REIT - Hard Landing Now A Possibility

2023-10-22 09:00:00 ET

Summary

- U.S. equity markets slumped on a turbulent week as benchmark interest rates swelled to fresh multi-decade highs after Fed Chair Powell left open the possibility of additional Fed rate hikes.

- Following two weeks of modest gains, the S&P 500 slumped 2.4% this week, while the tech-heavy Nasdaq 100 dipped nearly 3%. The 10-Year Yield surged to the highest since 2002.

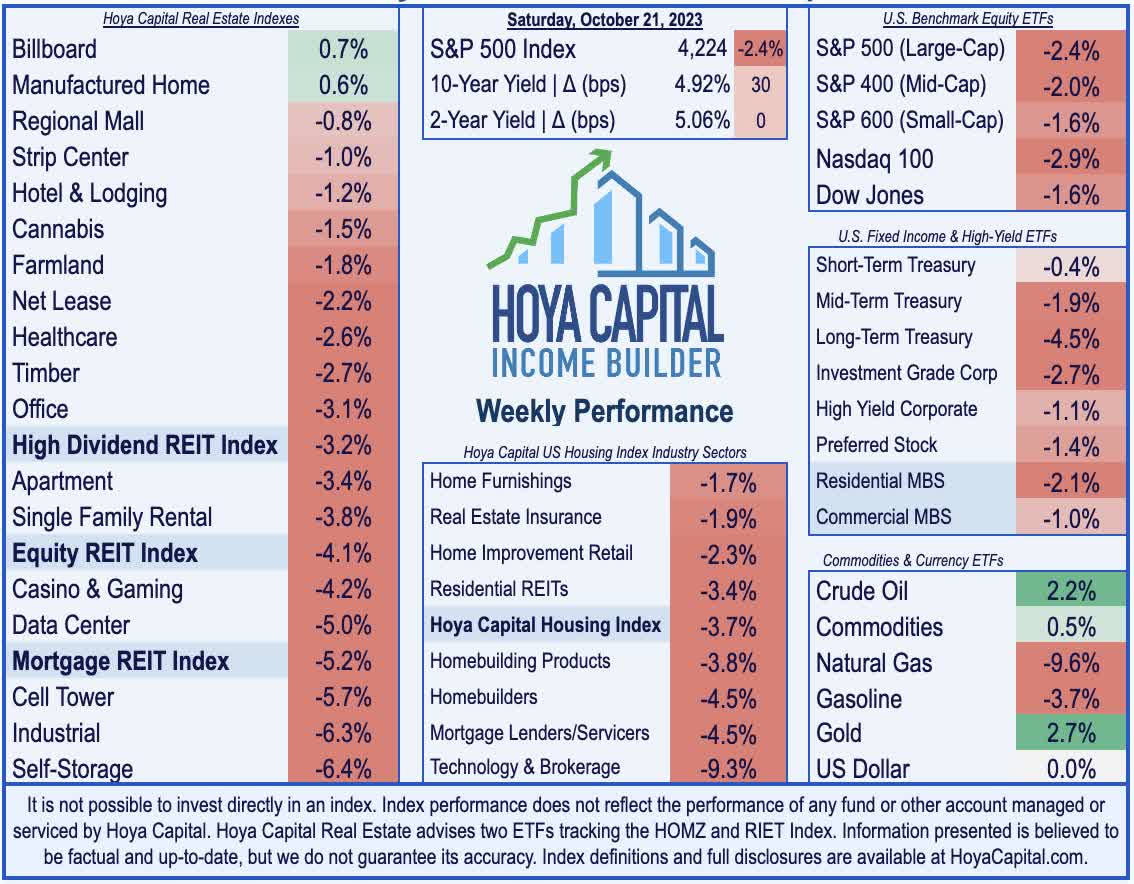

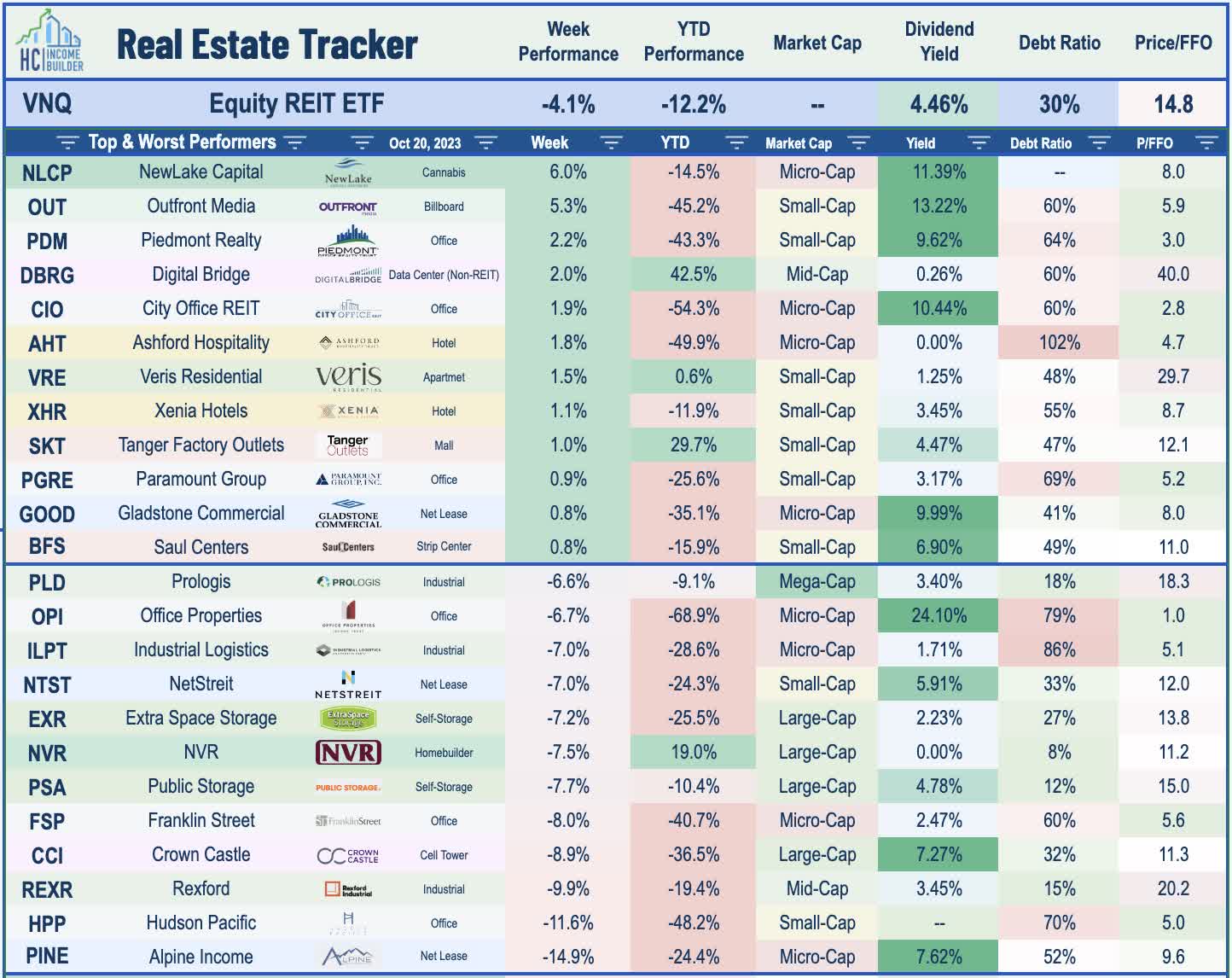

- Surging benchmark interest rates added renewed pressure to yield-sensitive segments of the equity market, overshadowing a decent start to REIT earnings season. The Equity REIT Index slumped 4.1%.

