CA - Hammond Power Solutions: Supplying The Electrical Grid With Critical Solutions

2023-09-02 00:23:00 ET

Summary

- Hammond Power Solutions is benefiting from the global build-out of electrical infrastructure and the electrification of the vehicle grid.

- Hammond is a leading supplier of dry-type transformers in the US and Canada.

- The stock is currently trading at just 11 times earnings, well below its peers.

- There are some concerns about margins reverting, leading to a low multiple, but if sustainable, the stock likely remains undervalued.

Introduction

Hammond Power Solutions ( HPS.A:CA ) manufactures and distributes various electrical components and equipment. The company is specifically known for their dry-type transformers (more on this below). Hammond has a strong history of profitability, with profits inflecting significantly higher beginning in 2022. The company is benefitting from several key tailwinds, including a global build-out of electrical infrastructure to support green energy production and the electrification of the vehicle grid. At the same time, competitors have failed to obtain supply, allowing Hammond to raise prices.

That said, the stock has gone on a run and you'd be forgiven for thinking you're too late. The key question now is whether earnings are sustainable, and what multiple the stock could trade at if they are. Currently the stock trades at just 11 times earnings, well below peers.

The Products, Business, and Competitive Advantages

Hammond manufactures a variety of industrial electrical components and products, but they're best known for their dry-type, cast resin, and liquid filled (wet-type) transformers. More specifically, Hammond's reputation for dry-type transformers is among the best for reliability and delivery times.

Hammond has manufacturing facilities in Canada, the US, Mexico, and India. All major competitors manufacture overseas. One industry insider told me that Hammond's manufacturing grants Hammond the ability to deliver to North American companies faster, one of several key reasons a customer would opt for a Hammond transformer over a competitor. This delivery time can often be critical for a project to be completed on schedule.

Hammond's western manufacturing facilities allow the company to use high quality materials and quickly come up with customized solutions, two things that are more difficult for competitors manufacturing overseas to do. Overseas manufacturers have to deal with language barriers, long lead times, and more complex supply chains, leading them to attempt short cuts, resulting in lower quality products. As a result, Hammond has grown to be one of the top dry-type transformer manufacturer/suppliers in North America. Hammond discusses this a bit in their Annual Reports , which are an excellent resource for anyone beginning to look at this company.

Furthermore, transformers, although can individually cost a respectable sum of money, often pale in comparison to the scope and size of an entire project, and thus customers are somewhat price-insensitive relative to completion time. It is often the contractor that makes a transformer purchasing decision, but additional costs may be passed on from the contractor to the contractee in some agreements. This further reinforces Hammond's ability to maintain pricing.

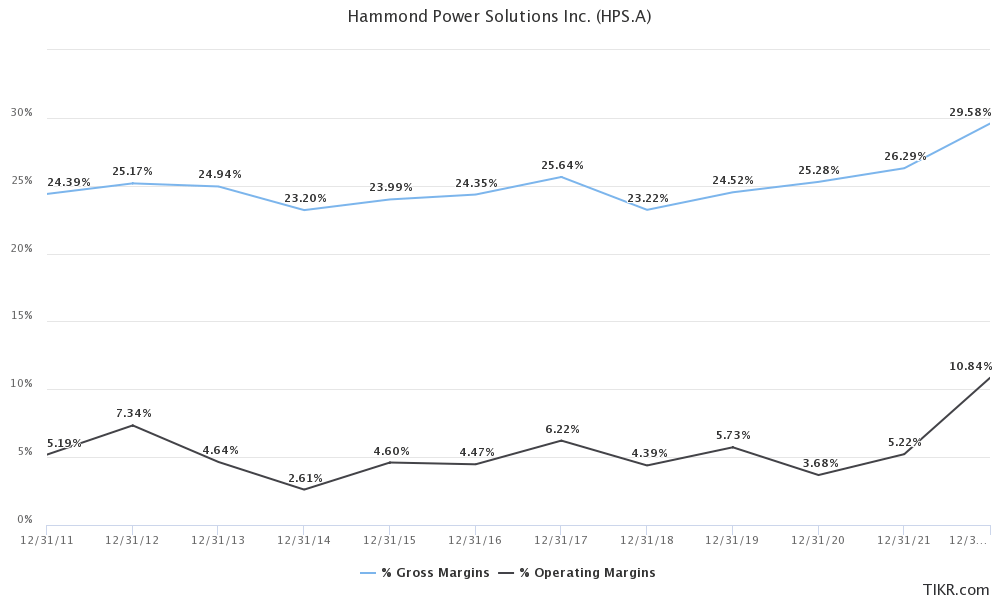

Hammond's margins have seen an improvement recently. It seems plausible that these may be sustainable and a "new" normal, but I think it's also fair to be cautiously optimistic going forward.

Hammond Power Solutions Margins (TIKR.com)

{kind=link}

Most Recent Quarter

Hammond's stock price had a somewhat muted reaction to the company's most recent quarter, which they reported in Early August. I thought the earnings report was good, but some cost pressures began to reveal themselves, perhaps leading to the market's non-reaction. Revenue grew 25% YoY to a record $172M CAD . Operating income grew to $19M, up 90% from just $10M in the same quarter of 2022, although down slightly from Q1 2023 when Hammond earned $22.6M. Management suggested on the earnings call that the decrease in margins in Q2 from Q1 was mainly attributable to an unfavorable customer mix and higher inventory provisions. Management was optimistic that margins could be maintained going forward and that demand and pricing remains strong.

