CA - H&R REIT: We Are Moving To The Sidelines

Summary

- H&R REIT has delivered a stellar performance over the last 2 years.

- More importantly, management has made all the right moves and we can find no fault.

- We go over the most recent results and tell you why we are still downgrading this to a neutral rating.

Note: All values are in Canadian Dollars and stock price references are to the price on the TSX, not for the OTC stock.

When we last covered H&R REIT (HRUFF) ( HR.UN:CA ), we noted that the REIT was still being punished for its past errors and not getting enough credit for its transformation plan. We stamped a buy rating and suggested the shares may have some room to rise.

But the REIT remains positioned to succeed and we believe in the NAV supported by high quality residential and industrial properties. We are maintaining our price target at $16 as the two forces of higher cap rates and higher USD-CAD exchange rate, essentially cancel each other out.

Source: H&R REIT Still In Purgatory

The stock has delivered a modest return since then, but that has been about in line with broader REIT sector as represented by iShares S&P/TSX Capped REIT ETF ( XRE:CA ).

With Q4-2022 results out , we looked to see how H&R's transformation strategy was progressing.

Q4-2022

The fourth quarter capped off a solid year for H&R. The REIT delivered a 2 cent beat on funds from operations ((FFO)) versus consensus, powered by strong net operating income ((NOI)). The company's occupancy ratio moved up to 96.6%. That number is quite an achievement considering that it still has substantial office and retail assets in its fold. In fact, the gains in occupancy were primarily powered by office and retail segments moving up, while residential stayed flat. Another notable announcement followed in the press release with Elgin Street being sold for more than a quarter billion dollars.

The REIT has entered into an agreement to sell 160 Elgin Street ("160 Elgin"), an office property in Ottawa, ON, for $277.0 million. The selling price is in line with 160 Elgin's value recorded at December 31, 2022. 160 Elgin was classified as held for sale at December 31, 2022. Closing is expected to occur in April 2023.

Source: H&R Q4-2022 Press Release (linked above)

This was a notable sale and reduces concentration within the office segment further.

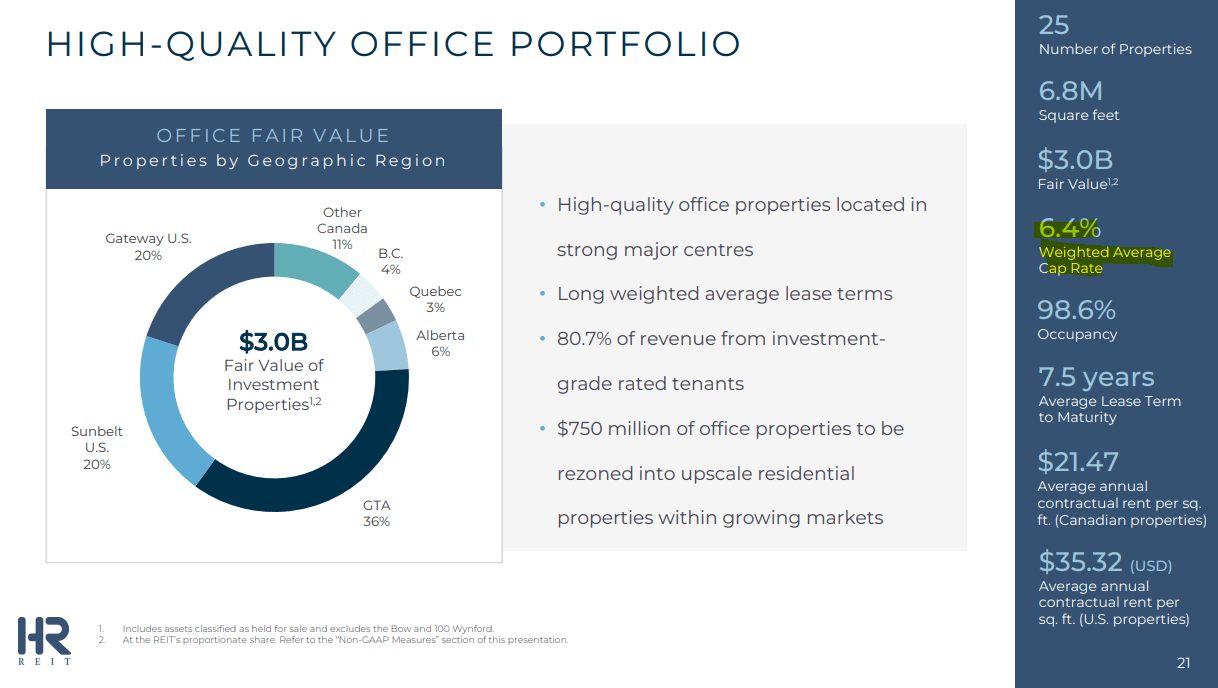

And lastly, our Canadian office segment, not subject to rezoning, represents the remaining $1 billion, of this $1 billion, 160 Elgin represents 27% of that office segment's fair value and is the only office property located in Ottawa, which is not considered a core market for H&R.

