HE - Hawaiian Electric: No Turnaround In Sight

2023-11-26 02:22:42 ET

Summary

- Hawaiian Electric Industries faces challenges such as regulatory hurdles and market dynamics, but also dominates the market and is committed to clean energy solutions.

- The company's financials have been impacted by the Maui windstorm and wildfires, leading to a suspension of dividends and reduced revenues.

- Despite some positive indicators such as improving liquidity metrics and commitment to sustainability, concerns over litigation, regulatory scrutiny, and financial stability support a cautious approach.

Investment Thesis

In this article, I articulate my investment thesis on Hawaiian Electric Industries ( HE ), a pivotal entity in Hawaii's energy and economic landscape. My analysis is rooted in a holistic view of the company, factoring in its strategic initiatives, financial health, and the broader industry context. I approach this evaluation with a critical eye, aiming to dissect the complexities of HE's operations and financials to offer a well-rounded perspective. This piece is designed to guide investors through the intricacies of HE's current position and future potential, providing a comprehensive outlook on its investment viability.

My investment thesis hinges on a cautious yet forward-looking stance. I delve into the challenges HE faces, such as regulatory hurdles and market dynamics, while also acknowledging its market domination and commitment to clean energy solutions. This dual focus is crucial in understanding HE's position in the evolving energy sector. Readers should anticipate an in-depth analysis that goes beyond surface-level financial metrics, exploring the strategic underpinnings of HE's decisions and their long-term implications. This article is not just a snapshot of HE's current financial state but an exploration of its trajectory, offering insights into how the company may navigate its future.

Introduction

Hawaiian Electric Industries serves as the parent company to a family of businesses that are integral to Hawaii’s economic and community activity. At its core, Hawaiian Electric provides energy, serving 95% of the state and pushing forward towards a future of 100% clean, carbon-neutral energy. The company’s commitment extends to fostering strong community partnerships and sustainable economics for shareholders and stakeholders alike??. American Savings Bank, another HE subsidiary, propels Hawaii’s growth by financing the needs of its families, businesses, and communities, further supporting Hawaiian Electric’s clean, energy-efficient initiatives??. Additionally, Pacific Current, as HE’s investment arm, focuses on projects that enhance Hawaii’s sustainability goals, underpinning the state’s environmental and economic ambitions?.

Current Financials

As I analyze Hawaiian Electric Industries' current financials, the situation is complex and warrants careful consideration for my strong sell thesis. In the first quarter of 2023, the HE Board of Directors approved a modest increase in the quarterly dividend from $0.35 to $0.36 per share. However, the ongoing challenges posed by the Maui windstorm and wildfires led to the suspension of these dividends after the second quarter to ensure adequate liquidity and support rebuilding efforts??. This dividend suspension, while prudent, does signal potential financial strain and might concern long-term investors seeking steady income.

The financial impact of the Maui incidents is significant. Based on the third quarter earnings of 2023, operation and maintenance expenses rose by approximately $21 million, a substantial 18% increase compared to the same period in 2022. This increase was largely due to costs associated with the Maui windstorm and wildfires??. Additionally, kilowatt-hour sales volume decreased by 2.5% in the same period, with Maui experiencing an 8.1% decrease. Elevated fuel prices have persisted, impacting electricity consumption and leading to a reduction in sales volume??.

On the positive side, customer accounts receivable decreased by $47 million, or 16%, with a 17% reduction in the number of accounts past due since December 31, 2022. This decrease in receivables has benefited the utility's liquidity, a crucial factor in maintaining operational stability??.

However, the overall revenue picture is not as encouraging. For the three months ending September 30, 2023, electric utility revenues decreased significantly from $956 million in 2022 to $795 million in 2023; overall revenue decreased 13.46% YoY??. This decrease is attributed to a combination of lower fuel oil prices, lower purchased power energy prices, and lower PPAC revenues, despite higher MPIR revenue, higher investment interest income, and higher fuel-cost risk sharing adjustments.

Further complicating the financial landscape is the Public Utilities Commission (PUC) order issued on August 31, 2023, temporarily suspending the ESM (Earnings Sharing Mechanism) based on the Q3 earnings report. This suspension aims to prevent customers from bearing the costs associated with the Maui windstorm and wildfires without prior PUC review??.