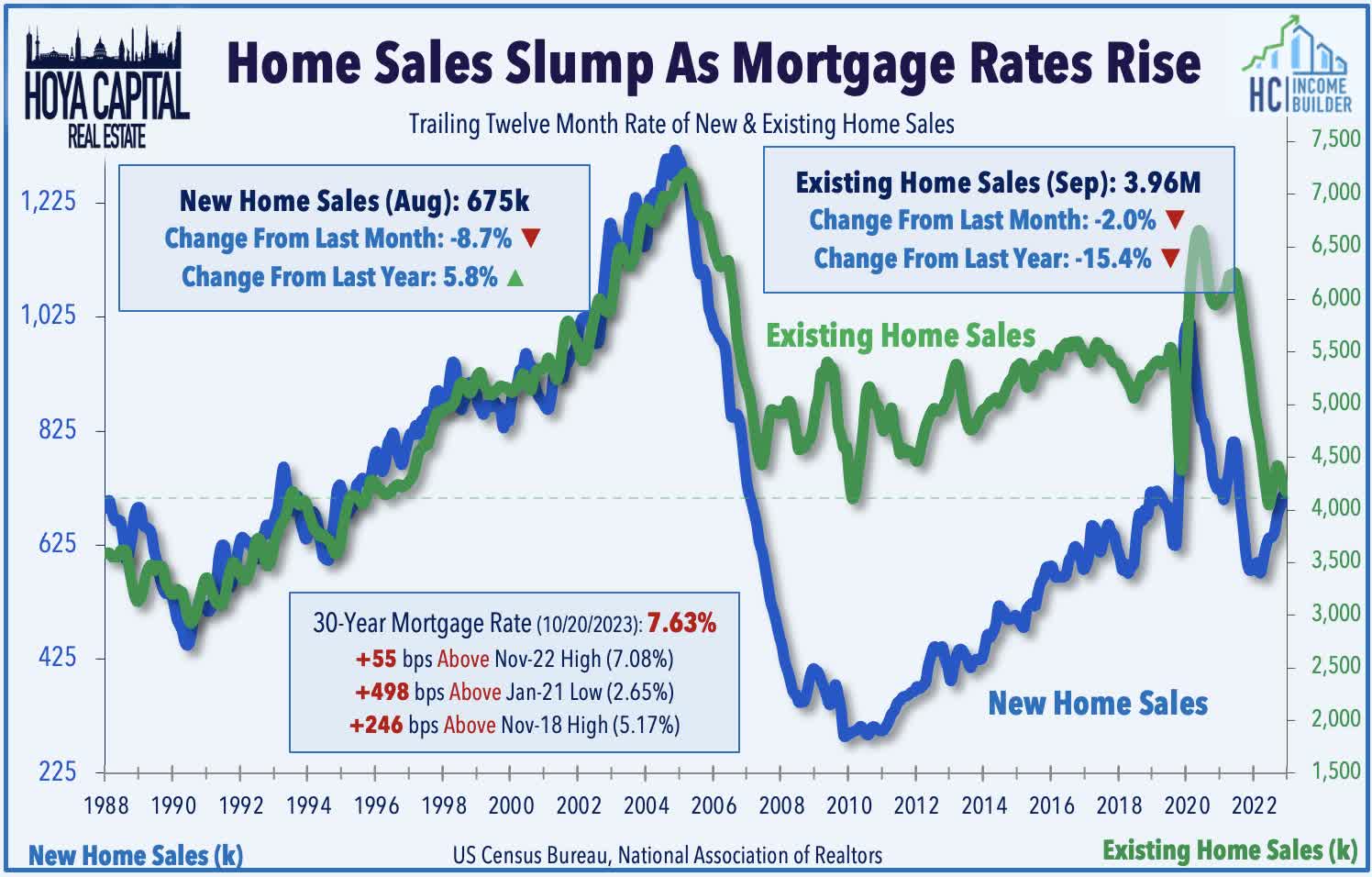

- Housing market data this week showed that rate-sensitive segments of the economy are certainly feeling the crunch of continued monetary tightening. Existing-home sales slid 15.4% from a year earlier as mortgage rates topped 8% - the second slowest month for home sales since 1995.

- Manufactured housing REIT Equity LifeStyle was an upside standout of the initial slate of REIT earnings reports, showing buoyant residential rent growth. Results were mixed across other property sectors as the effects of higher interest rates weighed the earnings outlook.

Real Estate Weekly Outlook

U.S. equity markets slumped on a turbulent week as benchmark interest rates swelled to fresh multi-decade highs after Fed Chair Powell left open the possibility of additional Fed rate hikes, while investors were unimpressed by the initial slate of corporate earnings results. An intensification of Middle East hostilities following terrorist attacks in Israel certainly didn't help matters either, lifting oil prices to the highs of the year as concern mounts that the United States could be dragged into another Middle East quagmire, a state of global affairs and macroeconomic conditions that bears a "spooky" resemblance to the months leading into 2007-2009 recession.

{kind=link}

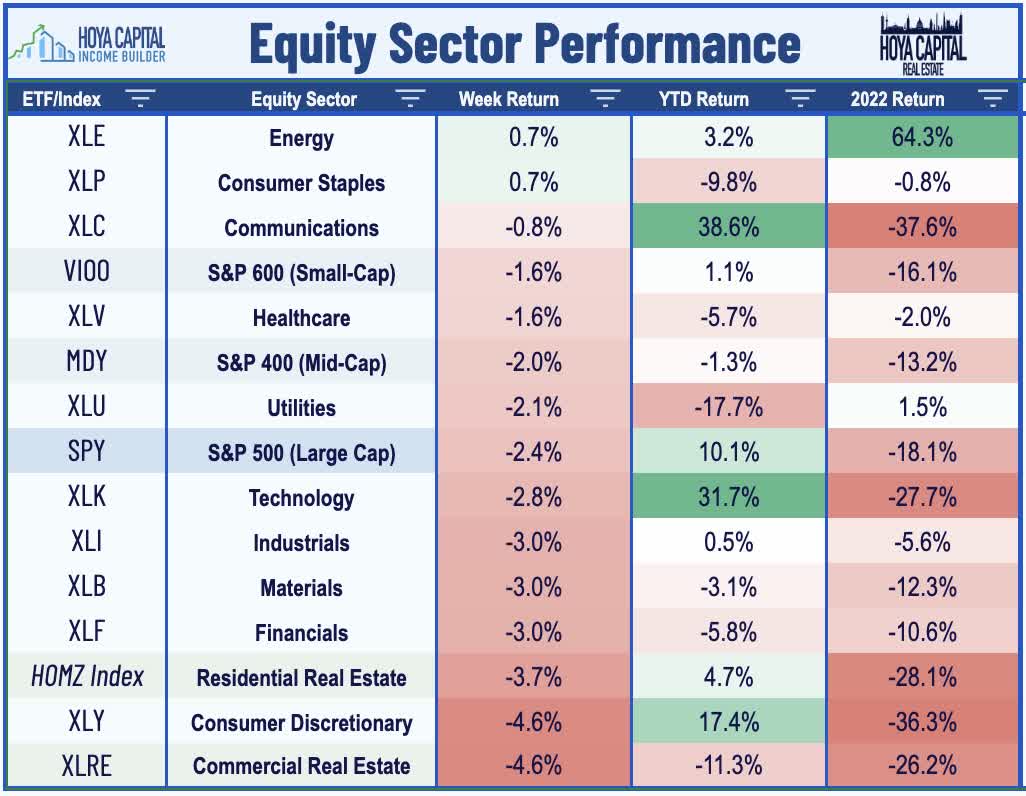

Following two weeks of modest gains, the S&P 500 slumped 2.4% this week, while the tech-heavy Nasdaq 100 dipped nearly 3%. Finishing roughly 5% below its intra-week highs, the Mid-Cap 400 declined 2.0% on the week, while the Small-Cap 600 posted a decline of 1.6%. Surging benchmark interest rates added renewed pressure to yield-sensitive segments of the equity market, overshadowing a decent start to REIT earnings season. The Equity REIT Index slumped 4.1% on the week, with 16-of-18 property sectors in negative territory, while the Mortgage REIT Index dipped 5.2%. Homebuilders also declined 4.5% this week after a weak slate of housing market data showed the early effects of surging mortgage rates, with Existing Home Sales slowing to levels last seen during the Financial Crisis.

{kind=link}

After several Fed officials appeared to adopt a more dovish tone last week in the wake of the terrorist attacks in Israel, we observed a notable reversion in tone this week back towards a hawkish policy stance. Traders keyed in on several remarks during the Fed Chair Powell's speech to the Economic Club of New York, including commentary suggesting that monetary policy was not “too tight" and that rates “haven’t been high enough for long enough.” After dipping 16 basis points last week, the 10-Year Treasury Yield surged 30 basis points to 4.92% - its highest close since 2002 - but the policy-sensitive 2-Year Treasury Yield remained at 5.06%. The market-implied probability of another Federal Reserve interest rate hike by January swung significantly during the week, briefly exceeding 50% mid-week before dipping back below 30% by Friday. The CBOE Volatility Index - a measure of equity market volatility - surged to the highest levels since mid-March during the height of the banking industry turmoil. Crude Oil finished the week higher by 2% amid concern over the implications of increased U.S. involvement in the Israel-Hamas conflict, while the U.S. Dollar Index snapped a 13-week winning streak.

{kind=link}

Real Estate Economic Data

Below, we recap the most important macroeconomic data points over this past week affecting the residential and commercial real estate marketplace.

