HE - Hawaiian Electric: Solid Q2 Results But Avoid Due To Wildfire Liability Risk

2023-08-17 11:53:14 ET

Summary

- Devastating wildfires in Maui have caused Hawaiian Electric shares to plummet by 58.84%.

- The company's second quarter results showed stable revenues and operating income.

- The potential liability from the wildfires is the biggest risk to the company, with fears of bankruptcy and a junk bond rating.

- The dividend can be covered by cash flow, but Hawaiian Electric Industries may have to cut to cover legal expenses or judgments.

- HE stock is probably best avoided until we have more insight into the wildfire liability.

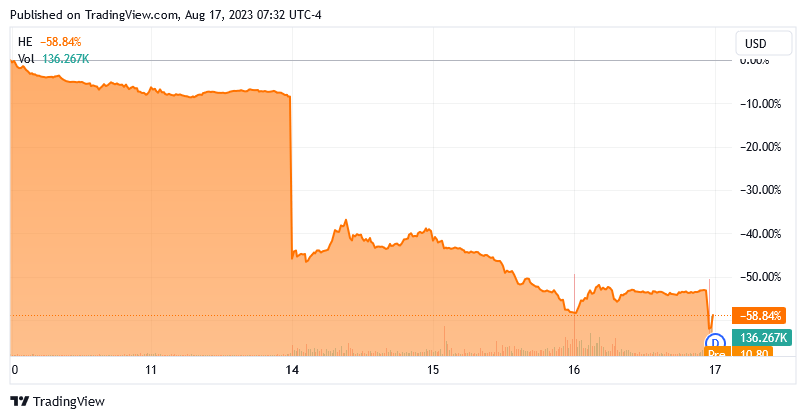

One of the biggest news stories over the past few weeks was the devastating wildfires that swept over the island of Maui, the second-largest island in Hawaii. These wildfires have been the deadliest in the state’s history, with officials currently claiming that 111 people have lost their lives. The wildfires have also destroyed the town of Lahaina, with thousands of residential and commercial buildings consumed by the blaze. As might be expected, Hawaiian Electric Industries, Inc. ( HE ) shares have taken a beating in response to this disaster, with the common stock losing 58.84% of its value over the past five days:

{kind=link}

This is certainly not in response to the company’s second-quarter results that came out last week. After all, the company’s revenues and operating income were almost totally flat year-over-year. We certainly do not expect that to cut its value by more than half. In fact, most of the share price decline appears to be that lawyers are investigating rumors that a downed power line may have been the spark that caused the fire.

I will admit that I am having flashbacks to PG&E ( PCG ), which was driven into bankruptcy following a series of lawsuits that accompanied a wildfire in California back in 2019. The market appears to be concerned that Hawaiian Electric will share the same fate. That is certainly a possibility, but it is important to keep in mind here that the state is far more dependent on Hawaiian Electric than California is on PG&E. There is almost no way that the company will not continue on as an operating entity, although it could definitely encounter some difficulties depending on the severity of the lawsuit awards.

Hawaiian Electric Q2 Earnings Results Analysis

While the wildfires and the potential issues surrounding them are undoubtedly the biggest things weighing on the company’s stock price right now, we should still take a look at the company’s second-quarter earnings report that came out last week so that we know just how much or little of the stock price decline was related to that. As regular readers are no doubt well aware, it is my regular practice to share the highlights from a company’s earnings report before delving into an analysis of its results. This is because these highlights provide a background for the remainder of the article as well as serve as a framework for the resultant analysis. Therefore, here are the highlights from Hawaiian Electric’s second-quarter 2023 earnings results:

- Hawaiian Electric Industries reported total revenues of $895.685 million during the second quarter of 2023. This represents a 0.009% increase over the $895.607 million that the company reported in the prior-year quarter.

- The company reported an operating income of $92.979 million in the reporting period. This represents a 7.28% increase over the $86.668 million that the company reported in the year-ago quarter.

- Hawaiian Electric Industries reported that 60% of its customers have now received “advanced smart meters” that are needed for the proper integration of renewables into its electric infrastructure. This constitutes approximately 285,000 meters now in service.

- The company reported an operating cash flow of $190.7 million during the most recent quarter. That compares very favorably to the negative $17.9 million that the company reported during the corresponding quarter of last year.

- Hawaiian Electric Industries reported a net income of $54.6 million during the second quarter of 2023. This represents a 4.00% increase over the $52.5 million that the company reported during the second quarter of 2022.