During the quarter, the company brought in a new CEO, Adrian Thomas , as the former CEO Bill Hammond retires after leading Hammond for over 20 years. Adrian Thomas brings significant experience, including positions at General Electric ( GE ), TMEIC, and Scheider Electric ( OTCPK:SBGSF ). While it's far too early to tell yet, he appears, on paper at least, to be a solid choice.

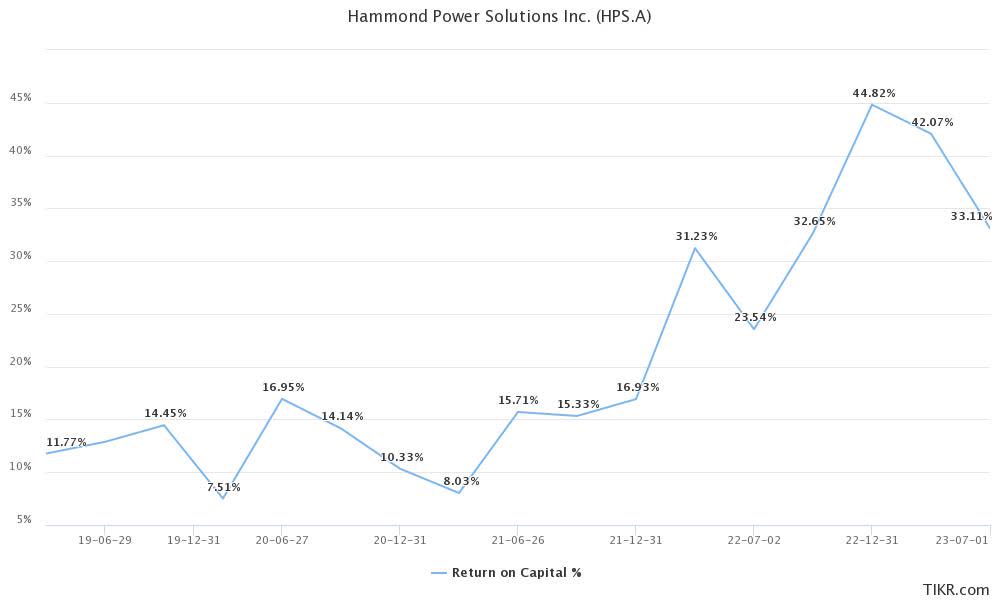

Hammond is continuing to reinvest in the business to increase production. Historically, Hammond has earned solid high single digit to mid teens double digit percentage returns on capital. In 2022 this spiked, however, even if this reverts to mid teens, Hammond's investments should ultimately generate considerable value for shareholders.

In parallel, we continue to expand our network of distributors in both the United States as well as Mexico, which broadens our ability to serve our customers and participate in new opportunities. Given our positive cash flow, we are investing in a significant expansion of our North American operations, which will increase our output by almost $250 million over the next several years. This includes a new small products plant in Mexico, which will be up and running by mid-2024. This capital investment will expand our foundation and capabilities to support our growth to $1 billion in sales before the end of the decade.

-Bill Hammond, Q2 2023 earnings call

Hammond Return on Invested Capital (TIKR.com)

{kind=link}

Overall, while not spectacular, I thought it was a solid quarter and the company is clearly demonstrating continued strong growth in both revenue and earnings. I expect the growth to continue on a YoY basis for the rest of this year, and I'm optimistic the company can continue growing in 2024 given increased production capabilities coming online sometime during 2024.

Competition & Valuation

Hammond has earned $4.94 CAD per share in the last twelve months. With the stock trading at $56.14 CAD, it's just over 11 times trailing earnings. This is substantially lower than its large-cap peers, although many of these peers are much larger and more diversified global businesses, so the comparison is not perfect.

Nonetheless, Hammond is a good business and if they can maintain or continue to grow earnings, then it's hard to argue that 11 times earnings is not an attractive valuation.

Risks and Concerns

Despite my rhetoric above, the sustainability of pricing remains a key question for potential Hammond Power investors. On the one hand, they've procured supply and maintained deliverability while holding a reputation for reliability, leading customers to stick with them. On the other hand, it is possible that competitors fix their supply chains, stock up on fully assembled transformer inventory in the West, and compete with Hammond on price. In the former scenario, Hammond likely maintains pricing power and margins likely maintain high single digits to low double digits percentage operating margins. In the latter scenario, Hammond's margins could revert back to historical levels of about 5%.

Investors should also consider increased investment in the electrical grid which has been a strong tailwind for Hammond recently. While I think this is likely to continue, it is possible that in a recession scenario, we see governments cut back on spending a bit, which may impact Hammond negatively.

Conclusion

Hammond is a good business that has historically been run well. The company is benefitting from structural tailwinds due to investment in the electrical grid which appears to be a long-term trend.

Overall, I'd lean bullish on Hammond, as I think the current valuation is pricing in a little bit of reversion. If we get that, well, investors may see the multiple climb, but the stock price stay flat. If, however, Hammond can maintain margins, then it seems likely the multiple and stock price increase as it becomes more clear what their sustainable earnings power ultimately is.

For further details see:

Hammond Power Solutions: Supplying The Electrical Grid With Critical Solutions