{kind=link}

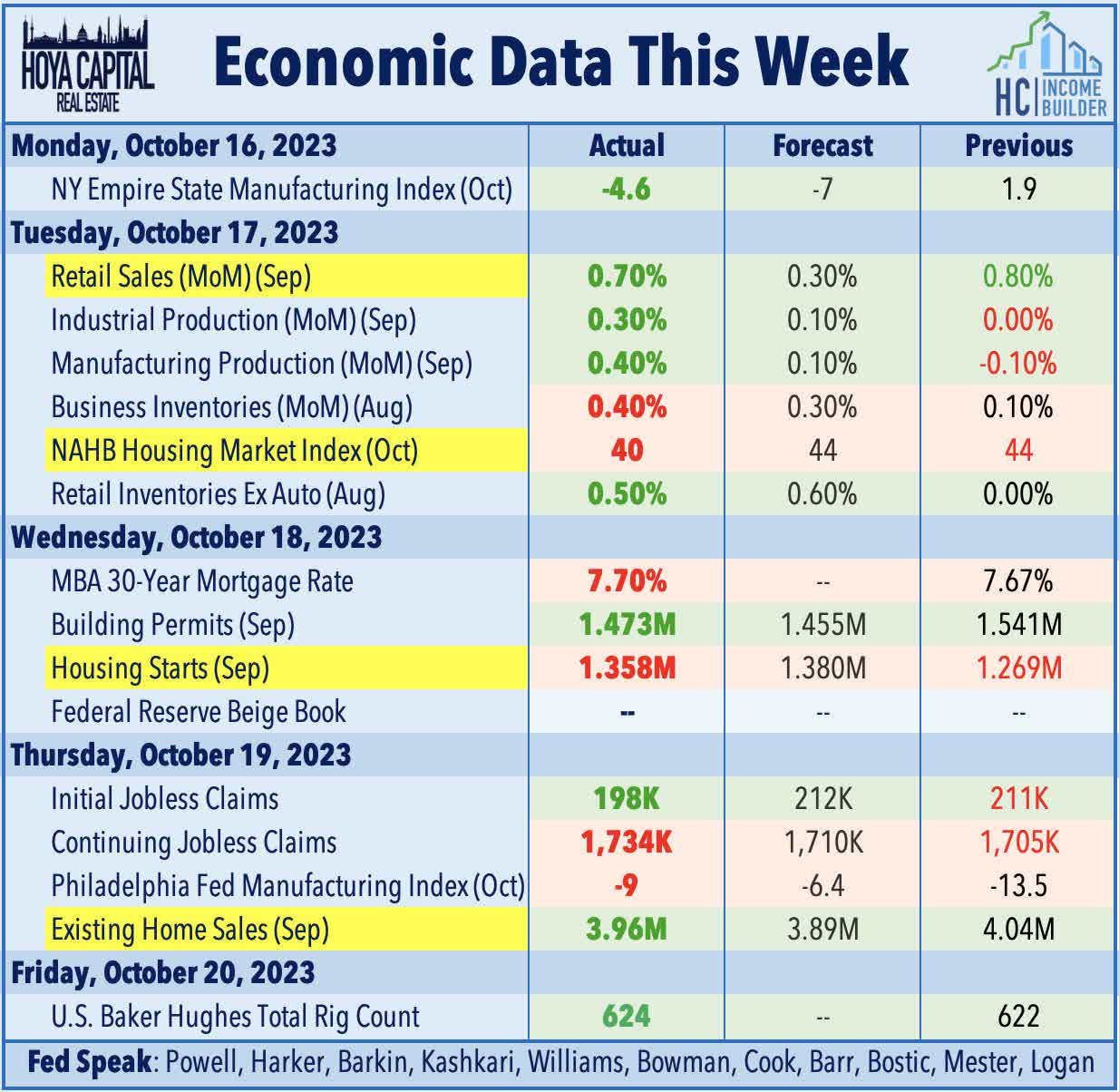

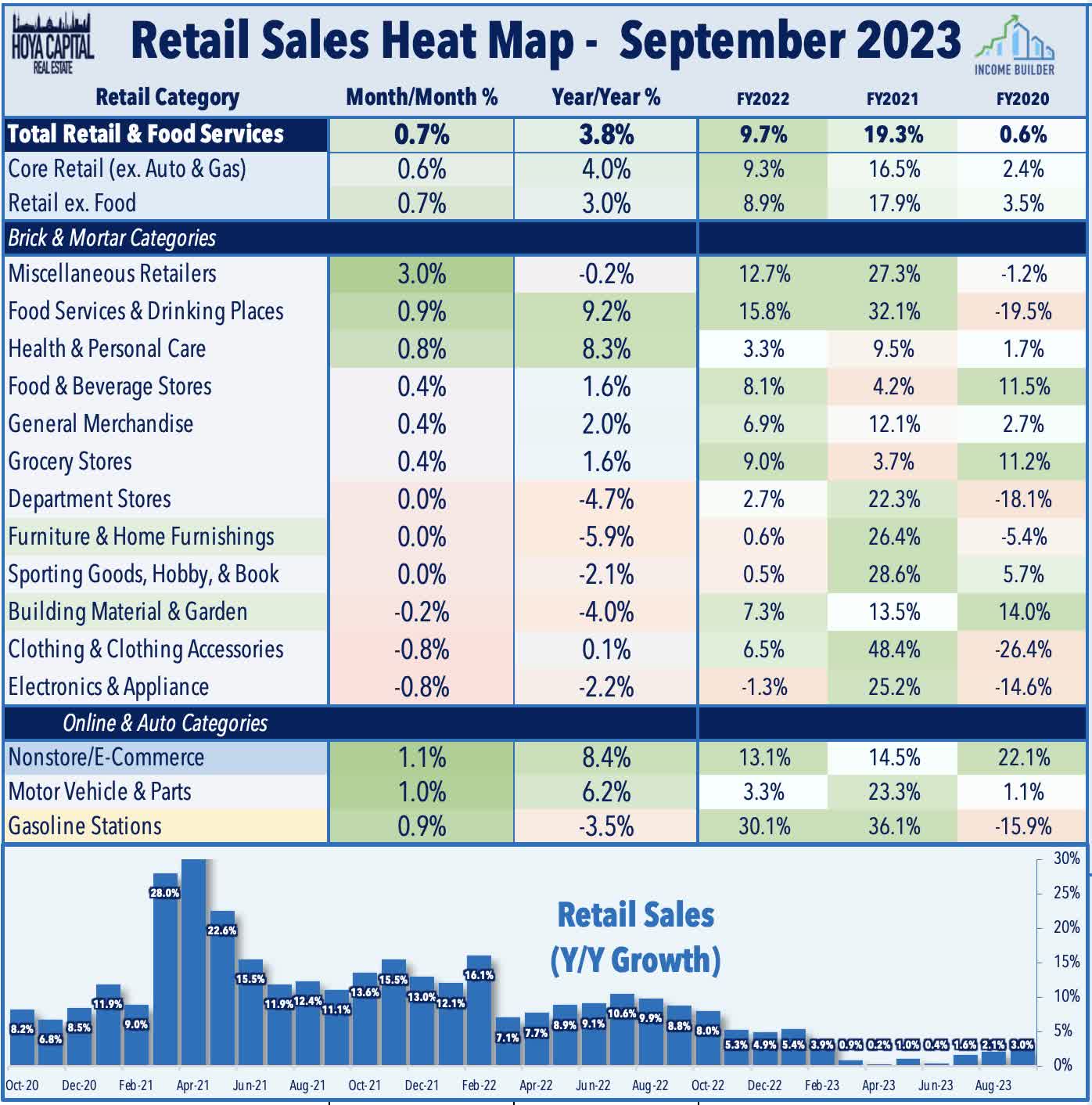

A key look into the health and sentiment of the U.S. consumer, retail sales data this week showed surprising broad-based strength in September, once again pushing back on slowdown calls and putting another Fed rate hike back in play. Total retail sales increased 0.7% in September compared to the prior month and 3.8% from last year - well above the 0.3% forecasted increase - while the prior two months were also revised higher. Spending strength was relatively broad-based with 9 of 13 categories posting sequential monthly increases. Retail Sales data showed continued softness from housing-related retailers, however, with the Building Materials retailers reporting that sales are down 4% from a year earlier, while Furniture retailers reported a 5.9% dip from last year, the weakest among the 13 categories.

{kind=link}

Housing market data this week showed that rate-sensitive segments of the economy are certainly feeling the crunch of continued monetary tightening. Existing-home sales slid 15.4% from a year earlier in September to a seasonally adjusted annual rate of 3.96 million - which marked the second slowest month for home sales since 1995, eclipsed only by one month - August 2010 - at the depths of the GFC-induced slowdown. Record-low inventory levels of existing single-family homes, however, has kept a floor on home values and helped to sustain some base level of demand for new home construction in the face of these substantial interest rate headwinds. Total housing inventory was down 8.1% from one year ago, while unsold inventory sits at a 3.4-month supply at the current sales pace - well below the historical average of roughly 6 months. Despite the sluggish overall sales pace, 69% of homes sold in September were on the market for less than a month.

{kind=link}

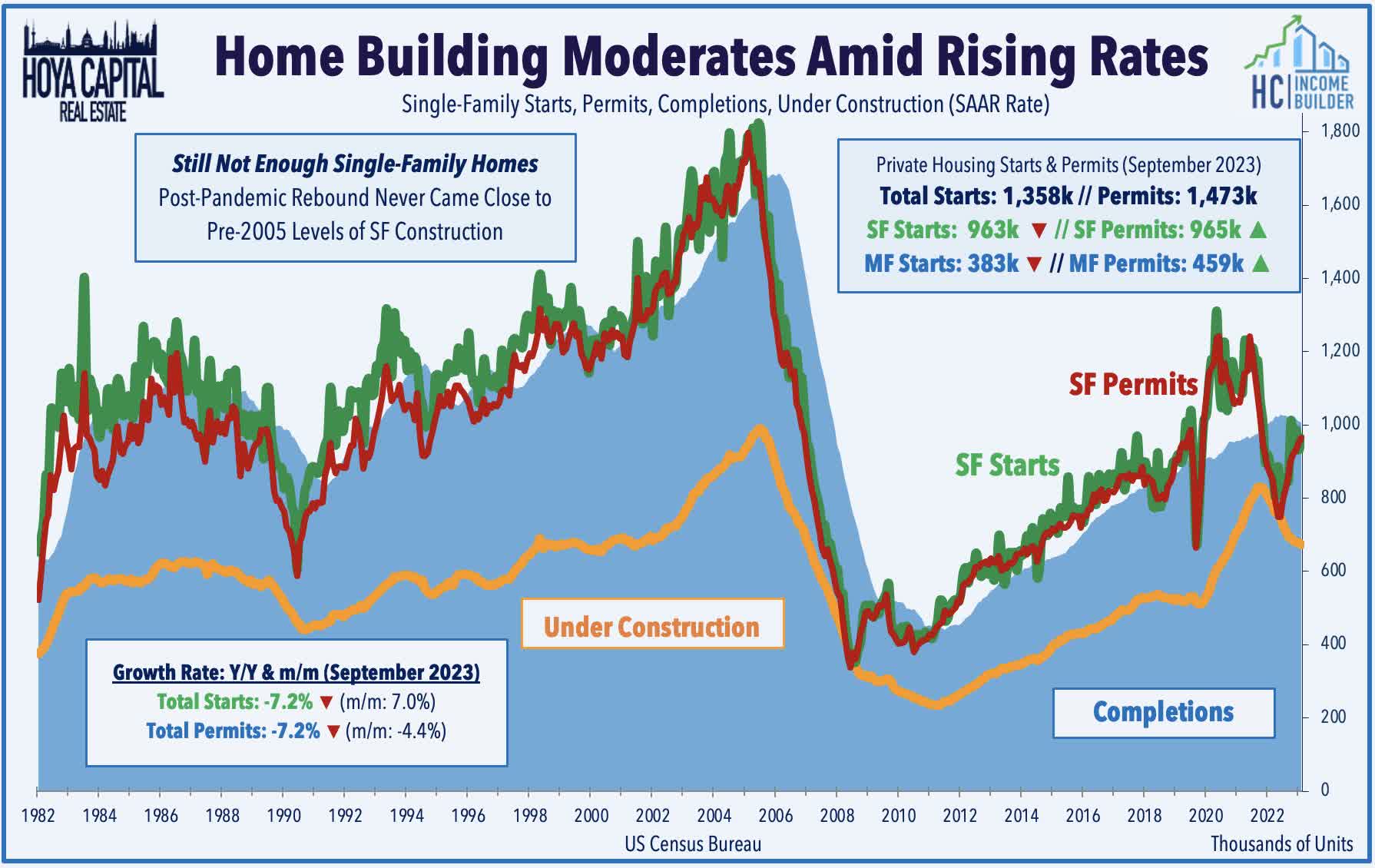

Inventory levels are unlikely to improve anytime soon, as housing starts declined 7% in September from the same period last year to a 1.36M annualized rate - shy of consensus estimates of 1.38M - while August construction data was revised lower as well. Multifamily construction activity has seen an especially sharp moderation in recent months, with starts cooling to a 383k annualized rate in September - down over 30% from the same month last year. The NAHB Homebuilder Sentiment report - a leading indicator of new housing construction activity - fell rather sharply in October as well - a third straight month of declines following a streak of seven-straight monthly increases. The dip in sentiment was attributed to the recent leg higher in mortgage rates, eclipsing 8% this week, according to Mortgage News Daily. The Homebuilder Sentiment Index fell to 40 in October from 44 in September, with all three sub-components posting declines of at least 4 points. The report showed that 32% of builders said they cut home prices in October - matching the highest rate since December - with an average price discount of 6%.

