HXL - Hexcel: Why I Am Not Upgrading To Buy

Summary

- Hexcel Corporation results have shown significant recovery.

- Share price appreciation is running ahead of recovery, making a Hexcel Corporation buy somewhat risky.

- Big question at this point is how commercial aircraft production rates will develop in the coming years and whether that is sufficient to generate sales to get to pre-pandemic levels.

- Hexcel Corporation remains a speculative buy in my book for the long-term recovery.

I have been following Hexcel Corporation (HXL) for some years. I believe that the company has a promising product portfolio, but partially due to the pandemic value generation has been underwhelming. In this report, I explain why I am not upgrading from Hold to Buy but do see long-term value for HXL shares. I will also comment on the company’s latest earnings release.

What Does Hexcel Do?

For those not familiar with Hexcel, it might be good to provide an introduction to the company’s operations. Hexcel Corporation provides composite materials and structures. These days the reduction of greenhouse gas emissions plays an important role. Composites provide lower-weight solutions, thereby reducing fuel consumption in, for instance, cars and aircraft. Furthermore, the company provides material solutions for the wind energy market. So, with green house gas emission reductions in mind, there are significant opportunities. On each of these sectors where Hexcel could provide solutions, there are remarks to be placed, which I will do when discussing my investment view on Hexcel Corporation.

Full Year Results Show Significant Improvement

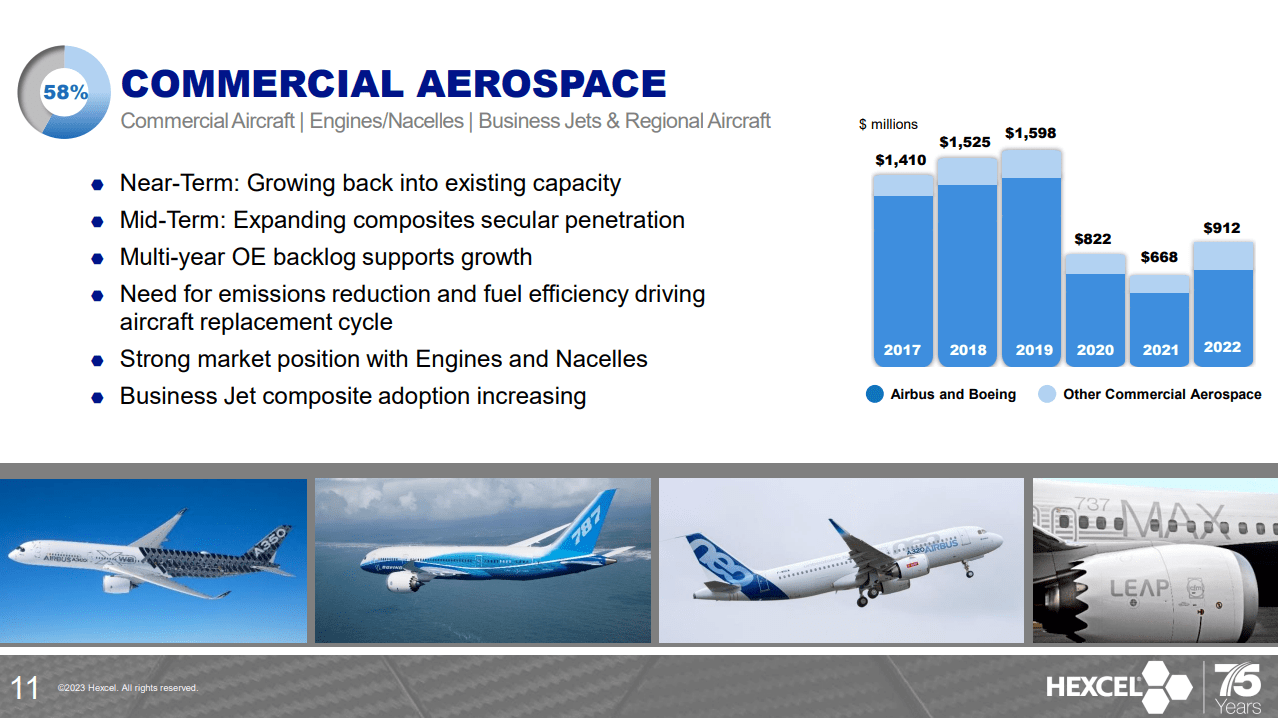

Hexcel Corporation commercial aerospace sales (Hexcel Corporation)