One of the defining characteristics shared by most electric utilities is that their finances tend to be remarkably stable over time, regardless of conditions in the broader economy. We can certainly see that here as both revenue and net income were almost flat year-over-year while operating income showed only a modest increase. I will admit that I suspected that Hawaiian tourist traffic was down year-over-year due to the fact that many American consumers are facing financial difficulties in today’s inflationary environment, but the Hawaii Department of Business, Economic Development, and Tourism states that tourist traffic to the islands was up 5.2% year-over-year in June (the most recent date for which data is currently available).

However, that increase was almost entirely international travel, as tourist traffic from the rest of the United States was down compared to the prior-year period. The full data can be downloaded here if you are interested in perusing the numbers yourself. This could have had an effect on Hawaiian Electric Industries due to the fact that hotels, restaurants, and other businesses will consume more electricity when tourist traffic is high than when it is low. For its part, the company reported that its sales of electricity were slightly down year-over-year:

| Q2 2023 |

| Q2 2022 |

| Hawaiian Electric |

| 1,480 |

| 1,506 |

| Hawaii Electric Light |

| 252 |

| 261 |

| Maui Electric |

| 262 |

| 264 |

| Total |

| 1,994 |

| 2,031 |

(All figures in kilowatt-hours.)

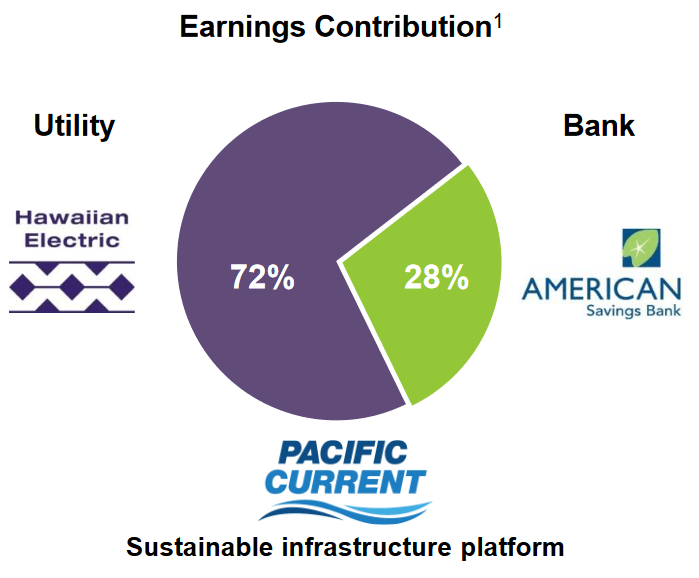

As has been noted in my previous articles on this company, Hawaiian Electric is both an electric utility and one of the largest banks in Hawaii. The electric utility is a far greater contributor to the company’s finances, though, as it accounts for roughly 72% of the company’s earnings:

{kind=link}

In the second quarter, the electric utility’s revenues were $794.191 million compared to $818.873 million a year ago. So, they were down slightly, but this makes sense considering that the consumption of electricity was also down slightly compared to the year-ago quarter. We do still see that the company’s financial performance in aggregate was quite stable.

The reason for this overall stability should be quite obvious. After all, utilities such as Hawaiian Electric provide a product that is generally considered a necessity for our modern way of life. After all, how many of us do not have electric service to our homes and businesses? Right now, only about 60,000 Americans do not have access to electricity, which is a very small percentage of the nation’s 334 million population. As such, most people will prioritize paying their electric bill ahead of making discretionary expenses during times when money gets tight, which certainly describes the situation that many people are in right now as real wages have not been keeping up with inflation. As households generally consume similar amounts of electricity over time and prioritize paying their electric bills ahead of most other expenses, the revenues of electric utilities tend to be very stable from quarter to quarter and year to year. This allows them to easily budget their expenses and ensures relatively stable finances over time. That is exactly the kind of thing that should appeal to most conservative income investors, or to anyone seeking a safe haven investment during challenging economic periods.

Growth Prospects

Naturally, as investors, we are unlikely to be satisfied with mere stability. We like to see any company in which we are invested grow and prosper with the passage of time. Fortunately, Hawaiian Electric Industries is positioned to do exactly this. The primary way through which it will achieve this growth is by increasing the size of its rate base. The rate base is the value of the company’s assets upon which regulators allow it to earn a specified rate of return. As this rate of return is a percentage, any increase to the rate base allows the company to positively adjust the prices that it charges its customers in order to earn that specified rate of return.