{kind=link}

Equity REIT Week In Review

Best & Worst Performance This Week Across the REIT Sector

{kind=link}

Manufactured Housing : Beginning with the winners this week, Equity LifeStyle ( ELS ) was one of the few REITs in positive territory after it kicked-off REIT earnings season with a solid report showing continued buoyancy in residential rent growth. ELS maintained the midpoint of its full-year FFO outlook - which calls for full-year FFO growth of 6.3% - as strength in its core manufactured housing ("MH") segment offset continued weakness in its transient recreational vehicle ("RV") segment. ELS maintained its full-year outlook for MH same-store revenue growth at 6.8%, but downwardly revised its RV & Marina outlook to 3.8% - lower by 80 basis points - as seasonal and transient RV revenues were down over 10% from last year, pressured by rising fuel prices and a post-pandemic normalization in RV utilization. Excluding the struggling transient RV component, full-year revenues in the RV & Marina segment are expected to increase 8.6% for the year. ELS also noted that it will begin sending renewal offers to its MH residents this month for the 2024 period, with average rent increases of 5.4%. ELS has set annual rates on 95% of its annual RV sites, with average rent increases of 7.0%.

{kind=link}

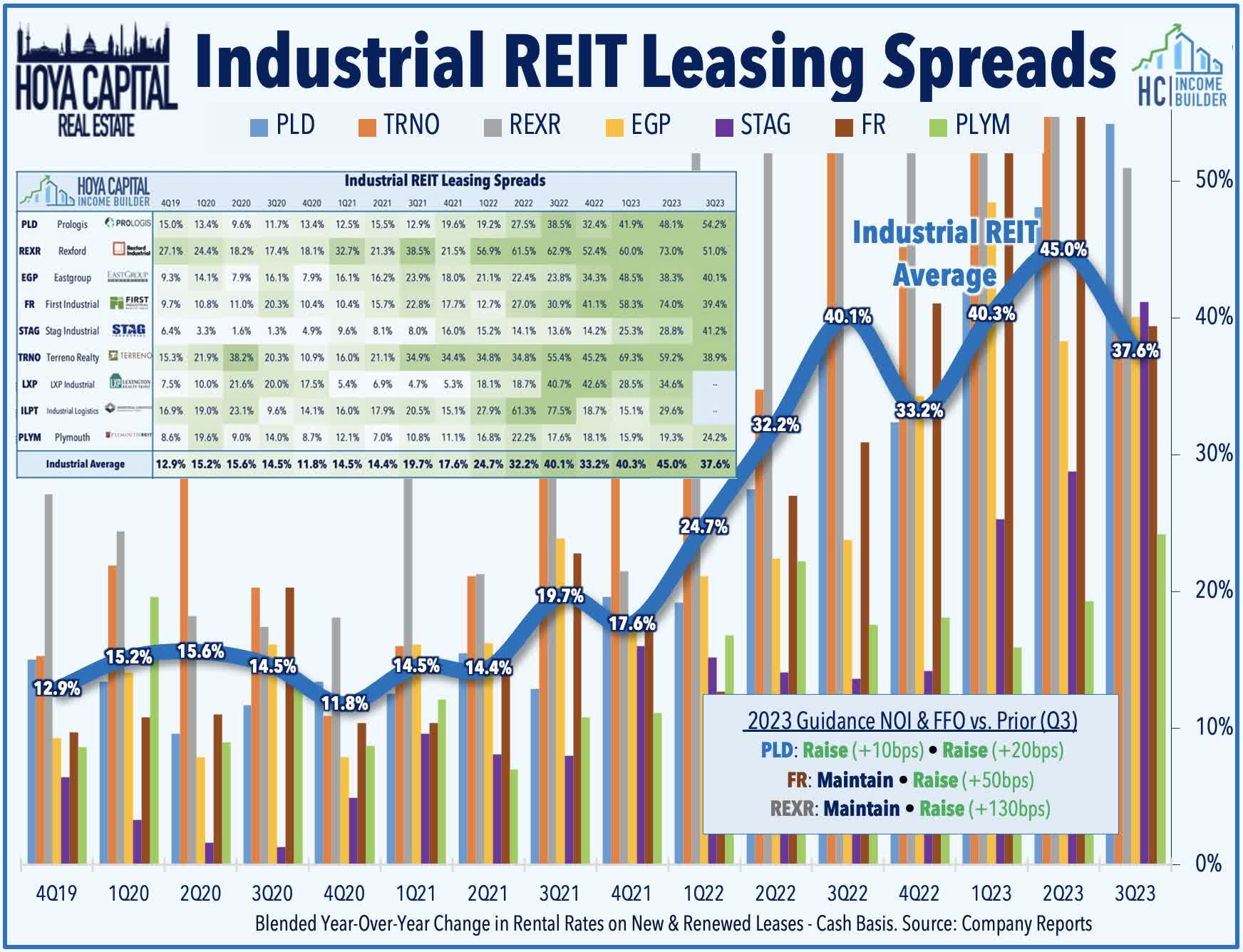

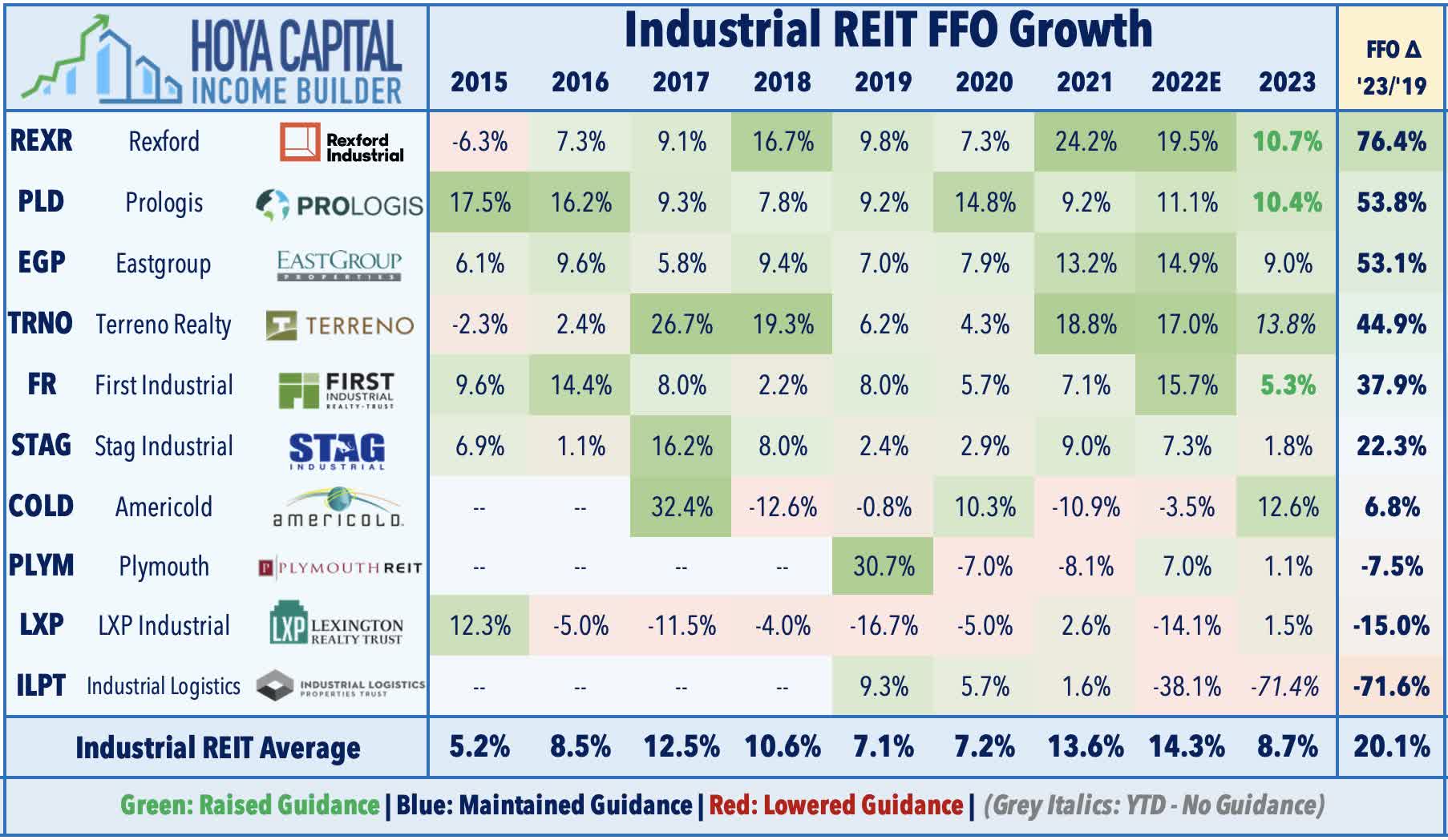

Industrial : A trio of industrial REITs reported results this week, all three of which posted declines of at least 6% despite a relatively strong slate of results. Prologis ( PLD ) declined 6% this week despite reporting "beat and raise" results but reiterated its expectation that elevated supply growth will negatively impact market fundamentals in the coming quarters. Interestingly, this cautious commentary was really nowhere to be seen in the third-quarter metrics or the updated full-year outlook, which continued to reflect extremely strong supply/demand conditions for logistics space, especially in the United States. Fueled by a record-setting cash re-leasing spread of 54.2% - led by a 63.1% increase in the U.S. - PLD now sees FFO growth of 10.4% this year - up 20 basis points from its prior forecast - and expects NOI growth of 9.9% - up 10 basis points from last quarter. Prologis also upwardly revised its forecasted spending on development starts and acquisitions. PLD expects completions to outpace net absorption by 150-200M square feet over the next three quarters but expects that trend to reverse by mid-2024, with demand exceeding supply by 75-125M SF in the following three quarters.