Moreover, a significant gap exists between PUC-allowed ROACEs and the actual ROACEs achieved by the company. This gap primarily results from the exclusion of certain expenses from rates, such as incentive compensation and charitable contributions, along with depreciation O&M expense and return on rate base exceeding what is currently recovered through rates??.

In summary, while Hawaiian Electric has demonstrated some resilience, the financial challenges posed by the Maui windstorm and wildfires, coupled with the dividend suspension, reduced revenues, and regulatory complexities, support my thesis for a cautious approach. The utility's ability to navigate these financial headwinds and maintain operational stability will be critical in determining its long-term viability and attractiveness to investors.

Forward Guidance

Looking ahead, the outlook for the company embodies both challenge and resilience. Amidst the backdrop of Maui's wildfire tragedy, there's a palpable sense of commitment in the words of Hawaiian Electric’s President and CEO, Scott Seu, who underscored the company's enduring dedication to community service and the urgency to reinforce infrastructure against climate risks. The formation of the One 'Ohana Initiative, with HE's substantial contribution, not funded by customers, signals a collaborative stride towards recovery and safety enhancements.

While the financial impact of the wildfires is reflected in the deferment of expenses and the suspension of dividends, Seu’s assertion states:

“Our decision to suspend the quarterly cash dividend impacts many of you... [but] we believe it was the right decision to support our ability to be a strong partner to our communities” - Q3 Earnings Transcript

It speaks to a prioritization of long-term stability over short-term gains—a move that, while difficult, may be prudent for the company's health and community trust. The utility's solid core operations and strong bank capital position, as detailed by CFO Scott Deghetto, are promising indicators. However, the non-provision of full-year EPS guidance due to uncertainties from the wildfires introduces a cautionary note to my investment thesis. It's this balance of strength and uncertainty that shapes my guarded approach going forward.

The company’s focus on updating its capital expenditure plan to bolster the grid against extreme weather demonstrates proactive management. Yet, the pending lawsuits and the complex litigation landscape HE navigates warrant a watchful stance. The commitment to defending against claims of causation and negligence underscores the challenges ahead, as this reinforces my strong sell rating while acknowledging the company's strong fundamentals and societal role.

In conclusion, HE's forward path is one of concerted effort toward resilience and community partnership, yet it is not without financial and operational headwinds that must be carefully navigated by investors.

My Concerns

The recent investigation initiated by Bragar Eagel & Squire, P.C. against Hawaiian Electric Industries raises significant concerns for long-term investors and supports a strong sell thesis for the stock. The class action complaint , filed on August 24, 2023, covering a Class Period from February 28, 2019, to August 16, 2023, alleges serious breaches of fiduciary duties by the board of directors. This investigation is a critical development, considering the law firm's national recognition in representing shareholder rights.

Key to the allegations is the claim that Hawaiian Electric made materially false and misleading statements about its business operations and prospects. The focus is on the company's wildfire prevention and safety protocols, which were reportedly inadequate despite the known wildfire risks, particularly in Maui. This inadequacy purportedly exposed the region to heightened risks of devastating wildfires, contradicting the company's public assurances. The legal case against Hawaiian Electric hinges on Hawaii's lack of an inverse condemnation law, unlike California. Plaintiffs are invoking the Hawaii Constitution's clause on compensation for property taken or damaged for public use. The case's outcome may depend on whether Hawaiian Electric took all reasonable measures to prevent the incident.

The gravity of these allegations cannot be overstated. If proven, they suggest a significant governance failure and misrepresentation of operational integrity at Hawaiian Electric. For investors, this represents not just a potential financial risk but also a reputational one. The misleading statements and the company's failure to disclose essential information about its wildfire safety measures could have far-reaching implications on investor confidence and the stock's performance.

Moreover, the involvement of Bragar Eagel & Squire, P.C., a firm with a track record in complex litigation, indicates that these allegations are taken seriously and could lead to substantial legal repercussions for Hawaiian Electric. This adds another layer of uncertainty and risk for the stock, making a strong case for considering the sale of HE shares. Investors must weigh these developments carefully, as they reflect on both the immediate and long-term prospects of Hawaiian Electric in an increasingly risk-aware market environment.

