ZBRA - Here Is Why I Keep Buying Zebra Technologies Even After Bad Q3 Results

Summary

- For the first time in eight quarters, Zebra missed earnings.

- The management addressed the issues in the quarter and showcased its high quality.

- FCF continues to be declining rapidly, but I believe these are outliers and will change in the coming years.

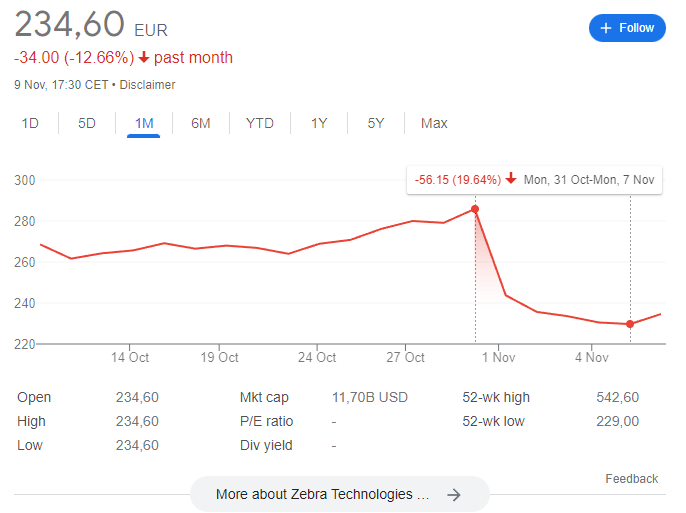

Zebra Technologies (ZBRA) stock crashed about 15% after reporting Q3 and fell an additional 5% in the following days. The stock is now around its 52-week low at $226 and down 63% from its highs last year. I believe this is just a short-term issue and I am encouraged by management's reaction to the problems. I remain invested in Zebra and bought the dip.

{kind=link}

Earnings recap

Zebra reported non-GAAP EPS of $4.12, missing by $0.41 and $1.38 billion in revenues, missing by $100 million. The company reported a declining revenue of 4% YoY versus its internal guidance of 2-4% positive YoY growth. These by no means are great earnings and goes against Zebra's good track record of beating expectation:

According to Seeking Alpha , the company beat EPS 7/8 times over the last eight quarters and revenues 7/8 times. This was the first time since Q1 2020 that the company didn't meet expectations.

Despite missing expectations, the company did perform well in the Asia Pacific (20% growth) and Latin America (10% growth), as well as its Asset Intelligence & Tracking business (AIT, 12.4% growth). SMB customers also performed much better than large enterprises, and this could provide a headwind in the future as SMBs usually adapt slower to macro changes.

The decline primarily occurred in the mobile computing segment, with data capture, printing, supplies, services and software growing in the quarter.