{kind=link}

While Prologis recorded very strong rent growth in its Sunbelt and Mid-Atlantic regions, Prologis specifically cited Southern California as an area of weakness, noting that market rents declined 2% in SoCal "as it continues to adjust to higher levels of vacancy." Rexford ( REXR ) - which focuses exclusively on the Southern California region - plunged 10% this week after reporting mixed results, raising its full-year FFO outlook but recording a sequential deceleration in leasing activity. REXR noted that it leased 1.5M SF in Q3 with cash rent increases of 51.4% - down from the 74.8% increase achieved on 2.1M SF of activity in the prior quarter. REXR still lifted its full-year FFO growth outlook to 10.7% - up 130 basis points from last quarter - but maintained its full-year NOI growth outlook at 9.9%. First Industrial ( FR ) - which owns a more geographically diverse portfolio - declined 6% after reporting similarly mixed results. FR lifted its full-year FFO growth outlook to 5.3% - up 50 basis points from last quarter - but maintained its full-year NOI growth outlook at 8.3%. FR noted that cash rental rates increased 39.4% - down from the record-high of 74.1% in the prior quarter. FR commented, "We're seeing tenants being cautious and delaying their decision-making, as tenants are hesitant to make commitments given the macroeconomic and geopolitical issues."

{kind=link}

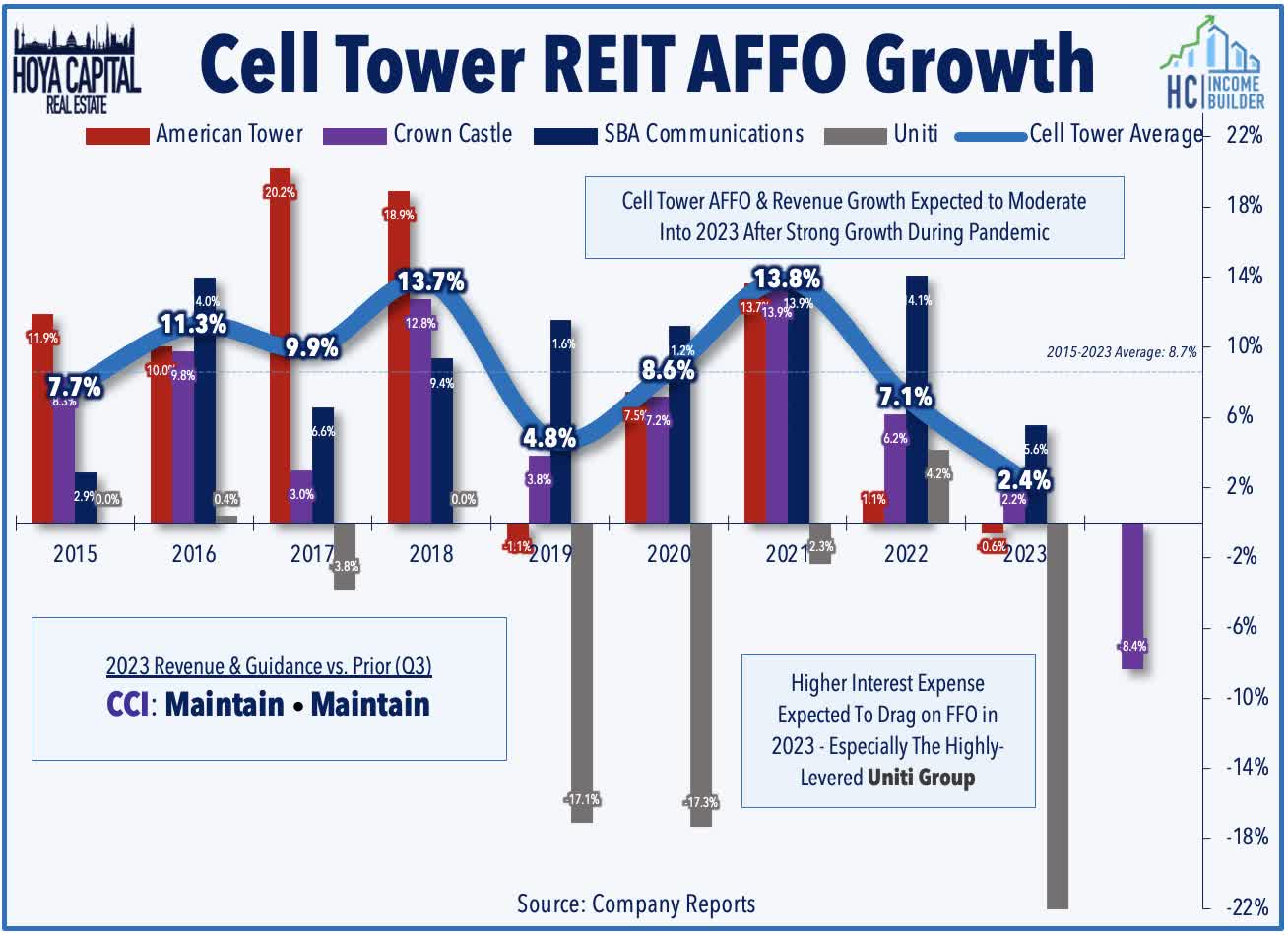

Cell Tower : Crown Castle ( CCI ) - which has already dipped more than 35% this year on impacts from higher rates and a slowdown in 5G network deployment - declined another 8% this week after reporting mixed results, maintaining its full-year 2023 outlook, but provided a downbeat initial 2024 outlook driven by higher interest expense. CCI - the second-largest cell tower owner in the U.S. - continues to expect FFO growth of 2% this year, but forecasts an 8% decline in FFO in 2024, commenting that it expects the "low-point of AFFO to occur during the first half of 2024, with growth expected in the second half of the year and beyond." Despite having an investment-grade balance sheet with 86% of its debt at fixed interest rates, the updated outlook notes that interest expense is still expected to soar 22% in 2023 from a year earlier - amounting to a $0.35/share negative impact - and is expected to rise by another 12% in 2024 - an additional $0.12/share drag. Property-level metrics remain steady, with CCI forecasting organic growth (excluding Sprint cancellations) of 4.8% next year - up from 4.1% in 2023 - comprised of 4.5% growth from towers, 13% from small-cells, and 3% from fiber.