Following, the lawsuit by Honua Ola Bioenergy against Hawaiian Electric Industries for over $1 billion in damages accentuates the gravity of risks associated with the stock. This legal action alleges monopolistic practices by Hawaiian Electric, specifically hindering Honua Ola's biomass power plant operations. Such accusations, if substantiated, could lead to significant financial liabilities and reputational harm for HE, underlining a compelling rationale for a strong sell recommendation in investment portfolios.

The downgrade of Hawaiian Electric Industries by Fitch to junk status, mirroring actions by Moody's and S&P Global, is a critical red flag for investors. This downgrade, driven by potential wildfire-related liabilities that could surpass $3.8 billion, signifies an existential financial threat to HE. Such a substantial downgrade, coupled with a 4.5% decline in share value and the ominous "Rating Watch Negative," underlines a deteriorating confidence in the company's financial stability, reinforcing the strong sell thesis for Hawaiian Electric's stock.

Bullish Indicators

As I delve into the financial aspects of Hawaiian Electric, I have also identified a few catalysts that could promote a rebound, despite the current challenges. Firstly, Hawaiian Electric's monopoly in serving 95% of Hawaii's energy needs is a significant advantage. This suggests a strong foundation for long-term growth, especially as Hawaii continues to expand and modernize its infrastructure.

Secondly, the company's commitment to a 100% clean, carbon-neutral energy future is not just a noble endeavor but also aligns with global trends towards renewable energy. This strategy establishes HE as a future-ready, sustainable energy leader, proactively addressing potential energy shortages.

Following, the decrease in customer accounts receivable and the reduction in the number of accounts past due since December 31, 2022, are also encouraging. These improvements in liquidity metrics indicate effective management of working capital and financial health, which are vital for enduring operational stability. The company also formed the One 'Ohana Initiative and HE's contribution to it, albeit not funded by customers, shows a strong commitment to community and sustainability. Such initiatives will add to the corporate reputation and stakeholder trust, which is critical in today's socially conscious investment climate.

In conclusion, while the current financial picture of Hawaiian Electric Industries has its complexities, the company's strategic focus on sustainable energy, strong market position, improving liquidity metrics, and commitment to community and environmental sustainability are key factors to make note of. These details not only point towards potential upside but also align with broader economic and environmental trends.

However, it's important to acknowledge the concerns of those who might be skeptical. The challenges stemming from the Maui windstorm and wildfires, the suspension of dividends, and regulatory complexities cannot be overlooked. These factors do introduce a level of risk and uncertainty that may deter some investors. The ongoing litigation and regulatory scrutiny are also major concerns that could impact the company's financials and reputation in the short term. As an investor, it's crucial to weigh these risks against the potential long-term benefits and make an informed decision based on one's investment strategy and risk tolerance.

Valuation

In examining the valuation metrics provided by Seeking Alpha, I find a compelling narrative to support my strong sell thesis. Firstly, in my opinion, the 14.56% short interest reflects a notable skepticism among investors about the company's future prospects. I view this high level of short interest as a red flag, indicating that a significant portion of the market anticipates a decline in the stock's value, which could lead to heightened volatility and uncertainty in its performance. The Forward Price to Earnings ((FWD P/E)) ratio, at 6.30 , sits substantially below the sector median of 16.60, indicating a -62.03% deviation. Such a depressed FWD P/E, even with an A+ grade, might suggest the market is skeptical of future earnings growth or profitability sustainability.

Moving to the Forward Price to Sales (FWD P/S) ratio, the figure of 0.38 compared to the sector median of 1.89, and the discrepancy of -79.62%, reinforces the undervaluation theme. Although the A+ grade could be construed as a sign of value, in my perspective, it reflects investor apprehension about the company's sales growth or margin expansion prospects.

