HELE - Helen of Troy Is A Case Study In Leveraged Rollups Hitting The Skids

2023-05-02 15:22:01 ET

Summary

- We're short Helen of Troy in staff personal accounts.

- The company operates as a debt-funded rollup of consumer brands and has some nested problems at present.

- The CFO and CEO have each resigned in recent weeks.

- We believe the stock has around 20% downside from here in the short term, and perhaps 50-80% downside in the medium term.

- We expand on the topic below, and include risk management commentary.

DISCLAIMER: This note is intended for US recipients only and, in particular, is not directed at, nor intended to be relied upon by any UK recipients. Any information or analysis in this note is not an offer to sell or the solicitation of an offer to buy any securities. Nothing in this note is intended to be investment advice and nor should it be relied upon to make investment decisions. Cestrian Capital Research, Inc., its employees, agents or affiliates, including the author of this note, or related persons, may have a position in any stocks, security, or financial instrument referenced in this note. Any opinions, analyses, or probabilities expressed in this note are those of the author as of the note's date of publication and are subject to change without notice. Companies referenced in this note or their employees or affiliates may be customers of Cestrian Capital Research, Inc. Cestrian Capital Research, Inc. values both its independence and transparency and does not believe that this presents a material potential conflict of interest or impacts the content of its research or publications.

Summary

We're short Helen of Troy (HELE) in staff personal accounts. The company is a leveraged rollup where growth has ground to a halt, where a high proportion of cash flow is required for debt service, meaning that new acquisitions are likely to prove difficult, and where the CFO and now CEO have each resigned. And all this in a sector - low-end consumer goods - and products - no-moat everyday items - that isn't supportive of premium pricing of the kind that's generally required to make leveraged rollups successful. The stock has we believe around 20% short-term downside from here before hitting localized support, and potentially a lot more downside thereafter if the capital structure starts to bite. Our short-term price target is $80, and if that support level is blown through, the next achievable price level we believe is in the mid-$50s/share.

We now discuss in more detail.

What Good Looks Like In Leveraged Rollups

That everyone likes to lob rocks at leveraged anything doesn't mean that leveraged rollups are in and of themselves a bad idea. It's just that most management teams are not good at them and, further, such businesses are often unsuited to life as a public company. And if the wheels start to come off, leverage does what leverage does, which is to say it amplifies the original impulse and delivers an outcome with greater speed and intensity than would otherwise have been the case.

Here's leveraged rollup 101.

1. Start by having a bigger friend. Specifically you want a fat equity cushion on hand for when the inevitable happens, ie, you buy the wrong company or you pay the wrong price or you hit a road bump in operating performance or something else that causes the debt to be a near-term problem. This is what "financial sponsors," aka. private equity firms, are for. Someone to provide the equity. If you're running a leveraged rollup as a public company, this is more challenging, because raising equity unexpectedly in public markets is a wonderful way to tank your stock price, and in any event public shareholders are wont to freak out if your leverage levels approach even half of what doesn't break a sweat over at your local barbarians' buyout shop.

2. Choose an industry and a set of companies where you have pricing power vs. your customers. Rollups mean buying more and more companies in the same market segment, which means that as time goes by you own more market share and can price more aggressively as a result. If the alternatives are scant but your products are important? Then even in the absence of unit growth you can keep organic revenue moving up through price increases (which by the way are 100% incremental free cash flow margin, which means each price rise does wonders for your debt service capacity). If you're rolling up an industry or a set of companies that have no pricing power, expect your competitors to have an advantage, since their lack of leverage means more ability to invest in R&D and/or sales & marketing; if your products have no "moat" then you are vulnerable to such tactics from your competitors.

3. Employ a management team that has proven itself capable of managing a leveraged capital structure and an acquisition-driven business model. This is a very specific set of skills. Managers who are good at this tend to be rather boring looking from the outside. They thrive on detail, get great satisfaction bringing in a quarter where net leverage is better than budget by 0.05x TTM EBITDA, prefer to drive a three-year old Lexus even when they can afford a Lamborghini, and they don't get stressed, aren't flamboyant, and say "no" a lot.

4. Have an exit plan. At some point the opportunity set in an industry sector starts to get too hard or too expensive or too restricted, and you need to hand the problem over to someone else. This means selling the company in an unemotional way, from a position of strength (because if you followed Rule 3 above and had an unemotional management team, they will have been telling you for a year or more that the business is soon going to be pushing water uphill and it's time to sell).