{kind=link}

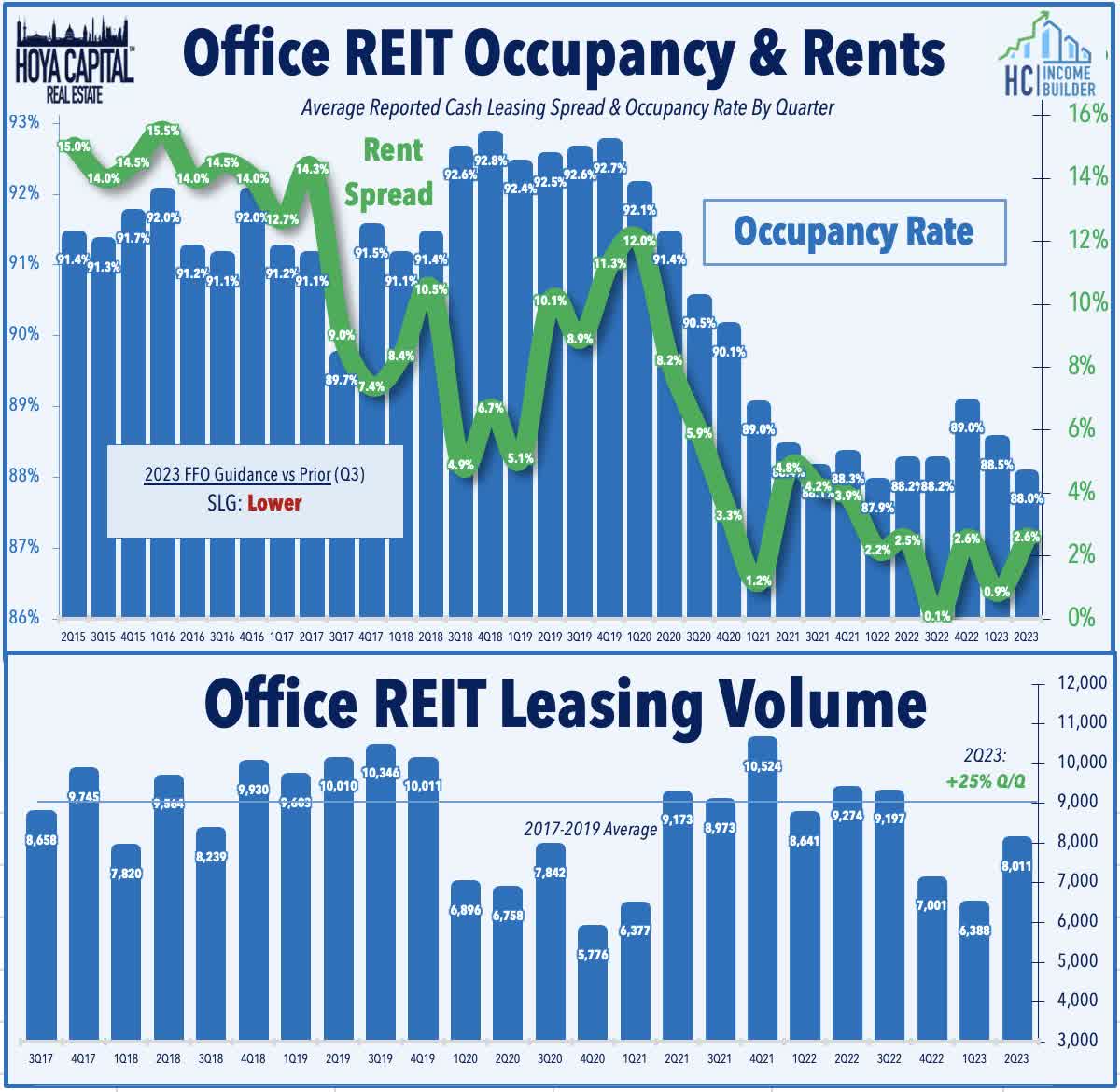

Office : NYC-focused SL Green ( SLG ) dipped 6% this week after it kicked off office REIT earning season with a weak report. SL Green - which owns 59 buildings in Manhattan and the NYC metro area - reported unimpressive results, lowering its full-year FFO guidance to $5.15 at the midpoint - representing a -23% decline from last year - down from its prior outlook calling for an -18% FFO decline. Like Crown Castle, interest expense has soared more than 50% compared to last year, representing a roughly $1.15/share full-year drag compared to 2022. Leasing volumes were light at 356k square feet, down from 411k last quarter and 505k in Q1, bringing the trailing four-quarter average to levels that are 34% below the pre-pandemic average from 2017-2019. For reference, the average coastal office REIT reported that leasing volumes were 24% below pre-pandemic levels on a TTM basis last quarter, while coastal office REITs reported volumes that were only 5% below pre-pandemic levels. SLG's occupancy rate ticked slightly higher, however, to 89.9% from 89.8% in the prior quarter, but reported a 3.8% decline in renewal rents, dragging its year-to-date spreads to -0.4%.

{kind=link}

Casino : VICI Properties ( VICI ) declined 5% this week after it announced that it acquired the real estate assets of 38 bowling alleys from Bowlero Corp - the largest operator of bowling alleys in the United States with roughly 350 locations - in a sale-leaseback transaction for an aggregate purchase price of $432.9M. The triple-net master lease will have an initial term of 25 years, with six 5-year tenant renewal options, and will escalate at the greater of 2.0% or CPI (subject to a 2.5% ceiling). VICI's first major acquisition outside of its core casino property sector focus, the deal was completed at an acquisition cap rate of 7.3% based on total annual rent of $31.6M. Bowlero will represent 1% of VICI’s rent roll, and VICI will have the right of first offer for eight years to acquire additional real estate assets of Bowlero. VICI - which already owns a relatively dominant share of casino assets in the Las Vegas strip following a half-decade of rapid external growth - has noted in recent earnings calls that it is exploring "experiential" asset classes with similar characteristics as the casino sector: lower than average cyclicality, low secular threat, proven durability, and favorable supply/demand dynamics.

{kind=link}

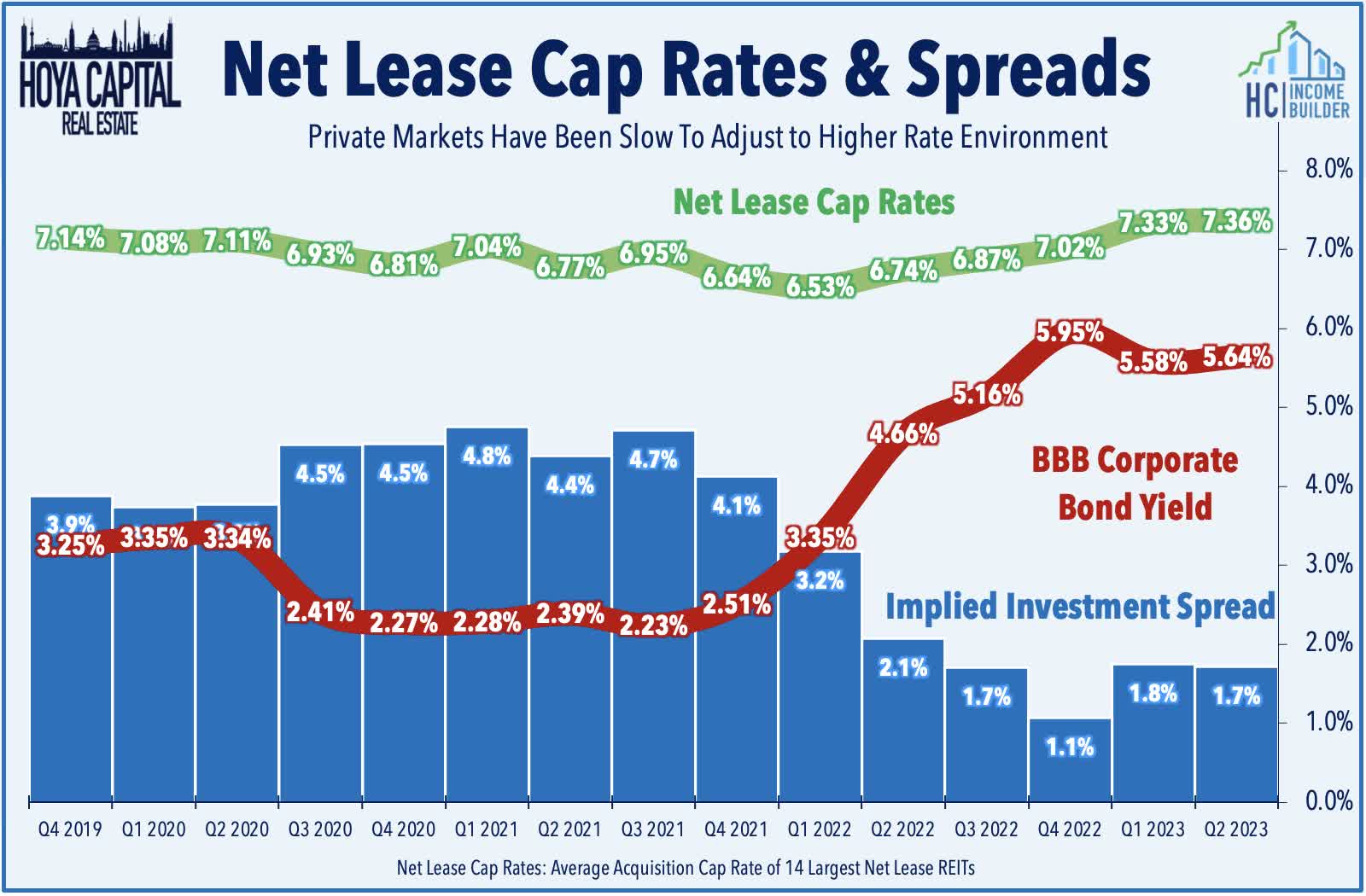

Net Lease : Alpine Income ( PINE ) dipped 15% this week after reporting soft results and lowering its full-year FFO outlook. Pressured by rising interest expense and the bankruptcy of one tenant, PINE now expects its full-year AFFO to dip 16.9% this year - down from its prior expectations of a 13.3% decline. PINE's occupancy rate ticked down to 99% from 100% last quarter as the result of the bankruptcy of Mountain Express, which operated seven Valero-branded convenience stores. PINE slowed its acquisition activity in Q2, noting that the net lease sector has been "slow to reprice in the rising interest rate environment." PINE acquired three properties for a total of $19.4M at an acquisition cap rate of 9.0%, while it sold eight properties for $20.6M at an average cap rate of 6.3%. Providing additional color on the broader net lease transactions environment, PINE noted, "the market's very tepid in the standoff between buyers and sellers" and noted that the challenging debt market will be "a factor in creating some opportunities." We'll hear results from several of the largest net lease REITs this coming week, including Agree Realty ( ADC ), EPR Properties ( EPR ), and Essential Properties ( EPRT ).

{kind=link}

Earnings season kicks into gear next week with results from nearly a third of the REIT sector and a half dozen of the nation's largest homebuilders. In our REIT Earnings Preview, we noted that the broader real estate sector once again enters earnings season on a skid, with the Vanguard Real Estate ETF ( VNQ ) dipping to the lowest levels since the depths of the pandemic in May 2020 this week on a price return basis. While property-level fundamentals have remained solid across most property sectors this year, even the most well-capitalized real estate owners have been unable to escape the gravitational force on valuations of "higher for longer" monetary policy on the naturally rate-sensitive real estate sector. Distress has generally remained isolated to the most debt-burdened private market portfolios, but the refinancing clock is ticking ever louder for even some of the most conservatively managed REITs. Capitulation from debt-burdened private portfolios should eventually create consolidation opportunities for well-capitalized REITs, similar to the dynamics seen in the early 1990s when a near-shutdown in CRE debt availability sparked the dawn of the 'Modern REIT Era' - a time remembered as a 'golden age' for public equity real estate.

