JMIA - Has Jumia Technologies Turned The Corner?

- Cost reductions and reiterated revenue guidance provide signs that Jumia Technologies may have finally turned the corner.

- Growth underpinned by customer growth and increased order rates.

- With JMIA stock's valuation likely successfully testing rock bottom levels, 2023 may offer more upside surprises.

It has been a minute since Jumia Technologies ( JMIA ) generated some sustained excitement following an earnings report. JMIA's second quarter earnings for 2022 included four key highlights:

- Tightened cost controls promising an end to growing quarterly losses

- Reiterated 2022 revenue guidance of $200M to $220M

- Strong growth in orders per active user

- Strong revenue growth

While there were a few blemishes, such as slower sequential growth, on balance JMIA looks like it has turned the corner from an operational standpoint. In turn, the stock also looks like it has turned the corner after a long period of suffering.

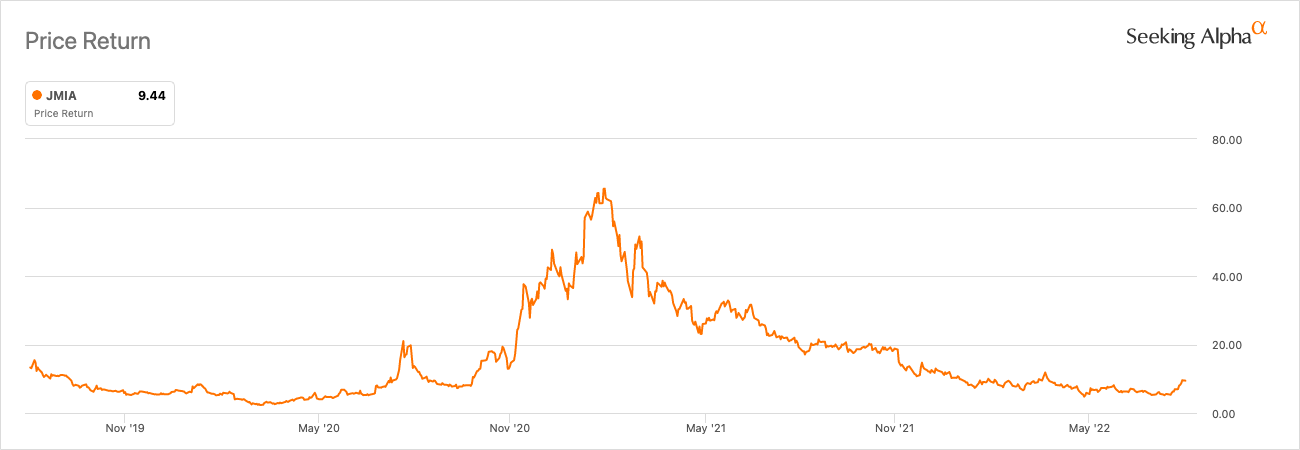

JMIA's price action looks like it has finally turned the corner. (Seeking Alpha)

{kind=link}

Jumia's Costs and Profits

Jumia reported two surprises on the cost front. The company slashed sales and advertising expenses to 18% below the lower end of first half guidance of $50-55M. Tremendous spending in this area of the business was a big issue late last year. The stock has yet to recover from that news of heavy spending . Now, in the earnings conference call , management proclaimed "We are very much aware of the increased market focused on profitability, our strategy and business execution are very much aligned with that." Management's consistent reference to "discipline" and reduced costs was telling.

The second surprise was a pullback in logistics expense which management described as "slowing down the phasing of logistics capacity expansion." This decision slashed full year capital expenditure ((CAPEX)) guidance from $15M to $25M down to $10M to $15M. During Q&A, management acknowledged that currency effects drove that guidance down given spending is in local currencies weakening against the U.S. dollar. While management called this a temporary reduction in line with operational flexibility, they reassured analysts that they will remain asset light.