What Helen of Troy Looks Like

Helen of Troy is a small cap (around $3bn enterprise value) standalone public company with no major financial powerhouse driving the rollup as a control or large minority shareholder. In short it has no bigger friend to provide an equity cushion.

It operates in an industry - consumer products - where there's pricing power at the high end - think LVMH and so on - but not at the low end where HELE plays. One set of low-cost kitchen tools is a lot like another. The company has no meaningful brand power and is therefore a price taker, not a price setter. That's a risky situation to which to apply leverage which, as we mention above, tends to amplify all situations good or bad.

The company at the present time has no management team to speak of, since the CFO and CEO resigned. The CEO will remain in post for some months but is hardly likely to be doing his best work. And his best work hasn't been so good of late either. The CEO-elect was previously the COO who has been at the company for a year, and prior to that held operational management roles at large-cap companies - in other words has no previous CEO experience and no experience running a leveraged facility or a rollup strategy. This is a major risk.

There's no exit plan, only a Bob Dylan Never-Ending Tour type restructuring plan, the evidence of which thus far amounts to a 40-plus page earnings release detailing how the business would have looked in 2020-21-22 under the restructured business units.

This is in short precisely the opposite of what good looks like in leveraged rollups.

Let's take a look at the numbers.

Summary Financials

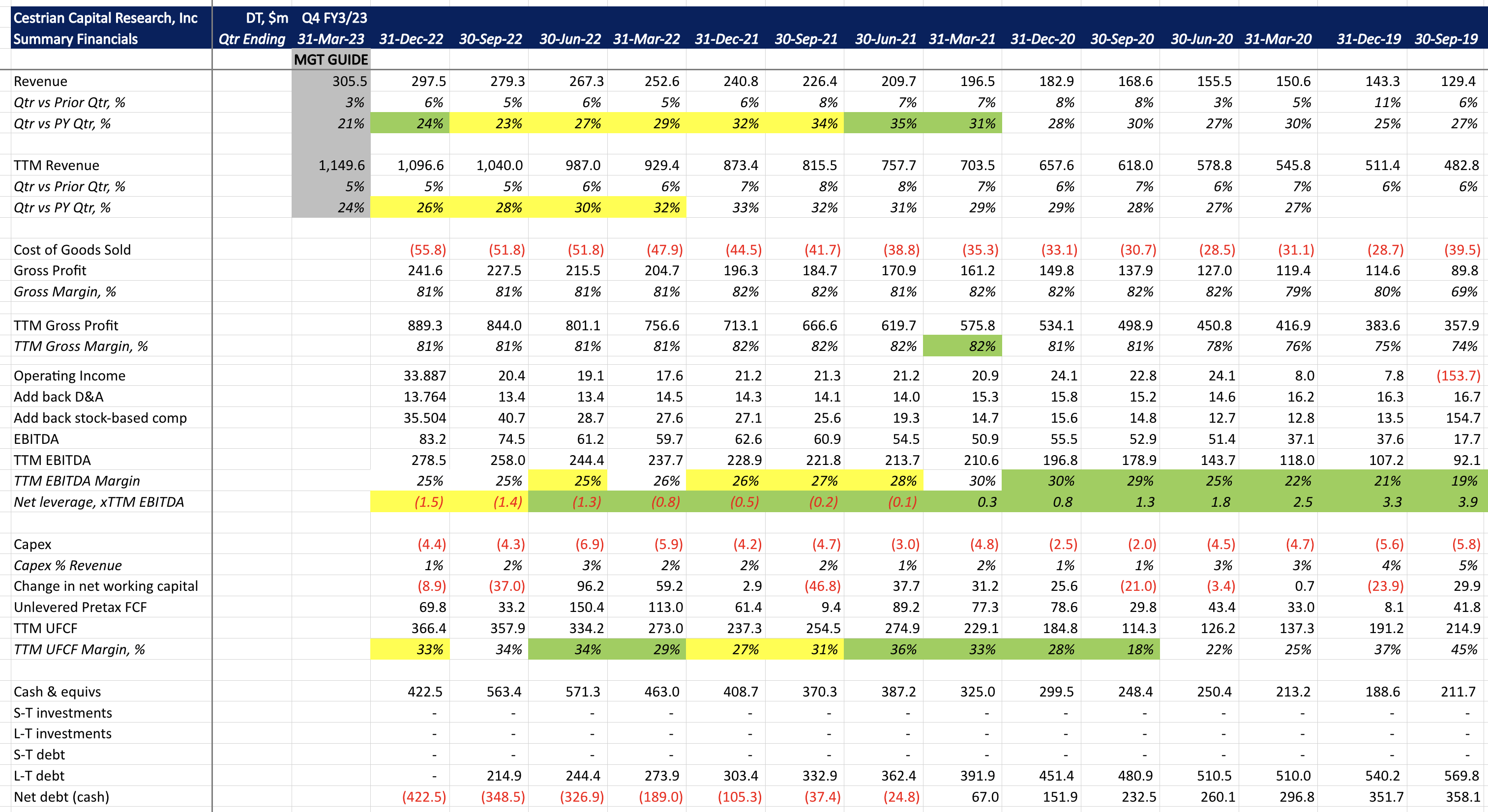

Indulge us a minor detail for a moment. There are some leveraged rollups with traded tickers that fit the mold to perfection. Here's Dynatrace ( DT ), an enterprise software company forged in the crucible of a buyout shop and let loose on public markets some years back.

DT Fundamentals (Company SEC filings, YCharts.com, Cestrian Analysis)

{kind=link}

Take a look at the combination of rock-solid revenue growth, cash flow exceeding EBITDA (meaning conservative earnings recognition policies, and very focused working capital management), and the rapid deleverage from IPO (when net leverage = 3.9x TTM EBITDA) to today (net leverage is negative ie. the balance sheet is now in a substantial net cash position).

That's what good looks like.