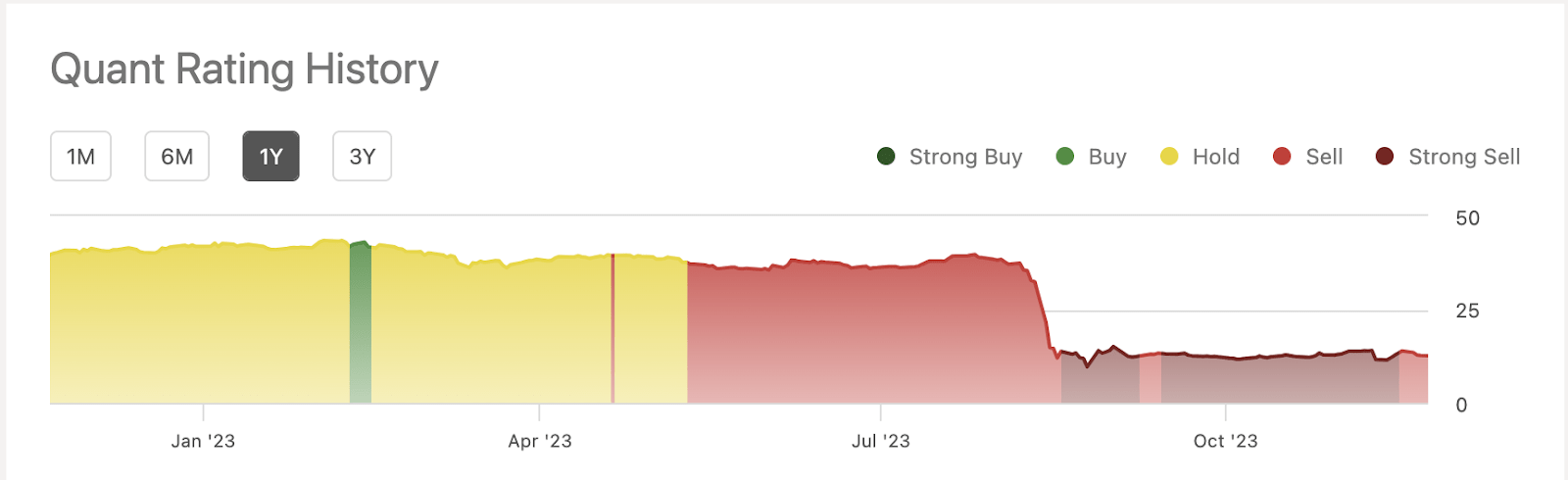

The Trailing Twelve Months Price to Book (TTM P/B) ratio further cements my stance. The stock's P/B ratio of 0.63 is significantly lower than the sector's 1.63 median, a -61.32% variance. An A+ grade here typically would imply robustness in asset valuation; however, in this context, it could denote underappreciation of the company's asset base or an overhang of potential write-downs. Another note that aligns with my thesis is the quant rating. The chart below clearly illustrates that the stock has maintained a consistent sell rating over an extended period.

Current Quant Rating (Seeking Alpha) Quant Rating History (Seeking Alpha)