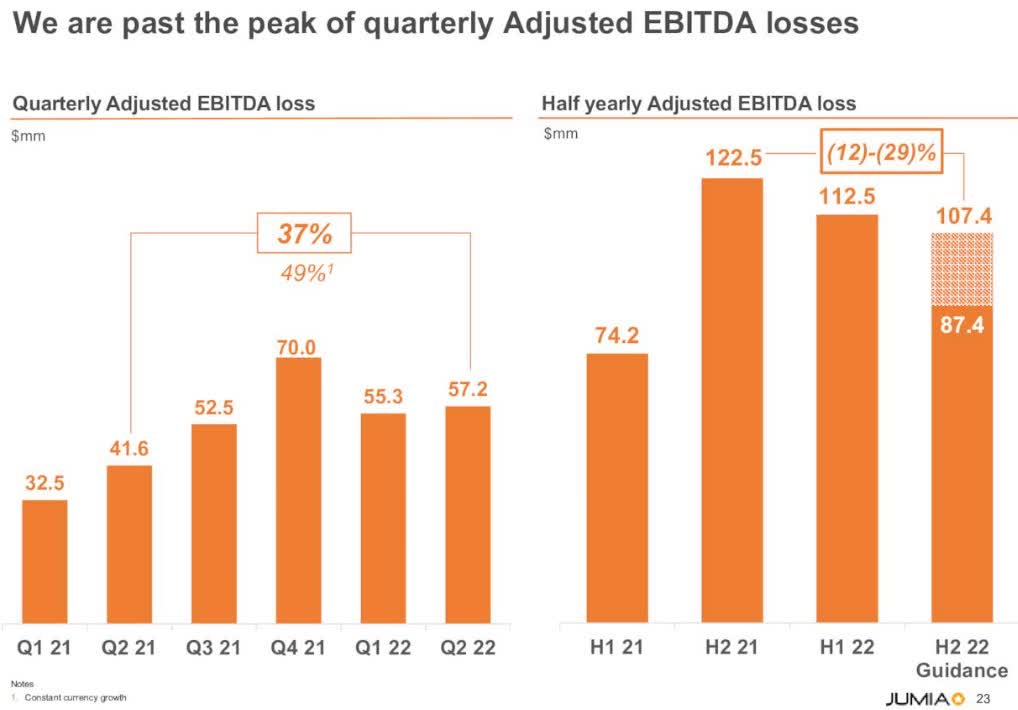

With lower costs and stable revenue guidance, Jumia now looks good to keep its promise of peak EBITDA losses. From the company's earnings presentation :

Turned the corner on EBITDA losses? (Jumia Technologies Q2 2022 earnings presentation)

{kind=link}

Note that the company decided to report conservative EBITDA guidance for the year at -$200M to -$220M with year-over-year reductions starting in 2023.

Gross profit margin also looks like it has turned the corner with the fastest growth in 5 quarters. Jumia expects the second half of the year to generate 27-44% year-over-year growth in gross profit. Again, from the earnings presentation:

Turned the corner on gross profit growth? (Jumia Technologies Q2 2022 earnings presentation)

{kind=link}

Jumia also revealed that it has a hiring freeze in place that includes no backfills for departing leaders. This policy will hold G&A (general and administrative) expenses "relatively stable."

Order and Revenue Growth

Jumia turned the corner in marketplace revenue growth with the fastest rate in 7 quarters at 17% year-over-year. Marketing & advertising and value-added services were the primary drivers while fulfillment contracted slightly thanks to an increase in free next-day delivery. Jumia increased the share of packages delivered within 24 hours of ordering to 60% (no comparison provided). Management indicated that this shipping strategy supports "consumer adoption and repurchase." The diversifying "monetization engine" also makes the company less reliant on these fees.

The improved consumer adoption and repurchase shows up in strong growth in orders per active customer now over 3 orders for the quarter and growing 8% year-over-year. These active consumers increased an impressive 25% year-over-year. Order rate growth and active user growth combined to drive orders up 35% year-over-year to 10.3M in Q2.