Addressing the issues

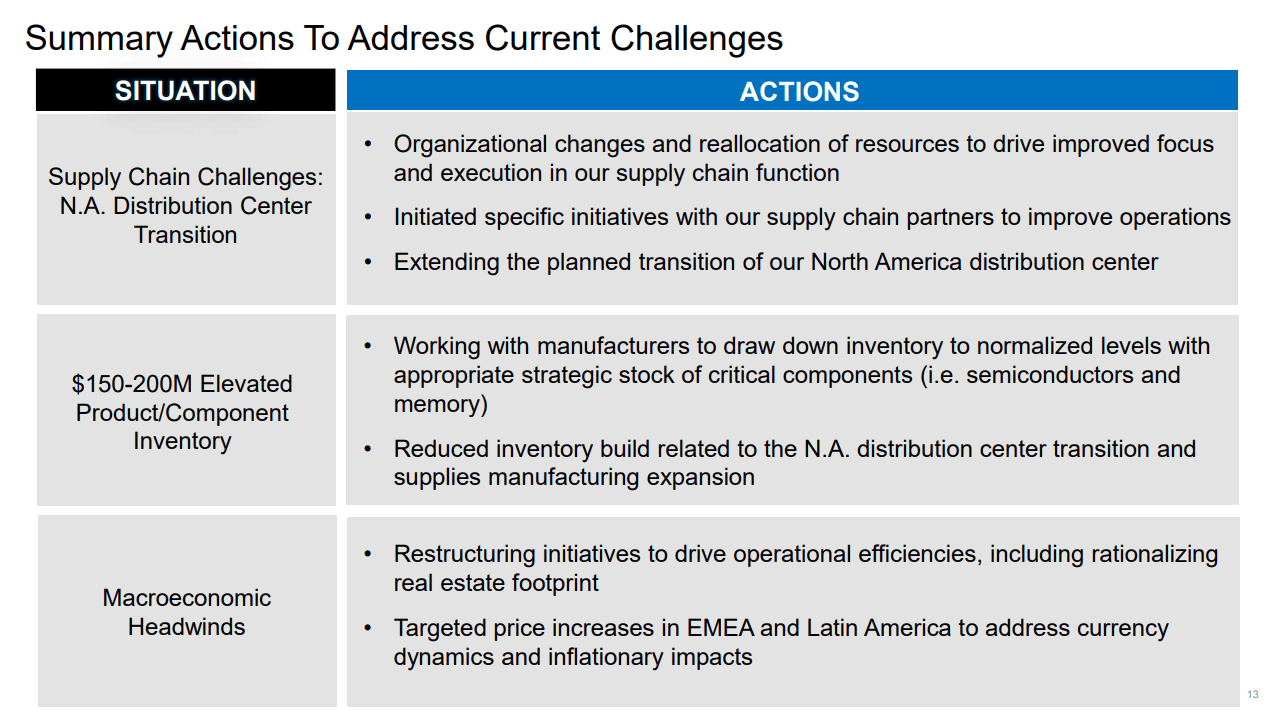

I am invested in Zebra Technologies because of its excellent management team around long-time CEO Anders Gustafsson. Management decided to point out the three main challenges that plagued Q3 and address their actions to resolve them. This is again a sign of excellent leadership. Many others would have just blamed it on macro and swept it under the rug. Not Zebra! Instead, they address their first hiccup in eight quarters directly.

{kind=link}

Supply Chain Challenges

The first issue is the supply chain challenges around its new Distribution Center in the Chicago area and the persisting component shortage for specific products. Due to both of these issues, the company did not manage to fulfill all orders it received, which led to lower throughput late in the quarter. Some larger customers also deferred some orders, splitting them into two parts, for example:

One is an example of what we’re seeing is a large customer who will take an order that they would have perhaps placed in Q3 or early in Q4. And now telling us we’re going to split that order, and we’re going to take 80% of it now and 20% of it later in 2023. That’s an example of the type of thing we’re getting.

Additional headwinds are tough comps in NA and EMEA, where the company saw some large mobile computing deployments last year and Russia's suspension, which cut into the results.

The new Distribution Center in DC saw problems with the transition and as a result, the company ramped back its Texas facility to bridge this transition time. The company streamlined the organization, promoted a new supply chain leader to lead global operations & the supply chain and pushed some functions and responsibilities out of the supply chain to get a better focus and accountability on the issues at hand. The following quote puts the level of supply chain issues into perspective:

But again, the Texas facility is nearly staffed to full capacity and we’ve had a really nice recovery here in deliveries in October. Just as context, we’ve shipped out nearly $200 million more in October than we did in the month of July, which is giving us both confidence in the performance of the DC as well as confidence in the Q4 guidance.