{kind=link}

On any normal day, the commercial aerospace segment provides the company with 70% of the revenues. However, we haven’t had a normal year since 2019. In 2019, the Boeing 737 MAX crisis sparked a reduction in the production rate. Hexcel provides the materials used to manufacture the acoustic inner barrels. While the reduction in production was significant, the relatively low shipset value and the strong production rates for other commercial aircraft programs did not lead to a reduction in revenues at the time. The subsequent year, however, was different as production of the Boeing 737 MAX was halted and the pandemic eroded demand for and the ability to manufacture commercial aircraft, and in 2021 things did not get much better.

Last year was a recovery year and we also see that in the results with a 37% increase in sales, but that recovery was less robust than desired by the industry, as supply chain issues caused major challenges in an attempt to increase production rates.

Revenues are only 57% recovered. However, year-over-year for the fourth quarter, we do see 28.7% higher net sales and 22.5% improvement quarter-over-quarter. The recovery is not as strong as the annualized improved, but that is because throughout the year sales have been increasing.

Hexcel Corporation space & defense sales (Hexcel Corporation )

{kind=link}

For the quarter, sales grew by 22% year-over-year and 16.5% sequentially and by 7% for the full year. Overall, defense and space remains a segment that provides stability with modest growth. That growth can either be driven by expanding defense budgets, as is the case now, or the introduction of new growth platforms, as we see with the CH-53K and Future Vertical Lift .