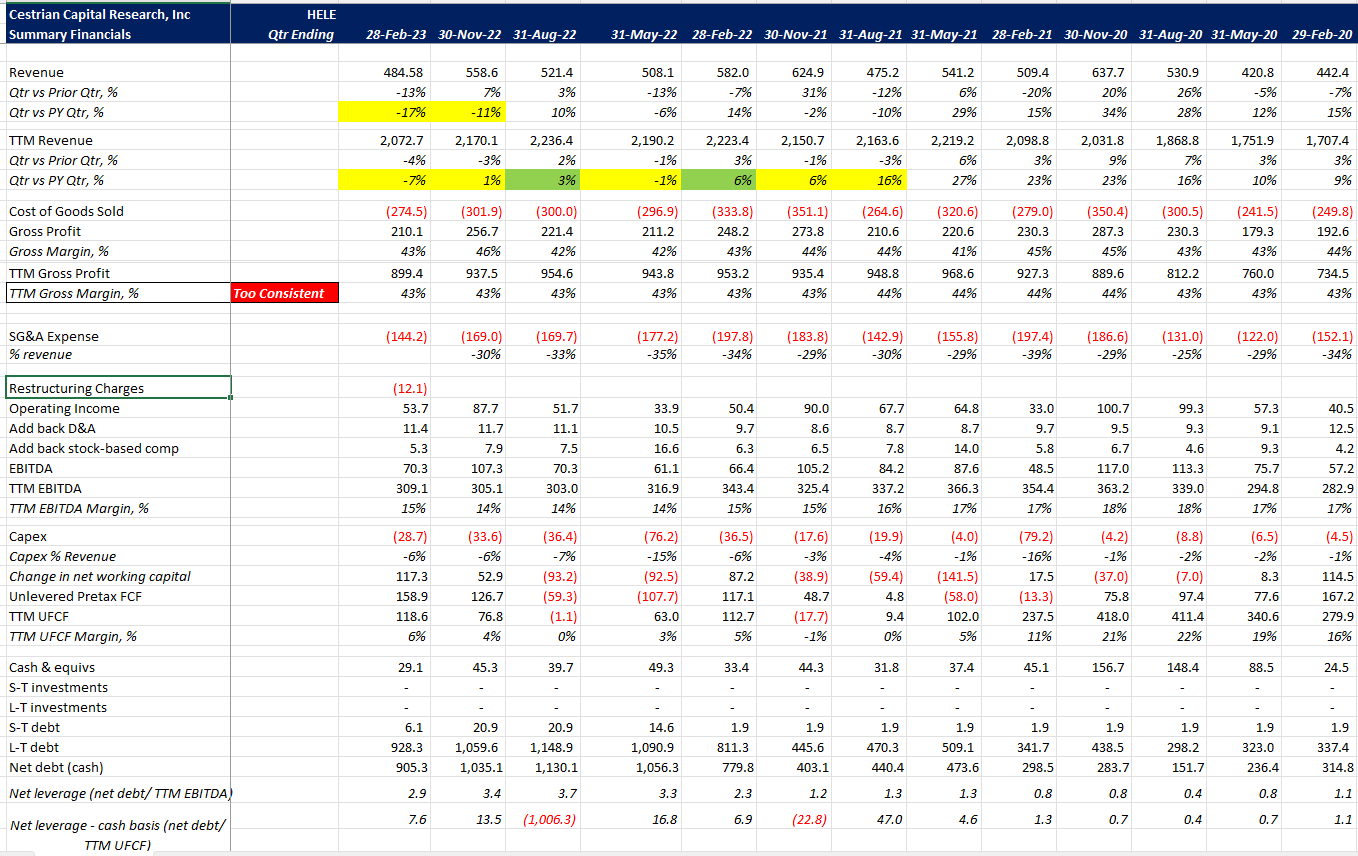

Now here's HELE.

HELE Fundamentals (Company SEC filings, YCharts.com, Cestrian Analysis)

{kind=link}

Oops. Revenue growth declining, cash flow margins barely positive, leverage increasing not decreasing. Oh and did we mention no management team with any experience of running a leveraged rollup?

Another couple nuggets for you.

TTM unlevered pretax FCF for the 12 months ending February 2023 was a little under $120m. Fully $100m of that was driven by inventory depletion, ie., selling stuff out of the stock room and not refilling the stock room. That's obviously not sustainable.

Looking at cash flow another way, in FY2/23, cash flow from operations was +$208m. The company spent -$319m in "capex and intangible asset expenditures," acquisitions net of cash acquired, and net of minor receipts from disposals. So the core business - because remember this