{kind=link}

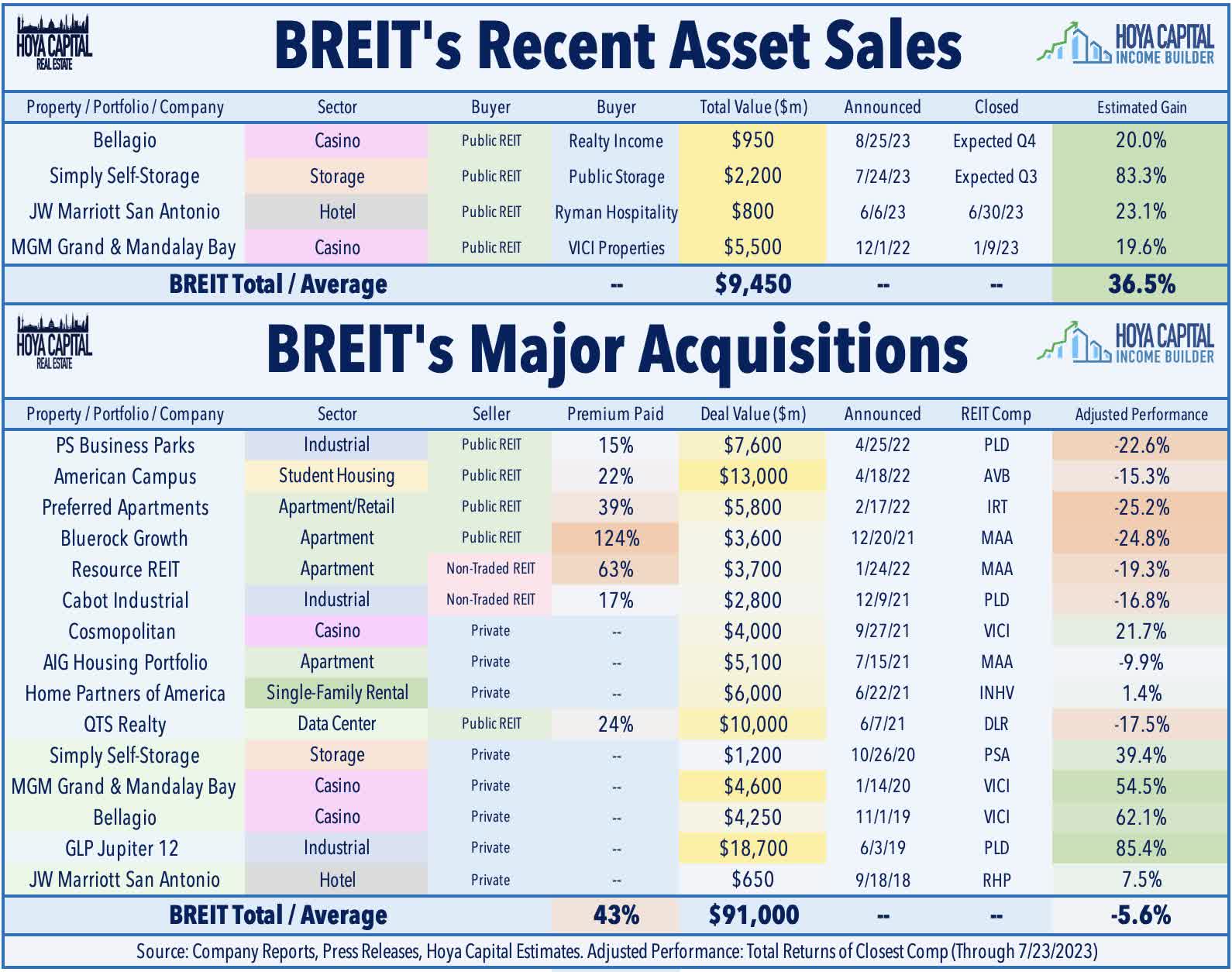

On the other side of that trade, and speaking of highly-levered private equity firms exposed to the impacts of higher rates, Blackstone ( BX ) plunged 10% this week after reporting soft earnings results, dragged down by continued outflows in its once-high-flying non-traded real estate platform, BREIT. Earlier this month, BX reported that redemption requests exceeded the fund's monthly and quarterly limits once again in September, an eleventh-straight month that the firm has had to limit investor withdrawals. BREIT caps redemptions at 2% of NAV per month and 5% of NAV per quarter. Since last November, when it began to limit these redemption requests, BREIT has fulfilled $11.3B of these withdrawal requests - a fraction of the total amount requested. In September, BREIT fulfilled only 29% of these withdrawal requests. Notably, investors who have filed redemption requests each month since last November have still not received all their money back. To meet these redemption requests, BREIT has sold roughly $10B in assets to public equity REITs since last December, with more likely in the pipeline.

{kind=link}

Mortgage REIT Week In Review

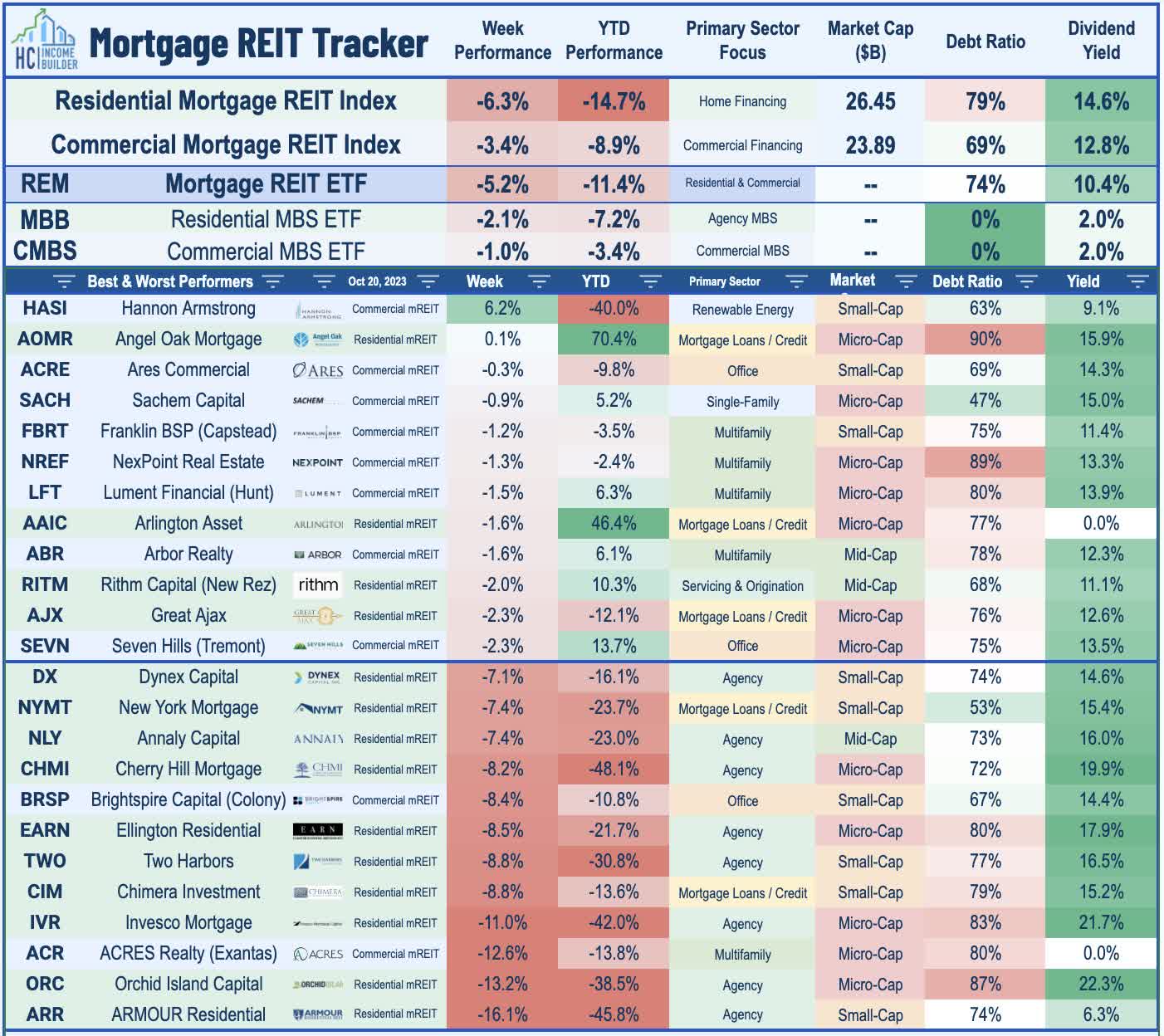

Pressured by the jump in benchmark interest rates and downward pressure on residential and commercial MBS valuations, mortgage REITs post sharp declines this week ahead of the start of earnings season in the week ahead. Declining in four of the past five weeks, the iShares Mortgage Real Estate ETF ( REM ) slid more than 5% this week, with particularly sharp pressure on residential mREITs. The iShares MBS ETF ( MBB ) - an unlevered benchmark tracking agency RMBS valuations - slid another 2.1% this week and is now lower by over 7% this year, which would be the second-worst year on record behind last year. Since the start of 2022, the MBB Index has plunged nearly 20% on a total return basis (-15% total returns), a decline three times deeper than its next worst peak-to-trough decline seen in 2013. Interest rate volatility - as measured by the MOVE Index - swelled to the highest levels since May, resulting in particularly sharp pressure on some of the more highly-levered agency-focused residential mREITs, including Orchid Island ( ORC ), Invesco Mortgage ( IVR ), and ARMOUR Residential ( ARR ).