On a square foot basis, 160 Elgin represents nearly 1 million square feet out of 3.2 million square feet or said differently 160 Elgin represents approximately 30% on a square footage basis of our Canadian office, not currently being rezoned.

Source: H&R Q4-2022 Conference Call Transcript

Outlook

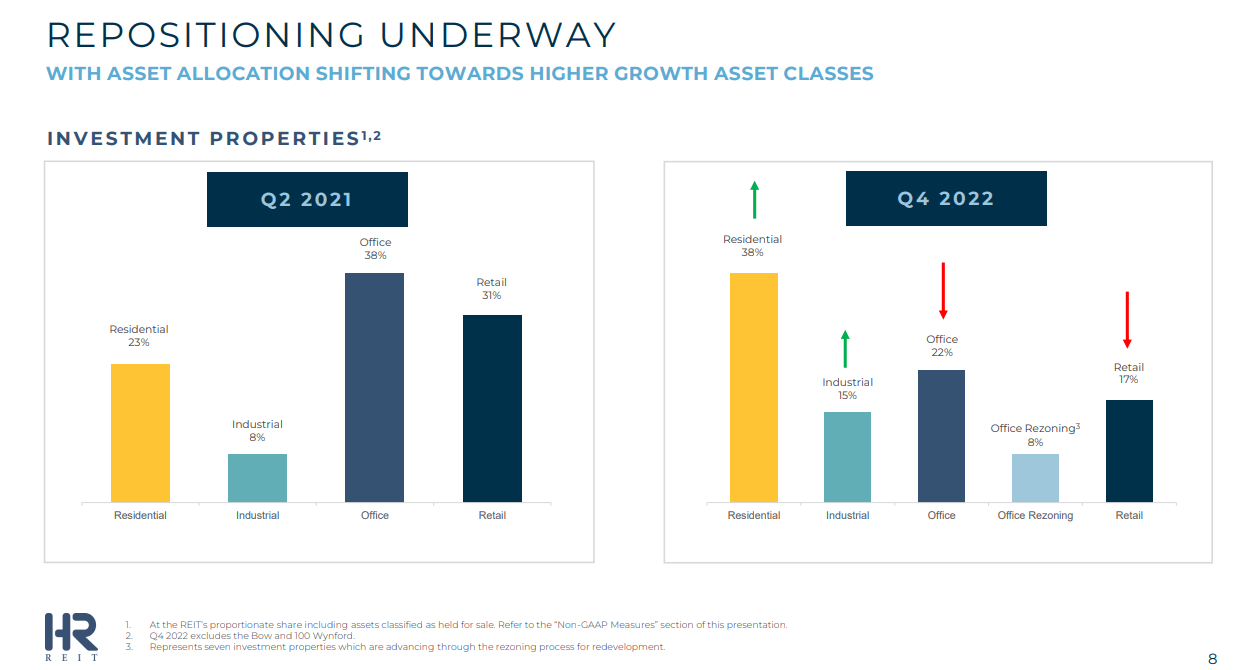

H&R's repositioning has gone according to plan.