is a rollup, and acquisitions are core business - produced negative $111m of cash flow last year. As a reminder, this company has gross outstanding debt of $934m and gross cash of $29m. In order to keep the lights on, the company drew down a net $107m from various financing sources, principally term loans and revolvers. So this company lives and dies by its ability to draw credit. In case you hadn't noticed, we're in a tightening credit environment, and HELE isn't what you would call an investment grade issuer.

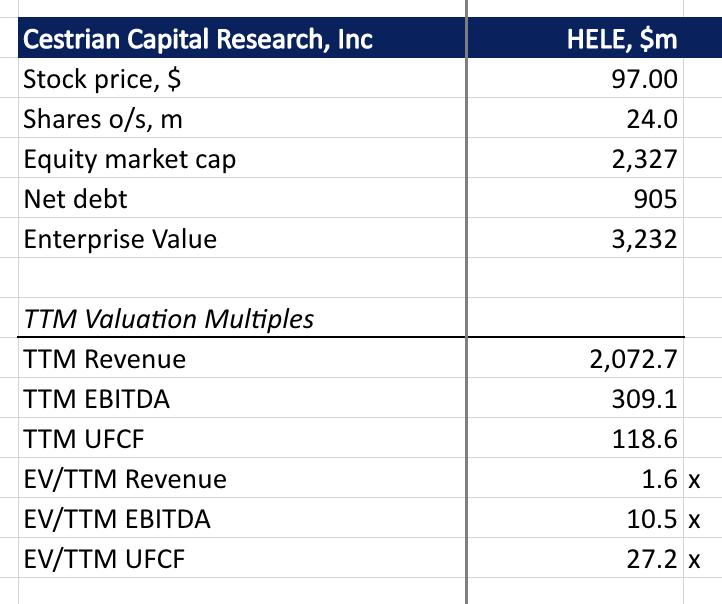

Despite all this, the market is still asking you to pay 27x TTM unlevered pretax FCF for this thing. As a reminder, a few months back you could have bought Meta Platforms ( META ) stock for under 7.5x TTM unlevered pretax FCF (see our note from the time, here ).

HELE Valuation Analysis (Company SEC filings, YCharts.com, Cestrian Analysis)