Nathan Winters, Zebra Technologies Q3 Earnings Call

Elevated Product/Component Inventory

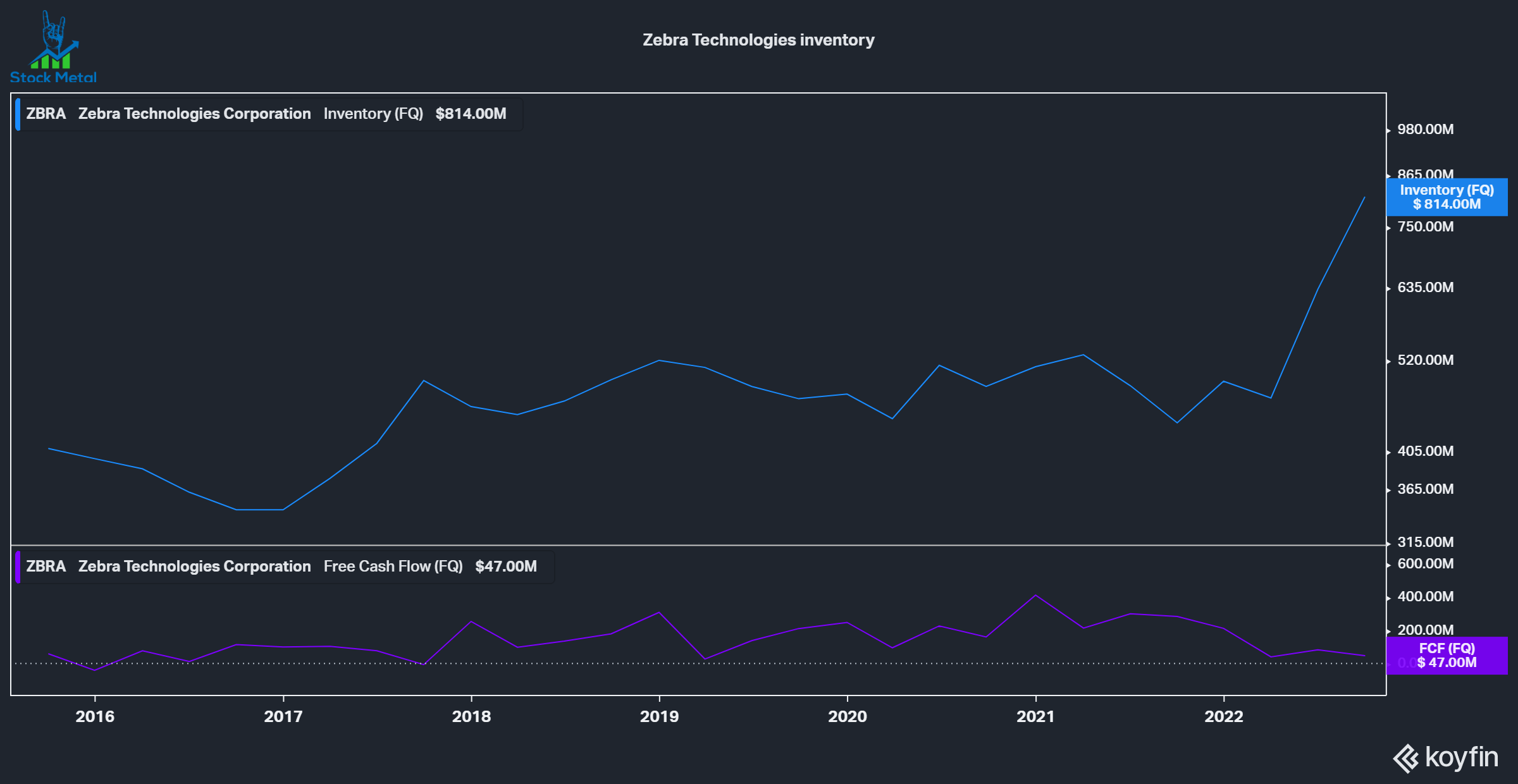

Many companies are plagued with bloating inventories in 2022, with some companies like Stanley Black & Decker ( SWK ) losing billions in cash in a single quarter ( read my article about SWK here ). Zebra is no exception and as you can see in the graphic below, inventory skyrocketed to $814 million in the last two quarters, generating around $150-200 million of elevated product and component inventories. The problems with the NA Distribution Center transition also significantly contributed to this issue. The company is now actively working with manufacturers to draw this inventory down through 2023 to normalized levels with an appropriate safety stock for critical components. The company has to walk a thin line between having a low inventory level but also being able to offer customers the solutions they need.

{kind=link}

Zebra Technologies Inventory (Koyfin)

Macroeconomic Headwinds

The company started to see a slowing in demand since late Q3, with demand and the order pipeline generally remaining healthy. This can already be seen in the deferred projects by some large customers mentioned earlier in this article. As a response, the company is looking to rationalize its real estate footprint and drive operational efficiencies, as well as raising prices in EMEA and LATAM, where currency and inflation are impacting results.

An ERP system for automation?

CEO Gustafsson shared this quote, which I liked a lot:

I’ve talked about how we be lieve that our solutions are now more like, say, an ERP implementation, it’s harder to dial them up and down. And I think the results from Q3 gives some credence to that expecta tion.

Zebra keeps increasing its switching costs with companies by upselling them into new solutions. The company can do that due to its growing portfolio of solutions and services, driven by internal reinvestment and inorganic bolt-on acquisitions. I look forward to seeing the ERP system expand in the coming years.

I bought the dip!

