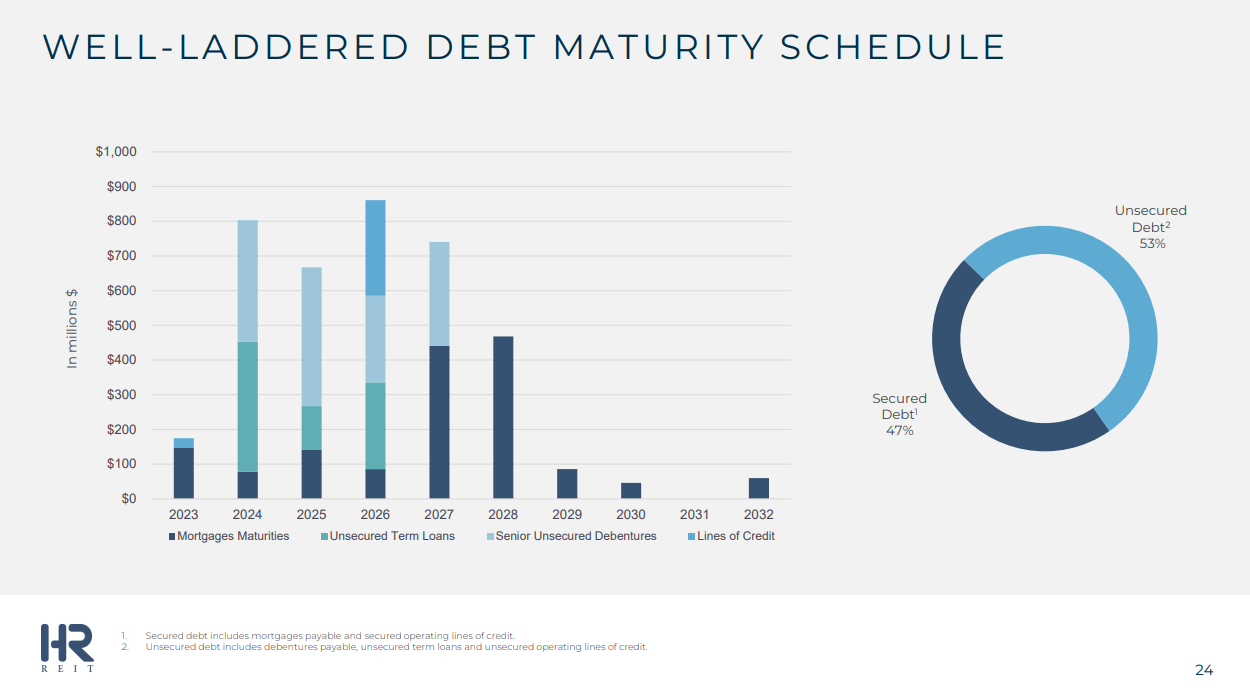

But the thing here that does not check out is the debt maturity schedule. It remains incredibly short by any stretch of the imagination.

{kind=link}

Not only is it short, but it is getting shorter as H&R appears to be waiting for lower rates.

The weighted average interest rate of H&R's debt as at June 30, 2023 was 4.0% with an average term to maturity of 2.9 years. The weighted average interest rate of H&R's debt as at December 31, 2022 was 3.8% with an average term to maturity of 3.2 years.

Source: H&R REIT Q2-2023 Results

Verdict

One of the best things about H&R is that their cap rates are quite realistic. We have harped on many Canadian REITs like Dream Office REIT ( D.UN:CA ) and True North Commercial REIT ( TNT.UN:CA ) that keep using very low cap rates to value their NAV. We found some industrial REITs using sub 4% cap rates in Canada. H&R looks really solid and they also marked down their properties this quarter once again.

{kind=link}

As a REIT that has a good history of selling properties well above their own NAV estimates, we think this adds an additional layer of buffer. So considering all that, the price of $10.30 relative to the NAV over $21.00 seems to offer enough of a buffer. But that debt maturity profile still is eye-watering. We just can't help but wonder what management was and is thinking here. All this is coming from the same REIT that had to slash its distribution by 50% and get financing at near 12% rates, because it did not manage its liquidity well enough.

DBRS has today maintained the BBB Issuer Rating and STA-3 (high) stability rating of H&R Real Estate Investment Trust (H&R or the Trust) Under Review with Negative Implications following the Trust's announcement on December 23, 2008, that Fairfax Financial Holdings Limited (Fairfax) has agreed to purchase, subject to the satisfaction of certain conditions, $200 million of 11.5% unsecured debentures, on a private placement basis, from H&R. Concurrently, the Trust has also announced a 50% reduction in its cash distribution from an annualized rate of $1.44 to $0.72 per unit.

The ratings were originally placed Under Review with Negative Implications on November 18, 2008, reflecting DBRS's concern that H&R could face difficulty in securing adequate financing for its development commitments in light of the challenging credit markets. DBRS estimated capital requirements on the Trust's development projects of $1.1 billion over the next four years, with a majority of this amount associated with The Bow office tower in Calgary (the Bow).

Source: Morningstar/DBRS December 2008

We have enough quality REITs today that offer investors a chance of good upside without these additional risks. We continue to rate H&R a hold and will consider an upgrade on further debt reduction and/or increase to weighted average debt maturity.

Please note that this is not financial advice. It may seem like it, sound like it, but surprisingly, it is not. Investors are expected to do their own due diligence and consult with a professional who knows their objectives and constraints.

For further details see:

H&R REIT: An Attractive Discount To NAV, But It Needs To Fix Two Things