{kind=link}

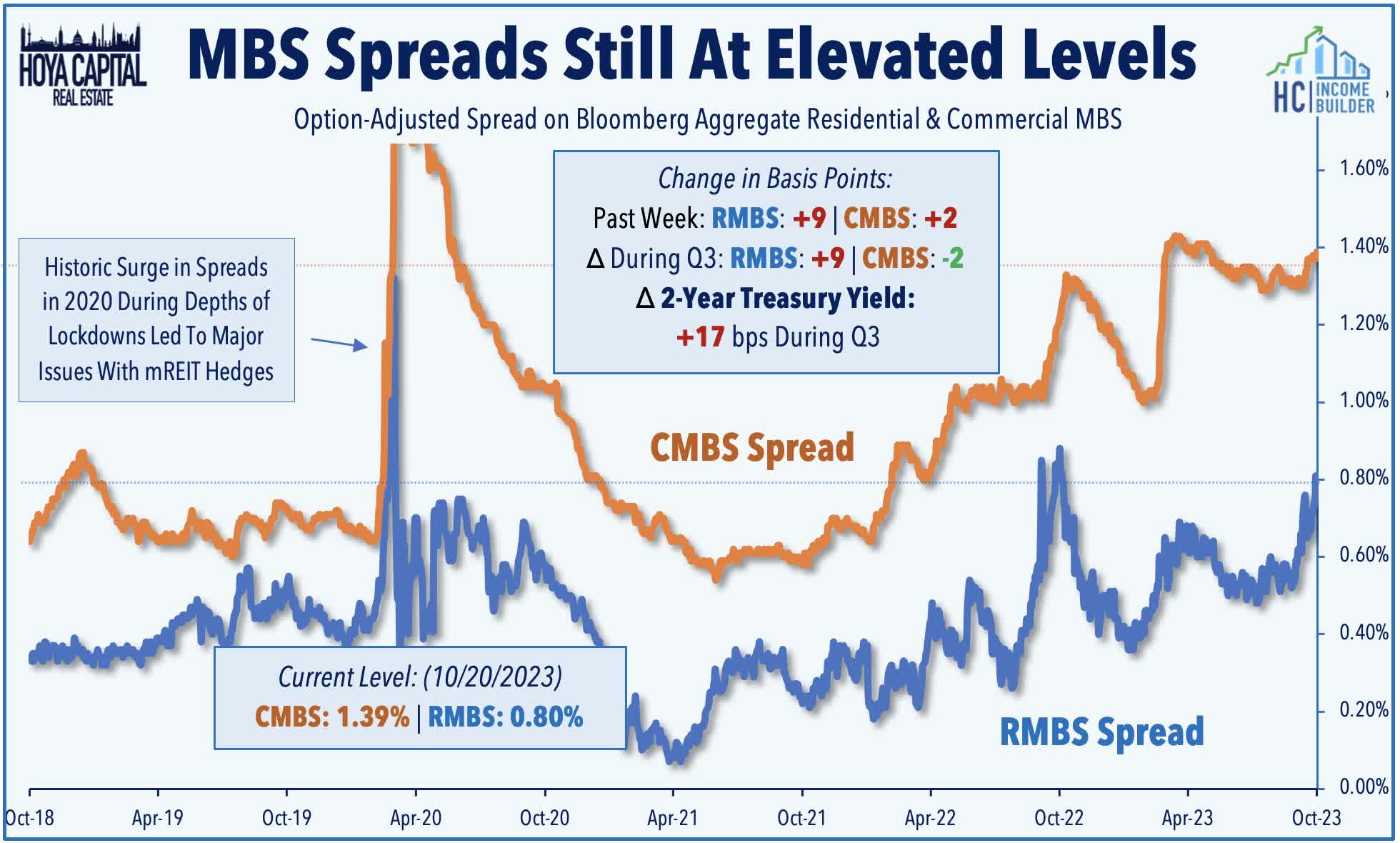

We'll hear earnings results from the initial half-dozen mREITs in the week ahead, including Dynex Capital ( DX ) and KKR Real Estate ( KREF ) on Monday; Blackstone Mortgage ( BXMT ) and Annaly Capital ( NLY ) on Tuesday; Orchid Island ( ORC ) on Thursday, and Ladder Capital ( LADR ) on Friday. Book Values remain in focus amid the recent resurgence in interest rate volatility and broader weakness on CMBS and RMBS valuations. Spreads on mortgage-backed bonds ("MBS spreads") - an important input into Book Value models - have trended significantly higher over the past month. Since the end of Q2 on June 30th, RMBS spreads have widened by 28 basis points to 0.80%, while CMBS spreads have widened by 6 basis points to 1.39%. Benchmark interest rates - the other critical input affecting Book Values - have also increased during this period, with the 2-Year Yield higher by 19 basis points.

{kind=link}

2023 Performance Recap

Nearing the end of October, the Equity REIT Index is now lower by 12.2% on a price return basis for the year (-8.8% on a total return basis), while the Mortgage REIT Index is lower by 8.9% (-4.3% on a total return basis). This compares with the 10.1% gain on the S&P 500 and the 1.3% decline for the S&P Mid-Cap 400 . Within the real estate sector, just 3-of-18 property sectors are still in positive territory on the year, led by Data Center, Single-Family Rental, and Healthcare REITs, while Cell Tower and Specialty REITs have lagged on the downside. At 4.92%, the 10-Year Treasury Yield has surged by 105 basis points since the start of the year - up sharply from its 2023 intra-day lows of 3.26% in April. Following the worst year for bonds in decades, the Bloomberg US Bond Index is lower again this year, producing total returns of -3.1% thus far. WTI Crude Oil - perhaps the most important inflation input - is higher by 15.1% this year, but Natural Gas prices have plunged 52%.

{kind=link}

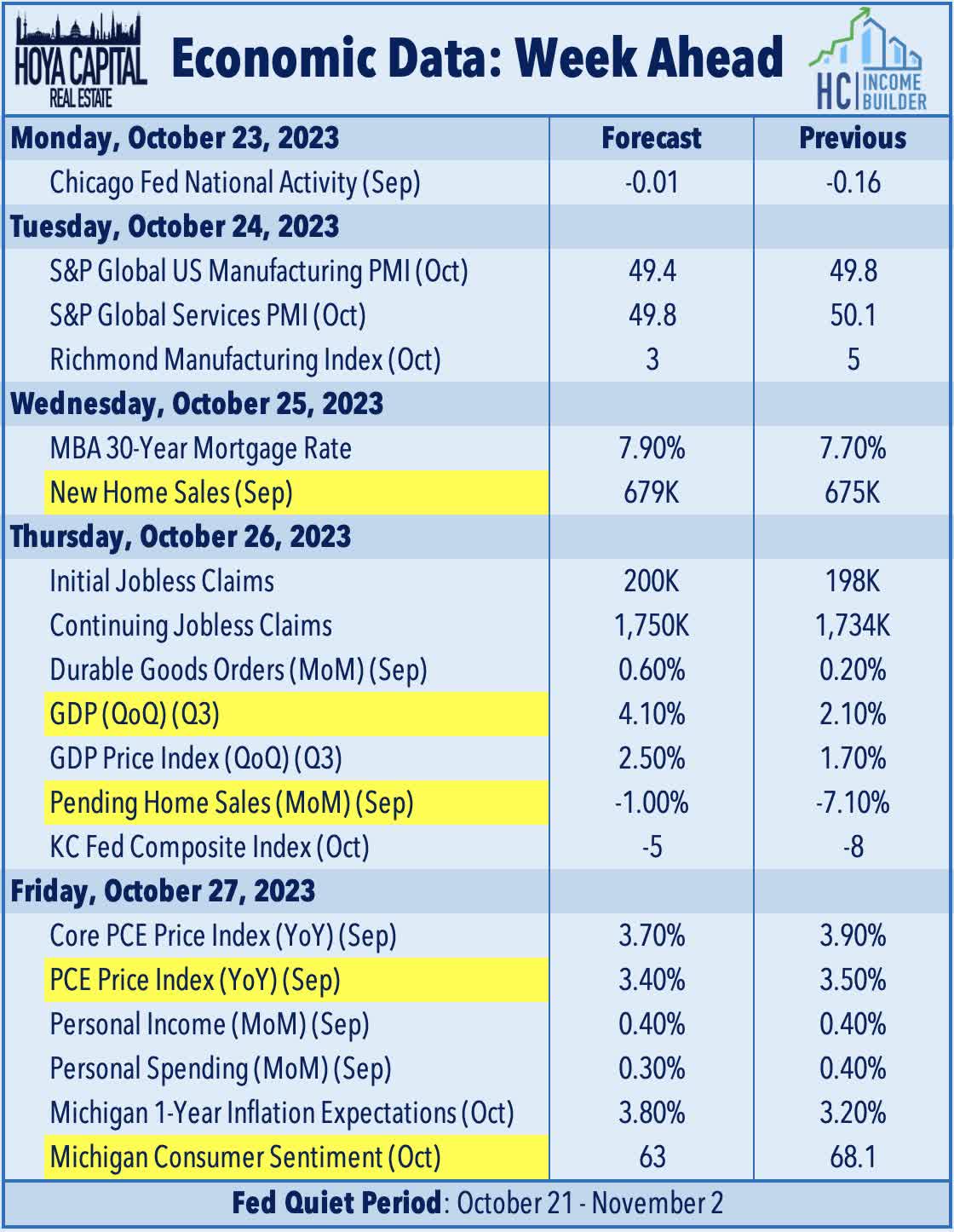

Economic Calendar In The Week Ahead

As the Federal Reserve enters its quiet period ahead of its November meeting, we'll see another jam-packed week of economic data and corporate earnings reports in the week ahead. The most closely-watched report of the week comes on Friday with the PCE Price Index - the Fed's preferred gauge of inflation - which is expected to show a year-over-year increase of 3.4% - down from the 3.5% increase last month and down sharply from the 7.0% rate seen a year ago. We'll also get our first look at third-quarter Gross Domestic Product, which is expected to show an expansion of 4.1% - confirming the surprising reacceleration in economic activity seen during the summer months. In the six quarters since Q1 2022, Real GDP growth has averaged just 1.2% - the weakest 18-month period of growth since 2010. The state of the U.S. housing market also remains in focus - the sector that had briefly emerged from a year-long rate-driven recession from mid-2021 through mid-2022, with New Home Sales data on Wednesday and Pending Home Sales on Thursday. The largest single-family homebuilders have, so far, been able to cope with multi-decade-high mortgage rates by leveraging their platform's scale to offer more attractive financing options than what's currently available for prospective homebuyers in the traditional existing home sales market.

{kind=link}

For an in-depth analysis of all real estate sectors, check out all of our quarterly reports: Apartments , Homebuilders , Manufactured Housing , Student Housing , Single-Family Rentals , Cell Towers , Casinos , Industrial , Data Center , Malls, Healthcare , Net Lease , Shopping Centers , Hotels , Billboards , Office , Farmland , Storage , Timber , Mortgage , and Cannabis.

Disclosure : Hoya Capital Real Estate advises two Exchange-Traded Funds listed on the NYSE. In addition to any long positions listed below, Hoya Capital is long all components in the Hoya Capital Housing 100 Index and in the Hoya Capital High Dividend Yield Index . Index definitions and a complete list of holdings are available on our website.

{kind=link}

For further details see:

Hard Landing Now A Possibility