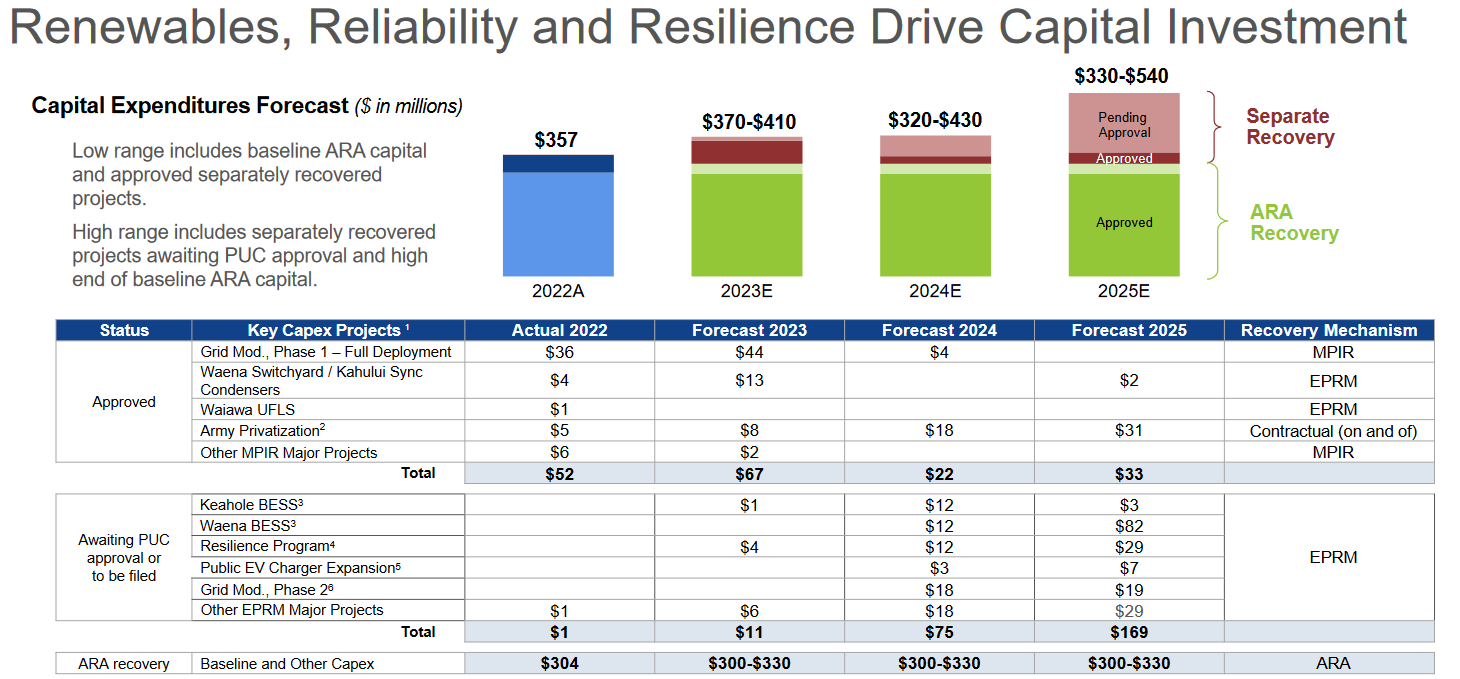

The usual way through which a company grows its rate base is by investing money into upgrading, modernizing, or possibly expanding its utility-grade infrastructure. Hawaiian Electric Industries is planning to do exactly this as it has outlined a $900 million to $990 million capital spending program for the 2023 to 2025 period:

{kind=link}

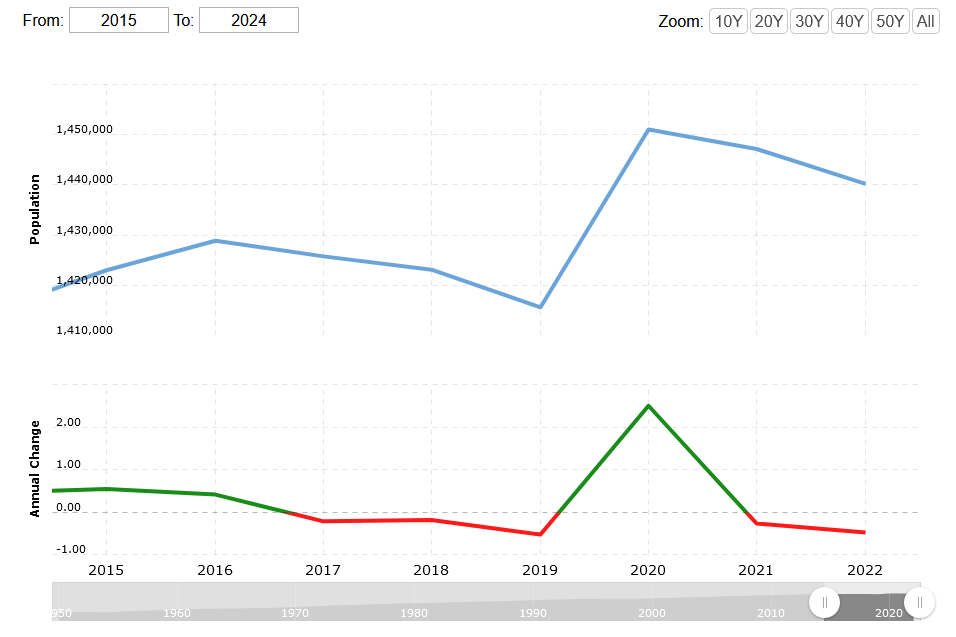

This is a much less expansive program than many other utilities have presented. That makes a certain amount of sense for Hawaii though, as space is rather limited, and the population has been relatively static for a while:

{kind=link}

As such, it does not really need to expand its infrastructure as the customer base is not growing nearly as much as in other places. Thus, the majority of this spending is intended for the modernization of its infrastructure as it prepares to shift to a greater dependence on renewables for electric generation capacity. In Hawaii, renewables might actually make sense because the state is closer to the equator than the rest of the nation (so the amount of sunlight does not vary much from season to season), and the sun’s rays are much more direct and intense than elsewhere in the United States.

The company has stated that it expects that this capital spending program will drive the utility company’s earnings upwards by about 5% annually. This is lower than some other utilities’ growth rates, but once again that is not surprising given the nature of the Hawaiian market.

Wildfire Liability Risk

As mentioned in the introduction, the potential liability to the company from the wildfires on Maui is without a doubt the biggest near-term risk to the company. The fears of this have already cut the stock price by more than half, and have resulted in a ratings downgrade by S&P. As of the time of writing, Hawaiian Electric Industries is one of the only utilities in the United States that now has a junk bond rating.

It is hard to properly evaluate and analyze the risks posed by liability settlements. Accuweather currently predicts that the economic costs to Maui because of the wildfires could be around $16 billion right now. As of June 30, 2023, Hawaiian Electric Industries had total assets of $16.5193 billion and shareholders’ equity of $2.2837 billion. If the company is found fully liable by the court and is ordered to pay anything close to that $16 billion figure, it would bankrupt the company instantly.

With that said, there are a few things to consider here:

- Hawaiian Electric Industries has a monopoly on the Hawaiian electric supply. The company serves more than 95% of the state’s population. Any court judgment would wind up resulting in much higher electric bills for the state’s population.

- The American Savings Bank is the second-largest bank in Hawaii, boasting $8.2 billion in deposits.

Realistically, the state is too dependent on Hawaiian Electric Industries to allow the company to fail, regardless of what happens in any court case to assign liability for the fires. The fact that the company has entered into discussions with restructuring professionals could give us some insight into what the final outcome of this situation would be if the company does end up with liability for the fires.

One very strong possibility is that the American Savings Bank will be spun off from the company and either acquired by another bank or operate as its own company. The bank has approximately $8.2 billion in deposits backing $9.2 billion in assets. The bank’s assets are quite solid, with 83% of its $6.1 billion of outstanding loans being in real estate with an average loan-to-value under 55%.

In the second quarter, the bank earned $0.18 per share ($20.204 million total). If we annualize that and assign it a price-to-earnings ratio that is comparable to other banks (about 9.4), that should allow it to be spun off with a market cap of $760 million. Obviously, that won’t help a lot if the company has to settle a multi-billion-dollar judgment, but it still seems a likely way for the company to go.