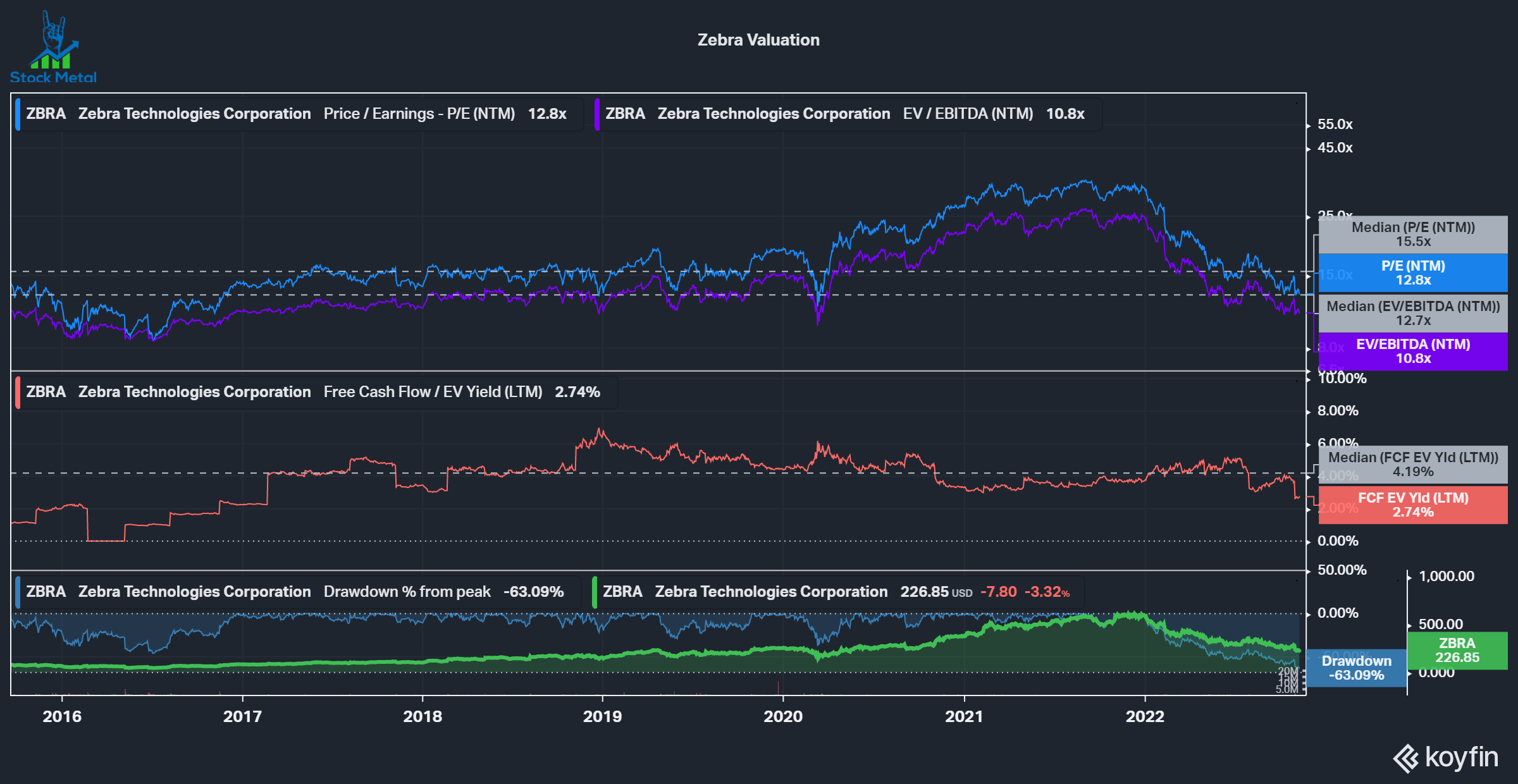

Zebra currently trades meaningfully below its median PE and EV/EBITDA ratio, but it is looking quite expensive on an FCF yield. I do not see this as an issue, though, because historically, Zebra converted at least 100% of its earnings into Free Cash Flow. This year is an outlier due to an extensive inventory build-up and the headwind from the $360 million settlement payment to Honeywell ( HON ), which is paid in increments for the last two quarters and into the following quarters. Management demonstrated its long-term thinking and quality by addressing these issues head-on in this earnings report without trying to find a way to blame others. This is the type of management I want to trust my money with, and I now hold 6% of my portfolio in Zebra Technology.

{kind=link}

For further details see:

Here Is Why I Keep Buying Zebra Technologies Even After Bad Q3 Results