{kind=link}

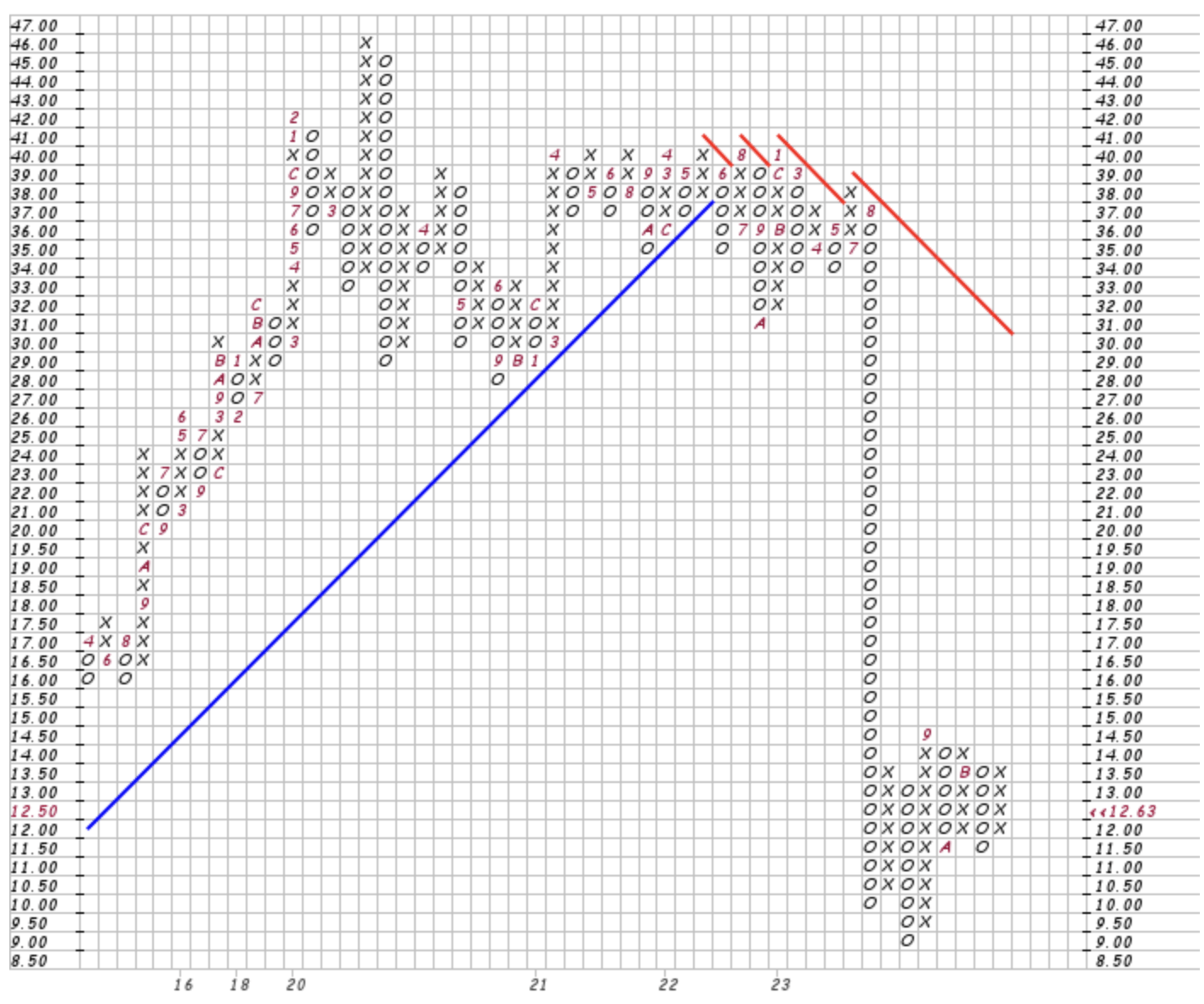

I would also like to highlight a key metric in the point and figure chart below:

HE Point & Figure Chart (Stock Charts)

{kind=link}

Based on this traditional 3 box reversal graph, if you bring your attention to the bottom right corner, I am led to believe that the price will continue to test the 11.50 bench-line. This is where the support has been held on two occasions. However, the trend prior to August (9) was where the stock broke through its support at 10.00 and made a mark at 9.00. If the stock makes a reversal it could cross the support line and potentially fall further due to the support line being lost (possibly traveling to the 9.00-10.00 range, but I would predict a 10.50-11.00 price), which promotes my strong sell thesis and why I would raise caution to current investors.

While Seeking Alpha's grades suggest a favorable valuation, the stark contrast with sector medians across these metrics highlights a market consensus that is wary of this stock's future performance. The heavy short interest on HE undermines the vision from many investors betting that this company will drift lower. This discrepancy is a cornerstone of my rationale for advocating a strong sell position. Additionally, the quant rating supports my overall thesis and as I described the point and figure chart’s support line, it will likely plunge to 10.50-11.00 if the support is broken. In essence, the market, it seems, is pricing in challenges that may not be fully reflected on the balance sheet just yet, making this an opportune moment to exit.

Conclusion

In concluding this comprehensive analysis of Hawaiian Electric Industries, my stance is firmly towards a strong sell recommendation. This decision stems from a critical assessment of the company's multifaceted challenges, ranging from operational and financial difficulties to broader market and regulatory complexities. While recognizing HE's significant role in Hawaii's energy sector and its reduction in customer accounts receivable and past due accounts, the overshadowing concerns include litigation risks, regulatory uncertainties, and financial pressures, which significantly tilts the balance. My opinion encapsulates the intricate dynamics at play in HE's current scenario and its potential future trajectory. For those in the energy sector, this article serves as a guide, offering a nuanced understanding of HE's position within a rapidly evolving landscape. I believe investors should have a cautious approach for the next six months, where I will later weigh the current risks against the long-term prospects.

For further details see:

Hawaiian Electric: No Turnaround In Sight