HELE - Helen of Troy: Near-Term Uncertainties Keep Me On The Sidelines

2023-05-06 08:52:20 ET

Summary

- Near-term uncertainties about lower consumer discretionary spending are expected to remain a concern for revenue growth.

- Margins are expected to improve due to moderating freight and commodity cost and cost-saving initiatives.

- However, recent churn at the top management level adds to some uncertainty around the execution of cost-saving initiatives.

- Valuation is lower than historical averages.

Investment Thesis

Helen of Troy Limited (HELE) is expected to experience ongoing pressure on revenue growth due to softening consumer demand for discretionary products. Although inventory destocking is easing, consumer buying patterns are likely to continue getting adversely impacted from rising interest rates and increasing prices.

On the margin front, the company is expected to see some improvement as commodity and freight costs are moderating. The company has also launched cost-saving initiatives under Project Pegasus. However, there are some uncertainties surrounding the execution of these cost-saving initiatives due to the continuous changes at management levels. While the stock is trading at attractive valuations, I prefer being on the sidelines till revenue begins to recover and the success of new management in the cost-saving initiatives takes hold. Hence, I have a neutral rating on the stock.

Q4FY23 Earnings

Helen of Troy announced recently reported better-than-expected results for the fourth quarter of fiscal 2023. The company's revenue decreased by 19.8% organically or by 16.7% year-over-year (YoY) on a reported basis to $485 million, exceeding the consensus estimate of $457.7 million. Although adjusted earnings per share declined by 19.9% YoY to $2.01, it surpassed the consensus EPS estimate of $1.88. The adjusted operating margin grew by 130 basis points YoY to 13.8%. The decline in revenue was driven by lower demand for discretionary products, while margins increased due to favorable outbound freight costs and lower marketing expenses. Adjusted EPS declined due to lower adjusted operating income and higher interest expense.

Revenue Analysis and Outlook

In my previous article on Helen of Troy in March, I suggested remaining on the sidelines due to uncertainties around tight consumer discretionary spending, which was a concern for revenue growth. Since then, the company has reported its fourth-quarter fiscal 2023 earnings, which revealed similar dynamics.

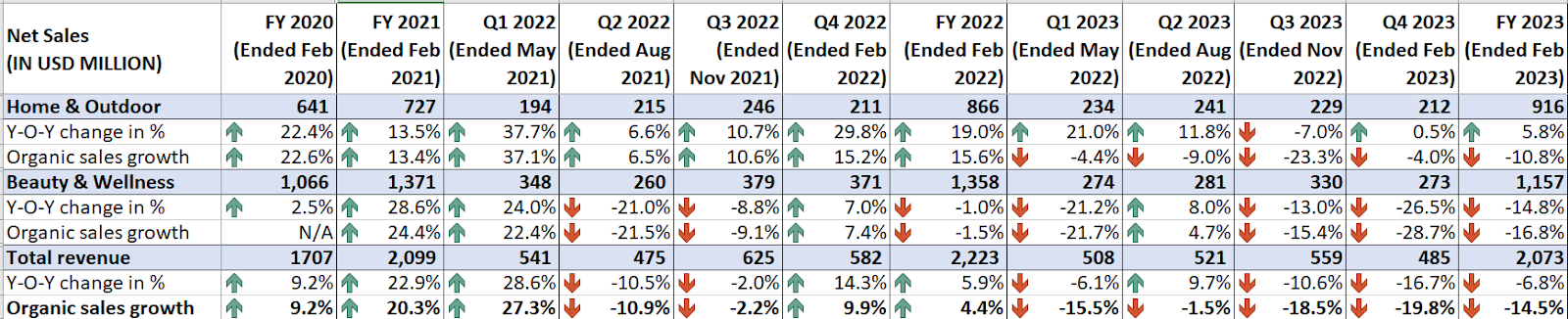

During the fourth quarter of fiscal 2023, lower consumer demand for general merchandise and discretionary products in an inflationary environment continued to impact sales negatively, resulting in a 16.7% YoY decline in revenue to $485 million. Excluding a 3.4 percentage point benefit from acquisition synergies and a 0.4 percentage point FX headwind, sales declined by 19.8% YoY on an organic basis due to retailer inventory destocking as a result of lower sell-through.

HELE's Historical Revenue (Company Data, GS Analytics Research)

{kind=link}

Looking ahead, uncertainties surrounding consumer behavior are expected to continue to pose a challenge in the coming quarters. The discretionary product category is expected to suffer due to high-interest rates and continuous price increases of consumer staple products, resulting in consumers delaying purchases of non-essential discretionary items in an inflationary environment. This is likely to lead to lower demand for HELE's product category, and I anticipate that the macroeconomic environment should remain unfavorable for the company's sales growth in the near term.