{kind=link}

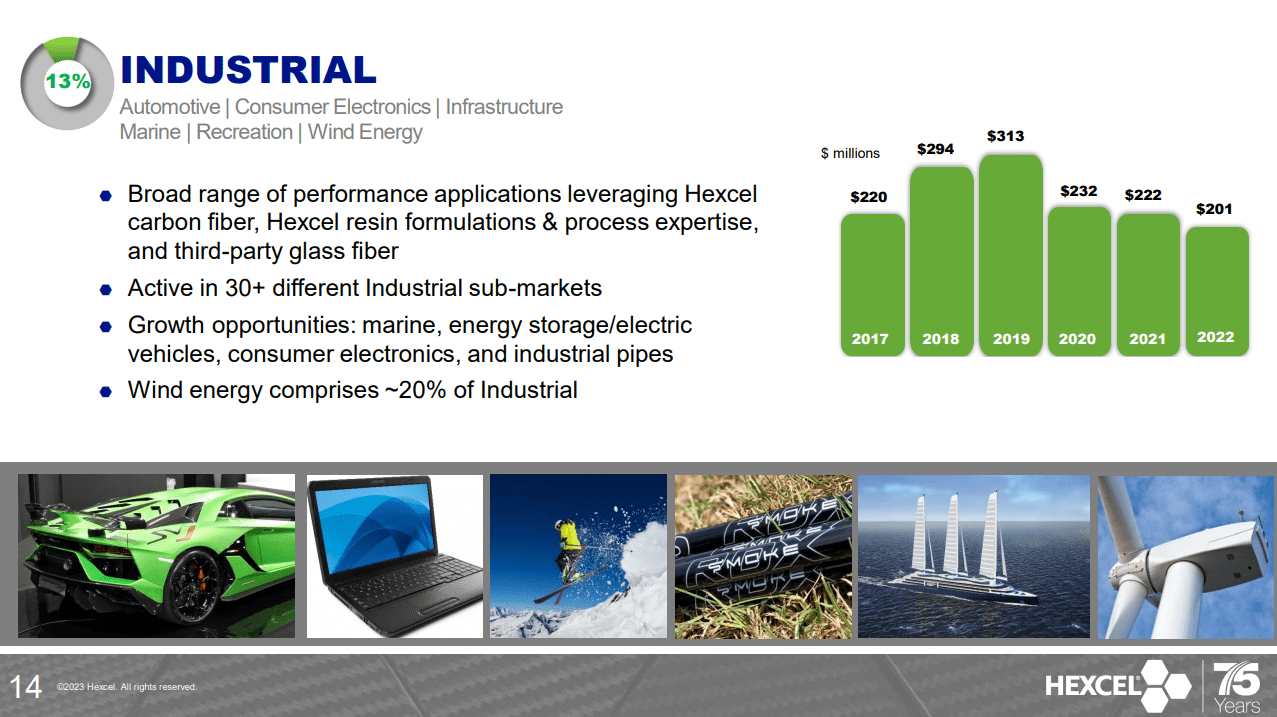

The industrial side is one that is actually rather ugly for Hexcel. The opportunities to drive a greener future are significant, but it is simply not translating. Hexcel lost supply work for Vestas, which was pivotal to the company’s wind energy business. As I pointed out last year, this is supply work we do not expect to be returning .

During the fourth quarter earnings call, this was also confirmed :

Industrial sales of $47 million were down 7% year-over-year in constant currency. Given the economic pressures, the wind energy industry has changed structurally and opportunities for our legacy glass prepreg products have limited.

Sequentially, revenues were stable, while year-over-year sales were down 15% and down 9.5% for the year, and that really is what I would call the ugly duckling in Hexcel’s business. While Industry should have a lot of growth platforms, it actually doesn’t have that growth driven by lower wind energy sales, and while automotive is a promising segment, the business is currently focused on high-end cars.

The company now states it is pivoting away from wind energy to other markets such as consumer electronics, marine, and automotive, but we are not given any kind of insights on the trajectory of those sales segments.

Why I Don’t Upgrade Hexcel Stock To Buy

{kind=link}

One could wonder with the recovery in commercial aerospace is not driving me to upgrade shares to buy. After all, we do see improvement in the results on all metrics. The reason is that shares are currently trading at $66, and at the $80 per share level prior to the MAX crisis. Adjusted EBIT is only 38% recovered and adjusted EBITDA is 52% recovered, while share prices are >80% recovered. So, it does seem that Hexcel Corporation shares have gotten ahead of themselves a bit encapsulating further recovery in 2023.

However, looking at commercial aerospace, we do see annualized effects of recovery and step-ups in production rates, but at the same time we do not see a clear path to get back to 2019 levels for the foreseeable future. Furthermore, inflation, energy costs and shipping are putting some pressure on margins, while their Industrial will remain under pressure.

For the full year, Hexcel guided for $1.725 billion to $1.825 billion in sales. Commercial sales will be around 58% of the sales at roughly $1 billion to $1.06 billon, pointing at 16% sales growth, while defense will have 29% of the pie valued at $500 million to $530 million, pointing at 14% sales growth. The Industrial segment will be around 13% of the sales, indicating $224.25 million to $237 million in sales and indicating a year-over-year growth of 18%. Had share prices not have run up significantly and ahead of earnings recovery, I would without doubt have marked shares a strong buy. It is not the case that shares have not performed well, in fact, since I last put a hold and speculative buy rating for Hexcel, its shares have appreciated by more than 20% compared to 6.5% appreciation for the broader markets.

So, I see the value, but Hexcel Corporation shares have gotten a bit ahead of the results, I believe. That creates some risks, especially since the gap from 2023 sales for commercial aerospace segment to pre-pandemic sales of $1.6 billion is one that needs to be filled, with uncertain production plans depending primarily on wide body production rates.

Conclusion: Early Bird Gets The Worm

Hexcel Corporation results showed significant improvement year-over-year, and its guidance suggests that this will continue. As a result, I believe that those that invest early on could get some very rewarding rewards on their investment.

I am tending towards marking shares a buy, but for the moment I am refraining to do so since shares prices have gotten ahead of the recovery in underlying financials quite a bit, which means that Hexcel needs to deliver. While I have little doubt they actually will, my main point of concern is how they get from their 2023 guidance for commercial aerospace sales to pre-pandemic sales, because the major components to getting back to those levels or close to those levels are single aisle production rates, for which increases have been pushed back, and wide body production increases, which are sliding a bit as well and are somewhat uncertain.

Either way, looking at what Hexcel Corporation offers to the market, I do believe that for the long term this can be an extremely rewarding opportunity. So, I am maintaining my view on Hexcel Corporation as a speculative buy with a minimum Hold rating.

For further details see:

Hexcel: Why I Am Not Upgrading To Buy