The largest contributor to revenue growth remained first-party revenue with a whopping 95% year-over-year growth to $13.0M. Jumia attributed this growth to FMCG (Fast-moving Consumer Goods), particularly grocery. The company continues to shift its selling strategy toward "everyday product categories" and away from phones and electronics.

One point I am keeping an eye on is slower sequential growth. Since Q2 2022 sequential growth was slower than Q2 2021 sequential growth, I am looking to the all-important Q4 as an indicative tell and confirmation that Jumia has truly turned the corner on translating operational effectiveness into healthier financial performance..

Overall, the revenue base for Jumia looks solid and supports the claim on reiterated revenue guidance.

JumiaPay

The penetration and usage of JumiaPay continues to crawl along. However, management insisted that it will continue to apply a "disciplined and gradual" approach. They expect JumiaPay to become a monetization driver in 2023 through access to 3rd party merchants on other platforms. A ramp in this service would mark an important element in Jumia turning the corner. On-platform, JumiaPay's total payment volume grew 31% year-over-year but remains just 27.4% of gross merchandise value (GMV), up from 25.3% a year ago.

JMIA Stock - Turning the Corner

Seeking Alpha quant ratings have also turned the corner along with Jumia. The quant rating for JMIA has gone from a long string of strong sells to hold starting August 11, 2022. If I had not already accumulated my desired stake in the company, I would buy shares here and on future dips.

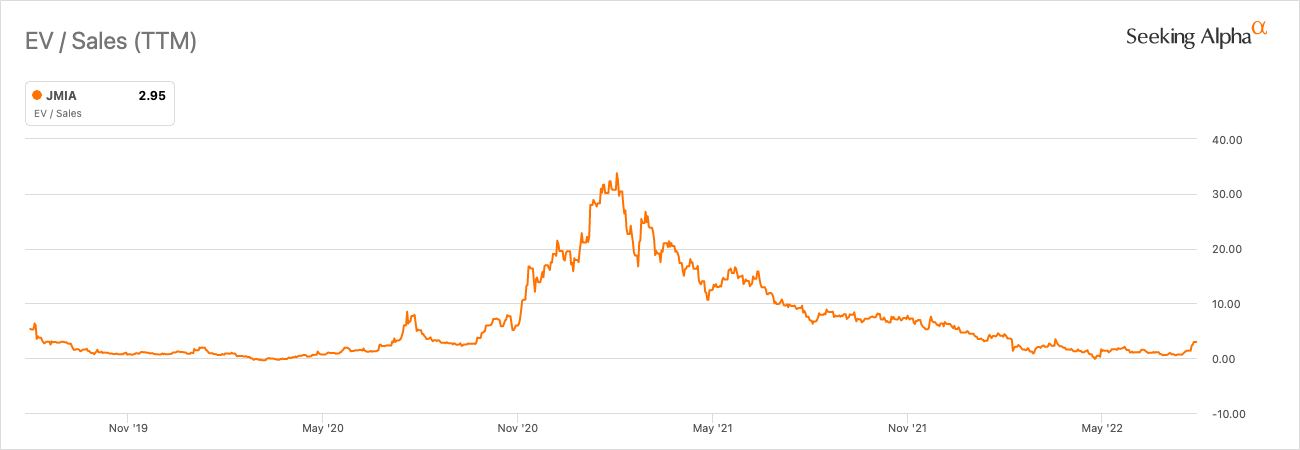

From a valuation perspective, Jumia seems to have sufficiently retested rock bottom enterprise value to sales (EV/sales) levels.

Turned the corner on EV/sales from rock bottom valuations? (Seeking Alpha)

{kind=link}

Overall, Jumia's performance and guidance looks even more encouraging given the backdrop of growing recession fears in the global economy. Still, these macro risks will remain an important wildcard going forward.

Be careful out there!

For further details see:

Has Jumia Technologies Turned The Corner?