Furthermore, the company's market share performance across its product portfolio is currently mixed. While there are positive share gains in a few brands like OXO and inhalants and air purifiers, there are also categories that are losing market share. The Hydro Flask brand, which has been a good growth driver in the past, is seeing softness due to consumers shifting preference to tumblers from water bottles, resulting in market share loss for the category. HELE is also seeing softness in the hair appliance and kitchen appliance categories due to lower discretionary spending. This mixed market share performance, coupled with a slowdown in discretionary sales, adds further uncertainty around sales growth in the future.

One positive point that could help HELE partially offset the lower demand environment in FY24 is the easing of inventory destocking-related headwinds. Inventory destocking was a major headwind in FY23, and after the last few quarters of significant destocking, I believe the inventory levels are much more closely aligned to end-market demand. So, unless there is another leg down in demand, this would be one less headwind looking forward.

Overall, the revenue outlook for FY24 is slightly negative, with the lower consumer discretionary demand being a headwind, but the Y/Y improving inventory situation partially offsetting it.

Margin Analysis and Outlook

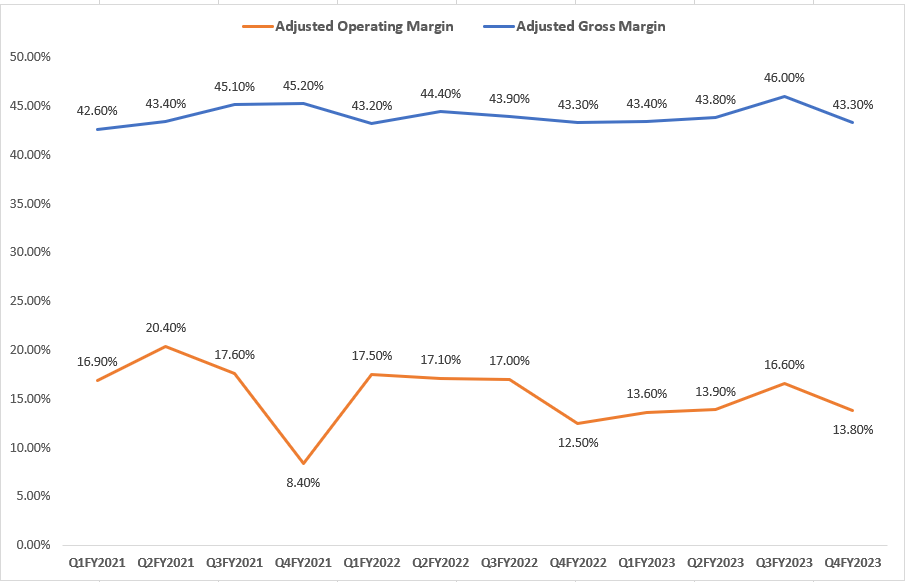

The company's margins were negatively impacted in the last quarter due to inflationary input and labor costs, as well as sales deleverage. However, HELE was able to offset them through price increases, reduced marketing expenses, and lower outbound freight costs. As a result, the company achieved a flat Y/Y adjusted gross margin of 43.3% and a 130 bps Y/Y increase in adjusted operating margin to 13.8%.

HELE's Historical Adjusted Gross Margin and Adjusted Operating Margin (Company Data, GS Analytics Research)

{kind=link}

Looking forward, while volume deleverage should be a concern, the cost environment is turning positive with freight and commodity cost coming down, which should help margins. The company has also launched "Project Pegasus," a three-year initiative to reduce costs in which the company is targeting $75 mn to $85 mn in cost savings by 2026. While management's plans are definitely impressive, the recent news about CFO Matt Osberg's departure and CEO Julien R. Mininberg's retirement makes me somewhat concerned about the execution of these cost-saving initiatives. So, I would use a "wait-and-watch" approach to get a better sense of the benefits of Project Pegasus initiatives.

There are a few cost headwinds as well in FY24. HELE is expected to incur higher depreciation costs of ~$12 million related to the company's new distribution center in Tennessee, which has been operational since early this fiscal year. There is also an incremental ~$27 million in higher annual incentive compensation costs for FY24.

I believe the company's margin outlook is mixed with moderating inflation and Project Pegasus helping whiles sales deleverage and some incremental costs being a headwind.

Valuation and Conclusion

HELE is currently trading at an 11.35x FY24 consensus EPS estimate of $ 8.73 and a 9.86x FY25 consensus EPS estimate of $10.05, which is significantly below the historical 5-year average forward P/E of 16.75x. However, my concerns about the company's growth prospects remain due to near-term revenue growth headwinds from lower consumer discretionary spending. Additionally, the continuous changes in management raise concerns about the execution of cost-saving initiatives. Therefore, I would remain on the sidelines and closely monitor the new management's approach toward executing cost-saving initiatives. I continue to maintain a neutral rating on the stock for now.

For further details see:

Helen of Troy: Near-Term Uncertainties Keep Me On The Sidelines