{kind=link}

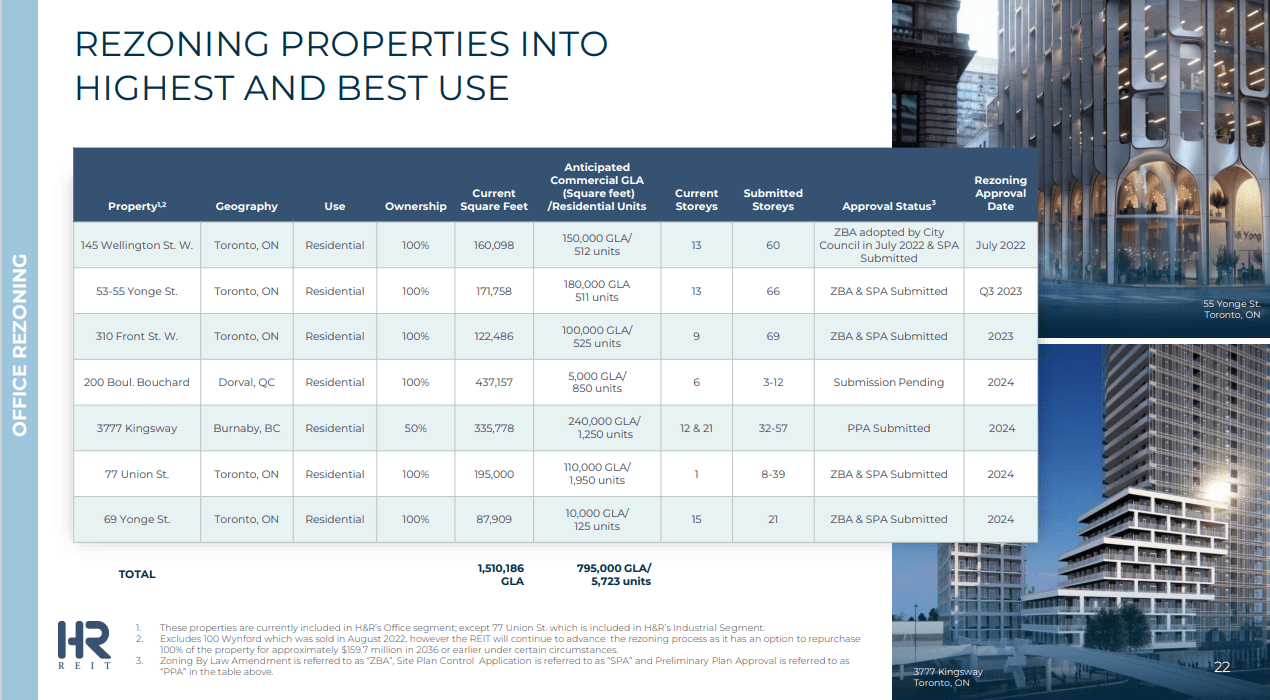

The rezoned office segment is slated to be converted to residential in some extremely pricy areas of Toronto and Burnaby.

{kind=link}

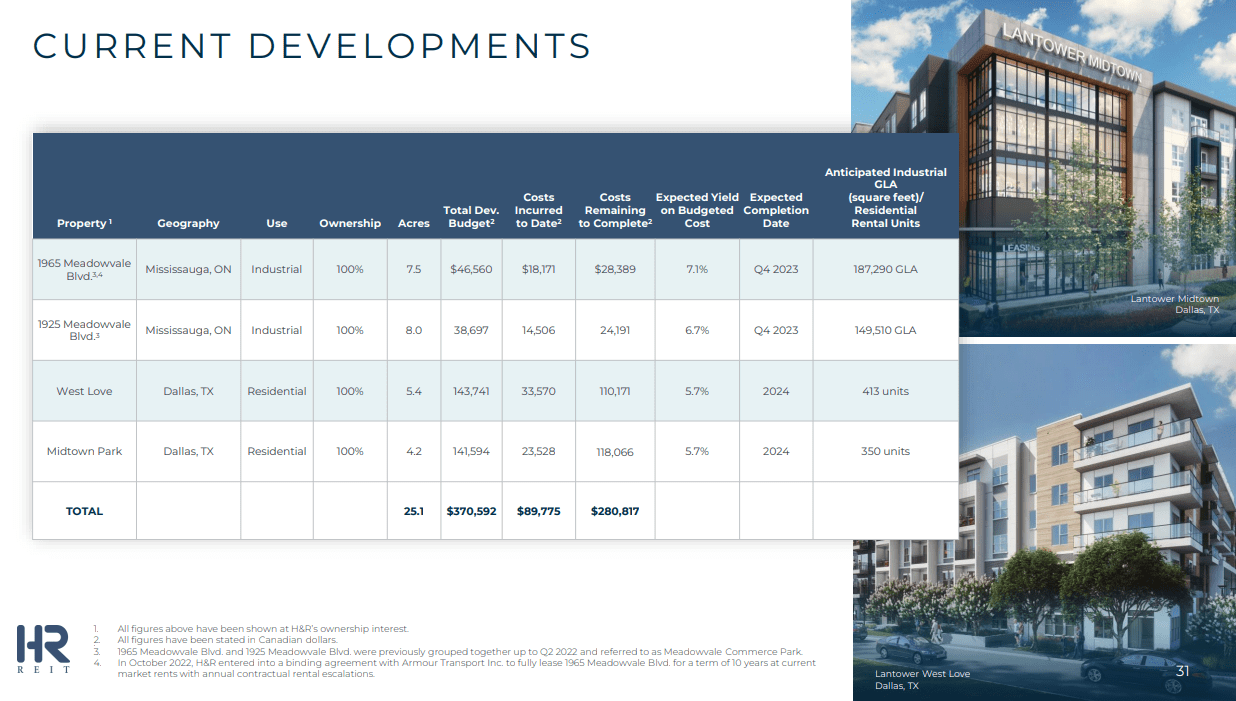

This will be a long drawn out process and investors should not expect quick results. Most of these will only be approved for rezoning by end of 2024. There will be a large amount of capex spend for this and results will take another 3-5 years after that. What H&R has going for it is an extraordinarily low payout ratio near 50%. This allows over $150 million of FFO to be retained and directed towards the repositioning process annually. The repositioning extends beyond just the office rezoning process. It also involves H&R building and expanding its residential and industrial presence.