{kind=link}

Stock Chart And Price Targets

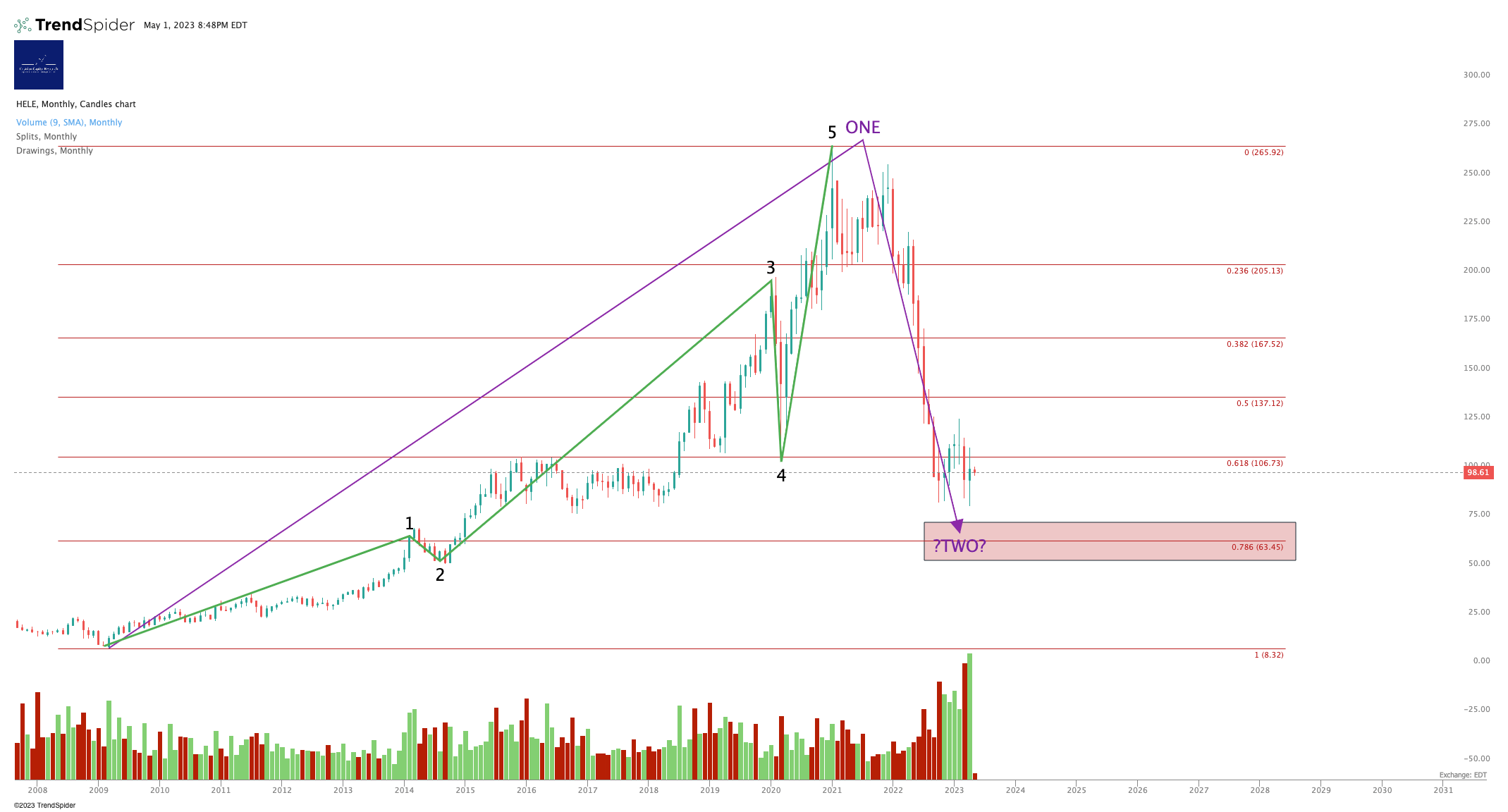

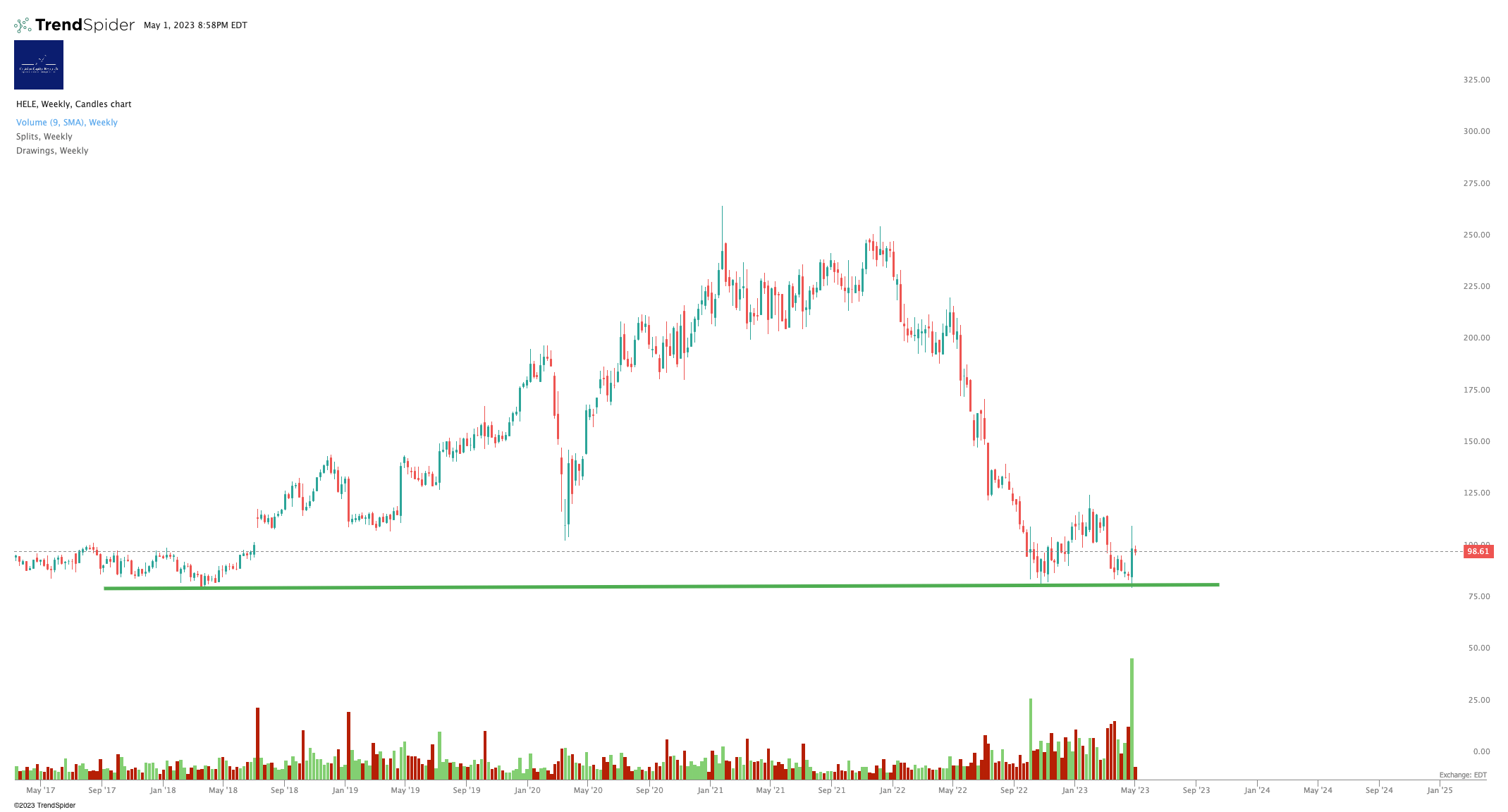

Let's see what we can learn from the stock chart. You can open a full page version for easier reading by clicking here .

{kind=link}

A great many stocks have found support lately after a huge selloff - if you look at Intel (INTC), Netflix (NFLX) and others they have all plunged to the 78.6% Fibonacci retracement of a prior large Wave 1 up. We think that this pattern may repeat at HELE. Here's how we think about price targets for a short position.

1 - Jackpot Case. The company defaults on its credit facilities, lenders accelerate, equity crushed, stock is worth single digit dollars. Let's call that an 80-90% drop from here. This does happen sometimes - witness Silicon Valley Bank (SIVB) and Signature Bank of New York ( OTC:SBNY ) and for that matter First Republic Bank ( FRC ) - but it's probably wise not to bet the farm on this as your most probable outcome.

2 - The Intel Case. INTC just found support at the 78.6 retrace of its huge move up from the 2009 lows to the 2021 highs. If HELE were to do that - not because it's analogous to INTC, merely because this kind of retracement and then support is more common than one might at first think - then we may see HELE fall to the mid-$50s/share, or around a 45% gain from here if you take a simple short equity position and ignore borrowing fees etc.

3 - The Chicken Bear Case. Horizontal support for HELE stock lies at around $80 as can be seen below .

{kind=link}

We can call that 20% ish from here.

Risk management? If the stock gets much above say $105-110 then we may see a sustained short squeeze. Renowned short seller Marc Cohodes is beating the drum for this short idea and the noise reverberating through Twitter from the Cohodes diaspora is loud indeed - an easy enough target to squeeze long if someone is so minded. That's likely a short term strategy but it doesn't mean nobody will try it. So if you're considering a short position here, consider a buy-stop in that low 100s zone.

Distribute rating.

Cestrian Capital Research, Inc - 1 May 2023.

For further details see:

Helen of Troy Is A Case Study In Leveraged Rollups Hitting The Skids