HTZ - Hertz Global Holdings Q3: Selloff Is Overdone

2023-11-01 17:34:10 ET

Summary

- HTZ remains a buy at the current valuation due to what I believe is an overdone stock sell-off.

- HTZ reported strong 3Q23 results with robust demand and favorable supply situation, supporting positive top-line growth.

- Near-term challenges related to increased EV collision costs may impact EBITDA growth, but the longer-term demand-supply dynamics remain favorable.

Overview

My recommendation for Hertz Global Holdings ( HTZ ) is a buy rating, as I believe the stock sell-off is overdone, making the current stock price attractive from a risk/reward perspective. The demand-supply dynamic remains favorable, and I believe the EV-related cost issue does not impair the medium-term positives. Note that I previously gave a buy rating for HTZ as I believed the setup for the business was very positive. There is a strong likelihood of robust utilization due to the rebound in demand, which, coupled with the supply situation, should contribute to EBITDA growth in FY24.

Recent results & updates

For 3Q23 , HTZ reported $2.7 billion in revenue, $270 million in adjusted pre-tax income, and $0.70 in adjusted EPS. There was a 15.6% increase in rental days that drove revenue in the Americas segment to $2.17 billion, even though pricing fell by 8%. As a whole, the Americas segment generated $302 million in EBITDA. International reported $531 million in revenue, with an increase in rental days of 18% offsetting a larger price drop of 12%. The division's EBITDA was $109 million.

The stock has exhibited an opposite trajectory compared to my prior expectations, primarily attributable to the anticipated decrease in third-quarter EBITDA. This decrease is likely a result of heightened collision and repair expenses associated with the electric vehicle segment of HTZ's operations. Specifically, I believe that the Americas segment EBITDA has been impacted by the higher-than-expected vehicle interest expense due to the higher interest rates, as well as the higher direct operating expense due to higher Tesla repair costs. During the 3Q23 conference call, the management has acknowledged my belief, specifically regarding the relative immaturity of Tesla car and parts in the market compared to other well-established entities that have been operating for several decades..

There is an aftermarket of parts that is there, that is less mature, obviously, in the context of Tesla and so, I suspect as implied by your question. That margins will improve, and this issue will improve as we look to diversify. From: 3Q 2023 earnings call

One might recall that EV was a strategy that management had been promoting, which has supported the stock narrative to a certain extent. From a numerical perspective, HTZ has grown the number of EVs as a percentage of the total fleet to 11%, and Tesla is a huge chunk of it. However, the matter of fact is that EV collision costs are much more expensive , which is likely to eat into the operating expenses of HTZ as EVs become a larger part of the pie. I believe this dynamic is likely to cause a lot of uncertainty as near-term EBITDA might become more volatile, especially with management suddenly pulling the brakes on this EV strategy .

Yeah, sure. So first on the EV question, recognize that the total EV fleet is about 11% of the total fleet and Tesla's represent about 80% of that. And so, there's quite a bit of the cost element that relates to the Tesla's, as opposed to others. From: 3Q 2023 earnings call

That said, objectively, I think the stock underperformance is overly extended. Certainly, there are merits to the notion that EV-related cost issues could persist for the next few quarters, ultimately weighing on EBITDA growth and margins, with vehicle funding costs going up as well. However, if we look into 2024 and beyond, I still think the demand-supply dynamic setup remains attractive. As I discussed previously, below are two quotes from the HTZ 2Q23 earnings call that remain relevant and important for the near future.

When you look at analyses of 2024 in terms of OEM production, it's marked to be only about 2% higher than 2023. So, yes, cars will be freer, if you will, than where they were in the depth of COVID, but not nearly back to where pre-pandemic levels are. from: 2Q 2023 earnings call

But I think overall, very strong demand of which we're going to find other channels to feed it even more and continued strength in price, again, in a very stable rate environment relative to what we otherwise might have seen or cynically thought would come, again, with a slightly looser availability of cars and so forth. From: 2Q 2023 earnings call

The important takeaway is that the demand environment has remained strong and the industry remains rational (as seen from the supply situation). This should continue to support continued strength in RPD and ultimately top-line growth. This gives confidence that the EBITDA margin at the fundamental level (excluding the impact of elevated EV collision repair costs) should be well supported.

Demand in the quarter was strong across our business with leisure corporate and rideshare volumes all up year-over-year, demonstrating the continued strength of the traveling consumer. From: 3Q2023 earnings call

Valuation and risk

{kind=link}

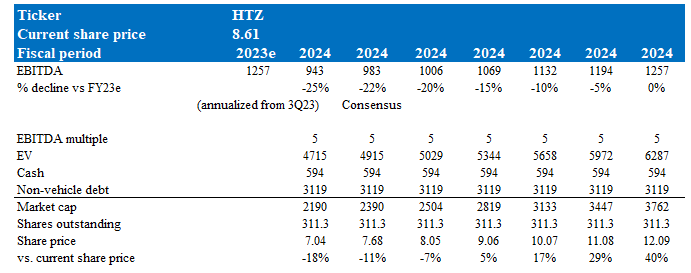

Using a similar approach as I did previously, my model above aims to illustrate the risk/reward situation given the major de-rating in share price over the past few months. The key assumption is: how much will the EV-related cost pressure impact EBITDA in the near term? I use a range of -25% to 0% and a 5x forward EBITDA multiple to illustrate the ups and downs. The reason for using -25% as the worst-case scenario is to capture the potential for HTZ to miss consensus estimates, and the best case at 0% is to be conservative. Previously, I modeled HTZ to trade at 6.5x forward EBITDA, a premium to its peer Avis Budget Group ( CAR ), because of my positive EBITDA outlook. Given the circumstances, I believe HTZ is likely to trade at a discount (CAR trades at 5.9x) in the near term, given the uncertain EBTIDA outlook.

Remember that demand remains strong and the supply situation is favorable for HTZ; as such, it is unlikely we will see a sustained decline in EBITDA growth. I suspect this EV-related cost pressure will last 1 or 2 quarters before things rebound. Given that consensus is expecting a 23% decline in EBITDA (based on an annualized FY23 EBITDA figure), I think that might be a little too harsh. If HTZ were to perform better than expected, I expect the stock sentiment to turn positive, which will drive the stock price up.

However, the risk is clear here. If the EV-related cost pressure blows up bigger than I expected, the stock could see further de-rating, riding on the already negative sentiment that is engulfing the stock. Even though the demand-supply situation is positive, investors are unlikely to abandon the stock until sentiment turns better.

Summary

In summary, my recommendation for HTZ remains a buy, despite the recent stock sell-off. The decline in stock price is, in my view, an overreaction to near-term challenges related to increased EV collision costs. While these challenges may impact EBITDA growth and margins for a few quarters, the longer-term demand-supply dynamics appear favorable. HTZ reported strong 3Q23 results, and the demand environment remains robust, particularly in leisure, corporate, and rideshare segments. The industry's rational supply situation and ongoing strength in rental pricing support positive top-line growth. I believe that HTZ's EBITDA margin should remain strong at a fundamental level, excluding the impact of elevated EV collision repair costs. While there are risks associated with the uncertain near-term EBITDA outlook, there is potential for a positive sentiment shift if HTZ outperforms expectations.

For further details see:

Hertz Global Holdings Q3: Selloff Is Overdone