Honestly, considering the risks here, I would advise conservative investors to stay away until we have more insight into how this situation will be resolved. I highly doubt that the company will fail and end up worthless, but at the moment we do not even know what the ultimate judgment will be, and it is too difficult to value until we have more information.

Financial Considerations

It is always important to investigate the way that a company is financing its operations before making an investment in it. This is because debt is a riskier way to finance a company than equity due to the fact that debt must be repaid at maturity. That is usually accomplished by issuing new debt and using the proceeds to repay the existing debt. After all, very few companies have sufficient cash on hand to completely repay their debt as it matures. This process can cause a company’s interest expenses to increase following the rollover, depending on the conditions in the market. As of the time of writing, the effective federal funds rate is higher than it has been at any time since 2007 so it seems likely that any rollover today will cause the company’s interest expenses to increase.

In addition to interest-rate risk, a company must also make regular payments on its debt if it is to remain solvent. Thus, an event that causes a company’s cash flows to decline could push it into financial distress if it has too much debt. While utilities such as Hawaiian Electric Industries usually have remarkably stable cash flows, there have been bankruptcies in the sector before so this is not a risk that we should ignore.

One metric that we can use to evaluate a company’s financial structure is the net debt-to-equity ratio. This ratio tells us the degree to which a company is financing its operations with debt as opposed to wholly-owned funds. It also tells us how well a company’s equity will cover its debt obligations in the event of a liquidation or bankruptcy, which is arguably more important.

As of June 30, 2023, Hawaiian Electric Industries had a net debt of $3.2923 billion compared to shareholders’ equity of $2.2837 billion. This gives the company a net debt-to-equity ratio of 1.44 today. Here is how that compares to some of the company’s peers:

| Company |

| Net Debt-to-Equity Ratio |

| Hawaiian Electric Industries |

| 1.41 |

| DTE Energy ( DTE ) |

| 1.89 |

| Eversource Energy ( ES ) |

| 1.58 |

| Exelon Corporation ( EXC ) |

| 1.68 |

| Otter Tail Corporation ( OTTR ) |

| 0.54 |

| Entergy Corporation ( ETR ) |

| 1.92 |

As we can see here, Hawaiian Electric Industries generally compares pretty well to other electric utilities in this respect. It is not a perfect comparison because none of the company’s peers have a bank accounting for about a quarter of their earnings, but the comparison should be good enough. Overall, we can clearly see that Hawaiian Electric Industries does not appear to be overly reliant on debt to finance its operations. Investors should not need to worry too much about the company’s debt load.

Distribution Analysis

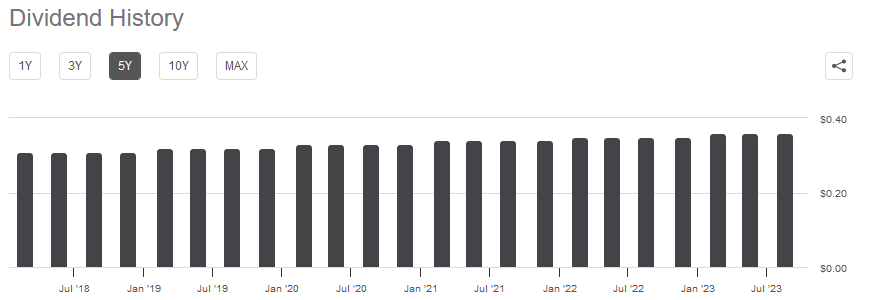

One of the biggest reasons why investors purchase utilities is that they tend to have a much higher dividend yield than just about anything else in the market. Hawaiian Electric Industries is certainly no exception to this, as the company boasts an incredibly attractive 9.88% yield at the current price. Admittedly, this yield is a direct result of the company’s share price plunging over the past week, which we have discussed at various times throughout this article. As is the case with most utilities, Hawaiian Electric Industries has a long history of raising its dividend on an annual basis:

{kind=link}

The fact that the company increases its dividend annually is something that we very much like to see in an inflationary environment, such as the one that we are in today. This is because inflation is constantly reducing the number of goods and services that we can purchase with the dividend that the company pays out. This can make it feel as though we are growing poorer and poorer with the passage of time, which is a particularly big problem for a retiree or anyone else that is depending on their portfolios to obtain the money that they need to pay their bills. The fact that the company increases its dividend every year helps to offset this effect and ensures that the dividend maintains its purchasing power over time.