{kind=link}

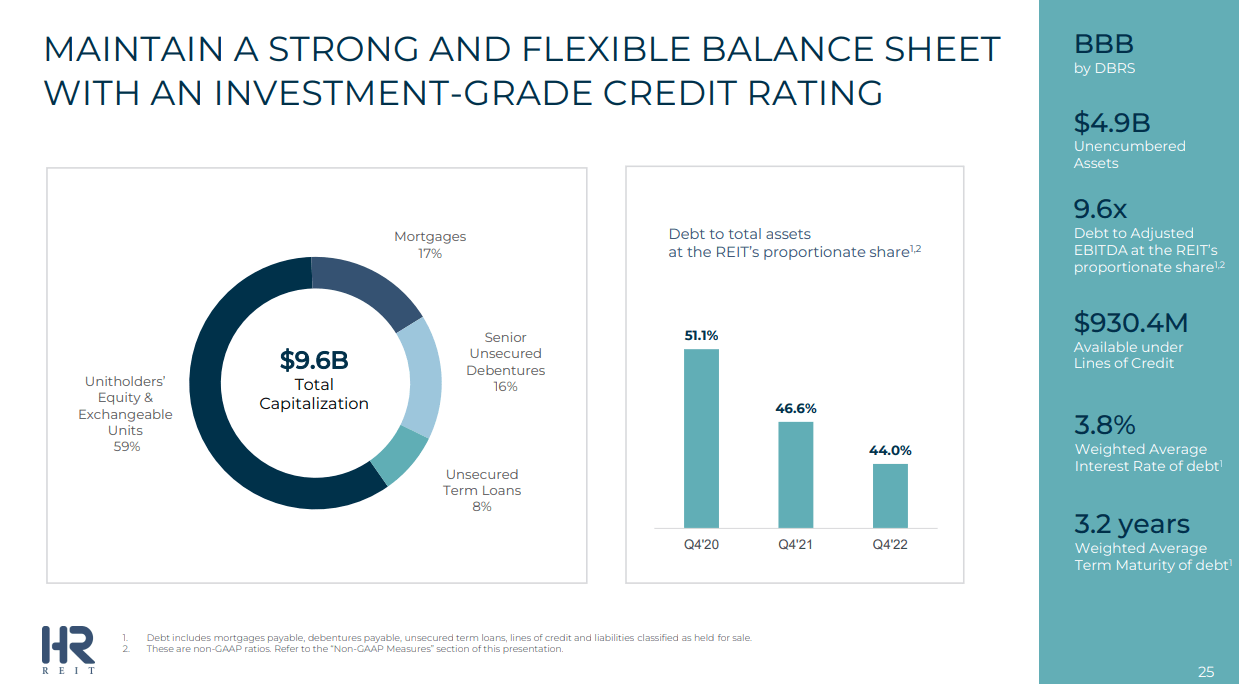

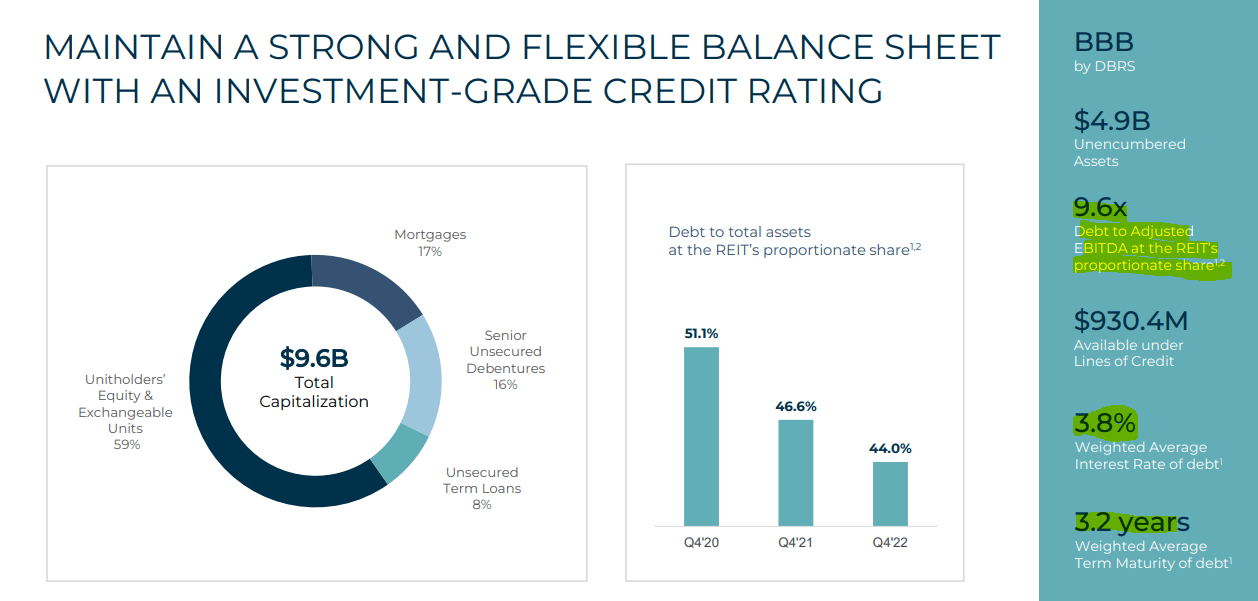

So H&R has been able to direct capex towards that while lowering the debt to asset ratio over the last 3 years.

{kind=link}

This is despite some aggressive buybacks over the last 12 months. The REIT purchased about 23 million units in 2022 at a weighted price of $12.99. According to the company's own valuation process, this was at a 40% discount to NAV.

On the negative side, the cap rates on the US Office portfolio still appear a bit optimistic to us.

{kind=link}

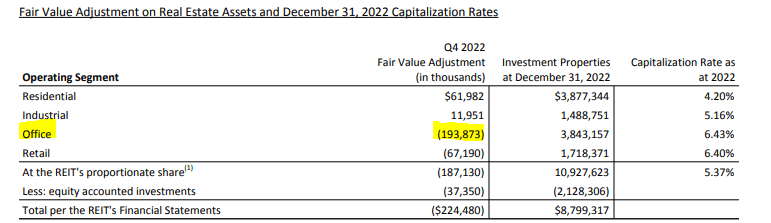

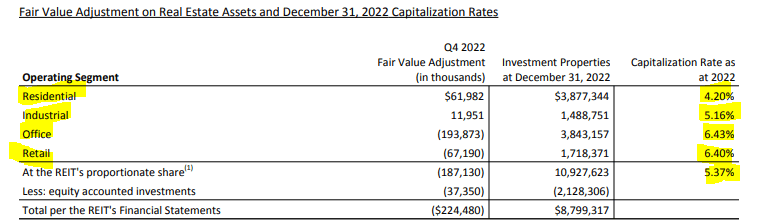

Investors may disagree with our repeated harping on this but H&R's NAV fell from $22.58 to $21.80 quarter over quarter. This is despite some aggressive buybacks which are NAV accretive. The driver here was the fair value adjustment on the office and retail side.

{kind=link}

We don't think the process is close to complete in an era of 5% risk free 1 Year Treasury rates in US. The other negative continues to be the weighted maturity of the debt. At 3.2 years it is deigned to inflict pain in this interest rate environment.

{kind=link}

We have not seen it yet as H&R sold almost half a billion of assets in 2022, offsetting the rise in rates as total debt went lower. But the impact is coming down the line.

Verdict

We really cannot find any fault with H&R's strategy. The residential and industrial look to be the most promising areas and that is where H&R is focusing its firepower. At the same time, office assets are being sold selectively, rather than via a fire sale. The company continues to deleverage and has not got wild with the payout ratio. While not a critique of the strategy per se, we think the cap rates are still extremely optimistic.

{kind=link}

Our numbers get us a to a NAV near $15 or $16. This is still a discount relative to the stock price, but perhaps offers less a margin of safety than what many might desire. What is also notable is that we see this or better level of discount across many REITs. We had recently covered Artis REIT ( AX.UN:CA ) and that trades at a wider discount to its own NAV and to our estimate of its NAV. So the question comes whether we want to pursue this here with the current levels of buffer. We have to go with a "no" at this point. Despite all the right moves being made by management, we don't see the current environment as extremely conducive for this. We might get more interested at a later time point, should the price decline enough to give us a better cushion. We are downgrading this to a "Hold/Neutral" rating.

For further details see:

H&R REIT: We Are Moving To The Sidelines