HELE - Helen Of Troy: Triumphs Over The Bears Further Progress Necessary

2023-07-11 06:49:35 ET

Summary

- Helen of Troy, seller of a diversified portfolio of owned and licensed leading brands, including Osprey and Vicks, soared over 18% following their first fiscal quarter results.

- The gains were attributable in part to better-than-expected profitability.

- Expansion in margins demonstrated that their operational restructuring strategy, known as Pegasus, is progressing as expected.

- Strength in key brands cuts against bearish views that the company is at increasing risk of "brand irrelevancy".

- Though results were mostly positive, I believe more progress needs to be made in certain aspects of the business.

In its battle with the bears, Helen of Troy ( HELE ) is proving triumphant. To ultimately prevail, the company will likely need to show that it can grow sales in key product classes.

Why Did HELE Soar Following Results?

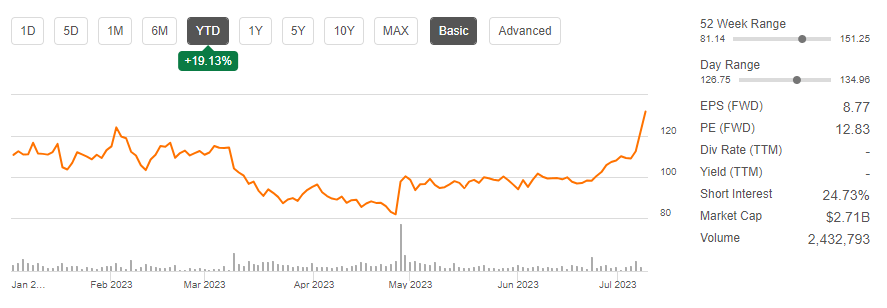

HELE, the seller of a diversified portfolio of owned and licensed brands, such as Osprey, Vicks, and PUR, among others, impressed markets with margin strength and quarterly sales in-line with expectations . The excitement led to shares up over 18% at the close of the trading day. The stock is now up 19% YTD, though still down nearly 30% over the past year.

{kind=link}

Seeking Alpha - YTD Gains Of HELE

Why Is HELE Short Interest High?

The stock has been pressured by a high degree of short interest, most notably from Hedgeye , who views the company’s brands as “semi-relevant” and at increased risk of market share loss to premium competitors.

This looks like a tough sell to investors who listened in to CEO Julien Mininberg, as he reported on Osprey, a longtime leader in technical and everyday packs who HELE acquired at the end of calendar 2021.

In Q1 , Osprey expanded their number one position in the U.S. backpack industry due to accelerated demand for travel and HELE’s improved supply position to meet this demand. Their backpacks are also consistently among the top-rated and most recommended hiking/camping backpacks. I, myself, utilize the pack for my outdoor adventures.

HELE also reported that their utensils-focused brand, OXO, gained share during the period. This came even as customer spending trends have shifted to other priorities. More innovative product offerings and added distribution contributed to these gains. Despite the gains, I view OXO as more susceptible to the bear case.

Though total sales remain above pre-pandemic levels, HELE does face stronger competitive threats from companies, such as Cuisinart and Weber, whose grilling offerings were ranked as “best overall” and “best value” by Food and Wine Magazine. As one would expect, their products, accordingly, are commanding an increasing share of retail shelf space. This in turn is also created headwinds in HELE’s club channel programs, which are on the decline.

{kind=link}

Their offerings of Hydro Flask insulated beverage bottles also are lagging to the growing popularly of travel tumblers, a type of bottle which is less addressed by Hydro. The hype surrounding the Yeti-offerings is a more pressing threat to HELE, in my view. HELE recently introduced a new bottle in response, but it’s too early to determine its prospects.

The ramped up efforts to better compete is putting pressure on adjusted operating margins in the respective segment as HELE increases inventory reserves and steps up marketing to move inventory.

HELE Margin Expansion Despite Competitive Threats

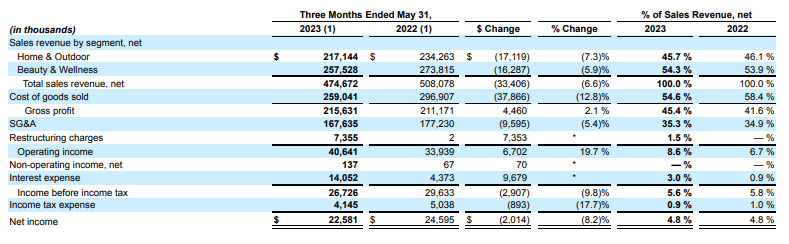

In Q1, the decline in margin was limited to just 30 basis points (“bps”), as favorable customer mix and freight provided positive leverage to increases elsewhere. Adjusted operating margins were also higher on an overall basis by 30bps due in part to strength in their Beauty & Wellness division, whose margins expanded 80bps.

The positive developments in profitability cuts against another bear case on the stock, which pertains to uncertainty surrounding the execution of their restructuring program, known as Project Pegasus (“Pegasus”), in the face of a difficult macroeconomic environment.

A key intention of the program is to expand operating margins. HELE appears to be moving in the right direction on this, even if they are somewhat behind in their Home/Outdoor segment. Aside from the expansion in adjusted operating margins, the company also reported a 380bps improvement in gross profit margins.

Another goal of Pegasus is to increase cash flows and improve operating and organizational efficiency. A more normalized inventory environment is helping in these efforts. Inventory balances, for example, were down over +$20M on a sequential basis. This keeps HELE on track to reduce overall inventory levels to sub +$400M by the end of the fiscal year.

Combined with other working capital improvements, the current period inventory reduction led to +$121M in operating cash flows and just shy of +$110M in free cash flows during the period. As cash flow continues to expand, HELE is then expected to further reduce their net leverage ratio to a target of between 1.85x and 2.0x by year end.

Is HELE Stock A Buy, Sell, Or Hold?

Outperformance in notable brands, such as Osprey, as well as competencies in executing on Project Pegasus adequately push back against bearish takes on the stock. Furthermore, just 25% of the savings from Pegasus is expected to be realized this fiscal year, with the largest benefit expected in fiscal 2025. This provides further room for HELE to run in this regard.

Leadership transition , however, does create inherent uncertainties. And despite strength in select brands, others within their home/outdoor unit are viewed to be more exposed to the competitive landscape. While more time is needed to determine the success of HELE’s new Hydro Flask offering, I don’t believe it will hit the mark with consumers. Likewise, I expect continued weakness in their club channel programs.

Current consumer spending priorities amplify these challenges. And though the improvement in overall margins is promising, total sales are still expected to decline. A bullish take on the stock would entail better-than-expected sales results in future periods. Markets, nevertheless, are likely to reset their expectations on the stock. Judging by the post-earnings spike in the share price, there was already a head start on this.

At less than 13x forward earnings, investors could do worse in finding value in the current markets. While the stock could, indeed, continue to rise on a reversal in sentiment, I believe investors would be better off remaining on hold.

Though Helen of Troy triumphed over the bears in Q1, the fiscal year has just begun, and the company still has more to prove.

For further details see:

Helen Of Troy: Triumphs Over The Bears, Further Progress Necessary