As is always the case, it is critical to ensure that the company can actually afford the dividend that it pays out. After all, we do not want to be the victims of a dividend cut, since that would reduce our incomes and almost certainly cause the company’s stock price to decline.

The usual way that we judge a company’s ability to pay its dividend is by looking at its free cash flow. The free cash flow is the amount of cash that was generated by a company’s ordinary operations and is left over after it pays all of its bills and makes all necessary capital expenses. It is therefore the amount that is available for tasks that benefit the shareholders such as reducing debt, buying back stock, or paying a dividend. In the twelve-month period that ended on June 30, 2023, Hawaiian Electric Industries reported a negative levered free cash flow of $595.2 million. That was obviously not nearly enough to pay any dividends, yet the company still paid out $155.5 million to its shareholders over the period. At first glance, this is likely to be concerning as the company is clearly not generating enough free cash flow to sustain the dividend.

However, it is not uncommon for a utility to finance its capital expenditures through the issuance of debt and equity. The company will then pay its dividends out of operating cash flow. This is done because it is incredibly expensive to construct and maintain utility-grade infrastructure over a wide geographic area, and these costs would otherwise make it impossible for a utility to ever provide a return to its investors if it had to finance them solely out of cash flow.

During the trailing twelve-month period that ended on June 30, 2023, Hawaiian Electric Industries reported an operating cash flow of $751.5 million. This was more than sufficient to cover the $155.5 million in dividends that the company paid out and still leave it with a substantial amount of money available for other tasks. Overall, the dividend does appear sustainable based on the company’s cash generation capacity.

With that said, there is a very real risk here that the company will cut its dividend if it winds up with a liability judgment against it. This happened to BP ( BP ) following the Macondo oil spill in 2010 and, while the situation is not exactly the same, it does seem like a likely outcome. After all, the Court would probably want the company to be paying that $155.5 million to the plaintiffs in a lawsuit rather than shareholders trying to make a profit. As such, we should not really classify this dividend as reliable even though the company can easily afford it based on its cash generation capacity.

HE Stock Valuation

It is always critical that we do not overpay for any assets in our portfolios. This is because overpaying for any asset is a surefire way to earn a suboptimal return on that asset. In the case of an electric utility like Hawaiian Electric Industries, we can value it by looking at the price-to-earnings growth ratio. This is a modified version of the familiar price-to-earnings ratio that takes a company’s earnings per share growth into account. A price-to-earnings growth ratio of less than 1.0 is a sign that a stock may be undervalued based on its forward earnings per share growth and vice versa.

However, there are very few stocks that are undervalued in today’s very expensive market , and this is especially true in the low-growth utility sector. As such, the best way to use this ratio today is to compare Hawaiian Electric Industries to its peers and see which company offers the most attractive relative valuation.

According to Zacks Investment Research , Hawaiian Electric Industries will grow its earnings per share at a 3.32% rate over the next three to five years. This gives the company a price-to-earnings growth ratio of 2.31 at the current price. Here is how that compares to the company’s peers:

| Company |

| PEG Ratio |

| Hawaiian Electric Industries |

| 2.31 |

| DTE Energy |

| 2.83 |

| Eversource Energy |

| 2.60 |

| Exelon Corporation |

| 2.68 |

| Otter Tail Corporation |

| NA |

| Entergy Corporation |

| 2.53 |

As was probably expected following the precipitous stock price decline, Hawaiian Electric Industries appears to be offering a rather attractive valuation relative to its peers. I am not certain that it is worth the risk though, particularly for risk-averse investors and anyone that is concerned with the preservation of principal. Hawaiian Electric Industries looks like a classic vulture investment right now, and while it probably would be pretty profitable if the outcome of the wildfire liability is in its favor, most investors that are buying utilities do not want to take on that kind of gamble.

Conclusion

In conclusion, Hawaiian Electric Industries’ stock has suffered a major blow due to lawyers and others attempting to assign blame to the company for the wildfires that have ravaged the island of Maui. Other than that, the company’s latest results were quite strong, so it appears that the wildfire liability risk is the only thing weighing on the stock. That will probably be the case until the issue is ultimately resolved, and we have no way of knowing how long that will be nor what the ultimate outcome will be. As such, Hawaiian Electric Industries, Inc. stock is probably best avoided until we know the resolution.

For further details see:

Hawaiian Electric: Solid Q2 Results, But Avoid Due To Wildfire Liability Risk